Deck 11: The Income Statement, the Statement of Comprehensive Income, the Statement of Stockholders Equity

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

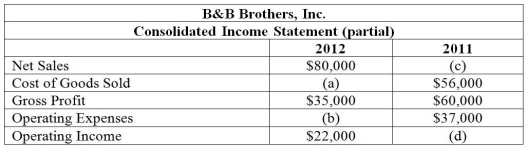

Shown below is a partial consolidated income statement for B&B Brothers, Inc. for 2011 and 2012.

Required: Calculate the missing amounts (a through d) using the information below.

Required: Calculate the missing amounts (a through d) using the information below.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

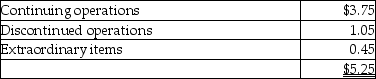

Current earnings per share information is as follows:  The interest capitalization rate is 7.5%. How much should an investor pay for a share of stock?

The interest capitalization rate is 7.5%. How much should an investor pay for a share of stock?

A) $50.00

B) $58.00

C) $64.00

D) $70.00

The interest capitalization rate is 7.5%. How much should an investor pay for a share of stock?A) $50.00

B) $58.00

C) $64.00

D) $70.00

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/125

Play

Full screen (f)

Deck 11: The Income Statement, the Statement of Comprehensive Income, the Statement of Stockholders Equity

1

Gross profit measures the overall profitability of a company.

False

2

Ongoing expenses incurred by the entity, other than direct expenses for merchandise and other costs directly related to sales, are called:

A) other expenses.

B) extraordinary items.

C) cost of goods sold.

D) operating expenses.

A) other expenses.

B) extraordinary items.

C) cost of goods sold.

D) operating expenses.

D

3

U.S. GAAP and IFRS do not have the same revenue recognition criteria.

True

4

Sales revenue less cost of goods sold is called:

A) gross profit.

B) net income.

C) net profit.

D) net sales.

A) gross profit.

B) net income.

C) net profit.

D) net sales.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

5

If net sales are $1,200,000 and cost of goods sold are $300,000, gross profit is $900,000.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

6

A type of financial statement fraud that is accomplished by shipping more to customers than they ordered, with the expectation that they may return some or all of the items is called:

A) improper shipping recognition.

B) improper sales recognition.

C) channel stuffing.

D) accidental shipping.

A) improper shipping recognition.

B) improper sales recognition.

C) channel stuffing.

D) accidental shipping.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

7

Financial statement fraud does not include the improper recognition of expenses.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

8

The characteristic of earnings that makes it most useful for decision making is called:

A) extraordinary item.

B) earnings quality.

C) comprehensive income.

D) clean opinion.

A) extraordinary item.

B) earnings quality.

C) comprehensive income.

D) clean opinion.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

9

The operating expense section of an income statement would NOT include:

A) salaries expense.

B) utilities expense.

C) supplies expense.

D) interest expense.

A) salaries expense.

B) utilities expense.

C) supplies expense.

D) interest expense.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

10

Steadily decreasing cost of goods sold as a percentage of net sales is a sign of:

A) increasing earnings quality.

B) decreasing earnings quality.

C) lower sales.

D) higher sales.

A) increasing earnings quality.

B) decreasing earnings quality.

C) lower sales.

D) higher sales.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

11

If ABC Corporation has net sales of $600,000 and cost of goods sold of $390,000, the gross profit percentage is:

A) 65%.

B) 54%.

C) 35%.

D) 25%.

A) 65%.

B) 54%.

C) 35%.

D) 25%.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

12

There will be income from operations if:

A) revenues are greater than cost of goods sold.

B) revenues are greater than operating expenses.

C) gross profit is greater than operating expenses.

D) cost of goods sold is greater than operating expenses.

A) revenues are greater than cost of goods sold.

B) revenues are greater than operating expenses.

C) gross profit is greater than operating expenses.

D) cost of goods sold is greater than operating expenses.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

13

The purpose of channel stuffing is to increase operating expenses.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

14

Revenue fraud includes all of the following EXCEPT:

A) reporting revenue when goods have not yet been delivered.

B) channel stuffing.

C) sales to nonexistent customers.

D) recognizing revenue when earned.

A) reporting revenue when goods have not yet been delivered.

B) channel stuffing.

C) sales to nonexistent customers.

D) recognizing revenue when earned.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

15

Roughly half of all financial statement frauds over the past two decades have involved:

A) improper expense recognition.

B) improper revenue recognition.

C) improper depreciation methods.

D) bankruptcy.

A) improper expense recognition.

B) improper revenue recognition.

C) improper depreciation methods.

D) bankruptcy.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

16

The revenue recognition principle requires that sales revenues be recognized when they are earned.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

17

The gross profit rate is computed by dividing gross profit by:

A) cost of goods sold.

B) net sales.

C) net income.

D) operating expenses.

A) cost of goods sold.

B) net sales.

C) net income.

D) operating expenses.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

18

The degree to which earnings are an accurate reflection of underlying economic events for both revenues and expenses, and the extent to which earnings from a company's core operations are improving over time, is:

A) earnings quality.

B) comprehensive income.

C) revenue recognition.

D) discontinued operations.

A) earnings quality.

B) comprehensive income.

C) revenue recognition.

D) discontinued operations.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

19

Recognizing revenue before it is earned is a major source of financial statement fraud.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

20

Gross profit is calculated by dividing cost of goods sold by net sales.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

21

Income tax expense helps measure income from operations.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

22

On August 1, Central Computers, Inc. purchased thirty computer chips, on account, from a company located in Taiwan for 500,000 Taiwan dollars. On that date the Taiwan dollar is worth $0.040. On September 1, when the Taiwan dollar was worth $0.038, payment was made. The journal entry to record the payment on September 1 would include a:

A) debit to Accounts Payable $19,000.

B) debit to Foreign-Currency Transaction Loss $1,000.

C) credit to Foreign-Currency Transaction Gain $1,000.

D) credit to Cash $20,000.

A) debit to Accounts Payable $19,000.

B) debit to Foreign-Currency Transaction Loss $1,000.

C) credit to Foreign-Currency Transaction Gain $1,000.

D) credit to Cash $20,000.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

23

Hedging enables an entity to protect itself from losing money in a foreign transaction by engaging in a counterbalancing transaction.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

24

Common stock should be purchased if the estimated value of a company exceeds its current market value.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

25

The foreign-currency transaction gain account holds gains and losses on transactions settled in a foreign currency.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

26

On June 15, Central Computers, Inc. sold twenty-five computers, on account, to a company located in Argentina for 3,000,000 pesos. On that date the peso is worth $0.079. On July 15, when the peso was worth $0.070, payment was received. The journal entry to record the July 15 collection on account would include a:

A) credit to Cash $237,000

B) credit to Accounts Receivable $210,000.

C) debit to Foreign-Currency Transaction Loss $27,000.

D) credit to Sales $210,000.

A) credit to Cash $237,000

B) credit to Accounts Receivable $210,000.

C) debit to Foreign-Currency Transaction Loss $27,000.

D) credit to Sales $210,000.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

27

Operating income includes income from discontinued operations.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

28

Income tax payable is the amount of tax to be paid to the government in the next period.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

29

In a foreign-currency transaction, all funds must be converted to U.S. dollars for reporting purposes.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

30

When a company discontinues a segment of its business, the income statement should report income (loss) from continuing operations and income (loss) from discontinued operations.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

31

Foreign-currency transaction losses can be avoided if international transactions are settled in U.S. dollars.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

32

Shown below is a partial consolidated income statement for B&B Brothers, Inc. for 2011 and 2012.

Required: Calculate the missing amounts (a through d) using the information below.

Required: Calculate the missing amounts (a through d) using the information below.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

33

On August 1, Central Computers, Inc. purchased thirty computer chips, on account, from a company located in Taiwan for 500,000 Taiwan dollars. On that date the Taiwan dollar is worth $0.040. On September 1, when the Taiwan dollar was worth $0.038, payment was made. The journal entry to record the sale on August 1 would include a:

A) credit to Accounts Payable $19,000.

B) credit to Accounts Payable $20,000.

C) credit to Foreign-Currency Transaction Gain $1,000.

D) credit to Cash $20,000.

A) credit to Accounts Payable $19,000.

B) credit to Accounts Payable $20,000.

C) credit to Foreign-Currency Transaction Gain $1,000.

D) credit to Cash $20,000.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

34

All foreign transactions will result in a foreign-currency exchange rate gain or loss.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

35

One reason why taxable income and accounting income may not match is due to the difference in depreciation methods.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

36

On June 15, Central Computers, Inc. sold twenty-five computers on account to a company located in Argentina for 3,000,000 pesos. On that date, the peso is worth $0.079. On July 15, when the peso was worth $0.070, payment was received. The journal entry to record the sale on June 15 would include a:

A) debit to Accounts Receivable $237,000

B) debit to Accounts Receivable $210,000.

C) debit to Foreign-Currency Transaction Loss $27,000.

D) credit to Sales $210,000.

A) debit to Accounts Receivable $237,000

B) debit to Accounts Receivable $210,000.

C) debit to Foreign-Currency Transaction Loss $27,000.

D) credit to Sales $210,000.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

37

Income tax payable is computed by multiplying income before income taxes per the income statement by the income tax rate.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

38

The net of foreign-currency transaction gains and losses will appear on the balance sheet.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

39

Components of earnings quality include all of the following EXCEPT:

A) low operating expenses compared to sales.

B) high and improving gross margin.

C) a low gross profit.

D) proper revenue and expense recognition.

A) low operating expenses compared to sales.

B) high and improving gross margin.

C) a low gross profit.

D) proper revenue and expense recognition.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

40

Taxable income should always match accounting income.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

41

The loss incurred as a result of writing down obsolete inventory should be reported as:

A) part of discontinued operations.

B) an operating expense.

C) other expenses and losses.

D) an extraordinary item.

A) part of discontinued operations.

B) an operating expense.

C) other expenses and losses.

D) an extraordinary item.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

42

Current earnings per share information is as follows: The interest capitalization rate is 7.5%. How much should an investor pay for a share of stock?

A) $50.00

B) $58.00

C) $64.00

D) $70.00

The interest capitalization rate is 7.5%. How much should an investor pay for a share of stock?A) $50.00

B) $58.00

C) $64.00

D) $70.00

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

43

Extraordinary gains and losses are shown "net of tax" on the income statement.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

44

Western Corporation has taxable income of $390,000 and pretax accounting income of $363,000. The company's income tax rate is 35%. The entry to record the income tax includes a:

A) debit to Income Tax Expense $136,500.

B) debit to Deferred Tax Asset $127,050.

C) debit to Deferred Tax Asset $9,450.

D) credit to Income Tax Payable $127,050.

A) debit to Income Tax Expense $136,500.

B) debit to Deferred Tax Asset $127,050.

C) debit to Deferred Tax Asset $9,450.

D) credit to Income Tax Payable $127,050.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

45

The discontinued operations section of the income statement refers to the:

A) loss on products that did not sell.

B) discontinuance of a product line.

C) disposal of out of date equipment.

D) disposal of a segment of a business.

A) loss on products that did not sell.

B) discontinuance of a product line.

C) disposal of out of date equipment.

D) disposal of a segment of a business.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

46

When pretax accounting income exceeds taxable income:

A) Deferred Tax Asset is debited.

B) Deferred Tax Liability is credited.

C) Prepaid Income Tax is credited.

D) Prepaid Income Tax is debited.

A) Deferred Tax Asset is debited.

B) Deferred Tax Liability is credited.

C) Prepaid Income Tax is credited.

D) Prepaid Income Tax is debited.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

47

Income tax expense appears on the:

A) tax return.

B) statement of stockholders' equity.

C) income statement.

D) balance sheet.

A) tax return.

B) statement of stockholders' equity.

C) income statement.

D) balance sheet.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

48

An event or transaction should be considered as an extraordinary item if it is unusual in nature and if it occurs infrequently.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

49

The gain or loss on the disposal of a business segment is shown on the income statement as:

A) an extraordinary item.

B) part of discontinued operations

C) part of income from operations.

D) other gains or losses.

A) an extraordinary item.

B) part of discontinued operations

C) part of income from operations.

D) other gains or losses.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

50

Southern Corporation has pretax accounting income of $575,000 and taxable income of $560,000. The company's income tax rate is 35%. The entry to record the income tax includes a:

A) debit to Deferred Tax Asset $5,250.

B) debit to Deferred Tax Asset $196,000.

C) credit to Deferred Tax Liability $5,250.

D) credit to Deferred Tax Liability $196,000.

A) debit to Deferred Tax Asset $5,250.

B) debit to Deferred Tax Asset $196,000.

C) credit to Deferred Tax Liability $5,250.

D) credit to Deferred Tax Liability $196,000.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

51

The following items are extraordinary items EXCEPT:

A) newly enacted laws.

B) natural disasters.

C) expropriation of company assets by a foreign government.

D) losses on a failing product line.

A) newly enacted laws.

B) natural disasters.

C) expropriation of company assets by a foreign government.

D) losses on a failing product line.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

52

The formula to determine income tax expense is:

A) taxable income (from the income tax return) multiplied by the income tax rate.

B) taxable income(from the income statement) multiplied by the income tax rate.

C) income before income tax expense (from the tax return) multiplied by the income tax rate.

D) income before income tax expense (from the income statement) multiplied by the income tax rate.

A) taxable income (from the income tax return) multiplied by the income tax rate.

B) taxable income(from the income statement) multiplied by the income tax rate.

C) income before income tax expense (from the tax return) multiplied by the income tax rate.

D) income before income tax expense (from the income statement) multiplied by the income tax rate.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following statements is true?

A) The income tax return is prepared using GAAP.

B) The income tax return is prepared using rules set by the SEC.

C) The income tax return is prepared using rules set by the IRS.

D) The income tax return and the financial statements are the same documents.

A) The income tax return is prepared using GAAP.

B) The income tax return is prepared using rules set by the SEC.

C) The income tax return is prepared using rules set by the IRS.

D) The income tax return and the financial statements are the same documents.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following would be considered an extraordinary item?

A) Losses from a labor dispute

B) Losses from a natural disaster

C) Writing-down inventory to lower-of-cost or market

D) Losses from the sale of property

A) Losses from a labor dispute

B) Losses from a natural disaster

C) Writing-down inventory to lower-of-cost or market

D) Losses from the sale of property

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

55

The formula to determine income tax payable is:

A) taxable income (from the income tax return) multiplied by the income tax rate.

B) taxable income(from the income statement) multiplied by the income tax rate.

C) income before income tax expense (from the tax return) multiplied by the income tax rate.

D) income before income tax expense (from the income statement) multiplied by the income tax rate.

A) taxable income (from the income tax return) multiplied by the income tax rate.

B) taxable income(from the income statement) multiplied by the income tax rate.

C) income before income tax expense (from the tax return) multiplied by the income tax rate.

D) income before income tax expense (from the income statement) multiplied by the income tax rate.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

56

The disposal of a segment of a business is called:

A) an extraordinary item.

B) other expense.

C) a sales transaction.

D) discontinued operations.

A) an extraordinary item.

B) other expense.

C) a sales transaction.

D) discontinued operations.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

57

Income tax payable appears on the:

A) tax return.

B) statement of stockholders' equity.

C) income statement.

D) balance sheet.

A) tax return.

B) statement of stockholders' equity.

C) income statement.

D) balance sheet.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

58

The amount of tax to pay the government in the next period is known as:

A) deferred tax asset.

B) deferred tax liability.

C) income tax expense.

D) income tax payable.

A) deferred tax asset.

B) deferred tax liability.

C) income tax expense.

D) income tax payable.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

59

The estimated value of a company's stock is less than the current market value of the company. The appropriate investment decision should be to:

A) buy the company's stock.

B) hold the company's stock.

C) sell the company's stock.

D) purchase the bond's that the company has issued.

A) buy the company's stock.

B) hold the company's stock.

C) sell the company's stock.

D) purchase the bond's that the company has issued.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

60

Charming Charlie's, Inc. is going to discontinue one of its manufacturing divisions. At the time of discontinuance, the division's assets with a book value of $1,000,000 are sold for $750,000 and operating income amounted to $145,000. Ignoring income taxes, what total amount should be reported on the income statement as discontinued operations?

A) $105,000 loss

B) $250,000 loss

C) $395,000 loss

D) $145,000 gain

A) $105,000 loss

B) $250,000 loss

C) $395,000 loss

D) $145,000 gain

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

61

An extraordinary item is:

A) both infrequent and unusual for the company.

B) unusual for the company.

C) Infrequent for the company.

D) material with respect to the business and infrequent.

A) both infrequent and unusual for the company.

B) unusual for the company.

C) Infrequent for the company.

D) material with respect to the business and infrequent.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

62

Earnings per share shows how much income a company earned for each share of stock.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

63

Earnings per share is calculated:

A) only for preferred stock.

B) only for common stock.

C) for common and preferred stock.

D) only for treasury stock.

A) only for preferred stock.

B) only for common stock.

C) for common and preferred stock.

D) only for treasury stock.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

64

A correction in income of a prior-period requires a debit to the Retained Earnings account.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

65

Prepare a partial income statement starting with income before income taxes with the information below for Sawyer Corporation for the year ending December 31, 2012. The tax rate for Sawyer Corporation is 35%:

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

66

Prior-period adjustments appear on the statement of retained earnings.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

67

When a change in accounting principle occurs, the:

A) cumulative effect of the change should be reported in the current year's retained earnings statement.

B) change should be reported retroactively.

C) old accounting principle should be used for the current year.

D) new accounting principle should be used starting in the current year, with no change to the prior years.

A) cumulative effect of the change should be reported in the current year's retained earnings statement.

B) change should be reported retroactively.

C) old accounting principle should be used for the current year.

D) new accounting principle should be used starting in the current year, with no change to the prior years.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

68

All of the following are true regarding changes in accounting principles EXCEPT:

A) Accounting changes are allowed when new principles are preferred over previous ones.

B) The company retrospectively restates all prior-period amounts as though the new accounting method had been in effect all along.

C) The majority of the changes in accounting principles are reported in the current period when the change in principle occurred.

D) If an accounting change impacts periods prior to the earliest one presented in the current income statement, an adjustment to retained earnings must be made.

A) Accounting changes are allowed when new principles are preferred over previous ones.

B) The company retrospectively restates all prior-period amounts as though the new accounting method had been in effect all along.

C) The majority of the changes in accounting principles are reported in the current period when the change in principle occurred.

D) If an accounting change impacts periods prior to the earliest one presented in the current income statement, an adjustment to retained earnings must be made.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

69

The income statement provides better information about a company than the statement of cash flows.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

70

The amount of a company's net income per share of its outstanding common stock is:

A) net income per share.

B) gross profit per share.

C) earnings per share.

D) taxable income per share.

A) net income per share.

B) gross profit per share.

C) earnings per share.

D) taxable income per share.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

71

Extraordinary items:

A) include the expropriation of a company's assets by a foreign government.

B) include the loss from the sale or exchange of equipment.

C) are treated the same under IFRS and GAAP.

D) include the gains and losses due to management restructuring.

A) include the expropriation of a company's assets by a foreign government.

B) include the loss from the sale or exchange of equipment.

C) are treated the same under IFRS and GAAP.

D) include the gains and losses due to management restructuring.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

72

If an item is unusual but not infrequent it is:

A) reported net of tax as Other Gains and Losses.

B) reported at its gross amount as Other Gains and Losses.

C) disclosed as a note to the financial statements.

D) reported as an extraordinary item.

A) reported net of tax as Other Gains and Losses.

B) reported at its gross amount as Other Gains and Losses.

C) disclosed as a note to the financial statements.

D) reported as an extraordinary item.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

73

If a company reports both basic and diluted EPS, diluted EPS will always be lower than basic EPS.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

74

Prior-period adjustments are reported on the income statement.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

75

A prior-period adjustment is reported as an adjustment to the beginning balance of retained earnings.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

76

The ratio that uses weighted-average number of shares of common stock outstanding in the denominator is the:

A) earnings per share.

B) gross profit percentage.

C) price-earnings ratio.

D) current ratio.

A) earnings per share.

B) gross profit percentage.

C) price-earnings ratio.

D) current ratio.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

77

Items appear on the income statement in which order?

A) Extraordinary items, Discontinued operations, Other revenues and expenses

B) Discontinued operations, Extraordinary items, Other revenues and expenses

C) Other revenues and expenses, Discontinued operations, Extraordinary items

D) Other revenues and expenses, Extraordinary items, Discontinued operations

A) Extraordinary items, Discontinued operations, Other revenues and expenses

B) Discontinued operations, Extraordinary items, Other revenues and expenses

C) Other revenues and expenses, Discontinued operations, Extraordinary items

D) Other revenues and expenses, Extraordinary items, Discontinued operations

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

78

The income statement and the statement of cash flows often paint the same picture of the company.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

79

Central City, Inc. has incurred a $50,000 loss on property due to an earthquake. Earthquakes have occurred in this region. What amount will be reported for this loss on company's income statement, assuming a 30% tax rate?

A) $50,000

B) $35,000

C) $15,000

D) Zero, due to the fact that this event is infrequent in nature.

A) $50,000

B) $35,000

C) $15,000

D) Zero, due to the fact that this event is infrequent in nature.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

80

Changes in accounting estimates:

A) are not allowed under GAAP.

B) are a prior period adjustment

C) are reported for the current and future periods on the new basis.

D) require prior financial statements to be restated.

A) are not allowed under GAAP.

B) are a prior period adjustment

C) are reported for the current and future periods on the new basis.

D) require prior financial statements to be restated.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 125 flashcards in this deck.