Deck 18: Standard Costing and Variance Analysis

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

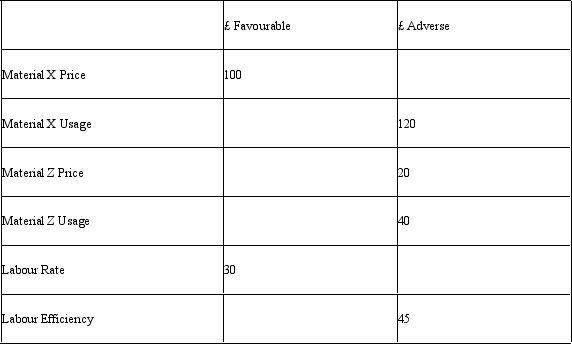

A company is reviewing the variances for the previous month:

Which of the following statements is most likely to be INCORRECT?

A) There is an adverse variance overall. This could be due to the standard being out of date

B) The large favourable price variance on Material X indicates that buyers have found the best deal for the company

C) The favourable labour rate and adverse efficiency variances could be the result of using new, inexperienced staff

D) An adverse labour rate variance could be the result of a recent pay rise

Which of the following statements is most likely to be INCORRECT?

A) There is an adverse variance overall. This could be due to the standard being out of date

B) The large favourable price variance on Material X indicates that buyers have found the best deal for the company

C) The favourable labour rate and adverse efficiency variances could be the result of using new, inexperienced staff

D) An adverse labour rate variance could be the result of a recent pay rise

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/25

Play

Full screen (f)

Deck 18: Standard Costing and Variance Analysis

1

Direct labour efficiency variance can be expresses as:

A) Standard hours x (actual rate - standard rate)

B) Standard rate x (actual hours - standard hours)

C) Standard rate x (actual hours + standard hours)

D) Actual rate x (actual hours - standard hours)

A) Standard hours x (actual rate - standard rate)

B) Standard rate x (actual hours - standard hours)

C) Standard rate x (actual hours + standard hours)

D) Actual rate x (actual hours - standard hours)

B

2

Standard costing can help establish variances in costs,but does not consider the volume of production

False

3

Which of the following would lead to a materials price variance?

A) More materials have been used than standard

B) More labour hours have been worked than standard

C) The price of materials was higher than standard

D) Direct labour rate was higher than standard

A) More materials have been used than standard

B) More labour hours have been worked than standard

C) The price of materials was higher than standard

D) Direct labour rate was higher than standard

C

4

The LAH company produces product BG,which includes variable overhead standard cost of 5 hours at £15 per hour,based on a budget production of 3,000 units.The actual results for the last period were as follows:

Calculate the variable overhead cost variance.

A) £5,000 favorable

B) £5,000 adverse

C) £7,500 favorable

D) £7,500 adverse

Calculate the variable overhead cost variance.

A) £5,000 favorable

B) £5,000 adverse

C) £7,500 favorable

D) £7,500 adverse

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

5

Direct materials usage variance can be expressed as:

A) Actual quantity x (standard price - actual quantity)

B) Actual quantity x (standard price x standard quantity)

C) Standard price x (actual quantity x standard quantity)

D) Standard price x (actual quantity - standard quantity)

A) Actual quantity x (standard price - actual quantity)

B) Actual quantity x (standard price x standard quantity)

C) Standard price x (actual quantity x standard quantity)

D) Standard price x (actual quantity - standard quantity)

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

6

Direct materials price variance can be expressed as:

A) Actual quantity x (actual price - standard price)

B) Actual quantity x (standard price x standard quantity)

C) Standard price x (actual quantity x standard quantity)

D) Standard price x (actual quantity - standard quantity)

A) Actual quantity x (actual price - standard price)

B) Actual quantity x (standard price x standard quantity)

C) Standard price x (actual quantity x standard quantity)

D) Standard price x (actual quantity - standard quantity)

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following is likely to cause an adverse fixed overhead variance?

A) Unexpectedly large maintenance expense

B) Inflation

C) "Fixed overheads" were not as fixed as first thought and increased as production increased

D) All of the above

A) Unexpectedly large maintenance expense

B) Inflation

C) "Fixed overheads" were not as fixed as first thought and increased as production increased

D) All of the above

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

8

The sales margin volume variance measures the effect of a change in sales price

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

9

While standard costing can help establish how actual performance differs from standard performance,it is not compatible with performance related pay systems

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

10

Variable overhead variances are typically in proportion to direct labour variance,as variable overheads are typically charged as a proportion of direct labour hours

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

11

LR Kinncaid Company assembles steel components for trains.The standard labour cost per unit is:

3 hours @ £3.20 per hour

The actual results for last period were:

Calculate the direct labour efficiency variance

A) £48,000 favorable

B) £48,000 adverse

C) £1,650 favorable

D) £1,650 adverse

3 hours @ £3.20 per hour

The actual results for last period were:

Calculate the direct labour efficiency variance

A) £48,000 favorable

B) £48,000 adverse

C) £1,650 favorable

D) £1,650 adverse

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

12

The LAH company produces product BG,which includes variable overhead standard cost of 5 hours at £15 per hour,based on a budget production of 3,000 units.The actual results for the last period were as follows:

Calculate the variable overhead efficiency variance.

A) £5,000 favorable

B) £5,000 adverse

C) £7,500 favorable

D) £7,500 adverse

Calculate the variable overhead efficiency variance.

A) £5,000 favorable

B) £5,000 adverse

C) £7,500 favorable

D) £7,500 adverse

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

13

LR Kinncaid Company assembles steel components for trains.The standard labour cost per unit is:

3 hours @ £3.20 per hour

The actual results for last period were:

Calculate the direct labour rate variance

A) £48,000 favorable

B) £48,000 adverse

C) £1,650 favorable

D) £1,650 adverse

3 hours @ £3.20 per hour

The actual results for last period were:

Calculate the direct labour rate variance

A) £48,000 favorable

B) £48,000 adverse

C) £1,650 favorable

D) £1,650 adverse

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

14

Fixed overhead expenditure variance can be expressed as:

A) Actual fixed overhead - budget fixed overhead

B) Actual fixed overhead/budget fixed overhead

C) Actual fixed overhead x budget fixed overhead

D) Budget fixed overhead/actual fixed overhead

A) Actual fixed overhead - budget fixed overhead

B) Actual fixed overhead/budget fixed overhead

C) Actual fixed overhead x budget fixed overhead

D) Budget fixed overhead/actual fixed overhead

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

15

Variable overhead price variance can be expressed as:

A) Actual quantity x (actual price + standard price)

B) Actual price x ( actual price - standard price)

C) Actual quantity x (actual price - standard price)

D) Standard price x ( actual quantity - standard quantity)

A) Actual quantity x (actual price + standard price)

B) Actual price x ( actual price - standard price)

C) Actual quantity x (actual price - standard price)

D) Standard price x ( actual quantity - standard quantity)

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

16

An adverse variable overhead cost variance might mean that some item of variable overhead,such as cleaning costs,has cost more than expected

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following would lead to a labour usage variance?

A) More materials have been used than standard

B) More labour hours have been worked than standard

C) The price of materials was higher than standard

D) Direct labour rate was higher than standard

A) More materials have been used than standard

B) More labour hours have been worked than standard

C) The price of materials was higher than standard

D) Direct labour rate was higher than standard

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

18

The direct labour rate variance can be expressed as:

A) Actual hours x (actual rate - standard rate)

B) Standard rate x (actual hours - standard hours)

C) Actual hours x (standard rate x standard hours)

D) Standard rate x (actual hours/standard hours)

A) Actual hours x (actual rate - standard rate)

B) Standard rate x (actual hours - standard hours)

C) Actual hours x (standard rate x standard hours)

D) Standard rate x (actual hours/standard hours)

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following would be the most likely cause of an adverse material usage variance?

A) Use of cheaper (lower quality) of materials

B) Having to purchase materials at short notice (and higher price)

C) Increase in market prices

D) Labour overtime

A) Use of cheaper (lower quality) of materials

B) Having to purchase materials at short notice (and higher price)

C) Increase in market prices

D) Labour overtime

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

20

What might you assume if a company had a favourable material price variance and an unfavourable material usage variance?

A) Direct labour rate was higher than standard

B) The actual material cost per unit was less than the standard cost per unit

C) Less material per unit was used than the standard usage per unit

D) All of the above

A) Direct labour rate was higher than standard

B) The actual material cost per unit was less than the standard cost per unit

C) Less material per unit was used than the standard usage per unit

D) All of the above

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

21

A company is reviewing the variances for the previous month:

Which of the following statements is most likely to be INCORRECT?

A) There is an adverse variance overall. This could be due to the standard being out of date

B) The large favourable price variance on Material X indicates that buyers have found the best deal for the company

C) The favourable labour rate and adverse efficiency variances could be the result of using new, inexperienced staff

D) An adverse labour rate variance could be the result of a recent pay rise

Which of the following statements is most likely to be INCORRECT?

A) There is an adverse variance overall. This could be due to the standard being out of date

B) The large favourable price variance on Material X indicates that buyers have found the best deal for the company

C) The favourable labour rate and adverse efficiency variances could be the result of using new, inexperienced staff

D) An adverse labour rate variance could be the result of a recent pay rise

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

22

The Standard Cost Card for a batch of 3,000 bottles of shampoo includes the following:

1,500 litres of liquid S at £0.30 per litre

1)5kg of powder P at £1.20 per kg

A batch of 3,000 bottles had the following usage:

1,700 litres of liquid S which cost £476 and 1.2kg of powder which cost £1.80

What are the material price and usage variances for the liquid?

A) The Usage Variance is £30 Favourable and the Price Variance is £56 Adverse

B) The Usage Variance is £56 Adverse and the Price Variance is £30 Favourable

C) The Usage Variance is £60 Adverse and the Price Variance is £34 Favourable

D) The Usage Variance is £34 Adverse and the Price Variance is £60 Favourable

1,500 litres of liquid S at £0.30 per litre

1)5kg of powder P at £1.20 per kg

A batch of 3,000 bottles had the following usage:

1,700 litres of liquid S which cost £476 and 1.2kg of powder which cost £1.80

What are the material price and usage variances for the liquid?

A) The Usage Variance is £30 Favourable and the Price Variance is £56 Adverse

B) The Usage Variance is £56 Adverse and the Price Variance is £30 Favourable

C) The Usage Variance is £60 Adverse and the Price Variance is £34 Favourable

D) The Usage Variance is £34 Adverse and the Price Variance is £60 Favourable

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

23

A company has a total budgeted fixed overhead of £135,000 for the year.

Budgeted production is 15,000 units per year.Each unit takes 45 minutes.

Production and costs are spread evenly throughout the year.Overheads are absorbed on the basis of labour hours.

In one month,1,200 units are made and 800 hours are worked.The overhead cost is £10,000.

Which of the following statements are correct?

(i) The Budgeted Overhead Absorption Rate is £12.00 per hour

(ii) The Overhead Absorption Rate is £12.50

(iii) The Fixed Overhead Expenditure Variance is £1,250 Favourable

(iv) The Fixed Overhead Expenditure Variance is £400 Adverse

(v) The Fixed Overhead Volume Variance is £1,650 Adverse

(vi)The Fixed Overhead Volume Variance is £450 Adverse

A) (i), (iii) and (vi)

B) (ii), (iii) and (v)

C) (i) and (iv) only

D) None of them are correct

Budgeted production is 15,000 units per year.Each unit takes 45 minutes.

Production and costs are spread evenly throughout the year.Overheads are absorbed on the basis of labour hours.

In one month,1,200 units are made and 800 hours are worked.The overhead cost is £10,000.

Which of the following statements are correct?

(i) The Budgeted Overhead Absorption Rate is £12.00 per hour

(ii) The Overhead Absorption Rate is £12.50

(iii) The Fixed Overhead Expenditure Variance is £1,250 Favourable

(iv) The Fixed Overhead Expenditure Variance is £400 Adverse

(v) The Fixed Overhead Volume Variance is £1,650 Adverse

(vi)The Fixed Overhead Volume Variance is £450 Adverse

A) (i), (iii) and (vi)

B) (ii), (iii) and (v)

C) (i) and (iv) only

D) None of them are correct

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

24

The Standard Cost Card for a batch of 3,000 bottles of shampoo includes the following:

36 hours in Process 1 at £6.00 per hour

4 hours in Process 2 at £9.00 per hour

A batch of 3,000 bottles had the following usage:

40 hours in Process 1 at a total cost of £260

3)5 hours in process 2 at a cost of £35.

What are the labour efficiency and rate variances for the Process 2?

A) The Efficiency Variance is £3.50 Favourable and the Rate Variance is £4.50 Adverse

B) The Efficiency Variance is £4.50 Favourable and the Rate Variance is £3.50 Adverse

C) The Efficiency Variance is £4 Favourable and the Rate Variance is £1 Adverse

D) The Efficiency Variance is £4 Adverse and the Rate Variance is £5 Favourable

36 hours in Process 1 at £6.00 per hour

4 hours in Process 2 at £9.00 per hour

A batch of 3,000 bottles had the following usage:

40 hours in Process 1 at a total cost of £260

3)5 hours in process 2 at a cost of £35.

What are the labour efficiency and rate variances for the Process 2?

A) The Efficiency Variance is £3.50 Favourable and the Rate Variance is £4.50 Adverse

B) The Efficiency Variance is £4.50 Favourable and the Rate Variance is £3.50 Adverse

C) The Efficiency Variance is £4 Favourable and the Rate Variance is £1 Adverse

D) The Efficiency Variance is £4 Adverse and the Rate Variance is £5 Favourable

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following statements is INCORRECT?

A) Variances are often inter-related and must never be considered in isolation

B) Standards are difficult to set

C) A favourable sales variance is always good news

D) Variances are useful for monthly reporting to various managers across the business

A) Variances are often inter-related and must never be considered in isolation

B) Standards are difficult to set

C) A favourable sales variance is always good news

D) Variances are useful for monthly reporting to various managers across the business

Unlock Deck

Unlock for access to all 25 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 25 flashcards in this deck.