Deck 3: Business Combinations

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

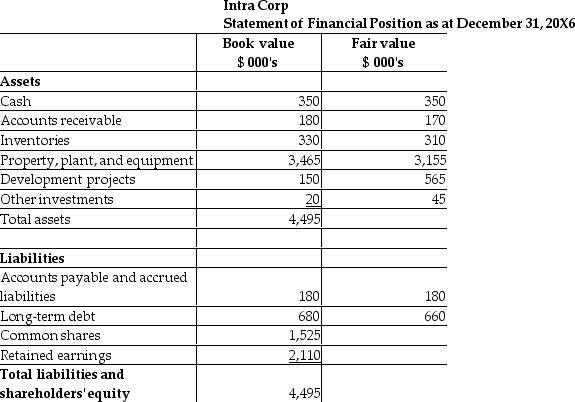

On January 1, 20X7, Falcon acquired the net assets of Intra for $3,400,000 with the issue of shares. The statement of financial position for Intra at the date of acquisition is shown below, together with estimates of the fair values of Intra's recorded assets and liabilities.

Required:

Required:

What is the amount of goodwill to be recorded for this business combination?

Prepare the journal entry that Falcon will use to record the business combination. Prepare the statement of financial position for Intra on January 1, 20X7, directly after the transaction is completed. Reconcile the book value of the retained earnings for Intra on December 31, 20X6, to its balance on January 1, 20X7. Explain any differences.

Required:What is the amount of goodwill to be recorded for this business combination?

Prepare the journal entry that Falcon will use to record the business combination. Prepare the statement of financial position for Intra on January 1, 20X7, directly after the transaction is completed. Reconcile the book value of the retained earnings for Intra on December 31, 20X6, to its balance on January 1, 20X7. Explain any differences.

Question

Question

Question

Question

Question

Question

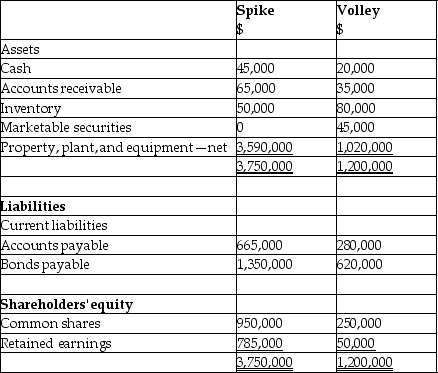

On September 1, 20X7, Spike Limited decided to buy 100% of the outstanding shares of Volley Inc. for $1,200,000, paid for with the issuance of shares. Acquisition costs for the deal totaled $30,000: $20,000 related to the issue of the shares and the remaining amount for legal, valuation, and administrative costs. All of these costs were paid in cash. In addition Spike has agreed to pay an additional $250,000 if the revenues of Volley have a 5% growth over the next two years from the date of the acquisition. It has been determined that the fair value of this contingent consideration is $175,000.

The balances showing on the statement of financial position for the two companies at August 31, 20X7, are as follows:

After a review of the financial assets and liabilities, Spike determines that some of the assets of Volley have fair values different from their carrying values. These items are listed below:

After a review of the financial assets and liabilities, Spike determines that some of the assets of Volley have fair values different from their carrying values. These items are listed below:

Property, plant, and equipment: fair value is $1,350,000

Patent: fair value is $255,000

Brand name: fair value is $135,000

Required:

Determine the amount of goodwill that will be recorded on the business combination.

Prepare the consolidated statement of financial position as at September 1, 20X7.

The balances showing on the statement of financial position for the two companies at August 31, 20X7, are as follows:

After a review of the financial assets and liabilities, Spike determines that some of the assets of Volley have fair values different from their carrying values. These items are listed below:Property, plant, and equipment: fair value is $1,350,000

Patent: fair value is $255,000

Brand name: fair value is $135,000

Required:

Determine the amount of goodwill that will be recorded on the business combination.

Prepare the consolidated statement of financial position as at September 1, 20X7.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/43

Play

Full screen (f)

Deck 3: Business Combinations

1

Dupuis Ltd. acquired Waul Ltd. through an exchange of shares. How should Waul record this on its books?

A)Waul should debit an "Investment by Dupuis" account and credit its share capital account.

B)Waul should debit an "Investment by Dupuis" account and remove all its asset and liability accounts.

C)Waul should close all its balance sheet accounts.

D)No entry should be made.

A)Waul should debit an "Investment by Dupuis" account and credit its share capital account.

B)Waul should debit an "Investment by Dupuis" account and remove all its asset and liability accounts.

C)Waul should close all its balance sheet accounts.

D)No entry should be made.

D

2

Under IFRS 3, Business Combinations, which method must be used to account for business combinations?

A)Purchase method

B)Pooling-of-interests method

C)Acquisition method

D)New entity method

A)Purchase method

B)Pooling-of-interests method

C)Acquisition method

D)New entity method

C

3

How should the cost of issuing debt in an acquisition be recognized?

A)Expensed

B)Amortized over the term of the debt

C)Deducted from the value of the debt

D)Deducted from shareholders' equity

A)Expensed

B)Amortized over the term of the debt

C)Deducted from the value of the debt

D)Deducted from shareholders' equity

C

4

After an exchange of shares in a business combination, each group of shareholders held 50% of the voting rights. Which of the following factors should be considered in determining the acquirer?

A)Head office location

B)Composition of the board of directors

C)If there are material transactions between the combining companies

D)Which company initiated the combination

A)Head office location

B)Composition of the board of directors

C)If there are material transactions between the combining companies

D)Which company initiated the combination

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

5

Able Ltd. offers to buy shares from the existing shareholders of Wei Co. at a premium price. The current management and board of directors of Wei have let the Wei shareholders know that they do not approve of this. This is an example of a(n)________.

A)open market purchase

B)hostile takeover

C)poison pill strategy

D)reverse takeover

A)open market purchase

B)hostile takeover

C)poison pill strategy

D)reverse takeover

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

6

Perez Co. acquired Roo Co. in a business combination. Perez issued new shares to Roo's shareholders in exchange for their outstanding shares. What type of share exchange is this?

A)Direct exchange

B)Indirect exchange

C)Hostile takeover

D)Reverse takeover

A)Direct exchange

B)Indirect exchange

C)Hostile takeover

D)Reverse takeover

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

7

Perez Co. plans to acquire Roo Co. Roo has substantial depreciable assets that have fair values in excess of their book values. Considering only the income tax impact, which of the following statements is true?

A)Perez would prefer to purchase Roo's assets and Roo would prefer to sell its shares to Perez.

B)Perez would prefer to purchase Roo's shares and Roo would prefer to sell its assets to Perez.

C)Both Perez and Roo would prefer Perez to purchase Roo's shares.

D)Both Perez and Roo would prefer Perez to purchase Roo's assets.

A)Perez would prefer to purchase Roo's assets and Roo would prefer to sell its shares to Perez.

B)Perez would prefer to purchase Roo's shares and Roo would prefer to sell its assets to Perez.

C)Both Perez and Roo would prefer Perez to purchase Roo's shares.

D)Both Perez and Roo would prefer Perez to purchase Roo's assets.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

8

How should negative goodwill be shown on the consolidated financial statements of the acquirer?

A)As a gain on the statement of comprehensive income

B)As a loss on the statement of comprehensive income

C)As a liability on the statement of financial position

D)As a separate amount under shareholders' equity on the statement of financial position

A)As a gain on the statement of comprehensive income

B)As a loss on the statement of comprehensive income

C)As a liability on the statement of financial position

D)As a separate amount under shareholders' equity on the statement of financial position

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

9

How should accounting fees for an acquisition be treated?

A)Expensed in the period of acquisition

B)Capitalized as part of the acquisition cost

C)Deferred and amortized

D)Deferred until the company is disposed of or wound-up

A)Expensed in the period of acquisition

B)Capitalized as part of the acquisition cost

C)Deferred and amortized

D)Deferred until the company is disposed of or wound-up

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

10

Thad Ltd. acquired 100% of the common shares of Zoe Co. for $560,000. At the time of acquisition, Zoe had the following: In this acquisition, how much goodwill has been created?

A)$0

B)$22,000

C)$35,000

D)$56,000

A)$0

B)$22,000

C)$35,000

D)$56,000

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

11

Ha Ltd. and Hee Ltd. exchanged shares in a business combination. After the share exchange, each company held the same number of voting shares. Which of the following statements is true?

A)The company with the highest net assets is considered the acquirer.

B)The companies must ask the courts to decide which company is the acquirer.

C)A number of factors must be considered to determine which company is the acquirer.

D)There is no acquirer as this is not a proper business combination.

A)The company with the highest net assets is considered the acquirer.

B)The companies must ask the courts to decide which company is the acquirer.

C)A number of factors must be considered to determine which company is the acquirer.

D)There is no acquirer as this is not a proper business combination.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

12

How should the transaction costs of issuing shares in an acquisition be recognized?

A)Expensed

B)Capitalized as part of the cost of the shares

C)Deducted in total from shareholders' equity

D)Deducted from shareholders' equity, net of related income tax benefits

A)Expensed

B)Capitalized as part of the cost of the shares

C)Deducted in total from shareholders' equity

D)Deducted from shareholders' equity, net of related income tax benefits

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

13

Perez Co. acquired Roo Co. in a business combination. Roo issued new shares to Perez's shareholders in exchange for their outstanding shares. What type of share exchange is this?

A)Direct exchange

B)Indirect exchange

C)Hostile takeover

D)Reverse takeover

A)Direct exchange

B)Indirect exchange

C)Hostile takeover

D)Reverse takeover

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

14

Sya Ltd. acquired all the assets and liabilities of Littman Ltd. by issuing common shares to Littman. After this transaction, Littman owned 30% of Sya's outstanding shares. Which of the following statements is true?

A)Littman is now a subsidiary of Sya.

B)This is an intercorporate investment for Sya.

C)Sya does not need to prepare consolidated financial statements.

D)Sya should use the equity method to reflect its investment in Littman.

A)Littman is now a subsidiary of Sya.

B)This is an intercorporate investment for Sya.

C)Sya does not need to prepare consolidated financial statements.

D)Sya should use the equity method to reflect its investment in Littman.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

15

At December 31, 20X0, Crowe Company has 80,000 common shares outstanding while Dylan Inc. has 40,000 common shares outstanding. Crowe wishes to gain control over Dylan and will enter into a reverse takeover of Dylan to gain Dylan's listing on the stock exchange. In order to facilitate the reverse takeover, which of the following would have to occur?

A)Dylan would have to issue more than 40,000 shares.

B)Dylan would have to issue less than 40,000 shares.

C)Crowe would have to issue less than 80,000 shares.

D)Crowe would have to issue more than 80,000 shares.

A)Dylan would have to issue more than 40,000 shares.

B)Dylan would have to issue less than 40,000 shares.

C)Crowe would have to issue less than 80,000 shares.

D)Crowe would have to issue more than 80,000 shares.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

16

What is the most common valuation method used for intangible assets?

A)Market-based

B)Income-based

C)Cost-based

D)Amortized cost

A)Market-based

B)Income-based

C)Cost-based

D)Amortized cost

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

17

Cheers acquired 100% of Tapp's shares for $150,000. On the acquisition date, the fair value of the current assets and the net capital assets of Tapp Ltd. were $104,000 and $216,000, respectively. The fair value of the liabilities equalled their book value. What is the amount of goodwill created in this acquisition?

A)$(24,000)

B)$ 0

C)$18,000

D)$40,000

A)$(24,000)

B)$ 0

C)$18,000

D)$40,000

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following is not a business combination?

A)Statutory amalgamation

B)Joint venture

C)A company's purchase of 100% of another company's net assets

D)A company's purchase of 80% of another company's voting shares

A)Statutory amalgamation

B)Joint venture

C)A company's purchase of 100% of another company's net assets

D)A company's purchase of 80% of another company's voting shares

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

19

Sya Ltd. acquired all the assets and liabilities of Littman Ltd. by issuing common shares to Littman. After this transaction, Littman owned 30% of Sya's outstanding shares. Which of the following statements is true?

A)Littman Ltd. ceases to exist.

B)Littman must record its receipt of Sya shares using the equity method.

C)Sya must prepare single-entity and consolidated financial statements.

D)Sya should not treat this transaction as an intercorporate investment.

A)Littman Ltd. ceases to exist.

B)Littman must record its receipt of Sya shares using the equity method.

C)Sya must prepare single-entity and consolidated financial statements.

D)Sya should not treat this transaction as an intercorporate investment.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

20

Sya Ltd. acquired all the assets and liabilities of Littman Ltd. by issuing common shares to Littman. After this transaction, Littman owned 30% of Sya's outstanding shares. How should Sya record Littman's assets and liabilities on its books?

A)At their original cost

B)At their net book value

C)At their fair market value

D)At their fair market value plus an allocated share of goodwill to each item

A)At their original cost

B)At their net book value

C)At their fair market value

D)At their fair market value plus an allocated share of goodwill to each item

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

21

Slade Co. has 1,000,000 shares outstanding and is traded on the TSX. On October 1, 20X6, Slade purchased all of the outstanding shares of Print Co. (a private company)by issuing 1,200,000 shares at $50 per share.

Required:

Explain the legal form of this transaction. What is the transaction in substance? How will this transaction be accounted for? Why might the transaction have been accomplished in this manner?

Required:

Explain the legal form of this transaction. What is the transaction in substance? How will this transaction be accounted for? Why might the transaction have been accomplished in this manner?

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

22

On December 31, 20X6, the statements of financial position of the Power Company and the Pro Company are as follows: (in 000s)

Power Company has 100,000 shares of common stock outstanding. Pro Company has 45,000 shares outstanding. On January 1, 20X7, Power issued an additional 90,000 shares of common stock in exchange for all the net assets of Pro. All assets and liabilities have book value equal to fair values, except as noted. In addition, Pro has a patent that has an appraised fair value of $450.

Market value of the new shares issued was $95 per share at the date of acquisition.

Required:

A)What is the amount of goodwill to be recorded for this business combination? Prepare the journal entry that Power would record on January 1, 20X7, related to this acquisition. In this case, who are the shareholders, and what are their percentage holdings on January 1, 20X7? Prepare the statement of financial position for Power as at January 1, 20X7.

B)How would your answer differ if Power had purchased the shares rather than the net assets of Pro Company? In this case, who are the shareholders and what are their percentage holdings on January 1, 20X7?

Power Company has 100,000 shares of common stock outstanding. Pro Company has 45,000 shares outstanding. On January 1, 20X7, Power issued an additional 90,000 shares of common stock in exchange for all the net assets of Pro. All assets and liabilities have book value equal to fair values, except as noted. In addition, Pro has a patent that has an appraised fair value of $450.

Market value of the new shares issued was $95 per share at the date of acquisition.

Required:

A)What is the amount of goodwill to be recorded for this business combination? Prepare the journal entry that Power would record on January 1, 20X7, related to this acquisition. In this case, who are the shareholders, and what are their percentage holdings on January 1, 20X7? Prepare the statement of financial position for Power as at January 1, 20X7.

B)How would your answer differ if Power had purchased the shares rather than the net assets of Pro Company? In this case, who are the shareholders and what are their percentage holdings on January 1, 20X7?

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

23

Hurricane Inc. wants to acquire 100% of the net assets of Flood Inc. using all cash consideration. From Flood's shareholders' point of view, what are the advantages and disadvantages of Hurricane purchasing shares rather than net assets of Flood?

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following is not a reason why a private enterprise may be acquired as a bargain purchase?

A)It is a family business and the next generation does not want to continue the business.

B)The owner has health problems and does not have a successor.

C)The business only has equity financing and has no debt financing.

D)The owner is no longer interested in the business.

A)It is a family business and the next generation does not want to continue the business.

B)The owner has health problems and does not have a successor.

C)The business only has equity financing and has no debt financing.

D)The owner is no longer interested in the business.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

25

On December 31, 20X5, CI Co. purchased 100% of the outstanding common shares of SA Ltd. for $1,100,000 in cash; 80% of the cash was obtained by issuing a five-year note payable. The statements of financial position of CI and SA immediately before the acquisition and issuance of the notes payable were as follows (in 000s):

Required:

Prepare the journal entry that CI will post to record the acquisition of SA. Prepare the consolidated statement of financial position for CI immediately following the acquisition of SA.

Required:

Prepare the journal entry that CI will post to record the acquisition of SA. Prepare the consolidated statement of financial position for CI immediately following the acquisition of SA.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following statements is not true about revaluation accounting?

A)Revaluation must be done regularly.

B)Revaluation can be applied to tangible assets whose fair values can be reliably measured.

C)Revaluation can be applied to intangible assets if the assets have an active market.

D)Revaluation is applied to individual assets.

A)Revaluation must be done regularly.

B)Revaluation can be applied to tangible assets whose fair values can be reliably measured.

C)Revaluation can be applied to intangible assets if the assets have an active market.

D)Revaluation is applied to individual assets.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

27

Ski Ltd. has 500,000 shares outstanding. On July 1, 20X7, Ski purchased all of the outstanding shares of Snow Ltd. The consideration paid by Ski was in the form of 500,000 shares, valued at $20 per share, which was premium of 10% over the market value prior to the announcement. It has been decided that the CEO of the combined company will come from Ski, but the CFO and the COO will come from Snow. The chairman of the board of directors will come from Snow. The board will have six other directors, three from Ski and three from Snow.

Required:

Define what the acquirer is in a business combination. How would you identify the acquirer in the above transaction?

Required:

Define what the acquirer is in a business combination. How would you identify the acquirer in the above transaction?

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

28

How is negative goodwill reported on financial statements?

A)On the consolidated SFP as "an excess of fair value over cost of assets acquired" under shareholders' equity

B)On the consolidated SFP as "negative goodwill" between the liabilities and shareholders' equity

C)On the consolidated SCI as "negative goodwill"

D)On the consolidated SCI as a "gain on bargain purchase"

A)On the consolidated SFP as "an excess of fair value over cost of assets acquired" under shareholders' equity

B)On the consolidated SFP as "negative goodwill" between the liabilities and shareholders' equity

C)On the consolidated SCI as "negative goodwill"

D)On the consolidated SCI as a "gain on bargain purchase"

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

29

How is negative goodwill treated in accounting for a joint venture in the year of acquisition?

A)Included in the investor's equity in the earnings of the investee

B)Included in the carrying value of the investment

C)Allocated among the assets and liabilities

D)Shown as a line item on the SFP

A)Included in the investor's equity in the earnings of the investee

B)Included in the carrying value of the investment

C)Allocated among the assets and liabilities

D)Shown as a line item on the SFP

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

30

On December 31, 20X5, CI Co. purchased 100% of the outstanding common shares of SA Ltd. for $1,500,000 in cash; 80% of the cash was obtained by issuing a five-year note payable. The statements of financial position of CI and SA immediately before the acquisition and issuance of the notes payable were as follows (in 000s):

Required:

Prepare the journal entry that CI will post to record the acquisition of CI. Prepare the consolidated statement of financial position for CI immediately following the acquisition of SA.

Required:

Prepare the journal entry that CI will post to record the acquisition of CI. Prepare the consolidated statement of financial position for CI immediately following the acquisition of SA.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

31

Which accounting method yields the same results as push-down accounting?

A)Equity method

B)Cost method

C)Consolidation

D)Revaluation

A)Equity method

B)Cost method

C)Consolidation

D)Revaluation

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

32

Cheers acquired 100% of Tapp's shares for $144,000. The condensed statements of financial position for Cheers and Tapp are given above, as well as the fair values of Tapp's assets and liabilities on the acquisition date. What is the amount of the goodwill on the acquisition?

A)$0

B)$11,200

C)$20,800

D)$32,000

A)$0

B)$11,200

C)$20,800

D)$32,000

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

33

On December 31, 20X6, the statements of financial position of the Power Company and the Pro Company are as follows: (in 000s)

Power Company has 100,000 shares of common stock outstanding. Pro Company has 45,000 shares outstanding. On January 1, 20X7, Power issued an additional 90,000 shares of common stock in exchange for all the outstanding shares of Pro. All assets and liabilities have book values equal to fair values, except as noted above. In addition, Pro has a patent that has an appraised fair value of $450.

Market value of the new shares issued was $95 per share at the date of acquisition.

What is the amount of goodwill to be recorded for this business combination? Prepare the journal entry that Power would record on January 1, 20X7, related to this acquisition. Prepare the consolidated statement of financial position at January 1, 20X7.

Power Company has 100,000 shares of common stock outstanding. Pro Company has 45,000 shares outstanding. On January 1, 20X7, Power issued an additional 90,000 shares of common stock in exchange for all the outstanding shares of Pro. All assets and liabilities have book values equal to fair values, except as noted above. In addition, Pro has a patent that has an appraised fair value of $450.

Market value of the new shares issued was $95 per share at the date of acquisition.

What is the amount of goodwill to be recorded for this business combination? Prepare the journal entry that Power would record on January 1, 20X7, related to this acquisition. Prepare the consolidated statement of financial position at January 1, 20X7.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

34

Cheers acquired 100% of Tapp's shares for $144,000. The condensed statements of financial position for Cheers and Tapp are given above, as well as the fair values of Tapp's assets and liabilities on the acquisition date. On Cheers's consolidated statement of financial position at the acquisition date, what is the total shareholders' equity?

A)$576,000

B)$624,000

C)$688,000

D)$11,888,000

A)$576,000

B)$624,000

C)$688,000

D)$11,888,000

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

35

Nashman Ltd. is a private enterprise with five subsidiaries. Which of the following statements is true?

A)Nashman must prepare consolidated financial statements.

B)Nashman should report all subsidiaries on the same basis.

C)Nashman must use the cost basis to report all subsidiaries.

D)Nashman can choose the subsidiaries it wishes to include in its consolidated financial statements.

A)Nashman must prepare consolidated financial statements.

B)Nashman should report all subsidiaries on the same basis.

C)Nashman must use the cost basis to report all subsidiaries.

D)Nashman can choose the subsidiaries it wishes to include in its consolidated financial statements.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

36

On January 1, 20X7, Falcon acquired the net assets of Intra for $3,400,000 with the issue of shares. The statement of financial position for Intra at the date of acquisition is shown below, together with estimates of the fair values of Intra's recorded assets and liabilities.

Required:

What is the amount of goodwill to be recorded for this business combination?

Prepare the journal entry that Falcon will use to record the business combination. Prepare the statement of financial position for Intra on January 1, 20X7, directly after the transaction is completed. Reconcile the book value of the retained earnings for Intra on December 31, 20X6, to its balance on January 1, 20X7. Explain any differences.

Required:What is the amount of goodwill to be recorded for this business combination?

Prepare the journal entry that Falcon will use to record the business combination. Prepare the statement of financial position for Intra on January 1, 20X7, directly after the transaction is completed. Reconcile the book value of the retained earnings for Intra on December 31, 20X6, to its balance on January 1, 20X7. Explain any differences.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

37

What does push-down accounting refer to?

A)Writing down assets where value is impaired

B)Applying the lower of cost or market approach

C)Recording fair values on a subsidiary's books after a business combination

D)Recording all consolidation adjustments on the books of the subsidiary

A)Writing down assets where value is impaired

B)Applying the lower of cost or market approach

C)Recording fair values on a subsidiary's books after a business combination

D)Recording all consolidation adjustments on the books of the subsidiary

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

38

Sugar Corp and Syrup Limited have reached an agreement in principle to combine their operations as of October 1, 20X9. However, the board of directors cannot decide on the best way to accomplish the combination. Below are the alternatives being considered.

1. Sugar acquires the net assets of Syrup for $1,700,000 cash.

2. Sugar acquires only the assets for $2,650,000 cash.

3. Sugar acquires all of the outstanding shares of Syrup by issuing shares with a fair market value of $1,700,000.

Syrup has the following assets and liabilities at October 1, 20X9 (in thousands of dollars).

The only item that has a fair value different from its carrying value is the property, plant, and equipment, which has a fair value of $1,900.

Required:

Explain how each transaction is different from the acquirer's point of view. Prepare the journal entry that would be recorded by Sugar for each these alternatives.

1. Sugar acquires the net assets of Syrup for $1,700,000 cash.

2. Sugar acquires only the assets for $2,650,000 cash.

3. Sugar acquires all of the outstanding shares of Syrup by issuing shares with a fair market value of $1,700,000.

Syrup has the following assets and liabilities at October 1, 20X9 (in thousands of dollars).

The only item that has a fair value different from its carrying value is the property, plant, and equipment, which has a fair value of $1,900.

Required:

Explain how each transaction is different from the acquirer's point of view. Prepare the journal entry that would be recorded by Sugar for each these alternatives.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

39

There are a number of possible approaches to reporting consolidated financial statements after one company acquires control over another. Which of the following methods reports the consolidated amounts by adding together the carrying values of the assets and liabilities of the parent and the subsidiary?

A)Pooling-of-interests method

B)Acquisition method

C)Purchase method

D)New entity method

A)Pooling-of-interests method

B)Acquisition method

C)Purchase method

D)New entity method

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

40

What type of business combination is accounted for in a manner that is essentially the same as the pooling-of-interests method?

A)Statutory amalgamation

B)Corporate restructuring

C)Reverse takeover

D)Hostile takeover

A)Statutory amalgamation

B)Corporate restructuring

C)Reverse takeover

D)Hostile takeover

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

41

A company is often purchased for its identifiable intangible assets, which must be measured at fair value at the date of acquisition. Discuss the three methods that are used to determine the fair value of identifiable intangibles. Why are these measurements subjective, and what is the ethical challenge relating to the determination of these values?

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

42

On September 1, 20X7, Spike Limited decided to buy 100% of the outstanding shares of Volley Inc. for $1,200,000, paid for with the issuance of shares. Acquisition costs for the deal totaled $30,000: $20,000 related to the issue of the shares and the remaining amount for legal, valuation, and administrative costs. All of these costs were paid in cash. In addition Spike has agreed to pay an additional $250,000 if the revenues of Volley have a 5% growth over the next two years from the date of the acquisition. It has been determined that the fair value of this contingent consideration is $175,000.

The balances showing on the statement of financial position for the two companies at August 31, 20X7, are as follows:

After a review of the financial assets and liabilities, Spike determines that some of the assets of Volley have fair values different from their carrying values. These items are listed below:

Property, plant, and equipment: fair value is $1,350,000

Patent: fair value is $255,000

Brand name: fair value is $135,000

Required:

Determine the amount of goodwill that will be recorded on the business combination.

Prepare the consolidated statement of financial position as at September 1, 20X7.

The balances showing on the statement of financial position for the two companies at August 31, 20X7, are as follows:

After a review of the financial assets and liabilities, Spike determines that some of the assets of Volley have fair values different from their carrying values. These items are listed below:Property, plant, and equipment: fair value is $1,350,000

Patent: fair value is $255,000

Brand name: fair value is $135,000

Required:

Determine the amount of goodwill that will be recorded on the business combination.

Prepare the consolidated statement of financial position as at September 1, 20X7.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

43

Explain how a business combination could occur with no transfer of consideration. Using the two scenarios below, explain how PCo could gain control of SCo with no transfer of consideration.

Scenario 1: SCo currently has 1,000,000 common shares outstanding, and PCo owns 300,000.

Scenario 2: SCo currently has 1,000,000 common shares outstanding. Although PCo owns 510,000 of these shares, PCo is unable to exert control due to regulatory restrictions.

Scenario 1: SCo currently has 1,000,000 common shares outstanding, and PCo owns 300,000.

Scenario 2: SCo currently has 1,000,000 common shares outstanding. Although PCo owns 510,000 of these shares, PCo is unable to exert control due to regulatory restrictions.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 43 flashcards in this deck.