Deck 11: Equity Portfolio Management Strategies

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

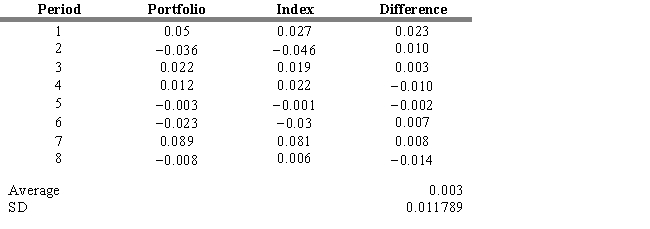

The table below provides returns on a portfolio along with returns for the corresponding benchmark index for the past eight quarters. The table also provides the difference between portfolio returns and the benchmark index, the average of these differences over the past eight quarters, and the standard deviation of these differences.  The annualized tracking error for this period is

The annualized tracking error for this period is

A) 2.36 percent.

B) 4.08 percent

C) 2.89 percent.

D) 3.33 percent.

E) 1.18 percent.

The annualized tracking error for this period isA) 2.36 percent.

B) 4.08 percent

C) 2.89 percent.

D) 3.33 percent.

E) 1.18 percent.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/65

Play

Full screen (f)

Deck 11: Equity Portfolio Management Strategies

1

Active equity portfolio management is a long-term buy-and-hold strategy.

False

2

Tracking error is defined as the degree to which the portfolio's returns deviate from those of the actual index.

True

3

A way to distinguish between these strategies is to decompose the total actual return that the portfolio manager attempts to produce.

True

4

The goal of active equity management is to earn a return that exceeds the return of a passive benchmark portfolio, net of transaction costs, on a risk-adjusted basis.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

5

A benchmark portfolio is defined as a passive portfolio whose average characteristics match the client's risk-return objectives.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

6

Exchange-Traded Funds (ETF) are depository receipts that give investors a pro rata claim on the capital gains and cash flows of securities held by financial institutions.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

7

An advantage of quadratic programming is that it relies on historical correlations.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

8

Active portfolio managers just try to capture the expected return consistent with the risk level of their portfolios.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

9

There is a direct relationship between a passive portfolio's tracking error relative to its index and the time and expense necessary to create and maintain the portfolio.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

10

Following an earnings momentum strategy, an investor acquires stocks that have enjoyed above-market stock price increases.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

11

Completeness funds are portfolios designed to complement active portfolios that do not cover the entire market.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

12

Growth stocks consistently outperform value stocks.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

13

A growth investor focuses on the current and future economic "story" of a company, with less regard for share valuation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

14

Passive portfolio managers attempt to "beat the market" by forming portfolios capable of producing actual returns that exceed risk-adjusted expected returns.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

15

The goal of a passive portfolio is to track the index as closely as possible.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

16

The difference between the actual and expected return is often called the portfolio's alpha,

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

17

An advantage of sampling is that portfolio returns will not track the index as closely as with full replication.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

18

An attempt on the manager's part to generate alpha is generally referred to as indexing.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

19

The value investor focuses on share price in anticipation of a market correction and, possibly, improving company fundamentals.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

20

The three basic techniques for constructing a passive index are: full replication, sampling, and linear programming.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

21

The goal of the passive portfolio manager is to minimize

A) alpha.

B) beta.

C) standard error.

D) tracking error.

E) portfolio risk.

A) alpha.

B) beta.

C) standard error.

D) tracking error.

E) portfolio risk.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

22

The table below provides returns on a portfolio along with returns for the corresponding benchmark index for the past eight quarters. The table also provides the difference between portfolio returns and the benchmark index, the average of these differences over the past eight quarters, and the standard deviation of these differences. The annualized tracking error for this period is

A) 2.36 percent.

B) 4.08 percent

C) 2.89 percent.

D) 3.33 percent.

E) 1.18 percent.

The annualized tracking error for this period isA) 2.36 percent.

B) 4.08 percent

C) 2.89 percent.

D) 3.33 percent.

E) 1.18 percent.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following is NOT considered an active management strategy?

A) sector rotation

B) use of factor models

C) quantitative screens

D) full replication

E) linear programming

A) sector rotation

B) use of factor models

C) quantitative screens

D) full replication

E) linear programming

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

24

All of the following are advantages of ETFs over mutual funds EXCEPT

A) The ability for continuous trading while markets are open.

B) the ability to time capital gain tax realizations.

C) a smaller management fee.

D) ETFs can be bought and sold like common stock.

E) smaller brokerage commission.

A) The ability for continuous trading while markets are open.

B) the ability to time capital gain tax realizations.

C) a smaller management fee.

D) ETFs can be bought and sold like common stock.

E) smaller brokerage commission.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

25

Style investing involves constructing portfolios in such a way as to capture one or more of the characteristics of equity securities.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following is considered a passive management strategy?

A) sector rotation

B) use of factor models

C) quantitative screens

D) sampling

E) linear programming

A) sector rotation

B) use of factor models

C) quantitative screens

D) sampling

E) linear programming

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

27

It does not make economic sense for portfolio managers to try to "time" between different investment styles.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

28

Style investing allows control of the total portfolio to be shared between investment managers and pension fund managers.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

29

A portfolio manager who uses tactical asset allocation is attempting to create alpha.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

30

Insured asset allocation is a strategy to limit investment losses by shifting funds between an existing equity portfolio and a risk-free security.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following is NOT a technique for constructing a passive index portfolio?

A) full replication

B) sampling

C) quadratic programming

D) linear programming

E) indexing

A) full replication

B) sampling

C) quadratic programming

D) linear programming

E) indexing

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

32

The integrated asset allocation strategy separately examines capital market conditions and the investor's objectives and constraints.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following statements concerning active equity portfolio management strategies is true?

A) The goal of active equity portfolio management is to earn a portfolio return that exceeds the return of a passive benchmark portfolio (net of transaction costs) on a risk-adjusted basis.

B) An actively managed equity portfolio has lower total transaction costs.

C) An actively managed equity portfolio has lower risk than the passive benchmark.

D) A key to success for an actively managed equity portfolio is to maximize trading activity.

E) An actively managed equity portfolio has lower turnover.

A) The goal of active equity portfolio management is to earn a portfolio return that exceeds the return of a passive benchmark portfolio (net of transaction costs) on a risk-adjusted basis.

B) An actively managed equity portfolio has lower total transaction costs.

C) An actively managed equity portfolio has lower risk than the passive benchmark.

D) A key to success for an actively managed equity portfolio is to maximize trading activity.

E) An actively managed equity portfolio has lower turnover.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

34

Growth oriented investors focus on the price component of the Price/Earnings ratio.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

35

Strategic asset allocation frequently adjusts the asset class mix in the portfolio to take advantage of changing market conditions.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

36

Tactical asset allocation is used to determine the long-term policy asset weights in a portfolio.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

37

In equity portfolio management, tracking error occurs when

A) the managed portfolio outperforms the benchmark portfolio.

B) the managed portfolio under performs the benchmark portfolio.

C) the return volatility of the managed portfolio is positively correlated with the return volatility of the benchmark portfolio.

D) the return volatility of the managed portfolio is negatively correlated with the return volatility of the benchmark portfolio.

E) the return volatility of the managed portfolio is not correlated with the return volatility of the benchmark portfolio.

A) the managed portfolio outperforms the benchmark portfolio.

B) the managed portfolio under performs the benchmark portfolio.

C) the return volatility of the managed portfolio is positively correlated with the return volatility of the benchmark portfolio.

D) the return volatility of the managed portfolio is negatively correlated with the return volatility of the benchmark portfolio.

E) the return volatility of the managed portfolio is not correlated with the return volatility of the benchmark portfolio.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

38

The difference between the actual and expected return is often called

A) alpha.

B) beta.

C) risk premium.

D) the risk-free rate.

E) the benchmark.

A) alpha.

B) beta.

C) risk premium.

D) the risk-free rate.

E) the benchmark.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

39

Style identification allows an investor to select investment managers that allow his overall portfolio to be properly diversified.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

40

In ____ strategy, certain economic sectors or industries are overweighted relative to the benchmark in anticipation of the next phase of the business cycle.

A) sector rotation

B) price momentum

C) earnings momentum

D) return rotation

E) passive momentum

A) sector rotation

B) price momentum

C) earnings momentum

D) return rotation

E) passive momentum

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

41

Growth stocks would have the following characteristics:

A) low price/book and high price/earnings.

B) low price/book and low price/earnings.

C) high EPS growth and high profitability.

D) low EPS growth and high profitability.

E) None of these are correct.

A) low price/book and high price/earnings.

B) low price/book and low price/earnings.

C) high EPS growth and high profitability.

D) low EPS growth and high profitability.

E) None of these are correct.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

42

A fundamental tenet of the contrarian investment strategy is the notion that

A) all stock returns are mean reverting.

B) certain stocks outperform others during different stages of the business cycle.

C) value stock investing is superior to growth stock investing.

D) growth stock investing is superior to value stock investing.

E) None of these are correct.

A) all stock returns are mean reverting.

B) certain stocks outperform others during different stages of the business cycle.

C) value stock investing is superior to growth stock investing.

D) growth stock investing is superior to value stock investing.

E) None of these are correct.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

43

A portfolio management strategy that overweights a particular industry, relative to the benchmark portfolio, based on the next expected phase of the business cycle is called

A) tactical asset allocation.

B) indexing.

C) sector rotation.

D) contrarian investing.

E) Bottom-up investing.

A) tactical asset allocation.

B) indexing.

C) sector rotation.

D) contrarian investing.

E) Bottom-up investing.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following is considered a strategy for timing the market and adding value to actively managed portfolios?

A) timing the markets by shifting between different types of securities based on market forecasts and estimated risk premiums.

B) shifting funds between the various equity sectors, industries, investment styles, etc., in order to take advantage of the "hot" concept before the remainder of the market does.

C) individual stock picking in order to buy low and sell high.

D) using tactical asset allocation strategies.

E) All of these are correct.

A) timing the markets by shifting between different types of securities based on market forecasts and estimated risk premiums.

B) shifting funds between the various equity sectors, industries, investment styles, etc., in order to take advantage of the "hot" concept before the remainder of the market does.

C) individual stock picking in order to buy low and sell high.

D) using tactical asset allocation strategies.

E) All of these are correct.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following statements is FALSE?

A) A manager's choice to align with an investment style communicates information to clients about the investor's focus, area of expertise, and stock evaluation methods.

B) An investment manager's style cannot be used as a basis for measuring the manager's performance relative to a benchmark.

C) Style identification allows an investor to select investment managers that allow his overall portfolio to be properly diversified.

D) Style investing allows control of the total portfolio to be shared between the investment managers and a knowledgeable sponsor.

E) An investor needs to be cautious about a manager whose portfolio exhibits unintentional style drift.

A) A manager's choice to align with an investment style communicates information to clients about the investor's focus, area of expertise, and stock evaluation methods.

B) An investment manager's style cannot be used as a basis for measuring the manager's performance relative to a benchmark.

C) Style identification allows an investor to select investment managers that allow his overall portfolio to be properly diversified.

D) Style investing allows control of the total portfolio to be shared between the investment managers and a knowledgeable sponsor.

E) An investor needs to be cautious about a manager whose portfolio exhibits unintentional style drift.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

46

If the annual geometric mean for the equity risk premium is 8.4 percent, what percentage of the equity risk premium is consumed by trading costs of 1.2 percent?

A) 7.20 percent

B) 9.60 percent

C) 9.70 percent

D) 10.08 percent

E) 14.29 percent

A) 7.20 percent

B) 9.60 percent

C) 9.70 percent

D) 10.08 percent

E) 14.29 percent

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following statements regarding momentum strategies is TRUE?

A) Price momentum is a fundamental strategy.

B) Earnings momentum is a technical strategy.

C) Price momentum and earnings momentum strategies will often result in identical portfolio strategies and holdings.

D) The earnings momentum investor will most likely acquire stocks for companies that have positive earnings surprises.

E) All of these are correct.

A) Price momentum is a fundamental strategy.

B) Earnings momentum is a technical strategy.

C) Price momentum and earnings momentum strategies will often result in identical portfolio strategies and holdings.

D) The earnings momentum investor will most likely acquire stocks for companies that have positive earnings surprises.

E) All of these are correct.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following statements regarding 130/30 strategies is FALSE?

A) Analysts can make full use of their knowledge of undervalued and overvalued stocks.

B) Long positions up to 130 percent of the value of the portfolio can be made.

C) Short positions up to 30 percent of the value of the portfolio can be made.

D) 130/30 strategies are not very popular due to the increased risk of hedging.

E) The use of short positions creates leverage.

A) Analysts can make full use of their knowledge of undervalued and overvalued stocks.

B) Long positions up to 130 percent of the value of the portfolio can be made.

C) Short positions up to 30 percent of the value of the portfolio can be made.

D) 130/30 strategies are not very popular due to the increased risk of hedging.

E) The use of short positions creates leverage.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

49

If you have a portfolio with a market value of $100 million and a beta (measured against the S&P 500) of 1.5, then if the market rises by 10 percent, what value would you expect your portfolio to have?

A) $100 million

B) $110 million

C) $150 million

D) $165 million

E) $1.65 billion

A) $100 million

B) $110 million

C) $150 million

D) $165 million

E) $1.65 billion

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following is NOT considered an asset allocation strategy?

A) integrated asset allocation

B) strategic asset allocation

C) tactical asset allocation

D) insured asset allocation

E) full replication

A) integrated asset allocation

B) strategic asset allocation

C) tactical asset allocation

D) insured asset allocation

E) full replication

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

51

An active portfolio manager sold $90 million of stocks in a year. If the portfolio had an average value of $110 million in assets under management what is the portfolio turnover ratio?

A) 22.2 percent

B) 81.8 percent

C) 90.0 percent

D) 110.0 percent

E) 122.2 percent

A) 22.2 percent

B) 81.8 percent

C) 90.0 percent

D) 110.0 percent

E) 122.2 percent

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

52

In returns-based style analysis, a coefficient of determination of 95 percent would suggest that

A) the portfolio manager outperformed 95 percent of his peers.

B) the portfolio manager was outperformed by 95 percent of his peers.

C) 95 percent of the portfolio return variability could be attributed to portfolio style.

D) 95 percent of the portfolio return variability could be attributed to stock selection skills.

E) 5 percent of the portfolio return variability could be attributed to portfolio style.

A) the portfolio manager outperformed 95 percent of his peers.

B) the portfolio manager was outperformed by 95 percent of his peers.

C) 95 percent of the portfolio return variability could be attributed to portfolio style.

D) 95 percent of the portfolio return variability could be attributed to stock selection skills.

E) 5 percent of the portfolio return variability could be attributed to portfolio style.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

53

The following is an example of a fundamental active equity portfolio management strategy.

A) contrarian investing

B) earnings momentum investing

C) low P/E and low P/BV investing

D) bottom up investing

E) investing on the basis of calendar effects

A) contrarian investing

B) earnings momentum investing

C) low P/E and low P/BV investing

D) bottom up investing

E) investing on the basis of calendar effects

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following statements about investment style is FALSE?

A) Growth stocks generally have smaller capitalizations than value stocks.

B) Value stocks have P/E and P/B ratios significantly lower than those of growth stocks.

C) Value stocks dividend yields are much higher than those of growth stocks.

D) Growth and levels of earnings is higher in growth stocks.

E) Value stocks have a higher risk premium.

A) Growth stocks generally have smaller capitalizations than value stocks.

B) Value stocks have P/E and P/B ratios significantly lower than those of growth stocks.

C) Value stocks dividend yields are much higher than those of growth stocks.

D) Growth and levels of earnings is higher in growth stocks.

E) Value stocks have a higher risk premium.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

55

Fund XYZ had a pretax return of 10.2 percent and a tax-adjusted return of 9.5 percent. Calculate Fund XYZ's tax cost ratio.

A) 0.006

B) 0.106

C) 0.116

D) 0.342

E) 0.635

A) 0.006

B) 0.106

C) 0.116

D) 0.342

E) 0.635

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following is NOT considered an investment style?

A) value

B) growth

C) market-oriented

D) benchmark

E) small-cap

A) value

B) growth

C) market-oriented

D) benchmark

E) small-cap

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

57

____ is a strategy used because the market seems to reward companies that have steady, above average earnings growth, or whose prices are rising because of market optimism.

A) Relative strength

B) Asset momentum

C) Rotational attribution

D) Sector rotation

E) Earnings momentum

A) Relative strength

B) Asset momentum

C) Rotational attribution

D) Sector rotation

E) Earnings momentum

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

58

Value stocks would have the following characteristics:

A) low price/book and high price/earnings.

B) low price/book and low price/earnings.

C) high EPS growth and high profitability.

D) low EPS growth and high profitability.

E) None of these are correct.

A) low price/book and high price/earnings.

B) low price/book and low price/earnings.

C) high EPS growth and high profitability.

D) low EPS growth and high profitability.

E) None of these are correct.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

59

In ____ asset allocation, the investor's risk tolerance and constraints are assumed to be constant over time. However, changes in capital market conditions result in changes in the portfolio's stock-bond mix.

A) integrated

B) strategic

C) tactical

D) insured

E) replication

A) integrated

B) strategic

C) tactical

D) insured

E) replication

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

60

An investor focusing on a growth strategy does all of the following EXCEPT

A) focus on the earnings per share (EPS) component on the P/E ratio.

B) seek out investments with higher expected growth in earnings.

C) implicitly assume that the P/E ratio will grow over the near term.

D) focus on the current and future economic "story" of a company.

E) All of these are correct.

A) focus on the earnings per share (EPS) component on the P/E ratio.

B) seek out investments with higher expected growth in earnings.

C) implicitly assume that the P/E ratio will grow over the near term.

D) focus on the current and future economic "story" of a company.

E) All of these are correct.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

61

The strategy that separately examines capital market conditions and the investor's objectives and constraints is called

A) integrated asset allocation.

B) tactical asset allocation.

C) sector rotation.

D) strategic asset allocation.

E) insured asset allocation.

A) integrated asset allocation.

B) tactical asset allocation.

C) sector rotation.

D) strategic asset allocation.

E) insured asset allocation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

62

A portfolio manager who is trying to generate alpha could use

A) hedge funds.

B) mutual funds.

C) insured asset allocation.

D) ETFs.

E) indexing.

A) hedge funds.

B) mutual funds.

C) insured asset allocation.

D) ETFs.

E) indexing.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

63

The strategy that is used to determine the long-term policy asset weights in a portfolio is called

A) integrated asset allocation.

B) tactical asset allocation.

C) sector rotation.

D) strategic asset allocation.

E) insured asset allocation.

A) integrated asset allocation.

B) tactical asset allocation.

C) sector rotation.

D) strategic asset allocation.

E) insured asset allocation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

64

A contrarian investment strategy is based on the belief that

A) stock returns are mean reverting.

B) the best time to buy is when other investors are bullish.

C) rising stocks will continue to rise.

D) passive management is preferred to active management.

E) a long/short portfolio will outperform a long only portfolio.

A) stock returns are mean reverting.

B) the best time to buy is when other investors are bullish.

C) rising stocks will continue to rise.

D) passive management is preferred to active management.

E) a long/short portfolio will outperform a long only portfolio.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

65

The strategy that frequently adjusts the asset class mix in the portfolio to take advantage of changing market conditions while assuming that the investor's risk tolerance and investment constraints to be constant over time is called

A) integrated asset allocation.

B) tactical asset allocation.

C) sector rotation.

D) strategic asset allocation.

E) insured asset allocation.

A) integrated asset allocation.

B) tactical asset allocation.

C) sector rotation.

D) strategic asset allocation.

E) insured asset allocation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 65 flashcards in this deck.