Deck 14: Cost Management

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Larry Ltd.has developed ideal standards for four activities: labour, materials, inspection, and receiving. Information is as follows: The actual prices paid per unit of each activity driver were equal to the standard prices. The nonvalue-added costs for materials are

A) £1,575,000.

B) £157,500.

C) £150,000.

D) £75,000.

A) £1,575,000.

B) £157,500.

C) £150,000.

D) £75,000.

Question

Question

Question

Question

Sasha Cat Company sells one of its products for £100 each. Sales volume averages 750 units per year. Recently, its main competitor reduced the price of its product to £80. Sasha Cat Company expects sales to drop dramatically unless it matches the competitor's price. In addition, the current profit per unit must be maintained. Information about the product (for production of 750) is as follows: The nonvalue-added cost per unit is

A) £41.67.

B) £43.33.

C) £40.47.

D) £38.33.

A) £41.67.

B) £43.33.

C) £40.47.

D) £38.33.

Question

Question

Question

Question

Question

Question

Question

Larry Ltd.has developed ideal standards for four activities: labour, materials, inspection, and receiving. Information is as follows: The actual prices paid per unit of each activity driver were equal to the standard prices. The value-added costs for labour are

A) £900,000.

B) £792,000.

C) £84,000.

D) £75,000.

A) £900,000.

B) £792,000.

C) £84,000.

D) £75,000.

Question

Question

Larry Ltd.has developed ideal standards for four activities: labour, materials, inspection, and receiving. Information is as follows: The actual prices paid per unit of each activity driver were equal to the standard prices. The nonvalue-added costs for inspection are

A) £420,000.

B) £60,000.

C) £480,000.

D) £40,000

A) £420,000.

B) £60,000.

C) £480,000.

D) £40,000

Question

Question

Question

Question

Question

Question

Larry Ltd.has developed ideal standards for four activities: labour, materials, inspection, and receiving. Information is as follows: The actual prices paid per unit of each activity driver were equal to the standard prices. The actual costs for receiving are

A) £85,500.

B) £67,500.

C) £49,500.

D) £18,000.

A) £85,500.

B) £67,500.

C) £49,500.

D) £18,000.

Question

Question

Question

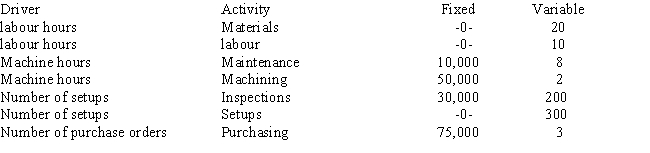

Rollo Company has developed cost formulas for the drivers of the following production activities: The activity levels are projected to be as follows:

What is budgeted for this projected activity level?

What is budgeted for this projected activity level?

A) £3,504,450

B) £1,655,430

C) £295,150

D) £165,543

What is budgeted for this projected activity level?A) £3,504,450

B) £1,655,430

C) £295,150

D) £165,543

Question

Question

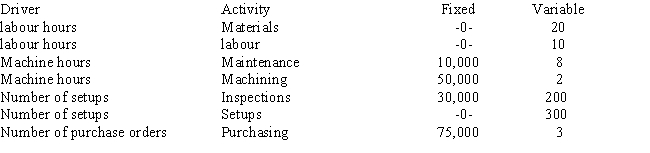

Rollo Company has developed cost formulas for the drivers of the following production activities: If the actual activity was 20 setups and the actual fixed cost for inspections was £28,000 and the variable cost for inspections was £5,000, the total variance for inspections is due to

A) favorable variance on fixed costs.

B) unfavorable variance on fixed costs.

C) favorable variance on variable costs.

D) unfavorable variance on variable costs.

A) favorable variance on fixed costs.

B) unfavorable variance on fixed costs.

C) favorable variance on variable costs.

D) unfavorable variance on variable costs.

Question

Question

Question

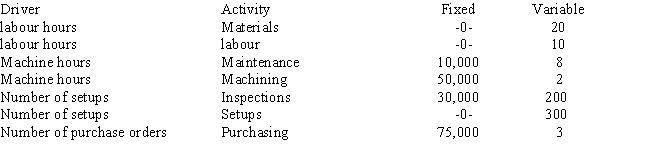

Rollo Company has developed cost formulas for the drivers of the following production activities: The budgeted inspection cost for 20 setups is

A) £175,860.

B) £40,000.

C) £34,000.

D) £30,000.

A) £175,860.

B) £40,000.

C) £34,000.

D) £30,000.

Question

Question

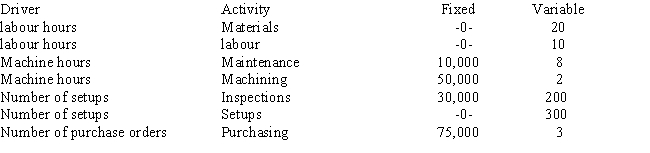

Rollo Company has developed cost formulas for the drivers of the following production activities: If the actual activity was 20 setups and the actual fixed cost for inspections was £28,000 and the variable cost for inspections was £5,000, the total variance for inspections is

A) £2,000 favorable.

B) £2,000 unfavorable.

C) £1,000 favorable.

D) £1,000 unfavorable.

A) £2,000 favorable.

B) £2,000 unfavorable.

C) £1,000 favorable.

D) £1,000 unfavorable.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Figure 1

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 1. Sammie's actual cycle time for this year would be

A) 1.8 hours per unit

B) 0.90 hours per unit

C) 0.56 hours per unit

D) 0.50 hours per unit

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 1. Sammie's actual cycle time for this year would be

A) 1.8 hours per unit

B) 0.90 hours per unit

C) 0.56 hours per unit

D) 0.50 hours per unit

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/156

Play

Full screen (f)

Deck 14: Cost Management

1

_____ are the results or products of an activity.

A) Activity inputs

B) Activity outputs

C) Cost driver analysis

D) Value-added activities

A) Activity inputs

B) Activity outputs

C) Cost driver analysis

D) Value-added activities

B

2

_____ is the effort expended to identify those factors that are the root causes of activity costs.

A) Activity inputs

B) Activity outputs

C) Cost driver analysis

D) Value-added activities

A) Activity inputs

B) Activity outputs

C) Cost driver analysis

D) Value-added activities

C

3

_____ are those activities necessary to remain in business.

A) Activity inputs

B) Activity outputs

C) Activity drivers

D) Value-added activities

A) Activity inputs

B) Activity outputs

C) Activity drivers

D) Value-added activities

D

4

_____ is an effort to reduce costs of existing products and processes.

A) Kaizen costing

B) Activity elimination

C) Activity selection

D) Activity reduction

A) Kaizen costing

B) Activity elimination

C) Activity selection

D) Activity reduction

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

5

The major source of information for the activity cost management system is

A) cost driver analysis.

B) an activity- based costing system.

C) a performance measurement system.

D) product information.

A) cost driver analysis.

B) an activity- based costing system.

C) a performance measurement system.

D) product information.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following process dimensions of the activity-based management model deals with "how well"?

A) resources

B) cost driver analysis

C) activities

D) performance measures

A) resources

B) cost driver analysis

C) activities

D) performance measures

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

7

_____ are the resources consumed by the activity in producing its output.

A) Activity inputs

B) Activity outputs

C) Cost driver analysis

D) Value-added activities

A) Activity inputs

B) Activity outputs

C) Cost driver analysis

D) Value-added activities

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following process dimensions of the activity-based management model deals with "what"?

A) resources

B) cost driver analysis

C) activities

D) performance measures

A) resources

B) cost driver analysis

C) activities

D) performance measures

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following process dimensions of the activity-based management model deals with "why"?

A) resources

B) cost driver analysis

C) activities

D) performance measures

A) resources

B) cost driver analysis

C) activities

D) performance measures

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following is NOT a necessary condition for classification as a value-added activity?

A) the activity produces no change of state

B) the change of state was not achievable by preceding activities

C) activity enables other activities to be performed

D) All of the above are necessary conditions.

A) the activity produces no change of state

B) the change of state was not achievable by preceding activities

C) activity enables other activities to be performed

D) All of the above are necessary conditions.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following is an example of a value-added activity?

A) supervision of production workers

B) inspection of products

C) scheduling of production

D) all are value-added activities

A) supervision of production workers

B) inspection of products

C) scheduling of production

D) all are value-added activities

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

12

_____ is the process of identifying, describing, and evaluating the activities an organization performs.

A) Activity inputs

B) Activity analysis

C) Cost driver analysis

D) Value-added activities

A) Activity inputs

B) Activity analysis

C) Cost driver analysis

D) Value-added activities

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

13

Nonvalue-added activities

A) are unnecessary inputs.

B) are valued outputs to internal users.

C) are valued outputs to external users.

D) help meet the organization's needs, not the product needs.

A) are unnecessary inputs.

B) are valued outputs to internal users.

C) are valued outputs to external users.

D) help meet the organization's needs, not the product needs.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following is an example of a nonvalue-added manufacturing activity?

A) assembly

B) scheduling

C) finishing

D) all are value-added activities

A) assembly

B) scheduling

C) finishing

D) all are value-added activities

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following is NOT an expected outcome of activity analysis?

A) What activities are performed?

B) How many people perform the activities?

C) The time and resources required to perform the activities

D) All of the above are expected outcomes.

A) What activities are performed?

B) How many people perform the activities?

C) The time and resources required to perform the activities

D) All of the above are expected outcomes.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

16

_____ involves choosing among various sets of activities that are caused by competing strategies.

A) Activity sharing

B) Activity elimination

C) Activity selection

D) Activity reduction

A) Activity sharing

B) Activity elimination

C) Activity selection

D) Activity reduction

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is a reason for managerial activity to be considered a value-added activity?

A) It is an enabling resource for operational activities that bring about a change of state.

B) Managing activities brings order by changing the state from uncoordinated activities to coordinated activities.

C) Both are reasons for classifying managerial activities as value-added activity.

D) Neither is a reason for classifying managerial activities as value-added activity.

A) It is an enabling resource for operational activities that bring about a change of state.

B) Managing activities brings order by changing the state from uncoordinated activities to coordinated activities.

C) Both are reasons for classifying managerial activities as value-added activity.

D) Neither is a reason for classifying managerial activities as value-added activity.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following is a value-added activity?

A) moving

B) inspection

C) processing

D) waiting

A) moving

B) inspection

C) processing

D) waiting

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

19

_____ focuses on nonvalue-added activities.

A) Activity sharing

B) Activity elimination

C) Activity selection

D) Activity reduction

A) Activity sharing

B) Activity elimination

C) Activity selection

D) Activity reduction

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

20

Activity management attempts to

A) identify and eliminate all unnecessary activities.

B) increase the efficiency of necessary activities.

C) add new activities that increase value.

D) do all of the above.

A) identify and eliminate all unnecessary activities.

B) increase the efficiency of necessary activities.

C) add new activities that increase value.

D) do all of the above.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

21

Larry Ltd.has developed ideal standards for four activities: labour, materials, inspection, and receiving. Information is as follows: The actual prices paid per unit of each activity driver were equal to the standard prices. The nonvalue-added costs for materials are

A) £1,575,000.

B) £157,500.

C) £150,000.

D) £75,000.

A) £1,575,000.

B) £157,500.

C) £150,000.

D) £75,000.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

22

A company has 20 days of finished goods inventory on hand to avoid stockouts. The carrying costs of the inventory average £5,000 per day. The value-added costs would be

A) £100,000.

B) £10,000.

C) £5,000.

D) £-0-.

A) £100,000.

B) £10,000.

C) £5,000.

D) £-0-.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

23

A company keeps 20 days of materials inventory on hand to avoid shutdowns due to materials shortages. Carrying costs average £4,000 per day. A competitor keeps 10 days of inventory on hand, and the competitor's carrying costs average £2,000 per day. The value-added costs are

A) £80,000.

B) £40,000.

C) £20,000.

D) £-0-.

A) £80,000.

B) £40,000.

C) £20,000.

D) £-0-.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

24

Value-added costs are standard costs based on

A) currently attainable standards.

B) ideal usage standards.

C) cycle time.

D) the value added.

A) currently attainable standards.

B) ideal usage standards.

C) cycle time.

D) the value added.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

25

Sasha Cat Company sells one of its products for £100 each. Sales volume averages 750 units per year. Recently, its main competitor reduced the price of its product to £80. Sasha Cat Company expects sales to drop dramatically unless it matches the competitor's price. In addition, the current profit per unit must be maintained. Information about the product (for production of 750) is as follows: The nonvalue-added cost per unit is

A) £41.67.

B) £43.33.

C) £40.47.

D) £38.33.

A) £41.67.

B) £43.33.

C) £40.47.

D) £38.33.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following focuses on the relationship of activity inputs to activity outputs?

A) activity reduction

B) quality

C) time

D) efficiency

A) activity reduction

B) quality

C) time

D) efficiency

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

27

Setup time for a product is 12 hours. A firm that uses JIT and produces the same product has reduced setup time by 1 hour. Setup labour is £20 per hour. If the company wants to reduce nonvalue-added costs by 40 percent next year, the currently attainable standard for setup time would be

A) 7.6 hours.

B) 7.2 hours.

C) 6.6 hours.

D) 4.8 hours.

A) 7.6 hours.

B) 7.2 hours.

C) 6.6 hours.

D) 4.8 hours.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

28

For nonvalue-added activities that are unnecessary, the standard quantity is

A) one.

B) zero.

C) actual quantity minus standard price.

D) actual quantity plus standard price.

A) one.

B) zero.

C) actual quantity minus standard price.

D) actual quantity plus standard price.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

29

A company keeps 20 days of materials inventory on hand to avoid shutdowns due to materials shortages. Carrying costs average £4,000 per day. A competitor keeps 10 days of inventory on hand, and the competitor's carrying costs average £2,000 per day. The nonvalue-added costs for the company are

A) £80,000.

B) £40,000.

C) £20,000.

D) £-0-.

A) £80,000.

B) £40,000.

C) £20,000.

D) £-0-.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

30

A time-and-motion study revealed that it should take 2 hours to produce a product that currently takes 6 hours to produce. labour is £8 per hour. The nonvalue-added costs are

A) £16.

B) £32.

C) £48.

D) £-0-.

A) £16.

B) £32.

C) £48.

D) £-0-.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

31

A time-and-motion study revealed that it should take 2 hours to produce a product that currently takes 6 hours to produce. labour is £8 per hour. The value-added costs are

A) £16.

B) £32.

C) £48.

D) £-0-.

A) £16.

B) £32.

C) £48.

D) £-0-.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

32

Larry Ltd.has developed ideal standards for four activities: labour, materials, inspection, and receiving. Information is as follows: The actual prices paid per unit of each activity driver were equal to the standard prices. The value-added costs for labour are

A) £900,000.

B) £792,000.

C) £84,000.

D) £75,000.

A) £900,000.

B) £792,000.

C) £84,000.

D) £75,000.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

33

A company has 20 days of finished goods inventory on hand to avoid stockouts. The carrying costs of the inventory average £5,000 per day. The nonvalue-added costs are

A) £100,000.

B) £10,000.

C) £5,000.

D) £250.

A) £100,000.

B) £10,000.

C) £5,000.

D) £250.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

34

Larry Ltd.has developed ideal standards for four activities: labour, materials, inspection, and receiving. Information is as follows: The actual prices paid per unit of each activity driver were equal to the standard prices. The nonvalue-added costs for inspection are

A) £420,000.

B) £60,000.

C) £480,000.

D) £40,000

A) £420,000.

B) £60,000.

C) £480,000.

D) £40,000

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

35

_____ decreases the time and resources required by different activities.

A) Activity sharing

B) Activity elimination

C) Activity selection

D) Activity reduction

A) Activity sharing

B) Activity elimination

C) Activity selection

D) Activity reduction

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

36

Each unit of product requires 16 pounds of material. Due to scrap and rework, each unit has been averaging 18 pounds of material. The material costs £6 per pound. If the company wants to reduce nonvalue-added costs by 25 percent next year, the currently attainable standard for material would be

A) 16.00 pounds.

B) 16.80 pounds.

C) 17.50 pounds.

D) 18.00 pounds.

A) 16.00 pounds.

B) 16.80 pounds.

C) 17.50 pounds.

D) 18.00 pounds.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

37

A firm's warranty costs are £125,000 per year. A competitor's warranty costs are £25,000 per year. The nonvalue-added costs are

A) £125,000.

B) £100,000.

C) £25,000.

D) £0.

A) £125,000.

B) £100,000.

C) £25,000.

D) £0.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

38

A time-and-motion study revealed that it should take 3 hours to produce a product that currently takes 7.5 hours to produce. labour is £18 per hour. The nonvalue-added costs are

A) £27.

B) £54.

C) £81.

D) £0.

A) £27.

B) £54.

C) £81.

D) £0.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

39

A firm's warranty costs are £125,000 per year. A competitor's warranty costs are £25,000 per year. The value-added costs are

A) £125,000.

B) £100,000.

C) £25,000.

D) £-0-.

A) £125,000.

B) £100,000.

C) £25,000.

D) £-0-.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

40

Larry Ltd.has developed ideal standards for four activities: labour, materials, inspection, and receiving. Information is as follows: The actual prices paid per unit of each activity driver were equal to the standard prices. The actual costs for receiving are

A) £85,500.

B) £67,500.

C) £49,500.

D) £18,000.

A) £85,500.

B) £67,500.

C) £49,500.

D) £18,000.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

41

Under what conditions would the activity capacity used be zero?

A) if the activity is value-added

B) if the activity is nonvalue-added

C) if the activity is discretionary

D) It would never be set at zero.

A) if the activity is value-added

B) if the activity is nonvalue-added

C) if the activity is discretionary

D) It would never be set at zero.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

42

Each unit of product requires 16 pounds of material. Due to scrap and rework, each unit has been averaging 18 pounds of material. The material costs £4 per pound. The value-added costs are

A) £4.

B) £8.

C) £64.

D) £72.

A) £4.

B) £8.

C) £64.

D) £72.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

43

Rollo Company has developed cost formulas for the drivers of the following production activities: The activity levels are projected to be as follows:

What is budgeted for this projected activity level?

A) £3,504,450

B) £1,655,430

C) £295,150

D) £165,543

What is budgeted for this projected activity level?A) £3,504,450

B) £1,655,430

C) £295,150

D) £165,543

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

44

Reengineering is another name for

A) product innovation

B) process innovation

C) process improvement

D) product improvement

A) product innovation

B) process innovation

C) process improvement

D) product improvement

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

45

Rollo Company has developed cost formulas for the drivers of the following production activities: If the actual activity was 20 setups and the actual fixed cost for inspections was £28,000 and the variable cost for inspections was £5,000, the total variance for inspections is due to

A) favorable variance on fixed costs.

B) unfavorable variance on fixed costs.

C) favorable variance on variable costs.

D) unfavorable variance on variable costs.

A) favorable variance on fixed costs.

B) unfavorable variance on fixed costs.

C) favorable variance on variable costs.

D) unfavorable variance on variable costs.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

46

Setup time for a product is 12 hours. A firm that uses JIT and produces the same product has reduced setup time to 1 hour. Setup labour is £6 per hour. The value-added costs are

A) £72.

B) £66.

C) £12.

D) £6.

A) £72.

B) £66.

C) £12.

D) £6.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

47

An activity analysis is used to determine

A) the activities an organization performs

B) how many people perform activities

C) the time and resources required to perform activities

D) all of the above

A) the activities an organization performs

B) how many people perform activities

C) the time and resources required to perform activities

D) all of the above

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

48

Rollo Company has developed cost formulas for the drivers of the following production activities: The budgeted inspection cost for 20 setups is

A) £175,860.

B) £40,000.

C) £34,000.

D) £30,000.

A) £175,860.

B) £40,000.

C) £34,000.

D) £30,000.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

49

In a continuous improvement environment, waste includes

A) inventories

B) rework

C) setup time

D) all of the above

A) inventories

B) rework

C) setup time

D) all of the above

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

50

Rollo Company has developed cost formulas for the drivers of the following production activities: If the actual activity was 20 setups and the actual fixed cost for inspections was £28,000 and the variable cost for inspections was £5,000, the total variance for inspections is

A) £2,000 favorable.

B) £2,000 unfavorable.

C) £1,000 favorable.

D) £1,000 unfavorable.

A) £2,000 favorable.

B) £2,000 unfavorable.

C) £1,000 favorable.

D) £1,000 unfavorable.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

51

The responsibility accounting system developed for operations in a continuous improvement environment would be

A) financial-based responsibility accounting

B) functional-based responsibility accounting

C) activity-based responsibility accounting

D) strategy-based responsibility accounting

A) financial-based responsibility accounting

B) functional-based responsibility accounting

C) activity-based responsibility accounting

D) strategy-based responsibility accounting

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

52

The purpose of trend reporting on nonvalue-added costs is to

A) trace resources to cost objectives.

B) assess value content.

C) define root causes.

D) see if cost reductions occurred as expected.

A) trace resources to cost objectives.

B) assess value content.

C) define root causes.

D) see if cost reductions occurred as expected.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following is not true about assigning rewards in activity-based responsibility accounting?

A) Rewards are assigned based on budgetary standards.

B) Rewards are assigned based on individual as well as team performance.

C) Rewards are assigned based on progress towards optimal standards.

D) Rewards include bonuses, profit sharing, and gainsharing.

A) Rewards are assigned based on budgetary standards.

B) Rewards are assigned based on individual as well as team performance.

C) Rewards are assigned based on progress towards optimal standards.

D) Rewards include bonuses, profit sharing, and gainsharing.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

54

A company keeps 15 days of materials inventory on hand to avoid shutdowns due to materials shortages. Carrying costs average £5,000 per day. A competitor keeps 12 days of inventory on hand, and the competitor's carrying costs average £3,000 per day. The value-added costs are

A) £5,000.

B) £-0-.

C) £30,000.

D) £75,000.

A) £5,000.

B) £-0-.

C) £30,000.

D) £75,000.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following is not an objective of activity-based management?

A) to improve decision making through better cost information

B) to increase the activity it takes to perform processes

C) to encourage cost reduction through continuous improvement

D) to increase profitability

A) to improve decision making through better cost information

B) to increase the activity it takes to perform processes

C) to encourage cost reduction through continuous improvement

D) to increase profitability

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

56

A technique for improving performance of activities and processes that searches for best practices is called

A) value-added reporting.

B) kaizen costing.

C) trend reporting.

D) benchmarking.

A) value-added reporting.

B) kaizen costing.

C) trend reporting.

D) benchmarking.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

57

Setup time for a product is 12 hours. A firm that uses JIT and produces the same product has reduced setup time to 1 hour. Setup labour is £6 per hour. The nonvalue-added costs are

A) £72.

B) £66.

C) £12.

D) £6.

A) £72.

B) £66.

C) £12.

D) £6.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

58

A technique for improving performance of activities and processes that compares the number of times an activity can be performed to the number actually performed is called

A) value-added activity reporting.

B) activity flexible budgeting.

C) activity capacity reporting.

D) activity trend reporting.

A) value-added activity reporting.

B) activity flexible budgeting.

C) activity capacity reporting.

D) activity trend reporting.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

59

Inspecting the components and the finished product is

A) necessary to assure TQM

B) a nonvalue-added activity

C) a value-added activity

D) none of the above

A) necessary to assure TQM

B) a nonvalue-added activity

C) a value-added activity

D) none of the above

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

60

Activity-based management attempts to

A) identify and eliminate all unnecessary activities

B) increase the efficiency of necessary activities

C) add new activities that increase value

D) do all of the above

A) identify and eliminate all unnecessary activities

B) increase the efficiency of necessary activities

C) add new activities that increase value

D) do all of the above

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

61

Figure 1

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 1 above. Sammie's theoretical cycle time for this year would be

A) 2.00 hours per unit

B) 1.80 hours per unit

C) 0.56 hours per unit

D) 0.50 hours per unit

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 1 above. Sammie's theoretical cycle time for this year would be

A) 2.00 hours per unit

B) 1.80 hours per unit

C) 0.56 hours per unit

D) 0.50 hours per unit

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

62

How does just-in-time manufacturing affect break-even analysis?

A) Variable costs are reduced with a corresponding increase in fixed costs.

B) Direct materials is the major variable cost.

C) Direct labour and maintenance are viewed as fixed costs.

D) all of the above

A) Variable costs are reduced with a corresponding increase in fixed costs.

B) Direct materials is the major variable cost.

C) Direct labour and maintenance are viewed as fixed costs.

D) all of the above

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

63

Product life-cycle costs do NOT include which of the following?

A) development costs

B) production costs

C) costs of logistics support

D) All of the above are life-cycle costs.

A) development costs

B) production costs

C) costs of logistics support

D) All of the above are life-cycle costs.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

64

Which of the following is TRUE about a manufacturing cell?

A) There is increased movement of work in process.

B) It usually produces a particular product or product family.

C) Workers are highly specialized.

D) Supervision is important.

A) There is increased movement of work in process.

B) It usually produces a particular product or product family.

C) Workers are highly specialized.

D) Supervision is important.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

65

The demand-pull system requires goods to be manufactured based on the

A) current demand

B) anticipated demand

C) previous year's demand

D) average of the next five years' demand

A) current demand

B) anticipated demand

C) previous year's demand

D) average of the next five years' demand

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

66

Life-cycle cost management is particularly important for firms that have

A) short life cycles because those firms have less opportunity to take advantage of the time value of money

B) long life cycles because those firms have more opportunity to take advantage of the time value of money

C) long life cycles because those firms have more opportunity to enhance profit performance through product redesign or cost reduction

D) short life cycles because those firms have less opportunity to enhance profit performance through product redesign or cost reduction

A) short life cycles because those firms have less opportunity to take advantage of the time value of money

B) long life cycles because those firms have more opportunity to take advantage of the time value of money

C) long life cycles because those firms have more opportunity to enhance profit performance through product redesign or cost reduction

D) short life cycles because those firms have less opportunity to enhance profit performance through product redesign or cost reduction

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

67

Figure 1

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 1. Sammie's goal for defective units as a percentage of total units produced would be

A) 3.0%

B) 2.5%

C) 1.5%

D) 0%

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 1. Sammie's goal for defective units as a percentage of total units produced would be

A) 3.0%

B) 2.5%

C) 1.5%

D) 0%

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

68

Kaizen costing is

A) continuous improvement with the objective of cost reduction

B) characterized by constant improvements to existing processes and products

C) characterized by incremental improvement to existing processes and products

D) all of the above

A) continuous improvement with the objective of cost reduction

B) characterized by constant improvements to existing processes and products

C) characterized by incremental improvement to existing processes and products

D) all of the above

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

69

The majority of the product cost is "locked in" during which of the following life-cycle stages?

A) Introduction

B) Growth

C) Development

D) Decline

A) Introduction

B) Growth

C) Development

D) Decline

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

70

Which of the following stages comes first?

A) Introduction

B) Growth

C) Development

D) Decline

A) Introduction

B) Growth

C) Development

D) Decline

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

71

Figure 1

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 1. Sammie's actual cycle time for this year would be

A) 1.8 hours per unit

B) 0.90 hours per unit

C) 0.56 hours per unit

D) 0.50 hours per unit

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 1. Sammie's actual cycle time for this year would be

A) 1.8 hours per unit

B) 0.90 hours per unit

C) 0.56 hours per unit

D) 0.50 hours per unit

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

72

Figure 1

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 1 above. Sammie's defective units as a percentage of total units produced would be

A) 3.16%

B) 3.00%

C) 1.67%

D) 1.50%

At the beginning of this year, Sammie Company installed a JIT purchasing and manufacturing system. The following information has been gathered about one of the company's products:

Refer to Figure 1 above. Sammie's defective units as a percentage of total units produced would be

A) 3.16%

B) 3.00%

C) 1.67%

D) 1.50%

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

73

Which of the following describes a kaizen cost reduction process?

A) It has two process cycles, namely, continuous improvement and maintenance.

B) It includes a kaizen standard, which is an ideal standard.

C) A maximum standard is set for future performance based on the current kaizen standard attained.

D) both a and c

A) It has two process cycles, namely, continuous improvement and maintenance.

B) It includes a kaizen standard, which is an ideal standard.

C) A maximum standard is set for future performance based on the current kaizen standard attained.

D) both a and c

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

74

Benchmarking

A) is an approach to standard setting that is used to identify opportunities for activity improvement

B) uses best practices as the standard for evaluating activity performance

C) Both a and b are correct.

D) Neither a nor b is correct.

A) is an approach to standard setting that is used to identify opportunities for activity improvement

B) uses best practices as the standard for evaluating activity performance

C) Both a and b are correct.

D) Neither a nor b is correct.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

75

According to the life-cycle cost budgeting model, 90 percent of costs are incurred during the

A) development stage

B) production stage

C) postproduction stage

D) logistics support stage

A) development stage

B) production stage

C) postproduction stage

D) logistics support stage

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

76

In comparison to a traditional environment, a JIT environment has more overhead assigned by

A) direct tracing

B) driver tracing

C) allocation

D) Overhead assignment is the same between traditional and JIT.

A) direct tracing

B) driver tracing

C) allocation

D) Overhead assignment is the same between traditional and JIT.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

77

The strategic objectives of JIT are

A) to increase profits

B) to improve a firm's competitive position

C) both a and b

D) neither a nor b

A) to increase profits

B) to improve a firm's competitive position

C) both a and b

D) neither a nor b

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

78

The just-in-time (JIT) approach to inventory management

A) allows greater flexibility as to when products can be manufactured

B) results in higher inventory levels but reduces ordering and setup costs

C) results in lower inventory carrying costs

D) None of the above are correct.

A) allows greater flexibility as to when products can be manufactured

B) results in higher inventory levels but reduces ordering and setup costs

C) results in lower inventory carrying costs

D) None of the above are correct.

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

79

Cell workers have responsibility over

A) multiple tasks within the cell

B) providing input for continuous improvement

C) support activities within the cell

D) all of the above

A) multiple tasks within the cell

B) providing input for continuous improvement

C) support activities within the cell

D) all of the above

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

80

A target cost is

A) the standard cost

B) the difference between the sales price needed to capture a predetermined market share and the desired per-unit profit

C) the long-run average cost over the life cycle of the product

D) none of the above

A) the standard cost

B) the difference between the sales price needed to capture a predetermined market share and the desired per-unit profit

C) the long-run average cost over the life cycle of the product

D) none of the above

Unlock Deck

Unlock for access to all 156 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 156 flashcards in this deck.