Deck 11: Standard Costing and Variance Analysis

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Figure 1

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

The company records materials price variances at the time of purchase.

Refer to Figure 1. Max's materials usage variance would be

A) £40,000 unfavorable

B) £40,000 favorable

C) £4,800 unfavorable

D) £4,800 favorable

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 1. Max's materials usage variance would be

A) £40,000 unfavorable

B) £40,000 favorable

C) £4,800 unfavorable

D) £4,800 favorable

Question

Figure 1

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 1. Max's labour rate variance would be

A) £920 unfavorable

B) £920 favorable

C) £800 unfavorable

D) £800 favorable

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 1. Max's labour rate variance would be

A) £920 unfavorable

B) £920 favorable

C) £800 unfavorable

D) £800 favorable

Question

Question

Question

Question

Question

Figure 1

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 1. Max's materials price variance would be

A) £50,000 favorable

B) £50,000 unfavorable

C) £10,000 unfavorable

D) £10,000 favorable

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 1. Max's materials price variance would be

A) £50,000 favorable

B) £50,000 unfavorable

C) £10,000 unfavorable

D) £10,000 favorable

Question

Question

Figure 1

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 1. Max's variable standard cost per unit would be

A) £392

B) £336

C) £296

D) £152

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 1. Max's variable standard cost per unit would be

A) £392

B) £336

C) £296

D) £152

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Figure 5

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

The company records materials price variances at the time of purchase.

Refer to Figure 5. Ebola's labour efficiency variance would be

A) £18,000 favorable

B) £18,000 unfavorable

C) £17,700 unfavorable

D) £17,700 favorable

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 5. Ebola's labour efficiency variance would be

A) £18,000 favorable

B) £18,000 unfavorable

C) £17,700 unfavorable

D) £17,700 favorable

Question

Figure 2

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

The company records materials price variances at the time of purchase.

Refer to Figure 2. Rax's materials price variance would be

A) £4,000 unfavorable

B) £4,000 favorable

C) £1,600 unfavorable

D) £1,600 favorable

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 2. Rax's materials price variance would be

A) £4,000 unfavorable

B) £4,000 favorable

C) £1,600 unfavorable

D) £1,600 favorable

Question

Figure 5

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 5. Ebola's materials price variance would be

A) £46,000 favorable

B) £46,000 unfavorable

C) £44,000 favorable

D) £44,000 unfavorable

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 5. Ebola's materials price variance would be

A) £46,000 favorable

B) £46,000 unfavorable

C) £44,000 favorable

D) £44,000 unfavorable

Question

Question

Figure 5

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 5. Ebola's labour rate variance would be

A) £15,000 unfavorable

B) £15,000 favorable

C) £15,300 unfavorable

D) £15,300 favorable

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 5. Ebola's labour rate variance would be

A) £15,000 unfavorable

B) £15,000 favorable

C) £15,300 unfavorable

D) £15,300 favorable

Question

Figure 5

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 5. Ebola's materials usage variance would be

A) £120,000 favorable

B) £120,000 unfavorable

C) £80,000 unfavorable

D) £80,000 favorable

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 5. Ebola's materials usage variance would be

A) £120,000 favorable

B) £120,000 unfavorable

C) £80,000 unfavorable

D) £80,000 favorable

Question

Figure 2

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 2. Rax's labour efficiency variance would be

A) £4,300 unfavorable

B) £4,300 favorable

C) £1,800 unfavorable

D) £1,800 favorable

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 2. Rax's labour efficiency variance would be

A) £4,300 unfavorable

B) £4,300 favorable

C) £1,800 unfavorable

D) £1,800 favorable

Question

Figure 1

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 1. Max's labour efficiency variance would be

A) £7,200 unfavorable

B) £7,200 favorable

C) £6,280 unfavorable

D) £6,280 favorable

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 1. Max's labour efficiency variance would be

A) £7,200 unfavorable

B) £7,200 favorable

C) £6,280 unfavorable

D) £6,280 favorable

Question

Question

Question

Question

Figure 2

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 2. Rax's materials usage variance would be

A) £8,400 unfavorable

B) £8,400 favorable

C) £5,600 unfavorable

D) £5,600 favorable

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 2. Rax's materials usage variance would be

A) £8,400 unfavorable

B) £8,400 favorable

C) £5,600 unfavorable

D) £5,600 favorable

Question

Figure 3

Tuvok Ltd. has developed the following standards for one of its products:

Refer to Figure 3. Tuvok's actual cost per pound of materials must have been (round to the nearest cent)

A) £0.50

B) £0.55

C) £0.61

D) £5.00

Tuvok Ltd. has developed the following standards for one of its products:

Refer to Figure 3. Tuvok's actual cost per pound of materials must have been (round to the nearest cent)

A) £0.50

B) £0.55

C) £0.61

D) £5.00

Question

Question

Figure 3

Tuvok Ltd. has developed the following standards for one of its products:

Refer to Figure 3. Tuvok's material price variance is

A) £1,000 unfavorable

B) £2,000 unfavorable

C) £1,100 unfavorable

D) cannot be computed from the information given

Tuvok Ltd. has developed the following standards for one of its products:

Refer to Figure 3. Tuvok's material price variance is

A) £1,000 unfavorable

B) £2,000 unfavorable

C) £1,100 unfavorable

D) cannot be computed from the information given

Question

Figure 3

Tuvok Ltd. has developed the following standards for one of its products:

Refer to Figure 3. Tuvok's materials usage variance is

A) £1,000 unfavorable

B) £1,100 unfavorable

C) £2,000 unfavorable

D) cannot be determined from the information given

Tuvok Ltd. has developed the following standards for one of its products:

Refer to Figure 3. Tuvok's materials usage variance is

A) £1,000 unfavorable

B) £1,100 unfavorable

C) £2,000 unfavorable

D) cannot be determined from the information given

Question

Figure 2

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 2. Rax's variable standard cost per unit would be

A) £78

B) £192

C) £246

D) £222

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 2. Rax's variable standard cost per unit would be

A) £78

B) £192

C) £246

D) £222

Question

Figure 2

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 2. Rax's labour rate variance would be

A) £4,300 favorable

B) £4,300 unfavorable

C) £2,500 favorable

D) £2,500 unfavorable

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 2. Rax's labour rate variance would be

A) £4,300 favorable

B) £4,300 unfavorable

C) £2,500 favorable

D) £2,500 unfavorable

Question

Figure 5

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 5. Ebola's variable overhead efficiency variance would be

A) £4,000 favorable

B) £4,000 unfavorable

C) £8,000 favorable

D) £12,000 unfavorable

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 5. Ebola's variable overhead efficiency variance would be

A) £4,000 favorable

B) £4,000 unfavorable

C) £8,000 favorable

D) £12,000 unfavorable

Question

Figure 5

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 5. Ebola's variable overhead spending (expenditure)variance would be

A) £36,000 favorable

B) £36,000 unfavorable

C) £40,000 favorable

D) £40,000 unfavorable

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 5. Ebola's variable overhead spending (expenditure)variance would be

A) £36,000 favorable

B) £36,000 unfavorable

C) £40,000 favorable

D) £40,000 unfavorable

Question

Question

Figure 6

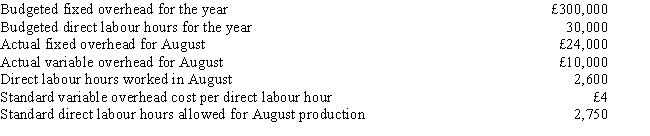

Refer to Figure 6. The variable overhead spending (expenditure) variance would be

A) £2,000 favorable

B) £1,200 favorable

C) £400 favorable

D) £200 favorable

Refer to Figure 6. The variable overhead spending (expenditure) variance would be

A) £2,000 favorable

B) £1,200 favorable

C) £400 favorable

D) £200 favorable

Question

Lisle Manufacturing has developed the following standards for one of its products:

The company records materials price variances at the time of purchase.

During August, Lisle purchased 16,000 yards of material costing £169,600 and used 12,500 yards in its manufacturing process. There was no material inventory at August 1. Lisle recorded a total of 4,600 direct labour hours worked for a total payroll of £72,680. Lisle manufactured 1,200 units in August.

Required:

a.

Calculate the materials price variance and indicate whether it is favorable or unfavorable.

b.

Calculate the materials usage variance and indicate whether it is favorable or unfavorable.

c.

Calculate the labour rate variance and indicate whether it is favorable or unfavorable.

d.

Calculate the labour efficiency variance and indicate whether it is favorable or unfavorable.

The company records materials price variances at the time of purchase.

During August, Lisle purchased 16,000 yards of material costing £169,600 and used 12,500 yards in its manufacturing process. There was no material inventory at August 1. Lisle recorded a total of 4,600 direct labour hours worked for a total payroll of £72,680. Lisle manufactured 1,200 units in August.

Required:

a.

Calculate the materials price variance and indicate whether it is favorable or unfavorable.

b.

Calculate the materials usage variance and indicate whether it is favorable or unfavorable.

c.

Calculate the labour rate variance and indicate whether it is favorable or unfavorable.

d.

Calculate the labour efficiency variance and indicate whether it is favorable or unfavorable.

Question

Figure 6

Refer to Figure 6. The standard rate for total overhead is

A) £14

B) £13

C) £10

D) £4

Refer to Figure 6. The standard rate for total overhead is

A) £14

B) £13

C) £10

D) £4

Question

Question

Figure 6

Refer to Figure 6. The variable overhead efficiency variance would be

A) £1,000 favorable

B) £600 favorable

C) £400 favorable

D) £200 favorable

Refer to Figure 6. The variable overhead efficiency variance would be

A) £1,000 favorable

B) £600 favorable

C) £400 favorable

D) £200 favorable

Question

Figure 8

The following information was extracted from the accounting records of Noelle Company:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Refer to Figure 8. Noelle's fixed overhead spending (expenditure) variance would be

A) £10,000 unfavorable

B) £11,000 unfavorable

C) £21,000 favorable

D) £31,000 favorable

The following information was extracted from the accounting records of Noelle Company:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Refer to Figure 8. Noelle's fixed overhead spending (expenditure) variance would be

A) £10,000 unfavorable

B) £11,000 unfavorable

C) £21,000 favorable

D) £31,000 favorable

Question

Figure 8

The following information was extracted from the accounting records of Noelle Company:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Refer to Figure 8. Noelle's standard fixed overhead rate is

A) £14.82

B) £14.48

C) £14.34

D) £14.00

The following information was extracted from the accounting records of Noelle Company:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Refer to Figure 8. Noelle's standard fixed overhead rate is

A) £14.82

B) £14.48

C) £14.34

D) £14.00

Question

Figure 6

Refer to Figure 6. The fixed overhead spending (expenditure) variance would be

A) £2,500 unfavorable

B) £2,500 favorable

C) £1,000 unfavorable

D) £1,000 favorable

Refer to Figure 6. The fixed overhead spending (expenditure) variance would be

A) £2,500 unfavorable

B) £2,500 favorable

C) £1,000 unfavorable

D) £1,000 favorable

Question

Figure 7

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November:

The company records materials price variances at the time of purchase.

The company records materials price variances at the time of purchase.

Refer to Figure 7. Orient's materials price variance would be

A) £22,000 unfavorable

B) £18,000 unfavorable

C) £6,000 unfavorable

D) £4,000 unfavorable

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November:

The company records materials price variances at the time of purchase.Refer to Figure 7. Orient's materials price variance would be

A) £22,000 unfavorable

B) £18,000 unfavorable

C) £6,000 unfavorable

D) £4,000 unfavorable

Question

Figure 7

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November:

The company records materials price variances at the time of purchase.

Refer to Figure 7. Orient's variable overhead spending (expenditure) variance would be

A) £4,800 favorable

B) £4,800 unfavorable

C) £3,600 unfavorable

D) £1,200 unfavorable

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November:

The company records materials price variances at the time of purchase.Refer to Figure 7. Orient's variable overhead spending (expenditure) variance would be

A) £4,800 favorable

B) £4,800 unfavorable

C) £3,600 unfavorable

D) £1,200 unfavorable

Question

Figure 7

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November:

The company records materials price variances at the time of purchase.

Refer to Figure 7. Orient's labour efficiency variance would be

A) £12,000 unfavorable

B) £12,000 favorable

C) £8,400 favorable

D) £3,600 unfavorable

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November:

The company records materials price variances at the time of purchase.Refer to Figure 7. Orient's labour efficiency variance would be

A) £12,000 unfavorable

B) £12,000 favorable

C) £8,400 favorable

D) £3,600 unfavorable

Question

Question

Figure 7

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November:

The company records materials price variances at the time of purchase.

Refer to Figure 7. Orient's labour rate variance would be

A) £12,000 unfavorable

B) £12,000 favorable

C) £8,400 favorable

D) £3,600 unfavorable

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November:

The company records materials price variances at the time of purchase.Refer to Figure 7. Orient's labour rate variance would be

A) £12,000 unfavorable

B) £12,000 favorable

C) £8,400 favorable

D) £3,600 unfavorable

Question

Question

Figure 7

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November:

The company records materials price variances at the time of purchase.

Refer to Figure 7. Orient's variable overhead efficiency variance would be

A) £1,200 unfavorable

B) £3,600 unfavorable

C) £4,800 unfavorable

D) £4,800 favorable

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November:

The company records materials price variances at the time of purchase.Refer to Figure 7. Orient's variable overhead efficiency variance would be

A) £1,200 unfavorable

B) £3,600 unfavorable

C) £4,800 unfavorable

D) £4,800 favorable

Question

Question

Figure 7

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November:

The company records materials price variances at the time of purchase.

Refer to Figure 7. Orient's materials usage variance would be

A) £22,000 unfavorable

B) £12,000 favorable

C) £10,000 unfavorable

D) £4,000 unfavorable

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November:

The company records materials price variances at the time of purchase.Refer to Figure 7. Orient's materials usage variance would be

A) £22,000 unfavorable

B) £12,000 favorable

C) £10,000 unfavorable

D) £4,000 unfavorable

Question

Figure 8

The following information was extracted from the accounting records of Noelle Company:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Refer to Figure 8. Noelle's variable overhead spending (expenditure) variance would be

A) £7,000 favorable

B) £8,000 unfavorable

C) £15,000 favorable

D) £23,000 unfavorable

The following information was extracted from the accounting records of Noelle Company:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Refer to Figure 8. Noelle's variable overhead spending (expenditure) variance would be

A) £7,000 favorable

B) £8,000 unfavorable

C) £15,000 favorable

D) £23,000 unfavorable

Question

Figure 8

The following information was extracted from the accounting records of Noelle Company:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Refer to Figure 8. Noelle's variable overhead efficiency variance would be

A) £7,000 favorable

B) £8,000 unfavorable

C) £15,000 favorable

D) £23,000 unfavorable

The following information was extracted from the accounting records of Noelle Company:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Refer to Figure 8. Noelle's variable overhead efficiency variance would be

A) £7,000 favorable

B) £8,000 unfavorable

C) £15,000 favorable

D) £23,000 unfavorable

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/95

Play

Full screen (f)

Deck 11: Standard Costing and Variance Analysis

1

Which of the following is NOT true about currently attainable standards?

A) They are based on an efficiently operating work force.

B) They are based on ideal conditions.

C) They allow for downtime and rest periods.

D) They are based on present production processes and technology.

A) They are based on an efficiently operating work force.

B) They are based on ideal conditions.

C) They allow for downtime and rest periods.

D) They are based on present production processes and technology.

B

2

Which department is usually held responsible for materials quantity variance?

A) purchasing

B) production

C) engineering

D) marketing

A) purchasing

B) production

C) engineering

D) marketing

B

3

Efficiency variances focus on the difference between

A) actual quantity used and standard quantity allowed for estimated activity

B) actual quantity used and standard quantity allowed for units actually produced

C) quantity allowed for estimated production and standard quantity allowed for units actually produced

D) none of the above

A) actual quantity used and standard quantity allowed for estimated activity

B) actual quantity used and standard quantity allowed for units actually produced

C) quantity allowed for estimated production and standard quantity allowed for units actually produced

D) none of the above

B

4

The materials usage variance is calculated as

A) (Actual price - Standard price) x Actual quantity

B) (Actual price - Standard price) x Standard quantity

C) (Actual quantity - Standard quantity) x Actual price

D) (Actual quantity - Standard quantity) x Standard price

A) (Actual price - Standard price) x Actual quantity

B) (Actual price - Standard price) x Standard quantity

C) (Actual quantity - Standard quantity) x Actual price

D) (Actual quantity - Standard quantity) x Standard price

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

5

An unfavorable materials usage variance may be caused by

A) excessive rework

B) a special price offered by suppliers

C) use of experienced workers

D) none of the above

A) excessive rework

B) a special price offered by suppliers

C) use of experienced workers

D) none of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

6

An unfavorable materials price variance may be caused by

A) excessive rework

B) a special price offered by suppliers

C) use of experienced workers

D) none of the above

A) excessive rework

B) a special price offered by suppliers

C) use of experienced workers

D) none of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

7

The purchase of inferior direct materials at a lower price might affect which of the following variances?

A) materials price variance

B) materials usage variance

C) labour efficiency variance

D) all of the above

A) materials price variance

B) materials usage variance

C) labour efficiency variance

D) all of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

8

Price variances focus on the difference between

A) actual price and standard price for actual quantity allowed for units actually produced

B) actual price and standard price for standard quantity allowed for units actually produced

C) actual price and standard price for actual quantity allowed for estimated activity

D) none of the above

A) actual price and standard price for actual quantity allowed for units actually produced

B) actual price and standard price for standard quantity allowed for units actually produced

C) actual price and standard price for actual quantity allowed for estimated activity

D) none of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

9

Variances indicate

A) the cause of the variance

B) who is responsible for the variance

C) that actual performance is not going according to plan

D) when the variance should be investigated

A) the cause of the variance

B) who is responsible for the variance

C) that actual performance is not going according to plan

D) when the variance should be investigated

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

10

For better control of direct material prices, when should direct material price variance be recognized?

A) when material is purchased

B) when material is issued from the storeroom

C) when material is put into production

D) when production is completed

A) when material is purchased

B) when material is issued from the storeroom

C) when material is put into production

D) when production is completed

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following is information that would be included in the standard cost card (sheet)?

A) quantity and price of direct materials for each unit of output

B) retail price of the product charged to the customers

C) delivery cost per unit of product

D) all of the above

A) quantity and price of direct materials for each unit of output

B) retail price of the product charged to the customers

C) delivery cost per unit of product

D) all of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

12

Standard cost systems can enhance operational control through the use of

A) price variances, which indicate the need for enhanced spending control

B) efficiency variances, which indicate the need for corrective action

C) standard costs, which indicate the desired cost of a unit of input

D) actual costs, which indicate the price received for units sold

A) price variances, which indicate the need for enhanced spending control

B) efficiency variances, which indicate the need for corrective action

C) standard costs, which indicate the desired cost of a unit of input

D) actual costs, which indicate the price received for units sold

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

13

To determine the unit standard cost for a particular input, a company must decide how much

A) input should be used per unit of output and how much should be paid for the quantity of the input to be used

B) input should be used per unit of output and how much output should be produced

C) output should be produced and how much should be paid for each unit produced

D) should be paid for the quantity of the input to be used and how much input should be purchased

A) input should be used per unit of output and how much should be paid for the quantity of the input to be used

B) input should be used per unit of output and how much output should be produced

C) output should be produced and how much should be paid for each unit produced

D) should be paid for the quantity of the input to be used and how much input should be purchased

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

14

An unfavorable materials price variance with a favorable materials usage variance would most likely be the result of

A) machines breaking down

B) problems with labour efficiency

C) purchase of high quality materials

D) problems with labour rates

A) machines breaking down

B) problems with labour efficiency

C) purchase of high quality materials

D) problems with labour rates

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

15

A favorable materials price variance may be caused by

A) excessive rework

B) a special price offered by suppliers

C) use of experienced workers

D) none of the above

A) excessive rework

B) a special price offered by suppliers

C) use of experienced workers

D) none of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is a disadvantage of adopting a standard costing system?

A) to improve planning and control

B) to facilitate product costing and pricing

C) to help establish the quality and safety of products

D) All of the above are advantages.

A) to improve planning and control

B) to facilitate product costing and pricing

C) to help establish the quality and safety of products

D) All of the above are advantages.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

17

Which statement about the selection of standards is true?

A) Ideal standards tend to extract higher performance levels since they give employees something to live up to.

B) Currently attainable standards may encourage operating inefficiencies.

C) Currently attainable standards discourage employees from achieving their full performance potential.

D) Ideal standards demand maximum efficiency, which may leave workers frustrated, thus causing a decline in performance.

A) Ideal standards tend to extract higher performance levels since they give employees something to live up to.

B) Currently attainable standards may encourage operating inefficiencies.

C) Currently attainable standards discourage employees from achieving their full performance potential.

D) Ideal standards demand maximum efficiency, which may leave workers frustrated, thus causing a decline in performance.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

18

A favorable materials usage variance may be caused by

A) excessive rework

B) a special price offered by suppliers

C) use of experienced workers

D) none of the above

A) excessive rework

B) a special price offered by suppliers

C) use of experienced workers

D) none of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

19

The materials price variance is calculated as

A) (Actual price - Standard price) x Actual quantity

B) (Actual price - Standard price) x Standard quantity

C) (Actual quantity - Standard quantity) x Actual price

D) (Actual quantity - Standard quantity) x Standard price

A) (Actual price - Standard price) x Actual quantity

B) (Actual price - Standard price) x Standard quantity

C) (Actual quantity - Standard quantity) x Actual price

D) (Actual quantity - Standard quantity) x Standard price

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

20

Standard costs include the quantity and price of inputs for each unit of product. These inputs include

A) delivery costs

B) marketing costs

C) accounting costs

D) overhead costs

A) delivery costs

B) marketing costs

C) accounting costs

D) overhead costs

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

21

Figure 1

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 1. Max's materials usage variance would be

A) £40,000 unfavorable

B) £40,000 favorable

C) £4,800 unfavorable

D) £4,800 favorable

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 1. Max's materials usage variance would be

A) £40,000 unfavorable

B) £40,000 favorable

C) £4,800 unfavorable

D) £4,800 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

22

Figure 1

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 1. Max's labour rate variance would be

A) £920 unfavorable

B) £920 favorable

C) £800 unfavorable

D) £800 favorable

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 1. Max's labour rate variance would be

A) £920 unfavorable

B) £920 favorable

C) £800 unfavorable

D) £800 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

23

During December, 6,000 pounds of raw materials were purchased at a cost of £16 per pound. If there was an unfavorable materials price variance of £6,000 for December, the standard cost per pound must be

A) £17

B) £16

C) £15

D) none of the above

A) £17

B) £16

C) £15

D) none of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

24

The standard fixed overhead rate is calculated as

A) Actual fixed overhead/Actual activity

B) Budgeted fixed overhead/Budgeted activity

C) Budgeted fixed overhead/Actual activity

D) Budgeted overhead/Budgeted activity

A) Actual fixed overhead/Actual activity

B) Budgeted fixed overhead/Budgeted activity

C) Budgeted fixed overhead/Actual activity

D) Budgeted overhead/Budgeted activity

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

25

If variable overhead is applied based on direct labour hours and there is an unfavorable labour efficiency variance,

A) the materials usage variance will be unfavorable

B) the labour rate variance will be favorable

C) the variable overhead efficiency variance will be unfavorable

D) the variable overhead spending (expenditure)variance will be unfavorable

A) the materials usage variance will be unfavorable

B) the labour rate variance will be favorable

C) the variable overhead efficiency variance will be unfavorable

D) the variable overhead spending (expenditure)variance will be unfavorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

26

The labour rate variance is calculated as

A) (Actual hourly wage rate - Standard hourly wage rate) x Actual direct labour hours used

B) (Actual hourly wage rate - Standard hourly wage rate) x Standard direct labour hours that should have been used

C) (Actual direct labour hours used - Standard direct labour hours that should have been used) x Actual hourly wage rate

D) (Actual direct labour hours used - Standard direct labour hours that should have been used) x Standard hourly wage rate

A) (Actual hourly wage rate - Standard hourly wage rate) x Actual direct labour hours used

B) (Actual hourly wage rate - Standard hourly wage rate) x Standard direct labour hours that should have been used

C) (Actual direct labour hours used - Standard direct labour hours that should have been used) x Actual hourly wage rate

D) (Actual direct labour hours used - Standard direct labour hours that should have been used) x Standard hourly wage rate

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

27

Figure 1

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 1. Max's materials price variance would be

A) £50,000 favorable

B) £50,000 unfavorable

C) £10,000 unfavorable

D) £10,000 favorable

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 1. Max's materials price variance would be

A) £50,000 favorable

B) £50,000 unfavorable

C) £10,000 unfavorable

D) £10,000 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

28

The labour efficiency variance is calculated as

A) (Actual direct labour hours used - Standard direct labour hours that should have been used) x Actual direct labour hours used

B) (Actual hourly wage rate - Standard hourly wage rate) x Standard direct labour hours that should have been used

C) (Actual direct labour hours used - Standard direct labour hours that should have been used) x Actual hourly wage rate

D) (Actual direct labour hours used - Standard direct labour hours that should have been used) x Standard hourly wage rate

A) (Actual direct labour hours used - Standard direct labour hours that should have been used) x Actual direct labour hours used

B) (Actual hourly wage rate - Standard hourly wage rate) x Standard direct labour hours that should have been used

C) (Actual direct labour hours used - Standard direct labour hours that should have been used) x Actual hourly wage rate

D) (Actual direct labour hours used - Standard direct labour hours that should have been used) x Standard hourly wage rate

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

29

Figure 1

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 1. Max's variable standard cost per unit would be

A) £392

B) £336

C) £296

D) £152

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 1. Max's variable standard cost per unit would be

A) £392

B) £336

C) £296

D) £152

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

30

The two variances for variable overhead are

A) spending (expenditure) and efficiency variances

B) spending and budget variances

C) budget and volume variances

D) budget and efficiency variances

A) spending (expenditure) and efficiency variances

B) spending and budget variances

C) budget and volume variances

D) budget and efficiency variances

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

31

During September, 40,000 units of product were produced. The standard quantity of material allowed per unit was four pounds at a standard cost of £6.00 per pound. If there was a favorable materials usage variance of £30,000 for April, the actual quantity of materials used must be

A) 41,250 pounds

B) 38,750 pounds

C) 165,000 pounds

D) 155,000 pounds

A) 41,250 pounds

B) 38,750 pounds

C) 165,000 pounds

D) 155,000 pounds

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

32

Who is responsible for unfavorable labour efficiency variances caused by poor quality materials?

A) warehouse manager

B) production manager

C) purchasing manager

D) engineering manager

A) warehouse manager

B) production manager

C) purchasing manager

D) engineering manager

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

33

If a company was concerned with controlling expenditures on overhead items, which variance would be useful?

A) fixed overhead volume variance

B) variable overhead efficiency variance

C) variable overhead spending (expenditure)variance

D) both b and c

A) fixed overhead volume variance

B) variable overhead efficiency variance

C) variable overhead spending (expenditure)variance

D) both b and c

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

34

During May, 6,000 pounds of raw materials were purchased at a cost of £2.60 per pound. If there was a favorable materials price variance of £900 for December, the standard cost per pound must be

A) £2.75

B) £2.60

C) £2.45

D) none of the above

A) £2.75

B) £2.60

C) £2.45

D) none of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

35

labour efficiency variances may be caused by

A) the use of highly skilled workers

B) frequent machinery breakdowns

C) the use of marginally skilled workers

D) all of the above

A) the use of highly skilled workers

B) frequent machinery breakdowns

C) the use of marginally skilled workers

D) all of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

36

During April, 80,000 units of product were produced. The standard quantity of material allowed per unit was two pounds at a standard cost of £5 per pound. If there was a favorable materials usage variance of £40,000 for April, the actual quantity of materials used must have been

A) 168,000 pounds

B) 152,000 pounds

C) 84,000 pounds

D) 76,000 pounds

A) 168,000 pounds

B) 152,000 pounds

C) 84,000 pounds

D) 76,000 pounds

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

37

labour rate variances can be the result of

A) the use of an average wage rate

B) unexpected overtime

C) seniority mix changes

D) all of the above

A) the use of an average wage rate

B) unexpected overtime

C) seniority mix changes

D) all of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

38

Using more highly skilled direct labourers might affect which of the following variances?

A) materials usage variance

B) labour efficiency variance

C) variable manufacturing overhead efficiency variance

D) all of the above

A) materials usage variance

B) labour efficiency variance

C) variable manufacturing overhead efficiency variance

D) all of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

39

A 5 percent wage increase for all factory employees would affect which of the following variances?

A) materials price variance

B) labour rate variance

C) labour efficiency variance

D) variable manufacturing overhead efficiency variance

A) materials price variance

B) labour rate variance

C) labour efficiency variance

D) variable manufacturing overhead efficiency variance

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

40

During October, 16,000 direct labour hours were worked at a standard cost of £6 per hour. If the labour rate variance for October was £4,000 unfavorable, the actual cost per labour hour must be

A) £6.25

B) £6.00

C) £5.75

D) none of the above

A) £6.25

B) £6.00

C) £5.75

D) none of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

41

Figure 5

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 5. Ebola's labour efficiency variance would be

A) £18,000 favorable

B) £18,000 unfavorable

C) £17,700 unfavorable

D) £17,700 favorable

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 5. Ebola's labour efficiency variance would be

A) £18,000 favorable

B) £18,000 unfavorable

C) £17,700 unfavorable

D) £17,700 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

42

Figure 2

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 2. Rax's materials price variance would be

A) £4,000 unfavorable

B) £4,000 favorable

C) £1,600 unfavorable

D) £1,600 favorable

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 2. Rax's materials price variance would be

A) £4,000 unfavorable

B) £4,000 favorable

C) £1,600 unfavorable

D) £1,600 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

43

Figure 5

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 5. Ebola's materials price variance would be

A) £46,000 favorable

B) £46,000 unfavorable

C) £44,000 favorable

D) £44,000 unfavorable

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 5. Ebola's materials price variance would be

A) £46,000 favorable

B) £46,000 unfavorable

C) £44,000 favorable

D) £44,000 unfavorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

44

During October, 14,000 direct labour hours were worked at a standard cost of £40 per hour. If the labour rate variance for October was £70,000 favorable, the actual cost per labour hour must be

A) £35

B) £40

C) £45

D) none of the above

A) £35

B) £40

C) £45

D) none of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

45

Figure 5

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 5. Ebola's labour rate variance would be

A) £15,000 unfavorable

B) £15,000 favorable

C) £15,300 unfavorable

D) £15,300 favorable

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 5. Ebola's labour rate variance would be

A) £15,000 unfavorable

B) £15,000 favorable

C) £15,300 unfavorable

D) £15,300 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

46

Figure 5

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 5. Ebola's materials usage variance would be

A) £120,000 favorable

B) £120,000 unfavorable

C) £80,000 unfavorable

D) £80,000 favorable

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 5. Ebola's materials usage variance would be

A) £120,000 favorable

B) £120,000 unfavorable

C) £80,000 unfavorable

D) £80,000 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

47

Figure 2

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 2. Rax's labour efficiency variance would be

A) £4,300 unfavorable

B) £4,300 favorable

C) £1,800 unfavorable

D) £1,800 favorable

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 2. Rax's labour efficiency variance would be

A) £4,300 unfavorable

B) £4,300 favorable

C) £1,800 unfavorable

D) £1,800 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

48

Figure 1

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 1. Max's labour efficiency variance would be

A) £7,200 unfavorable

B) £7,200 favorable

C) £6,280 unfavorable

D) £6,280 favorable

Max Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 1. Max's labour efficiency variance would be

A) £7,200 unfavorable

B) £7,200 favorable

C) £6,280 unfavorable

D) £6,280 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

49

If actual fixed overhead was £120,000 and there was a £2,600 favorable spending (expenditure) variance and a £2,000 unfavorable volume variance, budgeted fixed overhead must have been

A) £124,600

B) £122,000

C) £120,000

D) £122,600

A) £124,600

B) £122,000

C) £120,000

D) £122,600

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

50

Figure 4

Shannon Ltd.'s standard cost card contained the following information:

Direct labour: 1.25 hours x £8.00 per hour = £10.00

Shannon planned to make 12,000 units. Shannon actually made 10,000 units using 13,000 hours.

Refer to Figure 4. Shannon's standard hours allowed for production was

A) 12,500

B) 15,000

C) 16,250

D) 13,000

Shannon Ltd.'s standard cost card contained the following information:

Direct labour: 1.25 hours x £8.00 per hour = £10.00

Shannon planned to make 12,000 units. Shannon actually made 10,000 units using 13,000 hours.

Refer to Figure 4. Shannon's standard hours allowed for production was

A) 12,500

B) 15,000

C) 16,250

D) 13,000

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

51

Figure 4

Shannon Ltd.'s standard cost card contained the following information:

Direct labour: 1.25 hours x £8.00 per hour = £10.00

Shannon planned to make 12,000 units. Shannon actually made 10,000 units using 13,000 hours.

Refer to Figure 4. Shannon's labour efficiency variance was

A) £4,625 unfavorable

B) £4,000 unfavorable

C) £27,750 unfavorable

D) £24,000 unfavorable

Shannon Ltd.'s standard cost card contained the following information:

Direct labour: 1.25 hours x £8.00 per hour = £10.00

Shannon planned to make 12,000 units. Shannon actually made 10,000 units using 13,000 hours.

Refer to Figure 4. Shannon's labour efficiency variance was

A) £4,625 unfavorable

B) £4,000 unfavorable

C) £27,750 unfavorable

D) £24,000 unfavorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

52

Figure 2

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 2. Rax's materials usage variance would be

A) £8,400 unfavorable

B) £8,400 favorable

C) £5,600 unfavorable

D) £5,600 favorable

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 2. Rax's materials usage variance would be

A) £8,400 unfavorable

B) £8,400 favorable

C) £5,600 unfavorable

D) £5,600 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

53

Figure 3

Tuvok Ltd. has developed the following standards for one of its products:

Refer to Figure 3. Tuvok's actual cost per pound of materials must have been (round to the nearest cent)

A) £0.50

B) £0.55

C) £0.61

D) £5.00

Tuvok Ltd. has developed the following standards for one of its products:

Refer to Figure 3. Tuvok's actual cost per pound of materials must have been (round to the nearest cent)

A) £0.50

B) £0.55

C) £0.61

D) £5.00

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

54

Figure 4

Shannon Ltd.'s standard cost card contained the following information:

Direct labour: 1.25 hours x £8.00 per hour = £10.00

Shannon planned to make 12,000 units. Shannon actually made 10,000 units using 13,000 hours.

Refer to Figure 4. If Shannon's actual labour cost was £136,500, Shannon's labour rate variance was

A) £32,500 unfavorable

B) £32,500 favorable

C) £6,500 unfavorable

D) £6,500 favorable

Shannon Ltd.'s standard cost card contained the following information:

Direct labour: 1.25 hours x £8.00 per hour = £10.00

Shannon planned to make 12,000 units. Shannon actually made 10,000 units using 13,000 hours.

Refer to Figure 4. If Shannon's actual labour cost was £136,500, Shannon's labour rate variance was

A) £32,500 unfavorable

B) £32,500 favorable

C) £6,500 unfavorable

D) £6,500 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

55

Figure 3

Tuvok Ltd. has developed the following standards for one of its products:

Refer to Figure 3. Tuvok's material price variance is

A) £1,000 unfavorable

B) £2,000 unfavorable

C) £1,100 unfavorable

D) cannot be computed from the information given

Tuvok Ltd. has developed the following standards for one of its products:

Refer to Figure 3. Tuvok's material price variance is

A) £1,000 unfavorable

B) £2,000 unfavorable

C) £1,100 unfavorable

D) cannot be computed from the information given

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

56

Figure 3

Tuvok Ltd. has developed the following standards for one of its products:

Refer to Figure 3. Tuvok's materials usage variance is

A) £1,000 unfavorable

B) £1,100 unfavorable

C) £2,000 unfavorable

D) cannot be determined from the information given

Tuvok Ltd. has developed the following standards for one of its products:

Refer to Figure 3. Tuvok's materials usage variance is

A) £1,000 unfavorable

B) £1,100 unfavorable

C) £2,000 unfavorable

D) cannot be determined from the information given

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

57

Figure 2

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 2. Rax's variable standard cost per unit would be

A) £78

B) £192

C) £246

D) £222

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 2. Rax's variable standard cost per unit would be

A) £78

B) £192

C) £246

D) £222

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

58

Figure 2

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 2. Rax's labour rate variance would be

A) £4,300 favorable

B) £4,300 unfavorable

C) £2,500 favorable

D) £2,500 unfavorable

Rax Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 2. Rax's labour rate variance would be

A) £4,300 favorable

B) £4,300 unfavorable

C) £2,500 favorable

D) £2,500 unfavorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

59

Figure 5

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 5. Ebola's variable overhead efficiency variance would be

A) £4,000 favorable

B) £4,000 unfavorable

C) £8,000 favorable

D) £12,000 unfavorable

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 5. Ebola's variable overhead efficiency variance would be

A) £4,000 favorable

B) £4,000 unfavorable

C) £8,000 favorable

D) £12,000 unfavorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

60

Figure 5

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.

Refer to Figure 5. Ebola's variable overhead spending (expenditure)variance would be

A) £36,000 favorable

B) £36,000 unfavorable

C) £40,000 favorable

D) £40,000 unfavorable

Ebola Company has developed the following standards for one of its products:

The following activities occurred during the month of October:

The company records materials price variances at the time of purchase.Refer to Figure 5. Ebola's variable overhead spending (expenditure)variance would be

A) £36,000 favorable

B) £36,000 unfavorable

C) £40,000 favorable

D) £40,000 unfavorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

61

Taylor Company's budgeted sales were 10,000 units at £200 per unit. Actual sales were 9,200 units at £210 per unit. Taylor's sales price variance is

A) £68,000 (U).

B) £100,000 (U).

C) £8,000 (U).

D) £92,000 (F).

A) £68,000 (U).

B) £100,000 (U).

C) £8,000 (U).

D) £92,000 (F).

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

62

Figure 6

Refer to Figure 6. The variable overhead spending (expenditure) variance would be

A) £2,000 favorable

B) £1,200 favorable

C) £400 favorable

D) £200 favorable

Refer to Figure 6. The variable overhead spending (expenditure) variance would be

A) £2,000 favorable

B) £1,200 favorable

C) £400 favorable

D) £200 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

63

Lisle Manufacturing has developed the following standards for one of its products:

The company records materials price variances at the time of purchase.

During August, Lisle purchased 16,000 yards of material costing £169,600 and used 12,500 yards in its manufacturing process. There was no material inventory at August 1. Lisle recorded a total of 4,600 direct labour hours worked for a total payroll of £72,680. Lisle manufactured 1,200 units in August.

Required:

a.

Calculate the materials price variance and indicate whether it is favorable or unfavorable.

b.

Calculate the materials usage variance and indicate whether it is favorable or unfavorable.

c.

Calculate the labour rate variance and indicate whether it is favorable or unfavorable.

d.

Calculate the labour efficiency variance and indicate whether it is favorable or unfavorable.

The company records materials price variances at the time of purchase.

During August, Lisle purchased 16,000 yards of material costing £169,600 and used 12,500 yards in its manufacturing process. There was no material inventory at August 1. Lisle recorded a total of 4,600 direct labour hours worked for a total payroll of £72,680. Lisle manufactured 1,200 units in August.

Required:

a.

Calculate the materials price variance and indicate whether it is favorable or unfavorable.

b.

Calculate the materials usage variance and indicate whether it is favorable or unfavorable.

c.

Calculate the labour rate variance and indicate whether it is favorable or unfavorable.

d.

Calculate the labour efficiency variance and indicate whether it is favorable or unfavorable.

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

64

Figure 6

Refer to Figure 6. The standard rate for total overhead is

A) £14

B) £13

C) £10

D) £4

Refer to Figure 6. The standard rate for total overhead is

A) £14

B) £13

C) £10

D) £4

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

65

For planning and control purposes, fixed overhead is NOT included in the standard cost per unit because:

A) it is incurred based on the number of units produced.

B) the number of units produced do not vary from period to period.

C) it can best be controlled on a lump-sum basis.

D) of all of the above

A) it is incurred based on the number of units produced.

B) the number of units produced do not vary from period to period.

C) it can best be controlled on a lump-sum basis.

D) of all of the above

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

66

Figure 6

Refer to Figure 6. The variable overhead efficiency variance would be

A) £1,000 favorable

B) £600 favorable

C) £400 favorable

D) £200 favorable

Refer to Figure 6. The variable overhead efficiency variance would be

A) £1,000 favorable

B) £600 favorable

C) £400 favorable

D) £200 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

67

Figure 8

The following information was extracted from the accounting records of Noelle Company:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Refer to Figure 8. Noelle's fixed overhead spending (expenditure) variance would be

A) £10,000 unfavorable

B) £11,000 unfavorable

C) £21,000 favorable

D) £31,000 favorable

The following information was extracted from the accounting records of Noelle Company:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Refer to Figure 8. Noelle's fixed overhead spending (expenditure) variance would be

A) £10,000 unfavorable

B) £11,000 unfavorable

C) £21,000 favorable

D) £31,000 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

68

Figure 8

The following information was extracted from the accounting records of Noelle Company:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Refer to Figure 8. Noelle's standard fixed overhead rate is

A) £14.82

B) £14.48

C) £14.34

D) £14.00

The following information was extracted from the accounting records of Noelle Company:

Budgeted fixed overhead for the period is £420,000, and the budgeted fixed overhead rate is based on an expected capacity of 30,000 direct labour hours.

The following information is available regarding the company's operations for the period:

Refer to Figure 8. Noelle's standard fixed overhead rate is

A) £14.82

B) £14.48

C) £14.34

D) £14.00

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

69

Figure 6

Refer to Figure 6. The fixed overhead spending (expenditure) variance would be

A) £2,500 unfavorable

B) £2,500 favorable

C) £1,000 unfavorable

D) £1,000 favorable

Refer to Figure 6. The fixed overhead spending (expenditure) variance would be

A) £2,500 unfavorable

B) £2,500 favorable

C) £1,000 unfavorable

D) £1,000 favorable

Unlock Deck

Unlock for access to all 95 flashcards in this deck.

Unlock Deck

k this deck

70

Figure 7

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November:

The company records materials price variances at the time of purchase.

Refer to Figure 7. Orient's materials price variance would be

A) £22,000 unfavorable

B) £18,000 unfavorable

C) £6,000 unfavorable

D) £4,000 unfavorable

Orient Company has developed the following standards for one of its products:

The following activities occurred during the month of November: