Deck 8: Managing Interest Rate Risk: Economic Value of Equity

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following bank information for questions

What is the weighted average duration of assets?

A)2.56 years

B)3.75 years

C)4.85 years

D)5.00 years

E)7.5 years

What is the weighted average duration of assets?

A)2.56 years

B)3.75 years

C)4.85 years

D)5.00 years

E)7.5 years

Question

Question

Question

Question

Question

Use the following bank information for questions

What is the bank's expected economic net interest income?

A)$14.75

B)$32.25

C)$44.00

D)$76.25

E)$120.25

What is the bank's expected economic net interest income?

A)$14.75

B)$32.25

C)$44.00

D)$76.25

E)$120.25

Question

Question

Use the following bank information for questions

If interest rates rise 1% for all assets and liabilities, what is the approximate expected change in the economic value of equity?

A)-$2.56

B)$5.84

C)-$5.84

D)$6.85

E)-$6.85

If interest rates rise 1% for all assets and liabilities, what is the approximate expected change in the economic value of equity?

A)-$2.56

B)$5.84

C)-$5.84

D)$6.85

E)-$6.85

Question

Question

Question

Use the following bank information for questions

What is the bank's weighted average cost of liabilities?

A)$44

B)$76

C)$80

D)$94

E)$102

What is the bank's weighted average cost of liabilities?

A)$44

B)$76

C)$80

D)$94

E)$102

Question

Use the following bank information for questions

What is the bank's expected economic net interest income?

A)$34.5

B)$32.3

C)$39.5

D)$44.0

E)$120.5

What is the bank's expected economic net interest income?

A)$34.5

B)$32.3

C)$39.5

D)$44.0

E)$120.5

Question

Use the following bank information for questions

What is the bank's duration gap?

A)0.53

B)0.73

C)0.91

D)1.88

E)4.58

What is the bank's duration gap?

A)0.53

B)0.73

C)0.91

D)1.88

E)4.58

Question

Question

Use the following bank information for questions

What is the bank's duration gap?

A)0.53

B)0.73

C)0.91

D)2.03

E)4.58

What is the bank's duration gap?

A)0.53

B)0.73

C)0.91

D)2.03

E)4.58

Question

Question

Question

Question

Use the following bank information for questions

If interest rates rise 1% for all assets and liabilities, what is the approximate expected change in the economic value of equity?

A)-$2.56

B)$5.84

C)-$5.84

D)$22.19

E)-$22.19

If interest rates rise 1% for all assets and liabilities, what is the approximate expected change in the economic value of equity?

A)-$2.56

B)$5.84

C)-$5.84

D)$22.19

E)-$22.19

Question

Use the following bank information for questions

What is the bank's weighted average cost of liabilities?

A)$24.9

B)$34.5

C)$80.0

D)$94.3

E)$102.1

What is the bank's weighted average cost of liabilities?

A)$24.9

B)$34.5

C)$80.0

D)$94.3

E)$102.1

Question

Use the following bank information for questions

What is the weighted average duration of assets?

A)2.56 years

B)3.85 years

C)4.85 years

D)5.00 years

E)7.5 years

What is the weighted average duration of assets?

A)2.56 years

B)3.85 years

C)4.85 years

D)5.00 years

E)7.5 years

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/55

Play

Full screen (f)

Deck 8: Managing Interest Rate Risk: Economic Value of Equity

1

A 20-year annual coupon bond is currently selling for its par value of $10,000 with an annual yield of 7%.If the bond is callable at par, what is the effective duration of the bond, assuming rates change by 2%?

A)25.00 years

B)20.00 years

C)5.52 years

D)4.56 years

E)3.68 years

A)25.00 years

B)20.00 years

C)5.52 years

D)4.56 years

E)3.68 years

D

2

Which of the following is likely to have a negative effective duration?

A)A high coupon, interest only mortgage-backed security that is pre-paying at a high rate.

B)A low coupon U.S.Treasury bond.

C)Fed Funds purchased.

D)Demand deposits

E)None of the above can have a negative effective duration.

A)A high coupon, interest only mortgage-backed security that is pre-paying at a high rate.

B)A low coupon U.S.Treasury bond.

C)Fed Funds purchased.

D)Demand deposits

E)None of the above can have a negative effective duration.

A

3

What does a bank's duration gap measure?

A)The duration of short-term buckets minus the duration of long-term buckets.

B)The duration of the bank's assets minus the duration of its liabilities.

C)The duration of all rate-sensitive assets minus the duration of rate-sensitive liabilities.

D)The duration of the bank's liabilities minus the duration of its assets.

E)The duration of all rate-sensitive liabilities minus the duration of rate-sensitive assets.

A)The duration of short-term buckets minus the duration of long-term buckets.

B)The duration of the bank's assets minus the duration of its liabilities.

C)The duration of all rate-sensitive assets minus the duration of rate-sensitive liabilities.

D)The duration of the bank's liabilities minus the duration of its assets.

E)The duration of all rate-sensitive liabilities minus the duration of rate-sensitive assets.

B

4

Put the following steps in duration gap analysis in the proper order.

A)III, I, IV, II

B)I, II, III, IV

C)III, IV, I, II

D)IV, I, II, III

E)II, IV, I, III

A)III, I, IV, II

B)I, II, III, IV

C)III, IV, I, II

D)IV, I, II, III

E)II, IV, I, III

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following is false regarding duration gap analysis?

A)Duration gap analysis does not classify assets as rate-sensitive.

B)Duration gap analysis indicates the potential change in a bank's net interest income.

C)Duration gap accounts for bank leverage.

D)Duration gap accounts for the present value of cash flows associated with all liabilities.

E)Duration gap analysis indicates the potential change in a bank's market value of equity.

A)Duration gap analysis does not classify assets as rate-sensitive.

B)Duration gap analysis indicates the potential change in a bank's net interest income.

C)Duration gap accounts for bank leverage.

D)Duration gap accounts for the present value of cash flows associated with all liabilities.

E)Duration gap analysis indicates the potential change in a bank's market value of equity.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

6

A 10-year annual coupon bond is currently selling for its par value of $1,000 with an annual yield of 5%.If the bond is callable at par, what is the effective duration of the bond, assuming rates change by 1%?

A)10 years

B)7.36 years

C)5.52 years

D)4.60 years

E)3.68 years

A)10 years

B)7.36 years

C)5.52 years

D)4.60 years

E)3.68 years

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following is true regarding duration gap analysis?

A)The magnitude of the duration gap is related to the amount of interest rate risk a bank is subject to.

B)Management can adjust the duration gap to speculate on future interest rate changes.

C)A positive duration gap means a bank's market value of equity will decrease with an increase in interest rates.

D)All of the above are true.

E)a.and c.

A)The magnitude of the duration gap is related to the amount of interest rate risk a bank is subject to.

B)Management can adjust the duration gap to speculate on future interest rate changes.

C)A positive duration gap means a bank's market value of equity will decrease with an increase in interest rates.

D)All of the above are true.

E)a.and c.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

8

A 30-year zero coupon bond with a face value of $10,000 is currently selling for $2,313.77.Using the bond's modified duration, what is the approximate change in the price of the bond if interest rates rise by 15 basis points?

A)-15.00%

B)-4.29%

C)-0.43%

D)-0.15%

E)Not enough information is given to answer the question.

A)-15.00%

B)-4.29%

C)-0.43%

D)-0.15%

E)Not enough information is given to answer the question.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

9

A 20-year zero coupon bond with a face value of $1,000 is currently selling for $214.55.Using the bond's modified duration, what is the approximate change in the price of the bond if interest rates rise by 25 basis points?

A)-49.63%

B)-46.39%

C)-4.96%

D)-4.63%

E)Not enough information is given to answer the question.

A)-49.63%

B)-46.39%

C)-4.96%

D)-4.63%

E)Not enough information is given to answer the question.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

10

A bond has a Macaulay's duration of 21 years.If rates rise from 5% to 5.5%, the bonds price will:

A)increase by approximately 1%.

B)decrease by approximately 1%.

C)increase by approximately 10%.

D)decrease by approximately 10%.

E)Not enough information is given to answer the question.

A)increase by approximately 1%.

B)decrease by approximately 1%.

C)increase by approximately 10%.

D)decrease by approximately 10%.

E)Not enough information is given to answer the question.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

11

Duration gap analysis:

A)applies he the concept of duration to the bank's entire balance sheet.

B)applies he the concept of duration to the bank's entire income statement.

C)applies he the concept of duration to the bank's retained earnings.

D)indicates the difference in the GAP in the time it takes to collect on loan payments versus the time to attract deposits.

E)estimates when embedded options will be exercised.

A)applies he the concept of duration to the bank's entire balance sheet.

B)applies he the concept of duration to the bank's entire income statement.

C)applies he the concept of duration to the bank's retained earnings.

D)indicates the difference in the GAP in the time it takes to collect on loan payments versus the time to attract deposits.

E)estimates when embedded options will be exercised.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

12

Effective duration:

A)estimates when embedded options will be used.

B)directly indicates how much the price of a security will change given a change in interest rates.

C)is always greater than maturity.

D)is a weighted average of the time until cash flows are received.

E)All of the above

A)estimates when embedded options will be used.

B)directly indicates how much the price of a security will change given a change in interest rates.

C)is always greater than maturity.

D)is a weighted average of the time until cash flows are received.

E)All of the above

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

13

Macaulay's duration:

A)is a weighted average of the time until cash flows are received.

B)is always greater than maturity.

C)is never equal to maturity.

D)directly indicates how much the price of a security will change given a change in interest rates.

E)estimates when embedded options will be used.

A)is a weighted average of the time until cash flows are received.

B)is always greater than maturity.

C)is never equal to maturity.

D)directly indicates how much the price of a security will change given a change in interest rates.

E)estimates when embedded options will be used.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following would generally be considered price sensitive?

A)Fed funds purchased

B)Fed funds sold

C)Repurchase agreements

D)Demand deposits

E)A 20-year zero coupon bond

A)Fed funds purchased

B)Fed funds sold

C)Repurchase agreements

D)Demand deposits

E)A 20-year zero coupon bond

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following allows a security's cash flows to change when interest rates change?

A)Modified duration

B)Macaulay's duration

C)Effective duration

D)Balance sheet duration

E)Income statement duration

A)Modified duration

B)Macaulay's duration

C)Effective duration

D)Balance sheet duration

E)Income statement duration

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

16

A bond has a Macaulay's duration of 26.56 years.If rates rise from 6.25% to 6.50%, the bonds price will:

A)increase by approximately 6.25%.

B)decrease by approximately 6.25%.

C)increase by approximately 6.50%.

D)decrease by approximately 6.50%.

E)Not enough information is given to answer the question.

A)increase by approximately 6.25%.

B)decrease by approximately 6.25%.

C)increase by approximately 6.50%.

D)decrease by approximately 6.50%.

E)Not enough information is given to answer the question.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

17

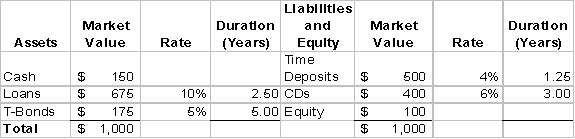

Use the following bank information for questions

What is the weighted average duration of assets?

A)2.56 years

B)3.75 years

C)4.85 years

D)5.00 years

E)7.5 years

What is the weighted average duration of assets?

A)2.56 years

B)3.75 years

C)4.85 years

D)5.00 years

E)7.5 years

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

18

EVE analysis: is essentially a _____________ analysis.

A)profitability

B)quality

C)liquidity

D)liquidation

E)earnings

A)profitability

B)quality

C)liquidity

D)liquidation

E)earnings

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

19

Modified duration:

A)estimates when embedded options will be used.

B)directly indicates how much the price of a security will change given a change in interest rates.

C)is always greater than maturity.

D)All of the above

E)a.and b.

A)estimates when embedded options will be used.

B)directly indicates how much the price of a security will change given a change in interest rates.

C)is always greater than maturity.

D)All of the above

E)a.and b.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

20

A bond has a Macaulay's duration of 10.7 years.If rates fall from 7% to 6%, the bonds price will:

A)increase by approximately 1%.

B)decrease by approximately 1%.

C)increase by approximately 10%.

D)decrease by approximately 10%.

E)Not enough information is given to answer the question.

A)increase by approximately 1%.

B)decrease by approximately 1%.

C)increase by approximately 10%.

D)decrease by approximately 10%.

E)Not enough information is given to answer the question.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

21

For a bank that has a positive duration gap, an increase in interest rates will cause a(n) _______ in the economic value of assets, a(n) _______ in the economic value of liabilities, and a(n) _______ in the economic value of equity.

A)increase, decrease, increase

B)increase, increase, decrease

C)increase, increase, increase

D)decrease, decrease, increase

E)decrease, decrease, decrease

A)increase, decrease, increase

B)increase, increase, decrease

C)increase, increase, increase

D)decrease, decrease, increase

E)decrease, decrease, decrease

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

22

Use the following bank information for questions

What is the bank's expected economic net interest income?

A)$14.75

B)$32.25

C)$44.00

D)$76.25

E)$120.25

What is the bank's expected economic net interest income?

A)$14.75

B)$32.25

C)$44.00

D)$76.25

E)$120.25

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

23

A liability sensitive bank decides to reduce risk by marketing 2-year CDs paying 5% instead of NOW accounts that pay 4%.The bank will benefit if:

A)the 2-year rate in one year is less than 5%.

B)the 1-year rate in one year is less than 6%.

C)the 1-year rate in one year is greater than 6%.

D)the 2-year rate in one year is greater than 6%.

E)Not enough information is given to determine the correct answer.

A)the 2-year rate in one year is less than 5%.

B)the 1-year rate in one year is less than 6%.

C)the 1-year rate in one year is greater than 6%.

D)the 2-year rate in one year is greater than 6%.

E)Not enough information is given to determine the correct answer.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

24

Use the following bank information for questions

If interest rates rise 1% for all assets and liabilities, what is the approximate expected change in the economic value of equity?

A)-$2.56

B)$5.84

C)-$5.84

D)$6.85

E)-$6.85

If interest rates rise 1% for all assets and liabilities, what is the approximate expected change in the economic value of equity?

A)-$2.56

B)$5.84

C)-$5.84

D)$6.85

E)-$6.85

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

25

For a bank that has a negative duration gap, an increase in interest rates will cause a(n) _______ in the economic value of assets, a(n) _______ in the economic value of liabilities, and a(n) _______ in the economic value of equity.

A)increase, decrease, increase

B)increase, increase, decrease

C)increase, increase, increase

D)decrease, decrease, increase

E)decrease, increase, decrease

A)increase, decrease, increase

B)increase, increase, decrease

C)increase, increase, increase

D)decrease, decrease, increase

E)decrease, increase, decrease

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

26

What is the strength of static GAP analysis relative to duration gap analysis?

A)Static GAP analysis recognizes the time value of money of each cash flow.

B)Static GAP analysis provides a measure of the total portfolio's interest rate risk.

C)Static GAP analysis is easier to understand.

D)Static GAP analysis takes the long-run view while duration gap analysis takes a shorter-run view.

E)The static GAP measure directly correlates with the risk of the bank, i.e., a bank with twice the static GAP is twice as risky.

A)Static GAP analysis recognizes the time value of money of each cash flow.

B)Static GAP analysis provides a measure of the total portfolio's interest rate risk.

C)Static GAP analysis is easier to understand.

D)Static GAP analysis takes the long-run view while duration gap analysis takes a shorter-run view.

E)The static GAP measure directly correlates with the risk of the bank, i.e., a bank with twice the static GAP is twice as risky.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

27

Use the following bank information for questions

What is the bank's weighted average cost of liabilities?

A)$44

B)$76

C)$80

D)$94

E)$102

What is the bank's weighted average cost of liabilities?

A)$44

B)$76

C)$80

D)$94

E)$102

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

28

Use the following bank information for questions

What is the bank's expected economic net interest income?

A)$34.5

B)$32.3

C)$39.5

D)$44.0

E)$120.5

What is the bank's expected economic net interest income?

A)$34.5

B)$32.3

C)$39.5

D)$44.0

E)$120.5

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

29

Use the following bank information for questions

What is the bank's duration gap?

A)0.53

B)0.73

C)0.91

D)1.88

E)4.58

What is the bank's duration gap?

A)0.53

B)0.73

C)0.91

D)1.88

E)4.58

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

30

What are the weaknesses of using static GAP analysis versus duration gap analysis?

A)Static GAP ignores the time value of money.

B)Static GAP ignores the cumulative impact of interest rate changes on a bank's risk profile.

C)Static GAP does not proscribe the treatment of demand deposits.

D)All of the above are weaknesses of using static GAP analysis versus duration gap analysis.

E)a.and b.

A)Static GAP ignores the time value of money.

B)Static GAP ignores the cumulative impact of interest rate changes on a bank's risk profile.

C)Static GAP does not proscribe the treatment of demand deposits.

D)All of the above are weaknesses of using static GAP analysis versus duration gap analysis.

E)a.and b.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

31

Use the following bank information for questions

What is the bank's duration gap?

A)0.53

B)0.73

C)0.91

D)2.03

E)4.58

What is the bank's duration gap?

A)0.53

B)0.73

C)0.91

D)2.03

E)4.58

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

32

For a bank that has a positive duration gap, a decrease in interest rates will cause a(n) _______ in the economic value of assets, a(n) _______ in the economic value of liabilities, and a(n) _______ in the economic value of equity.

A)increase, decrease, increase

B)increase, increase, decrease

C)increase, increase, increase

D)decrease, decrease, increase

E)decrease, increase, decrease

A)increase, decrease, increase

B)increase, increase, decrease

C)increase, increase, increase

D)decrease, decrease, increase

E)decrease, increase, decrease

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

33

If the yield curve is inverted, a portfolio manager can take advantage of this by:

A)pricing more deposits on a fixed-rate basis.

B)buying more long-term securities

C)making variable-rate, callable loans.

D)increasing the number of rate-sensitive assets.

E)All of the above.

A)pricing more deposits on a fixed-rate basis.

B)buying more long-term securities

C)making variable-rate, callable loans.

D)increasing the number of rate-sensitive assets.

E)All of the above.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

34

To perfectly immunize a bank's economic value of equity from changes in interest rate risk, it should:

A)adjust assets and liabilities such that its duration gap is equal to one.

B)adjust assets and liabilities such that its duration gap is greater than zero.

C)adjust assets and liabilities such that its duration gap is equal to zero.

D)adjust assets and liabilities such that its GAP is equal to zero.

E)adjust assets and liabilities such that its GAP is less than one.

A)adjust assets and liabilities such that its duration gap is equal to one.

B)adjust assets and liabilities such that its duration gap is greater than zero.

C)adjust assets and liabilities such that its duration gap is equal to zero.

D)adjust assets and liabilities such that its GAP is equal to zero.

E)adjust assets and liabilities such that its GAP is less than one.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

35

Use the following bank information for questions

If interest rates rise 1% for all assets and liabilities, what is the approximate expected change in the economic value of equity?

A)-$2.56

B)$5.84

C)-$5.84

D)$22.19

E)-$22.19

If interest rates rise 1% for all assets and liabilities, what is the approximate expected change in the economic value of equity?

A)-$2.56

B)$5.84

C)-$5.84

D)$22.19

E)-$22.19

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

36

Use the following bank information for questions

What is the bank's weighted average cost of liabilities?

A)$24.9

B)$34.5

C)$80.0

D)$94.3

E)$102.1

What is the bank's weighted average cost of liabilities?

A)$24.9

B)$34.5

C)$80.0

D)$94.3

E)$102.1

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

37

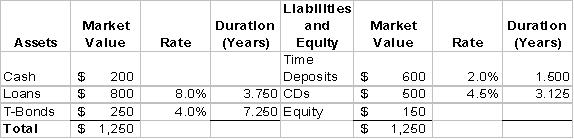

Use the following bank information for questions

What is the weighted average duration of assets?

A)2.56 years

B)3.85 years

C)4.85 years

D)5.00 years

E)7.5 years

What is the weighted average duration of assets?

A)2.56 years

B)3.85 years

C)4.85 years

D)5.00 years

E)7.5 years

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following will not affect a bank's duration estimate for the year?

A)Prepayments on loans that exceed expectations.

B)A 20-year corporate bond that is unexpectedly called in 6 months.

C)Certificates of deposit that are withdrawn early.

D)Holding a 30-year Treasury bond until maturity.

E)All of the above will affect a bank's estimated duration for the year.

A)Prepayments on loans that exceed expectations.

B)A 20-year corporate bond that is unexpectedly called in 6 months.

C)Certificates of deposit that are withdrawn early.

D)Holding a 30-year Treasury bond until maturity.

E)All of the above will affect a bank's estimated duration for the year.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following is not a weakness of duration gap analysis?

A)It is difficult to accurately compute duration.

B)Each future cash flow must be discounted by the appropriate future interest rate.

C)The duration of a portfolio must be constantly monitored.

D)It is difficult to estimate the duration on zero coupon bonds.

E)All of the above are weaknesses of duration gap analysis.

A)It is difficult to accurately compute duration.

B)Each future cash flow must be discounted by the appropriate future interest rate.

C)The duration of a portfolio must be constantly monitored.

D)It is difficult to estimate the duration on zero coupon bonds.

E)All of the above are weaknesses of duration gap analysis.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

40

For a bank that has a negative duration gap, a decrease in interest rates will cause a(n) _______ in the economic value of assets, a(n) _______ in the economic value of liabilities, and a(n) _______ in the economic value of equity.

A)increase, decrease, increase

B)increase, increase, decrease

C)increase, increase, increase

D)decrease, decrease, increase

E)decrease, increase, decrease

A)increase, decrease, increase

B)increase, increase, decrease

C)increase, increase, increase

D)decrease, decrease, increase

E)decrease, increase, decrease

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

41

An asset that is rate-sensitive is generally not price sensitive.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

42

Economic value of equity analysis focuses on net interest income.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

43

Effective duration considers a security's embedded options.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

44

A bank with a duration gap of 1 is more sensitive to changes in the economic value of equity than a bank with a duration gap of -1.5.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

45

Why is it difficult to estimate the duration of demand deposits?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

46

Discuss the differences between assets and liabilities that are price sensitive and those that are rate sensitive.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

47

The yield curve is typically inverted at the peak of the business cycle.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

48

How does effective duration differ from modified duration?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

49

Banks should never assume any interest rate risk.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

50

Discuss why a bank may have to sacrifice yield to vary its duration gap.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

51

Duration gap analysis focuses on changes in net interest income.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

52

The duration of a liability that does not pay interest must be equal to 0.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

53

Duration of equity measures the dollar change in EVE with a 1% change in interest rates.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

54

An investor that matches the duration of an investment with her holding period balances price risk and reinvestment risk.

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

55

What are the strengths and weaknesses of duration gap analysis?

Unlock Deck

Unlock for access to all 55 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 55 flashcards in this deck.