Deck 5: Intercompany Transactions: Bonds and Leases

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

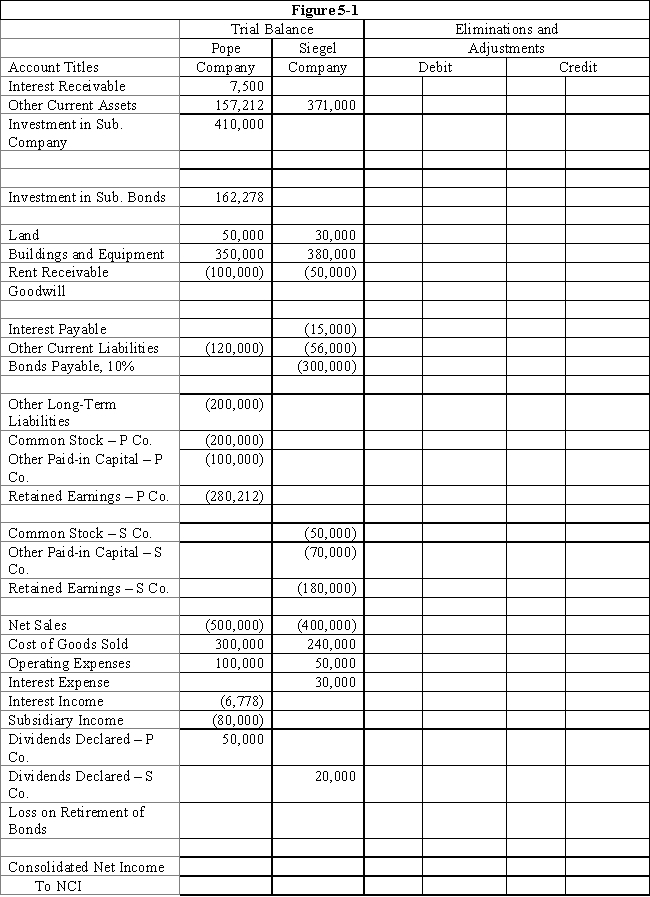

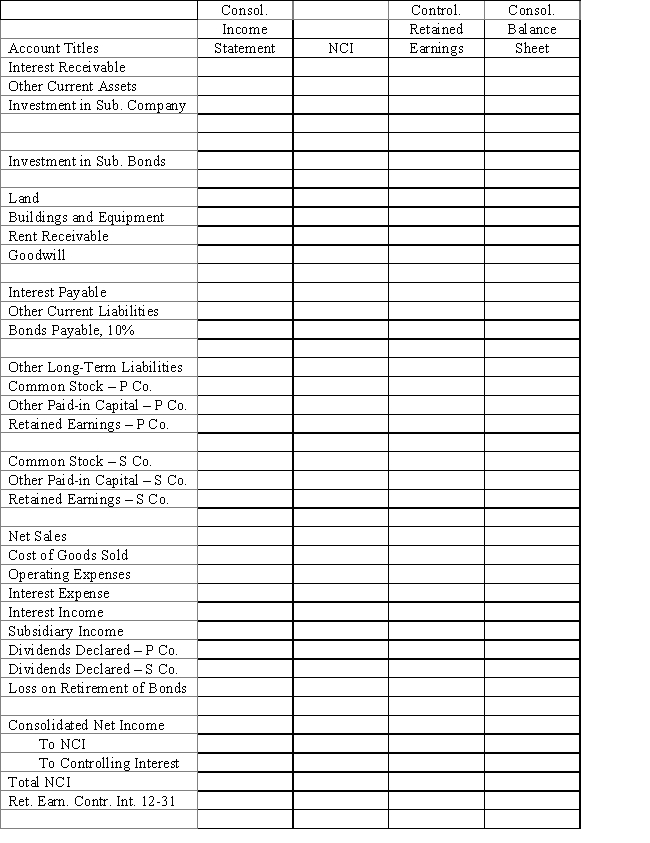

On January 1, 2016, Pope Company acquired 100% of the common stock of Siegel Company for $300,000.On this date Siegel had total owners' equity of $250,000.Any excess of cost over book value is attributable to goodwill.Pope accounts for its investment in Siegel using the simple equity method.

?

On July 1, 2016, Siegel Company sold to outside investors $300,000 par value of 10-year, 10% bonds.The price received was equal to par.The bonds pay interest semi-annually on July 1 and January 1.

?

During early 2019, market interest rates on bonds similar to those issued by Siegel decreased to 8%.As a result, the market value of the bonds increased.On July 1, 2019, Pope purchased $150,000 par value of Siegel's bonds, paying $163,000.Pope still holds the bonds on December 31, 2019 and has amortized the premium, using the straight-line method.

?

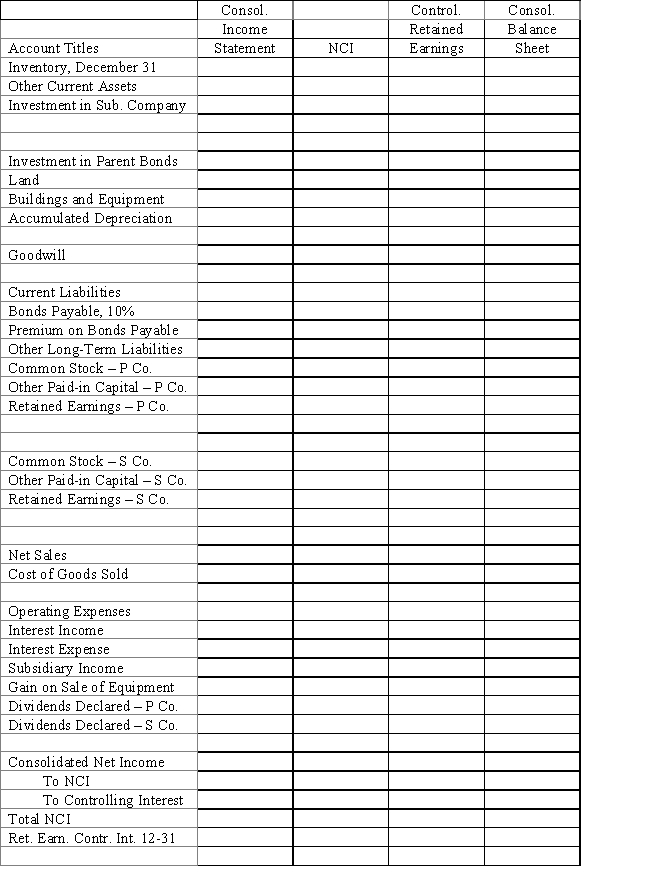

Required:

?

Complete the Figure 5-1 worksheet for consolidated financial statements for the year ended December 31, 2019.Round all computations to the nearest dollar.

?

?

?

?

?

On July 1, 2016, Siegel Company sold to outside investors $300,000 par value of 10-year, 10% bonds.The price received was equal to par.The bonds pay interest semi-annually on July 1 and January 1.

?

During early 2019, market interest rates on bonds similar to those issued by Siegel decreased to 8%.As a result, the market value of the bonds increased.On July 1, 2019, Pope purchased $150,000 par value of Siegel's bonds, paying $163,000.Pope still holds the bonds on December 31, 2019 and has amortized the premium, using the straight-line method.

?

Required:

?

Complete the Figure 5-1 worksheet for consolidated financial statements for the year ended December 31, 2019.Round all computations to the nearest dollar.

?

??

Question

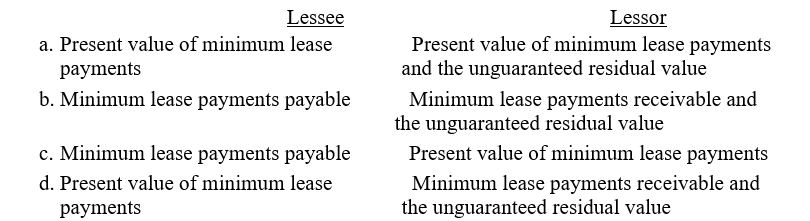

What is recorded by the lessee and the lessor when an intercompany lease contains an unguaranteed residual value? ?

Question

Question

Question

Question

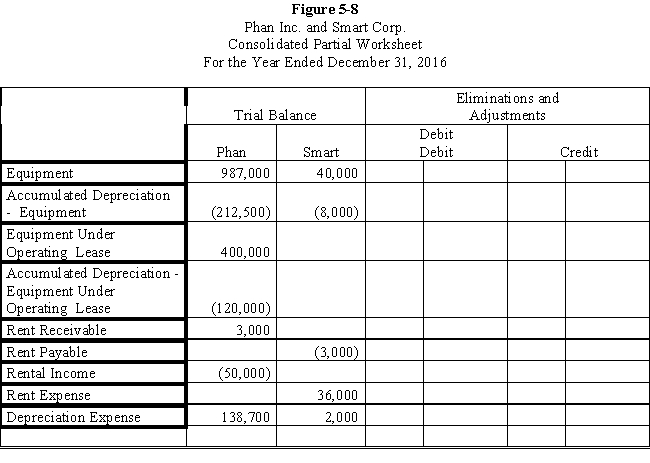

Smart Corporation is a 90%-owned subsidiary of Phan Inc.On January 2, 2016, Smart agreed to lease $400,000 of construction equipment from Phan for $3,000 a month on an operating lease.The equipment has a 10-year life and is being depreciated using the straight-line method.

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-8 partial worksheet for December 31, 2016.Key and explain all eliminations and adjustments.

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-8 partial worksheet for December 31, 2016.Key and explain all eliminations and adjustments.

Question

On January 1, 2016 Parent Company acquired 90% of the common stock of Subsidiary Company for $360,000.On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively.Any excess of cost over book value is due to goodwill.Parent accounts for the Investment in Subsidiary using the simple equity method.

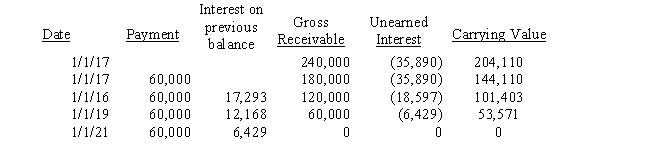

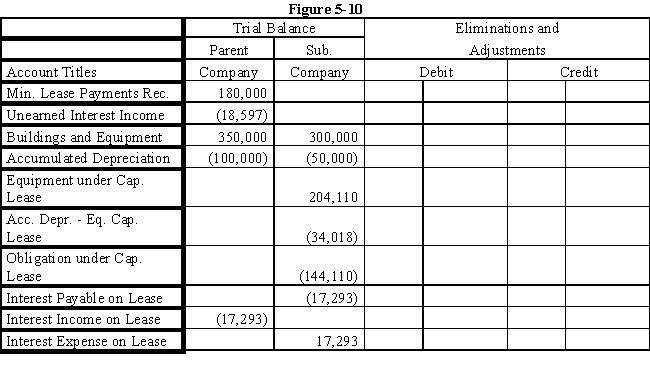

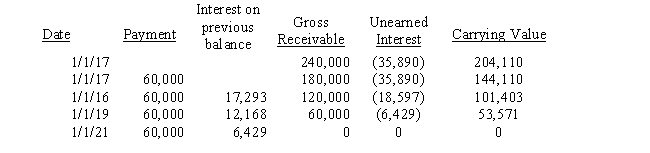

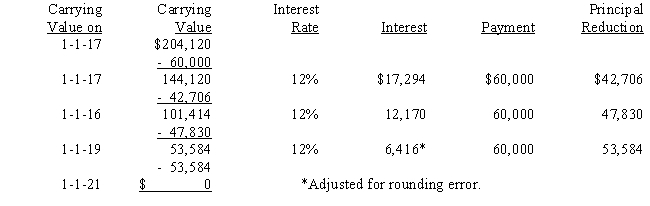

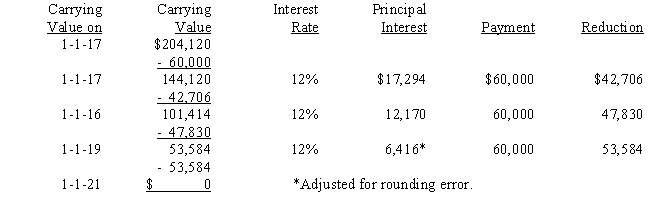

On January 1, 2017, Parent purchased equipment for $204,110 and immediately leased the equipment to Subsidiary on a 4-year lease.The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.The lease amortization schedule is presented below:

Required:

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-10 partial worksheet as of December 31, 2017.Key and explain all eliminations and adjustments.

On January 1, 2017, Parent purchased equipment for $204,110 and immediately leased the equipment to Subsidiary on a 4-year lease.The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.The lease amortization schedule is presented below:

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-10 partial worksheet as of December 31, 2017.Key and explain all eliminations and adjustments.

Question

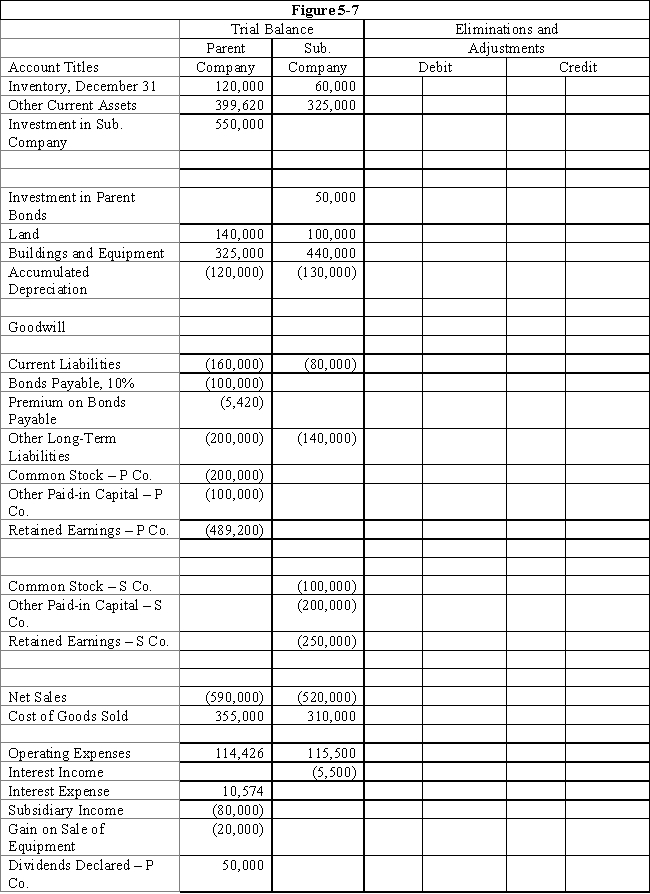

On January 1, 2016, Parent Company purchased 80% of the common stock of Subsidiary Company for $402,000.On this date Subsidiary had total owners' equity of $440,000.Any excess of cost over book value is due to goodwill.Parent accounts for its investment in Subsidiary using the simple equity method.

?

On January 1, 2016, Parent held merchandise acquired from Subsidiary for $50,000.During 2016, Subsidiary sold merchandise to Parent for $120,000, of which Parent holds $30,000 on December 31, 2016.Subsidiary's gross profit on sales is 40%.On December 31, 2016, Parent still owes Subsidiary $5,000 for merchandise.

?

On December 31, 2016, Parent sold $100,000 par value of 11%, 10-year bonds for $106,232, which resulted in an effective interest rate of 10%.The bonds pay interest semi-annually on June 30 and December 31.Parent uses the effective-interest method of amortization for the premium.

?

An amortization table for 2017 and 2016 is presented below:

?

?

On December 31, 2017, Subsidiary repurchased $50,000 par value of the bonds, paying a price equal to par.The bonds are still held on December 31, 2016.

?

On December 31, 2016, Parent sold equipment with a cost of $50,000 and accumulated depreciation of $30,000 to Subsidiary for $40,000.Subsidiary will use the equipment beginning in 2019.

?

Required:

?

Complete the Figure 5-7 worksheet for consolidated financial statements for the year ended December 31, 2016.Round all computations to the nearest dollar.

?

?

On January 1, 2016, Parent held merchandise acquired from Subsidiary for $50,000.During 2016, Subsidiary sold merchandise to Parent for $120,000, of which Parent holds $30,000 on December 31, 2016.Subsidiary's gross profit on sales is 40%.On December 31, 2016, Parent still owes Subsidiary $5,000 for merchandise.

?

On December 31, 2016, Parent sold $100,000 par value of 11%, 10-year bonds for $106,232, which resulted in an effective interest rate of 10%.The bonds pay interest semi-annually on June 30 and December 31.Parent uses the effective-interest method of amortization for the premium.

?

An amortization table for 2017 and 2016 is presented below:

?

?

On December 31, 2017, Subsidiary repurchased $50,000 par value of the bonds, paying a price equal to par.The bonds are still held on December 31, 2016.

?

On December 31, 2016, Parent sold equipment with a cost of $50,000 and accumulated depreciation of $30,000 to Subsidiary for $40,000.Subsidiary will use the equipment beginning in 2019.

?

Required:

?

Complete the Figure 5-7 worksheet for consolidated financial statements for the year ended December 31, 2016.Round all computations to the nearest dollar.

?

Question

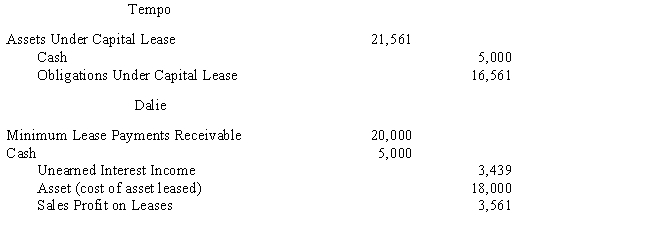

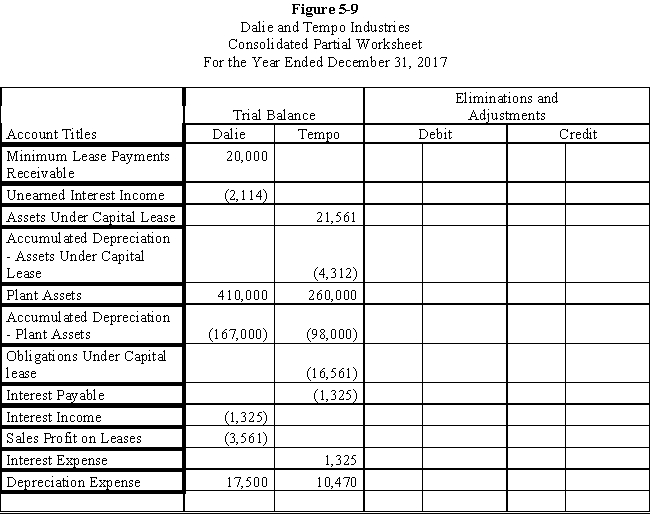

Tempo Industries is an 80%-owned subsidiary of Dalie Inc.On January 1, 2017, Dalie leased an asset to Tempo and the following journal entries were made:

?

?

The terms of the lease agreement require Tempo to make five payments of $5,000 each at the beginning of each year.The implicit interest rate used by both Dalie and Tempo is 8%.

The terms of the lease agreement require Tempo to make five payments of $5,000 each at the beginning of each year.The implicit interest rate used by both Dalie and Tempo is 8%.

?

Required:

?

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-9 partial worksheet of December 31, 2017.Key and explain all eliminations and adjustments.

?

?

?

?

The terms of the lease agreement require Tempo to make five payments of $5,000 each at the beginning of each year.The implicit interest rate used by both Dalie and Tempo is 8%.?

Required:

?

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-9 partial worksheet of December 31, 2017.Key and explain all eliminations and adjustments.

?

?

Question

Question

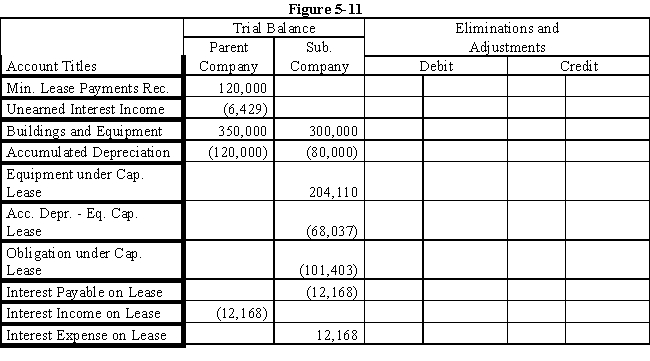

On January 1, 2016, Parent Company acquired 90% of the common stock of Subsidiary Company for $360,000.On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively.Any excess of cost over book value is due to goodwill.Parent uses the simple equity method to account for its investment in subsidiary.

On January 1, 2017, Parent purchased equipment for $204,110 and immediately leased the equipment to Subsidiary on a 4-year lease.The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.A lease amortization schedule, applicable to either company, is presented below:

Required:

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-11 partial worksheet as of December 31, 2016.Key and explain all eliminations and adjustments.

On January 1, 2017, Parent purchased equipment for $204,110 and immediately leased the equipment to Subsidiary on a 4-year lease.The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.A lease amortization schedule, applicable to either company, is presented below:

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-11 partial worksheet as of December 31, 2016.Key and explain all eliminations and adjustments.

Question

Question

Question

Question

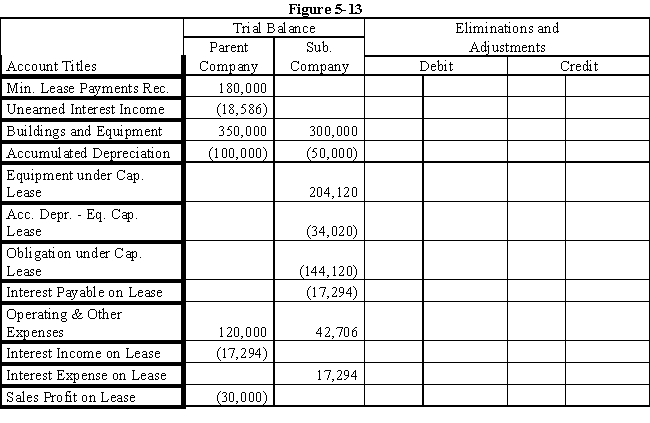

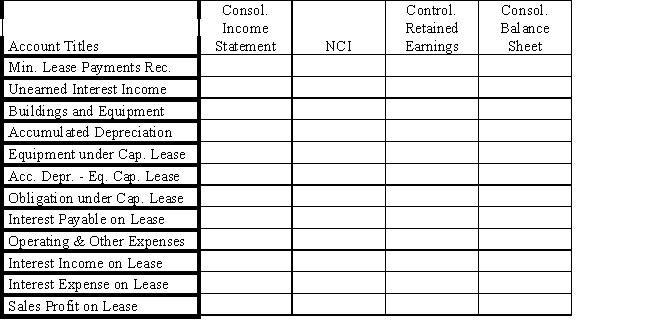

On January 1, 2016, Parent Company acquired 100% of the common stock of Subsidiary Company for $365,000.On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively.Any excess of cost over book value is due to goodwill.Parent uses the simple equity method to account for its investment in subsidiary.

?

On January 1, 2017, Parent purchased equipment for $174,120 and immediately leased the equipment to Subsidiary on a 4-year lease.The transaction was legally structured as a sales-type lease with a present value for the minimum lease payments of $204,120.Parent recorded the following entry:

?

?

The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.

?

A lease amortization schedule, applicable to either company, is presented below:

?

?

Required:

Required:

?

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-13 partial worksheet as of December 31, 2017.Key and explain all eliminations and adjustments.

?

?

?

On January 1, 2017, Parent purchased equipment for $174,120 and immediately leased the equipment to Subsidiary on a 4-year lease.The transaction was legally structured as a sales-type lease with a present value for the minimum lease payments of $204,120.Parent recorded the following entry:

?

?

The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.

?

A lease amortization schedule, applicable to either company, is presented below:

?

?

Required:?

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-13 partial worksheet as of December 31, 2017.Key and explain all eliminations and adjustments.

?

?

Question

Question

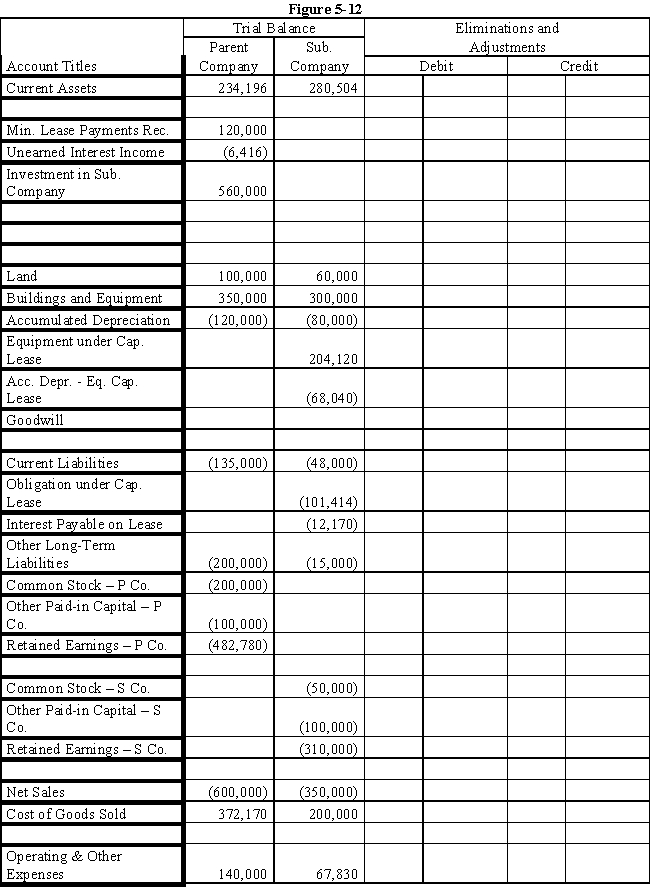

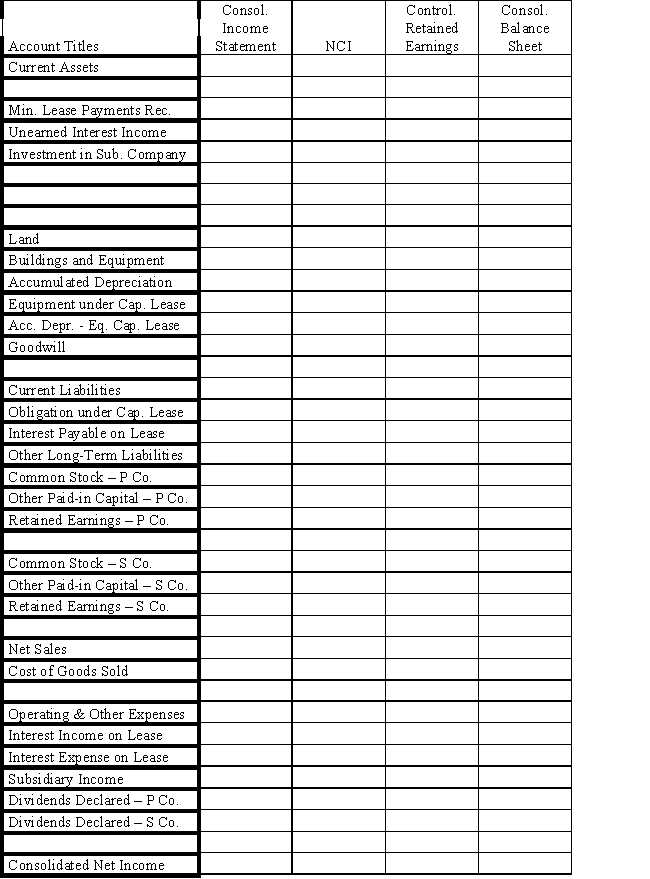

On January 1, 2016, Parent Company purchased 100% of the common stock of Subsidiary Company for $390,000.On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively.Any excess of cost over book value is due to goodwill.Parent accounts for the Investment in Subsidiary using the simple equity method.

On January 1, 2017, Parent purchased equipment for $204,120 and immediately leased the equipment to Subsidiary on a 4-year lease.The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.

A lease amortization schedule, applicable to either company, is presented below:

On January 1, 2016, Parent held merchandise acquired from Subsidiary for $10,000.During 2016, subsidiary sold merchandise to Parent for $50,000, of which $15,000 is held by Parent on December 31, 2016.Subsidiary's usual gross profit on affiliated sales is 40%.

On January 1, 2016, Parent held merchandise acquired from Subsidiary for $10,000.During 2016, subsidiary sold merchandise to Parent for $50,000, of which $15,000 is held by Parent on December 31, 2016.Subsidiary's usual gross profit on affiliated sales is 40%.

Required:

Complete the Figure 5-12 worksheet for consolidated financial statements for the year ended December 31, 2016.Round all computations to the nearest dollar.

On January 1, 2017, Parent purchased equipment for $204,120 and immediately leased the equipment to Subsidiary on a 4-year lease.The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.

A lease amortization schedule, applicable to either company, is presented below:

On January 1, 2016, Parent held merchandise acquired from Subsidiary for $10,000.During 2016, subsidiary sold merchandise to Parent for $50,000, of which $15,000 is held by Parent on December 31, 2016.Subsidiary's usual gross profit on affiliated sales is 40%.

Required:

Complete the Figure 5-12 worksheet for consolidated financial statements for the year ended December 31, 2016.Round all computations to the nearest dollar.

Question

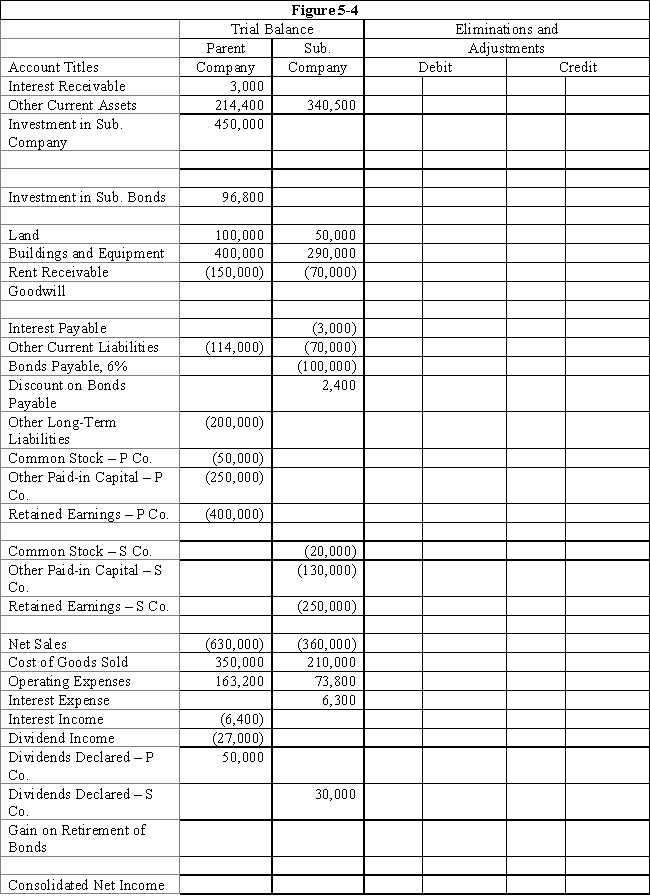

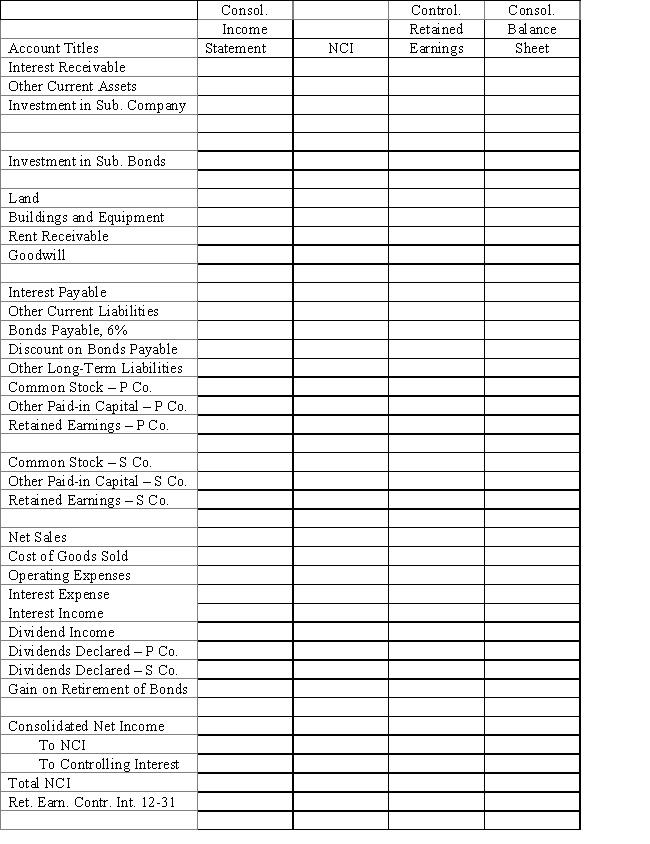

On January 1, 2019, Parent Company purchased 90% of the common stock of Subsidiary Company for $450,000.On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $20,000, $130,000, and $200,000, respectively.Any excess of cost over book value is due to goodwill.Parent accounts for the Investment in Subsidiary using the cost method.

?

On January 1, 2019, Subsidiary sold $100,000 par value of 6%, ten-year bonds for $97,000.The bonds pay interest semi-annually on January 1 and July 1 of each year.

?

On January 1, 2021, Parent repurchased all of Subsidiary's bonds for $96,400.The bonds are still held on December 31, 2021.

?

Both companies have correctly recorded all entries relative to bonds and interest, using straight-line amortization for premium or discount.

?

Required:

?

Complete the Figure 5-4 worksheet for consolidated financial statements for the year ended of December 31, 2021.Round all computations to the nearest dollar.

?

?

On January 1, 2019, Subsidiary sold $100,000 par value of 6%, ten-year bonds for $97,000.The bonds pay interest semi-annually on January 1 and July 1 of each year.

?

On January 1, 2021, Parent repurchased all of Subsidiary's bonds for $96,400.The bonds are still held on December 31, 2021.

?

Both companies have correctly recorded all entries relative to bonds and interest, using straight-line amortization for premium or discount.

?

Required:

?

Complete the Figure 5-4 worksheet for consolidated financial statements for the year ended of December 31, 2021.Round all computations to the nearest dollar.

?

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/54

Play

Full screen (f)

Deck 5: Intercompany Transactions: Bonds and Leases

1

Company S is a 100%-owned subsidiary of Company P.Company P purchased all the outstanding bonds of Company S at a discount.The bonds had a remaining issuance premium at the time of Company P's purchase.The bonds have 5 years to maturity.At the end of 5 years, consolidated retained earnings:

A)is greater as a result of the purchase.

B)is less as a result of the purchase.

C)is not affected by the purchase.

D)cannot be determined from the information provided.

A)is greater as a result of the purchase.

B)is less as a result of the purchase.

C)is not affected by the purchase.

D)cannot be determined from the information provided.

C

2

Company S is a 100%-owned subsidiary of Company P.Company P purchased, at a premium, Company S bonds that are outstanding and have a remaining discount.Consolidation theory takes the position that:

A)interest expense should be adjusted to reflect the market value of the bonds on the date of Company P's purchase.

B)the debt has been retired at a loss.

C)the debt is outstanding but should be shown at face value.

D)the gain or loss on retirement should be allocated over the remaining life of the bonds.

A)interest expense should be adjusted to reflect the market value of the bonds on the date of Company P's purchase.

B)the debt has been retired at a loss.

C)the debt is outstanding but should be shown at face value.

D)the gain or loss on retirement should be allocated over the remaining life of the bonds.

B

3

When one member of a consolidated group purchases only part of the outstanding bonds of another member of the group (for example, 80% of the bonds),

A)all bonds, and all the interest expense and interest revenue applicable to the bonds should be eliminated.

B)20% of the bonds, and 20% the interest expense and interest revenue applicable to the bonds should be eliminated.

C)80% of the bonds, and 80% the interest expense and interest revenue applicable to the bonds should be eliminated.

D)none of the bonds, and none of the interest expense and interest revenue applicable to the bonds should be eliminated.

A)all bonds, and all the interest expense and interest revenue applicable to the bonds should be eliminated.

B)20% of the bonds, and 20% the interest expense and interest revenue applicable to the bonds should be eliminated.

C)80% of the bonds, and 80% the interest expense and interest revenue applicable to the bonds should be eliminated.

D)none of the bonds, and none of the interest expense and interest revenue applicable to the bonds should be eliminated.

C

4

Elimination procedures for intercompany bonds purchased from outside parties by another member of the consolidated group are:

A)not needed except in the period of acquisition if purchased at par.

B)not needed except in the period of acquisition if purchased at a premium or discount.

C)not needed except in the period of acquisition if only a portion of the outstanding bonds are purchased.

D)needed each period as long as the intercompany investment in bonds exists.

A)not needed except in the period of acquisition if purchased at par.

B)not needed except in the period of acquisition if purchased at a premium or discount.

C)not needed except in the period of acquisition if only a portion of the outstanding bonds are purchased.

D)needed each period as long as the intercompany investment in bonds exists.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

5

The usual impetus for transactions that create a long-term debtor-creditor relationship between members of a consolidated group is due to the:

A)subsidiary's ability to borrow larger amounts of capital at more favorable terms than would be available to the parent.

B)parent's ability to borrow larger amounts of capital at more favorable terms than would be available to the subsidiary.

C)parent's desire to decentralize asset management and credit control.

D)parent's desire to eliminate long-term debt.

A)subsidiary's ability to borrow larger amounts of capital at more favorable terms than would be available to the parent.

B)parent's ability to borrow larger amounts of capital at more favorable terms than would be available to the subsidiary.

C)parent's desire to decentralize asset management and credit control.

D)parent's desire to eliminate long-term debt.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

6

Company P owns 80% of Company S.On January 1, 2016 Company S has outstanding 6% bonds with a face value of $200,000 and an unamortized discount of $3,000, which is being amortized on a straight-line basis over a remaining term of 10 years.On January 1, 2016, Company P purchased all the bonds for $205,000.The premium also is amortized on a straight-line basis.The net impact of the purchase on the non-controlling interest as of December 31, 2016, is ____.

A)$(8,000)

B)$(1,600)

C)$(1,440)

D)$(1,200)

A)$(8,000)

B)$(1,600)

C)$(1,440)

D)$(1,200)

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

7

Company S is a 100%-owned subsidiary of Company P.On January 1, 2016, Company S has $100,000 of 8% face rate bonds outstanding.The bonds had 5 years to maturity on January 1, 2016, and had an unamortized discount of $5,000.On that date, Company P purchased the bonds for $99,000.The net adjustment needed to consolidate retained earnings on December 31, 2016 is ____.

A)$(4,000)

B)$(3,200)

C)$(800)

D)$0

A)$(4,000)

B)$(3,200)

C)$(800)

D)$0

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

8

Sun Company is a 100%-owned subsidiary of Peter Company.On January 1, 2016, Sun Company has $500,000 of 8% face rate bonds outstanding, with an unamortized discount of $5,000 that is being amortized over a 5 year remaining life to maturity.On that date, Peter Company purchased the bonds for $497,000.The adjustment to the consolidated income of the two companies needed in the consolidation process for 2017 (the following year) is ____.

A)$2,800 increase

B)$400 decrease

C)$400 increase

D)$2,800 decrease

A)$2,800 increase

B)$400 decrease

C)$400 increase

D)$2,800 decrease

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

9

Powell Company owns an 80% interest in Sauter, Inc.On January 1, 2016, Sauter issued $400,000 of 10-year, 12% bonds at a premium of $50,000.On December 31, 2021, 5 years after original issuance, Powell purchased all of the outstanding bonds for $390,000.Both firms use the straight-line method of amortization.

The interest adjustment in the 2021 subsidiary income distribution schedule is ____.

A)$2,000

B)$5,000

C)$4,500

D)$0

The interest adjustment in the 2021 subsidiary income distribution schedule is ____.

A)$2,000

B)$5,000

C)$4,500

D)$0

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

10

Company S is a 100%-owned subsidiary of Company P.Company S has outstanding 6%, 10-year bonds sold to yield 7%.On January 1 of the current year, Company P purchased all of the Company S outstanding bonds at a price that reflected the current 6% effective interest rate.How should this event be reflected in the current year's consolidated statements?

A)The bonds remain in the balance sheet and are accounted for at a 7% effective rate.

B)The bonds remain in the balance sheet and are accounted for at a 9% effective rate.

C)Retirement of the bonds at a gain as of the purchase date.

D)Retirement of the bonds at a loss as of the purchase date.

A)The bonds remain in the balance sheet and are accounted for at a 7% effective rate.

B)The bonds remain in the balance sheet and are accounted for at a 9% effective rate.

C)Retirement of the bonds at a gain as of the purchase date.

D)Retirement of the bonds at a loss as of the purchase date.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

11

In the year when one member of a consolidated group purchases from outside parties the bonds of another affiliate, the consolidated income statement includes:

A)a gain if purchased above book value.

B)a gain if purchased below book value.

C)a loss if purchased below book value.

D)a deferred gain if purchased above book value.

A)a gain if purchased above book value.

B)a gain if purchased below book value.

C)a loss if purchased below book value.

D)a deferred gain if purchased above book value.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

12

Company S is a 100%-owned subsidiary of Company P.Company S has outstanding 6%, 10-year bonds sold to yield 7%.On January 1 of the current year, Company P purchased all of the Company S outstanding bonds at a price that reflected the current 9% effective interest rate.How should this event be reflected in the current year's consolidated statements?

A)The bonds remain in the balance sheet and are accounted for at a 7% effective rate.

B)The bonds remain in the balance sheet and are accounted for at a 9% effective rate.

C)Retirement of the bonds at a gain as of the purchase date.

D)Retirement of the bonds at a loss as of the purchase date.

A)The bonds remain in the balance sheet and are accounted for at a 7% effective rate.

B)The bonds remain in the balance sheet and are accounted for at a 9% effective rate.

C)Retirement of the bonds at a gain as of the purchase date.

D)Retirement of the bonds at a loss as of the purchase date.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

13

On an income distribution schedule, any gain or loss resulting from intercompany bonds is charged to

A)the issuer of the bonds.

B)the purchaser of the bonds.

C)allocation between the issuer and the purchaser.

D)none of the above

A)the issuer of the bonds.

B)the purchaser of the bonds.

C)allocation between the issuer and the purchaser.

D)none of the above

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

14

A subsidiary has outstanding $100,000 of 8% bonds that were issued at face value.The parent purchased all the bonds for $96,000 with 5 years remaining to maturity.How will the parent's use of the effective interest amortization rather than straight-line amortization of the discount affect the consolidated financial statements?

A)The consolidated financial statements report the same information whether the parent uses straight-line or effective interest amortization on its investment in sub's bonds.

B)Will result in a different gain on retirement

C)Will result in more interest expense in the first year after the intercompany purchase.

D)Will result in less interest expense in the first year after the intercompany purchase.

A)The consolidated financial statements report the same information whether the parent uses straight-line or effective interest amortization on its investment in sub's bonds.

B)Will result in a different gain on retirement

C)Will result in more interest expense in the first year after the intercompany purchase.

D)Will result in less interest expense in the first year after the intercompany purchase.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

15

The motivation of a parent company to purchase the outstanding bonds of a subsidiary could be to:

A)replace the existing debt with new debt at a lower interest rate.

B)reduce the parent company's acquisition price for the subsidiary.

C)increase the parent company's ownership percentage in the subsidiary.

D)create interest revenue to offset interest expense in future income statements.

A)replace the existing debt with new debt at a lower interest rate.

B)reduce the parent company's acquisition price for the subsidiary.

C)increase the parent company's ownership percentage in the subsidiary.

D)create interest revenue to offset interest expense in future income statements.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

16

In years subsequent to the year one member of a consolidated group purchases another member's outstanding bonds from outside parties, Consolidated Income Statements:

A)recognize a prorated share of any gain or loss from intercompany bonds.

B)recognize a prorated share of any gain but would not show a share of a loss from intercompany bonds.

C)recognize a prorated share of any loss but would not show a share of a gain from intercompany bonds.

D)would not recognize any gain or loss from intercompany bonds.

A)recognize a prorated share of any gain or loss from intercompany bonds.

B)recognize a prorated share of any gain but would not show a share of a loss from intercompany bonds.

C)recognize a prorated share of any loss but would not show a share of a gain from intercompany bonds.

D)would not recognize any gain or loss from intercompany bonds.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

17

Company S is a 100%-owned subsidiary of Company P.Company S has outstanding 8%, 10-year bonds sold to yield 7%.On January 1 of the current year, Company P purchased all of the Company S outstanding bonds at a price that reflected the current 9% effective interest rate.How should this event be reflected in the current year's consolidated statements?

A)The bonds remain in the balance sheet and are accounted for at a 7% effective rate.

B)The bonds remain in the balance sheet and are accounted for at a 9% effective rate.

C)Retirement of the bonds at a gain as of the purchase date.

D)Retirement of the bonds at a loss as of the purchase date.

A)The bonds remain in the balance sheet and are accounted for at a 7% effective rate.

B)The bonds remain in the balance sheet and are accounted for at a 9% effective rate.

C)Retirement of the bonds at a gain as of the purchase date.

D)Retirement of the bonds at a loss as of the purchase date.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

18

Intercompany debt that must be eliminated from consolidated financial statements may result from:

A)one member of a consolidated group selling its bonds directly to another member of the group.

B)one member of a consolidated group advancing funds to another member of the group so that the member may retire bonds it had issued to outside parties.

C)one member of a consolidated group purchasing bonds from outside parties as an investment that had been issued to outside parities by another member of the group.

D)all of the above.

A)one member of a consolidated group selling its bonds directly to another member of the group.

B)one member of a consolidated group advancing funds to another member of the group so that the member may retire bonds it had issued to outside parties.

C)one member of a consolidated group purchasing bonds from outside parties as an investment that had been issued to outside parities by another member of the group.

D)all of the above.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

19

Company S is a 100%-owned subsidiary of Company P.On January 1, 2019, Company S has $200,000 of 8% face rate bonds outstanding, which were issued at face value.The bonds had 5 years to maturity on January 1, 2019.Premiums or discounts would be amortized on a straight-line basis.On that date, Company P purchased the bonds for $198,000.The amount on the consolidated balance sheet relative to the debt is:

A)bonds payable $200,000.

B)bonds payable $200,000, discount $2,000.

C)bonds payable $200,000, discount $1,600.

D)The bonds do not appear on the consolidated balance sheet.

A)bonds payable $200,000.

B)bonds payable $200,000, discount $2,000.

C)bonds payable $200,000, discount $1,600.

D)The bonds do not appear on the consolidated balance sheet.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

20

Powell Company owns an 80% interest in Sauter, Inc.On January 1, 2016, Sauter issued $400,000 of 10-year, 12% bonds at a premium of $50,000.On December 31, 2021, 5 years after original issuance, Powell purchased all of the outstanding bonds for $390,000.Both firms use the straight-line method of amortization.

What is the gain on retirement on the 2021 consolidated income statement?

A)$12,500

B)$22,500

C)$10,000

D)$35,000

What is the gain on retirement on the 2021 consolidated income statement?

A)$12,500

B)$22,500

C)$10,000

D)$35,000

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

21

Under a sales-type lease between affiliated companies, how does the lessor treat the intercompany profit at the inception of the lease?

A)It is recognized at the inception of the lease.

B)It is deferred and amortized over the lessee's period of usage.

C)It is deferred and recognized at the end of the lease term.

D)There is no profit at the inception of the lease.

A)It is recognized at the inception of the lease.

B)It is deferred and amortized over the lessee's period of usage.

C)It is deferred and recognized at the end of the lease term.

D)There is no profit at the inception of the lease.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

22

Phil Company leased a machine to its 100%-owned subsidiary, Scout Company.The direct financing lease required annual lease payments in advance of $2,319 for 5 years.The present value of the minimum lease payments at 8% interest is $10,000.The adjustment needed to arrive at consolidated net income for the first year after the lease is ____.

A)$0

B)$800

C)$2,319

D)$10,000

A)$0

B)$800

C)$2,319

D)$10,000

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

23

Soap Company issued $200,000 of 8%, 5-year bonds on January 1, 2016.The discount on issuance was $12,000.Bond interest is paid annually on December 31.On December 31, 2018, Pumice Company purchased one-half of the outstanding bonds for $96,000.Both companies use the straight-line method of amortization.

What amount of gain or loss from retirement of debt will be reported on the 2018 consolidated financial statements?

A)$1,600 gain

B)$1,600 loss

C)$1,200 gain

D)$1,200 loss

What amount of gain or loss from retirement of debt will be reported on the 2018 consolidated financial statements?

A)$1,600 gain

B)$1,600 loss

C)$1,200 gain

D)$1,200 loss

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

24

When a parent buys subsidiary bonds:

A)The bonds become new investments/assets from a consolidated viewpoint and no elimination is necessary.

B)The bonds become new investments/assets but the parent company may not retire subsidiary bonds by lending money.

C)Intercompany interest expense/revenue and accrued interest receivable/payable are not eliminated as the new investments to the parent company and the new debt to the subsidiary company needs to be separately shown when consolidation occurs.

D)The bonds are retired when consolidation occurs by elimination and in periods after the purchase need to be eliminated and retained earnings adjustment for any retirement gain or loss that has not been amortized.

A)The bonds become new investments/assets from a consolidated viewpoint and no elimination is necessary.

B)The bonds become new investments/assets but the parent company may not retire subsidiary bonds by lending money.

C)Intercompany interest expense/revenue and accrued interest receivable/payable are not eliminated as the new investments to the parent company and the new debt to the subsidiary company needs to be separately shown when consolidation occurs.

D)The bonds are retired when consolidation occurs by elimination and in periods after the purchase need to be eliminated and retained earnings adjustment for any retirement gain or loss that has not been amortized.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

25

The parent company leased a machine to its subsidiary using a direct-financing lease that included a bargain purchase option.As a result of the intercompany lease, the following items should be eliminated in the consolidation process: ?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

26

Soap Company issued $200,000 of 8%, 5-year bonds on January 1, 2016.The discount on issuance was $12,000.Bond interest is paid annually on December 31.On December 31, 2018, Pumice Company purchased one-half of the outstanding bonds for $96,000.Both companies use the straight-line method of amortization.

How much interest expense will appear on the December 31, 2019, consolidated income statement?

A)$18,400

B)$16,000

C)$9,200

D)$8,000

How much interest expense will appear on the December 31, 2019, consolidated income statement?

A)$18,400

B)$16,000

C)$9,200

D)$8,000

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following statements is true?

A)No adjustments are made in the income distribution schedule as a result of operating, direct-financing, and sales-type leases.

B)No adjustments are made in the income distribution schedule as a result of operating and direct-financing leases.

C)No adjustments are made in the income distribution schedule as a result of operating and sales-type leases.

D)No adjustments are made in the income distribution schedule as a result of direct-financing and sales-type leases.

A)No adjustments are made in the income distribution schedule as a result of operating, direct-financing, and sales-type leases.

B)No adjustments are made in the income distribution schedule as a result of operating and direct-financing leases.

C)No adjustments are made in the income distribution schedule as a result of operating and sales-type leases.

D)No adjustments are made in the income distribution schedule as a result of direct-financing and sales-type leases.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

28

Park owns an 80% interest in the common stock of Stable Company.Park leased a machine to Stable under a 5-year, direct financing lease with a bargain purchase option.The lease term began January 1, 2019.The impact of the lease on the Non-controlling share of income for 2019:

A)is an increase.

B)is a decrease.

C)is zero.

D)cannot be determined from the information given.

A)is an increase.

B)is a decrease.

C)is zero.

D)cannot be determined from the information given.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

29

Phil Company leased a machine to its 100%-owned subsidiary, Scout Company.The direct financing lease required annual lease payments in advance of $2,319 for 5 years.The present value of the minimum lease payments at 8% interest is $10,000.The adjustment of assets and liabilities needed to prepare a consolidated balance sheet is to eliminate the:

A)asset leased.

B)asset leased and the obligation under the capital lease.

C)obligation under the capital lease and the present value of the minimum lease payments.

D)obligation under the capital lease.

A)asset leased.

B)asset leased and the obligation under the capital lease.

C)obligation under the capital lease and the present value of the minimum lease payments.

D)obligation under the capital lease.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

30

When there is an unguaranteed residual value for the lessor in a direct-financing lease, this means:

A)the total payments to be received by the lessor will come from the lessee.

B)the total payments to be received by the lessee will come from the lessor.

C)a portion of the total payments to be received by the lessor will come from parties outside the consolidated group.

D)a portion of the total payments to be received by the lessee will come from parties outside the consolidated group.

A)the total payments to be received by the lessor will come from the lessee.

B)the total payments to be received by the lessee will come from the lessor.

C)a portion of the total payments to be received by the lessor will come from parties outside the consolidated group.

D)a portion of the total payments to be received by the lessee will come from parties outside the consolidated group.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

31

Consolidation procedures for sales-type leases:

A)allow for the recognition of the profit or loss from the lease by the lessee at the inception of the lease.

B)allow for the recognition of the profit or loss from the lease by the lessor at the inception of the lease.

C)defer the profit or loss and then amortize it over the lessee's period of usage.

D)defer the profit or loss and then amortize it over the lessor's period of usage.

A)allow for the recognition of the profit or loss from the lease by the lessee at the inception of the lease.

B)allow for the recognition of the profit or loss from the lease by the lessor at the inception of the lease.

C)defer the profit or loss and then amortize it over the lessee's period of usage.

D)defer the profit or loss and then amortize it over the lessor's period of usage.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following statements is true?

A)No elimination entries are required on a worksheet as a result of operating, direct-financing, and sales-type leases.

B)No elimination entries are required on a worksheet as a result of direct-financing and sales-type leases.

C)No elimination entries are required on a worksheet as a result of operating leases.

D)All the preceding are false.

A)No elimination entries are required on a worksheet as a result of operating, direct-financing, and sales-type leases.

B)No elimination entries are required on a worksheet as a result of direct-financing and sales-type leases.

C)No elimination entries are required on a worksheet as a result of operating leases.

D)All the preceding are false.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

33

The purchase of outstanding subsidiary bonds by the parent company has the same impact on consolidated statements as:

A)the subsidiary retiring its own debt with the proceeds of new debt issued to outside parties.

B)the subsidiary retiring the debt with the proceeds of a loan from the parent.

C)the subsidiary retiring the debt with the proceeds of a new stock issue.

D)allowing the bonds to continue to be held by outside interests.

A)the subsidiary retiring its own debt with the proceeds of new debt issued to outside parties.

B)the subsidiary retiring the debt with the proceeds of a loan from the parent.

C)the subsidiary retiring the debt with the proceeds of a new stock issue.

D)allowing the bonds to continue to be held by outside interests.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

34

Leasing subsidiaries are formed to achieve centralized asset management through leasing to affiliated firms, and when they are consolidated with the parent, they are consolidated

A)only if the parent controls at least 20% of the leasing subsidiary.

B)only if the parent controls at least 50% of the leasing subsidiary.

C)only if the parent controls at least 90% of the leasing subsidiary.

D)regardless of the ownership percentage of the parent.

A)only if the parent controls at least 20% of the leasing subsidiary.

B)only if the parent controls at least 50% of the leasing subsidiary.

C)only if the parent controls at least 90% of the leasing subsidiary.

D)regardless of the ownership percentage of the parent.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

35

Soap Company issued $200,000 of 8%, 5-year bonds on January 1, 2016.The discount on issuance was $12,000.Bond interest is paid annually on December 31.On December 31, 2018, Pumice Company purchased one-half of the outstanding bonds for $96,000.Both companies use the straight-line method of amortization.

How much bond interest expense will appear on the December 31, 2018, consolidated income statement?

A)$18,400

B)$16,000

C)$9,200

D)$8,000

How much bond interest expense will appear on the December 31, 2018, consolidated income statement?

A)$18,400

B)$16,000

C)$9,200

D)$8,000

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

36

On January 1, 2016, Pope Company acquired 100% of the common stock of Siegel Company for $300,000.On this date Siegel had total owners' equity of $250,000.Any excess of cost over book value is attributable to goodwill.Pope accounts for its investment in Siegel using the simple equity method.

?

On July 1, 2016, Siegel Company sold to outside investors $300,000 par value of 10-year, 10% bonds.The price received was equal to par.The bonds pay interest semi-annually on July 1 and January 1.

?

During early 2019, market interest rates on bonds similar to those issued by Siegel decreased to 8%.As a result, the market value of the bonds increased.On July 1, 2019, Pope purchased $150,000 par value of Siegel's bonds, paying $163,000.Pope still holds the bonds on December 31, 2019 and has amortized the premium, using the straight-line method.

?

Required:

?

Complete the Figure 5-1 worksheet for consolidated financial statements for the year ended December 31, 2019.Round all computations to the nearest dollar.

?

?

?

?

On July 1, 2016, Siegel Company sold to outside investors $300,000 par value of 10-year, 10% bonds.The price received was equal to par.The bonds pay interest semi-annually on July 1 and January 1.

?

During early 2019, market interest rates on bonds similar to those issued by Siegel decreased to 8%.As a result, the market value of the bonds increased.On July 1, 2019, Pope purchased $150,000 par value of Siegel's bonds, paying $163,000.Pope still holds the bonds on December 31, 2019 and has amortized the premium, using the straight-line method.

?

Required:

?

Complete the Figure 5-1 worksheet for consolidated financial statements for the year ended December 31, 2019.Round all computations to the nearest dollar.

?

??

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

37

What is recorded by the lessee and the lessor when an intercompany lease contains an unguaranteed residual value? ?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

38

Lease terms can be considered to be "significantly affected":

A)when the terms are the same for affiliated firms as for independent firms.

B)when the terms could not reasonably be expected to occur between independent firms.

C)only if the lease is an operating lease to the lessee and lessor.

D)only if the lease is a direct-financing lease to the lessee and lessor.

A)when the terms are the same for affiliated firms as for independent firms.

B)when the terms could not reasonably be expected to occur between independent firms.

C)only if the lease is an operating lease to the lessee and lessor.

D)only if the lease is a direct-financing lease to the lessee and lessor.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

39

To eliminate intercompany bonds and interest expense of consolidated companies, Company P (Parent) and Company S (Subsidiary) which of the following is correct?

A)Debit Interest Expense and credit Interest Income and credit Bonds Payable and debit Investment in Company S

B)Credit Interest Expense and debit Interest Income and credit Bonds Payable and debit Investment in Company S

C)Debit Interest Income and credit Interest Expense and debit any related Loss on Bond Retirement, if any, and debit Bonds Payable and credit Investment in Company S Bonds

D)Debit Subsidiary Income and credit Investment in Company S Stock

A)Debit Interest Expense and credit Interest Income and credit Bonds Payable and debit Investment in Company S

B)Credit Interest Expense and debit Interest Income and credit Bonds Payable and debit Investment in Company S

C)Debit Interest Income and credit Interest Expense and debit any related Loss on Bond Retirement, if any, and debit Bonds Payable and credit Investment in Company S Bonds

D)Debit Subsidiary Income and credit Investment in Company S Stock

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

40

The effect of an operating lease on the income distribution schedule:

A)is non-existent.

B)affects only the lessee's income.

C)affects only the lessor's income.

D)affects the amount of income or distribution of income between the non-controlling and controlling interests.

A)is non-existent.

B)affects only the lessee's income.

C)affects only the lessor's income.

D)affects the amount of income or distribution of income between the non-controlling and controlling interests.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

41

Smart Corporation is a 90%-owned subsidiary of Phan Inc.On January 2, 2016, Smart agreed to lease $400,000 of construction equipment from Phan for $3,000 a month on an operating lease.The equipment has a 10-year life and is being depreciated using the straight-line method.

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-8 partial worksheet for December 31, 2016.Key and explain all eliminations and adjustments.

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-8 partial worksheet for December 31, 2016.Key and explain all eliminations and adjustments.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

42

On January 1, 2016 Parent Company acquired 90% of the common stock of Subsidiary Company for $360,000.On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively.Any excess of cost over book value is due to goodwill.Parent accounts for the Investment in Subsidiary using the simple equity method.

On January 1, 2017, Parent purchased equipment for $204,110 and immediately leased the equipment to Subsidiary on a 4-year lease.The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.The lease amortization schedule is presented below:

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-10 partial worksheet as of December 31, 2017.Key and explain all eliminations and adjustments.

On January 1, 2017, Parent purchased equipment for $204,110 and immediately leased the equipment to Subsidiary on a 4-year lease.The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.The lease amortization schedule is presented below:

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-10 partial worksheet as of December 31, 2017.Key and explain all eliminations and adjustments.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

43

On January 1, 2016, Parent Company purchased 80% of the common stock of Subsidiary Company for $402,000.On this date Subsidiary had total owners' equity of $440,000.Any excess of cost over book value is due to goodwill.Parent accounts for its investment in Subsidiary using the simple equity method.

?

On January 1, 2016, Parent held merchandise acquired from Subsidiary for $50,000.During 2016, Subsidiary sold merchandise to Parent for $120,000, of which Parent holds $30,000 on December 31, 2016.Subsidiary's gross profit on sales is 40%.On December 31, 2016, Parent still owes Subsidiary $5,000 for merchandise.

?

On December 31, 2016, Parent sold $100,000 par value of 11%, 10-year bonds for $106,232, which resulted in an effective interest rate of 10%.The bonds pay interest semi-annually on June 30 and December 31.Parent uses the effective-interest method of amortization for the premium.

?

An amortization table for 2017 and 2016 is presented below:

?

?

On December 31, 2017, Subsidiary repurchased $50,000 par value of the bonds, paying a price equal to par.The bonds are still held on December 31, 2016.

?

On December 31, 2016, Parent sold equipment with a cost of $50,000 and accumulated depreciation of $30,000 to Subsidiary for $40,000.Subsidiary will use the equipment beginning in 2019.

?

Required:

?

Complete the Figure 5-7 worksheet for consolidated financial statements for the year ended December 31, 2016.Round all computations to the nearest dollar.

?

?

On January 1, 2016, Parent held merchandise acquired from Subsidiary for $50,000.During 2016, Subsidiary sold merchandise to Parent for $120,000, of which Parent holds $30,000 on December 31, 2016.Subsidiary's gross profit on sales is 40%.On December 31, 2016, Parent still owes Subsidiary $5,000 for merchandise.

?

On December 31, 2016, Parent sold $100,000 par value of 11%, 10-year bonds for $106,232, which resulted in an effective interest rate of 10%.The bonds pay interest semi-annually on June 30 and December 31.Parent uses the effective-interest method of amortization for the premium.

?

An amortization table for 2017 and 2016 is presented below:

?

?

On December 31, 2017, Subsidiary repurchased $50,000 par value of the bonds, paying a price equal to par.The bonds are still held on December 31, 2016.

?

On December 31, 2016, Parent sold equipment with a cost of $50,000 and accumulated depreciation of $30,000 to Subsidiary for $40,000.Subsidiary will use the equipment beginning in 2019.

?

Required:

?

Complete the Figure 5-7 worksheet for consolidated financial statements for the year ended December 31, 2016.Round all computations to the nearest dollar.

?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

44

Tempo Industries is an 80%-owned subsidiary of Dalie Inc.On January 1, 2017, Dalie leased an asset to Tempo and the following journal entries were made:

?

?

The terms of the lease agreement require Tempo to make five payments of $5,000 each at the beginning of each year.The implicit interest rate used by both Dalie and Tempo is 8%.

?

Required:

?

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-9 partial worksheet of December 31, 2017.Key and explain all eliminations and adjustments.

?

?

?

?

The terms of the lease agreement require Tempo to make five payments of $5,000 each at the beginning of each year.The implicit interest rate used by both Dalie and Tempo is 8%.?

Required:

?

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-9 partial worksheet of December 31, 2017.Key and explain all eliminations and adjustments.

?

?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

45

On January 1, 2019, Parent Company purchased 90% of the common stock of Subsidiary Company for $360,000.On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $20,000, $130,000, and $200,000, respectively.Any excess of cost over book value is due to goodwill.Parent accounts for the Investment in Subsidiary using the simple equity method.

On January 1, 2019, Subsidiary sold $100,000 par value of 6%, ten-year bonds for $97,000.The bonds pay interest semi-annually on January 1 and July 1 of each year.

On January 1, 2021, Parent repurchased all of Subsidiary's bonds for $96,400.The bonds are still held on December 31, 2021.

Both companies have correctly recorded all entries relative to bonds and interest, using straight-line amortization for premium or discount.

Required:

Prepare the eliminating entries pertaining to the intercompany purchase of bonds for the year ended December 31, 2021.

On January 1, 2019, Subsidiary sold $100,000 par value of 6%, ten-year bonds for $97,000.The bonds pay interest semi-annually on January 1 and July 1 of each year.

On January 1, 2021, Parent repurchased all of Subsidiary's bonds for $96,400.The bonds are still held on December 31, 2021.

Both companies have correctly recorded all entries relative to bonds and interest, using straight-line amortization for premium or discount.

Required:

Prepare the eliminating entries pertaining to the intercompany purchase of bonds for the year ended December 31, 2021.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

46

On January 1, 2016, Parent Company acquired 90% of the common stock of Subsidiary Company for $360,000.On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively.Any excess of cost over book value is due to goodwill.Parent uses the simple equity method to account for its investment in subsidiary.

On January 1, 2017, Parent purchased equipment for $204,110 and immediately leased the equipment to Subsidiary on a 4-year lease.The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.A lease amortization schedule, applicable to either company, is presented below:

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-11 partial worksheet as of December 31, 2016.Key and explain all eliminations and adjustments.

On January 1, 2017, Parent purchased equipment for $204,110 and immediately leased the equipment to Subsidiary on a 4-year lease.The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.A lease amortization schedule, applicable to either company, is presented below:

Required:

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-11 partial worksheet as of December 31, 2016.Key and explain all eliminations and adjustments.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

47

On January 1, 2016, Pope Company acquired 100% of the common stock of Siegel Company for $300,000.On this date Siegel had total owners' equity of $250,000.Any excess of cost over book value is attributable to goodwill.Pope accounts for its investment in Siegel using the simple equity method.

?

Also on July 1, 2016, Siegel Company sold to outside investors $200,000 par value of 10-year, 10% bonds.The price received was equal to par.The bonds pay interest semi-annually on July 1 and January 1.

?

During early 2019, market interest rates on bonds similar to those issued by Siegel decreased to 8%.As a result, the market value of the bonds increased.On July 1, 2019, Pope purchased $100,000 par value of Siegel's bonds, paying $112,695.Pope still holds the bonds on December 31, 2019 and has amortized the premium, using the effective-interest method which has resulted in interest income of $4,508 and a balance in the Investment in Subsidiary Bonds account of $112,203.

?

Required:

?

Prepare the eliminating entries pertaining to the intercompany purchase of the bonds for the year ended December 31, 2019.

?

Also on July 1, 2016, Siegel Company sold to outside investors $200,000 par value of 10-year, 10% bonds.The price received was equal to par.The bonds pay interest semi-annually on July 1 and January 1.

?

During early 2019, market interest rates on bonds similar to those issued by Siegel decreased to 8%.As a result, the market value of the bonds increased.On July 1, 2019, Pope purchased $100,000 par value of Siegel's bonds, paying $112,695.Pope still holds the bonds on December 31, 2019 and has amortized the premium, using the effective-interest method which has resulted in interest income of $4,508 and a balance in the Investment in Subsidiary Bonds account of $112,203.

?

Required:

?

Prepare the eliminating entries pertaining to the intercompany purchase of the bonds for the year ended December 31, 2019.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

48

The Park Company owns 80% of the outstanding common stock of the Sea Company.Park is about to lease a machine with a 5-year life to the Sea Company.The lease would begin January 1, 2016.

?

Required:

?

Explain the adjustments that will be required in the consolidation process if each of the following occurs.

?

a.The lease is an operating lease.?

?

b.The lease is a direct financing lease with a bargain purchase option.?

?

c.The lease is a sales-type lease with a bargain purchase option.?

?

Required:

?

Explain the adjustments that will be required in the consolidation process if each of the following occurs.

?

a.The lease is an operating lease.?

?

b.The lease is a direct financing lease with a bargain purchase option.?

?

c.The lease is a sales-type lease with a bargain purchase option.?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

49

On January 1, 2016, Pope Company acquired 100% of the common stock of Siegel Company for $300,000.On this date Siegel had total owners' equity of $250,000.Any excess of cost over book value is attributable to goodwill.Pope accounts for its Investment in Siegel using the simple equity method.

On January 1, 2016, Siegel Company sold to outside investors $300,000 par value of 10-year, 10% bonds.The price received was equal to par.The bonds pay interest semi-annually on July 1 and January 1.

During 2016, market interest rates on bonds similar to those issued by Siegel decreased to 8%.As a result, the market value of the bonds increased.On December 31, 2016, Pope purchased $150,000 par value of Siegel's bonds, paying $163,000.Pope still holds the bonds on December 31, 2019 and has amortized the premium, using the straight-line method.

Required:

Prepare the eliminating entries pertaining to the intercompany purchase of bonds outstanding for the year ended December 31, 2019.

On January 1, 2016, Siegel Company sold to outside investors $300,000 par value of 10-year, 10% bonds.The price received was equal to par.The bonds pay interest semi-annually on July 1 and January 1.

During 2016, market interest rates on bonds similar to those issued by Siegel decreased to 8%.As a result, the market value of the bonds increased.On December 31, 2016, Pope purchased $150,000 par value of Siegel's bonds, paying $163,000.Pope still holds the bonds on December 31, 2019 and has amortized the premium, using the straight-line method.

Required:

Prepare the eliminating entries pertaining to the intercompany purchase of bonds outstanding for the year ended December 31, 2019.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

50

On January 1, 2016, Parent Company acquired 100% of the common stock of Subsidiary Company for $365,000.On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively.Any excess of cost over book value is due to goodwill.Parent uses the simple equity method to account for its investment in subsidiary.

?

On January 1, 2017, Parent purchased equipment for $174,120 and immediately leased the equipment to Subsidiary on a 4-year lease.The transaction was legally structured as a sales-type lease with a present value for the minimum lease payments of $204,120.Parent recorded the following entry:

?

?

The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.

?

A lease amortization schedule, applicable to either company, is presented below:

?

?

Required:

?

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-13 partial worksheet as of December 31, 2017.Key and explain all eliminations and adjustments.

?

?

?

On January 1, 2017, Parent purchased equipment for $174,120 and immediately leased the equipment to Subsidiary on a 4-year lease.The transaction was legally structured as a sales-type lease with a present value for the minimum lease payments of $204,120.Parent recorded the following entry:

?

?

The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.

?

A lease amortization schedule, applicable to either company, is presented below:

?

?

Required:?

Prepare the eliminations and adjustments required by the intercompany lease on the Figure 5-13 partial worksheet as of December 31, 2017.Key and explain all eliminations and adjustments.

?

?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

51

The Planes Company owns 100% of the outstanding common stock of the Sands Company.Sands issued $100,000 of face value, 9%, 10-year bonds on January 1, 2016, for $96,000.The discount is being amortized on a straight-line basis.On January 1, 2018, Planes purchased all the bonds as an investment for $95,000.

?

Required:

?

Be specific in answering the following questions and include numerical explanations.

?

a.How will this bond issue be recorded and accounted for in 2018 on the separate books of Planes and Sands?

?

?

b.How will this bond issue be accounted for on the 2018 consolidated statements?

?

?

c.How will this bond issue be recorded and accounted for in 2019 on the separate books of Planes and Sands?

?

?

d.How will this bond issue be accounted for on the 2019 consolidated statements?

?

Required:

?

Be specific in answering the following questions and include numerical explanations.

?

a.How will this bond issue be recorded and accounted for in 2018 on the separate books of Planes and Sands?

?

?

b.How will this bond issue be accounted for on the 2018 consolidated statements?

?

?

c.How will this bond issue be recorded and accounted for in 2019 on the separate books of Planes and Sands?

?

?

d.How will this bond issue be accounted for on the 2019 consolidated statements?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

52

On January 1, 2016, Parent Company purchased 100% of the common stock of Subsidiary Company for $390,000.On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively.Any excess of cost over book value is due to goodwill.Parent accounts for the Investment in Subsidiary using the simple equity method.

On January 1, 2017, Parent purchased equipment for $204,120 and immediately leased the equipment to Subsidiary on a 4-year lease.The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.

A lease amortization schedule, applicable to either company, is presented below:

On January 1, 2016, Parent held merchandise acquired from Subsidiary for $10,000.During 2016, subsidiary sold merchandise to Parent for $50,000, of which $15,000 is held by Parent on December 31, 2016.Subsidiary's usual gross profit on affiliated sales is 40%.

Required:

Complete the Figure 5-12 worksheet for consolidated financial statements for the year ended December 31, 2016.Round all computations to the nearest dollar.

On January 1, 2017, Parent purchased equipment for $204,120 and immediately leased the equipment to Subsidiary on a 4-year lease.The minimum lease payments of $60,000 are to be made annually on January 1, beginning immediately, for a total of 4 payments.The implicit interest rate is 12%.The lease provides for an automatic transfer of title at the end of 4 years.The estimated useful life of the equipment is 6 years.The lease has been capitalized by both companies.

A lease amortization schedule, applicable to either company, is presented below:

On January 1, 2016, Parent held merchandise acquired from Subsidiary for $10,000.During 2016, subsidiary sold merchandise to Parent for $50,000, of which $15,000 is held by Parent on December 31, 2016.Subsidiary's usual gross profit on affiliated sales is 40%.

Required:

Complete the Figure 5-12 worksheet for consolidated financial statements for the year ended December 31, 2016.Round all computations to the nearest dollar.

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

53

On January 1, 2019, Parent Company purchased 90% of the common stock of Subsidiary Company for $450,000.On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $20,000, $130,000, and $200,000, respectively.Any excess of cost over book value is due to goodwill.Parent accounts for the Investment in Subsidiary using the cost method.

?

On January 1, 2019, Subsidiary sold $100,000 par value of 6%, ten-year bonds for $97,000.The bonds pay interest semi-annually on January 1 and July 1 of each year.

?

On January 1, 2021, Parent repurchased all of Subsidiary's bonds for $96,400.The bonds are still held on December 31, 2021.

?

Both companies have correctly recorded all entries relative to bonds and interest, using straight-line amortization for premium or discount.

?

Required:

?

Complete the Figure 5-4 worksheet for consolidated financial statements for the year ended of December 31, 2021.Round all computations to the nearest dollar.

?

?

On January 1, 2019, Subsidiary sold $100,000 par value of 6%, ten-year bonds for $97,000.The bonds pay interest semi-annually on January 1 and July 1 of each year.

?

On January 1, 2021, Parent repurchased all of Subsidiary's bonds for $96,400.The bonds are still held on December 31, 2021.

?

Both companies have correctly recorded all entries relative to bonds and interest, using straight-line amortization for premium or discount.

?

Required:

?

Complete the Figure 5-4 worksheet for consolidated financial statements for the year ended of December 31, 2021.Round all computations to the nearest dollar.

?

Unlock Deck

Unlock for access to all 54 flashcards in this deck.

Unlock Deck

k this deck

54

On January 1, 2019, Parent Company purchased 90% of the common stock of Subsidiary Company for $360,000.On this date, Subsidiary had common stock, other paid in capital, and retained earnings of $20,000, $130,000, and $200,000 respectively.Any excess of cost over book value is due to goodwill.Parent account for the Investment in Subsidiary using the simple equity method.

?

On July 1, 2019, Subsidiary sold $100,000 par value of 9%, ten-year bonds for $106,755, which resulted in an effective interest rate of 8%.The bonds pay interest semi-annually on January 1 and July 1 of each year.Subsidiary uses the effective-interest method of amortizing the premium.

?

An amortization table for 2019 and 2021 is presented below:

?

?

On July 1, 2021, Parent repurchased all of Par's bonds for $94,153, which resulted in an effective interest rate of 10%.The bonds are still held at year end.

?