Deck 4: Appendix B: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions

Full screen (f)

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/6

Play

Full screen (f)

Deck 4: Appendix B: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions

1

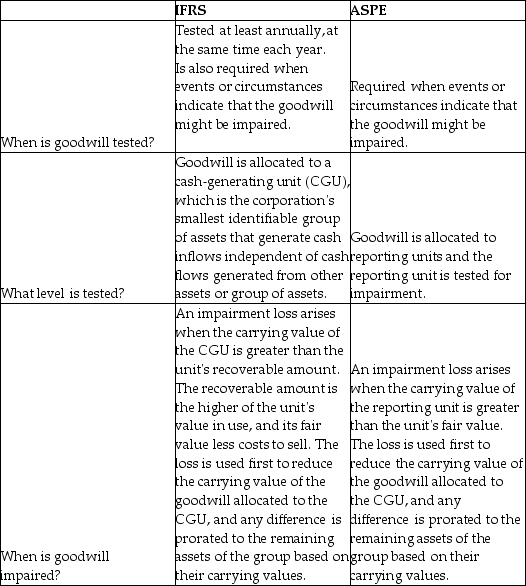

Compare and contrast the goodwill impairment test under IFRS and accounting standards for private enterprises (ASPE).

2

Proudfoot Ltd. acquired all the shares of Jacob Ltd. several years ago. In conducting its goodwill impairment test for the current year, Proudfoot has determined that there has been an impairment related to revalued assets. On Proudfoot's consolidated financial statements, where should this impairment be reported?

A)As part of profit or loss

B)As part of other comprehensive income

C)As an adjustment to retained earnings

D)As a separate amount under shareholders' equity

A)As part of profit or loss

B)As part of other comprehensive income

C)As an adjustment to retained earnings

D)As a separate amount under shareholders' equity

B

3

For private enterprises that have acquired goodwill in a business combination, how often should goodwill be tested for impairment?

A)At least once a year

B)At least once every two years

C)Whenever the parent company deems it necessary

D)Whenever there is a change in circumstances

A)At least once a year

B)At least once every two years

C)Whenever the parent company deems it necessary

D)Whenever there is a change in circumstances

D

4

How should goodwill acquired in a business combination be allocated?

A)Proportionately to assets

B)Proportionately to fair-value increments

C)To cash-generating units

D)It is not allocated.

A)Proportionately to assets

B)Proportionately to fair-value increments

C)To cash-generating units

D)It is not allocated.

Unlock Deck

Unlock for access to all 6 flashcards in this deck.

Unlock Deck

k this deck

5

Under IFRS, how often should goodwill acquired in a business combination be tested for impairment?

A)Whenever there is an indication of impairment

B)Whenever there is a change in circumstances in the business

C)At least once a year

D)At least once every two years

A)Whenever there is an indication of impairment

B)Whenever there is a change in circumstances in the business

C)At least once a year

D)At least once every two years

Unlock Deck

Unlock for access to all 6 flashcards in this deck.

Unlock Deck

k this deck

6

For private enterprises that have acquired goodwill in a business combination, which of the following is considered a change of circumstances for purposes of testing for goodwill impairment?

A)A large unfavourable income tax reassessment

B)Sale of a capital asset for a small loss

C)A major competitor has ceased operations

D)Retirement of the subsidiary's operations manager

A)A large unfavourable income tax reassessment

B)Sale of a capital asset for a small loss

C)A major competitor has ceased operations

D)Retirement of the subsidiary's operations manager

Unlock Deck

Unlock for access to all 6 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 6 flashcards in this deck.