Deck 26: Standard Costing and Variance Analysis

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

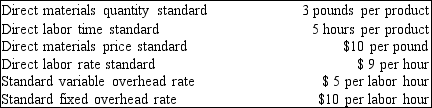

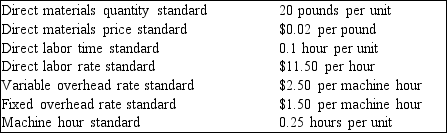

Ewing Corporation's controller has developed the cost and usage data listed below in preparation of standard unit cost information for the coming year.  The total standard unit cost is

The total standard unit cost is

A) $105.

B) $150.

C) $260.

D) $34.

The total standard unit cost isA) $105.

B) $150.

C) $260.

D) $34.

Question

Question

Question

Question

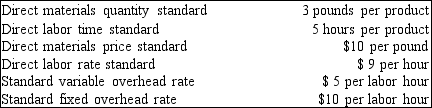

Ewing Corporation's controller has developed the cost and usage data listed below in preparation of standard unit cost information for the coming year.  The standard unit cost for direct labor is

The standard unit cost for direct labor is

A) $45.

B) $27.

C) $135.

D) $9.

The standard unit cost for direct labor isA) $45.

B) $27.

C) $135.

D) $9.

Question

Question

Question

Question

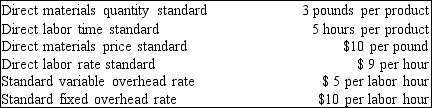

Ewing Corporation's controller has developed the cost and usage data listed below in preparation of standard unit cost information for the coming year.  The standard unit cost for overhead is

The standard unit cost for overhead is

A) $15.

B) $25.

C) $50.

D) $75.

The standard unit cost for overhead isA) $15.

B) $25.

C) $50.

D) $75.

Question

Question

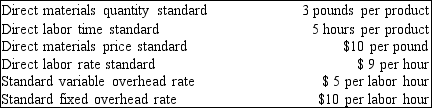

Ewing Corporation's controller has developed the cost and usage data listed below in preparation of standard unit cost information for the coming year.  The standard unit cost for direct materials is

The standard unit cost for direct materials is

A) $30.

B) $10.

C) $50.

D) $27.

The standard unit cost for direct materials isA) $30.

B) $10.

C) $50.

D) $27.

Question

Using the following information, compute the standard unit cost of a 20 pound bag of dog food:

A) $2.55

B) $2.21

C) $2.15

D) $2.80

A) $2.55

B) $2.21

C) $2.15

D) $2.80

Question

Question

Question

Question

Using the standard costs of $5 per pound for a 10 pound bag of chocolate and the following actual cost and usage data, compute the direct materials variance.

A) $45,000 (F)

B) $45,000 (U)

C) $54,000 (F)

D) $99,000 (F)

A) $45,000 (F)

B) $45,000 (U)

C) $54,000 (F)

D) $99,000 (F)

Question

Question

Question

Question

Question

Question

Question

Question

Using the standard costs of $5 per pound for a 10 pound bag of chocolate and the following actual cost and usage data, compute the direct materials quantity variance.

A) $45,000 (F)

B) $45,000 (U)

C) $54,000 (F)

D) $99,000 (F)

A) $45,000 (F)

B) $45,000 (U)

C) $54,000 (F)

D) $99,000 (F)

Question

Question

Question

Question

Using the standard costs of $5 per pound for a 10 pound bag of chocolate and the following actual cost and usage data, compute the direct materials price variance.

A) $45,000 (F)

B) $45,000 (U)

C) $54,000 (F)

D) $99,000 (F)

A) $45,000 (F)

B) $45,000 (U)

C) $54,000 (F)

D) $99,000 (F)

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/120

Play

Full screen (f)

Deck 26: Standard Costing and Variance Analysis

1

Standard costs are realistically predetermined costs of direct materials, direct labor, and overhead that usually are expressed as a cost per unit.

True

2

Predetermined overhead costs are the same as standard costs.

False

3

Service organizations use direct materials, direct labor, and overhead standard costs.

False

4

Although expensive to install and maintain, a standard cost accounting system can save a company considerable amounts of money by reducing resource waste.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

5

The direct labor rate standard is either set by a labor contract or defined by the company.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

6

A variance is the difference between a standard cost and a budgeted cost.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

7

Standard costs are based solely on expected future costs and conditions.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

8

The importance of direct labor standards and variances has been reduced.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

9

Standard costing is typically a sophisticated and inexpensive component to add to a company's existing cost accounting system.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

10

The standard overhead cost is the sum of the estimates of variable and fixed overhead costs in the next accounting period.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

11

The purchasing agent is responsible for developing the direct materials quantity standard.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

12

If standard costing is not economically feasible for a company, predetermined overhead rates should not be used.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

13

Even if a variance is insignificant, corrective action should be taken.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

14

The direct materials price standard is a carefully derived estimate or projected amount of what a particular type of direct material will cost when purchased during the next accounting period.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

15

Direct labor time standards express the hourly labor cost per function or job classification that exists during the current accounting period.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

16

Once standard costs for direct materials, direct labor, and variable and fixed overhead have been developed, a total standard unit cost can be determined at any time.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

17

Variance analysis involves computing the difference between standard and actual costs.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

18

The standard fixed overhead rate is usually based on the expected number of standard machine hours.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

19

The direct materials price standard is determined by averaging costs of current purchases.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

20

When a manufacturing company employs standard costs, all costs affecting the three inventory accounts and the Cost of Goods Sold account are stated in terms of standard or predetermined costs rather than in terms of actual costs incurred.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

21

The fixed overhead volume variance measures the use of existing facilities and capacity.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

22

The direct materials price variance is the difference between the actual price and the standard price, multiplied by the standard quantity.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

23

A flexible budget is a summary of expected costs for a range of activity levels and is geared to changes in the level of productive output.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

24

The static budget can be adjusted automatically for changes in the level of output.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

25

The total overhead variance is the difference between standard variable overhead costs and standard fixed overhead costs.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

26

If actual capacity used exceeds expected capacity, the fixed overhead volume variance is favorable.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

27

The "flex" in the flexible budget formula occurs in the variable cost segment.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

28

The direct materials quantity variance is the difference between the actual quantity used and the standard quantity times the standard price.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

29

The direct labor efficiency variance is the difference between the standard hours allowed and the actual hours multiplied by the actual labor rate.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

30

The variable overhead efficiency variance is the difference between actual total overhead costs incurred and the total overhead costs applied using the standard overhead rates.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

31

It is not necessary to provide an area on the performance report for a manager's reasons for variances.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

32

Another name for a flexible budget is a variable budget.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

33

A performance report should contain cost or revenue items that the manager receiving the report can control.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

34

The direct labor rate variance is the difference between actual hours worked and standard hours allowed for good units produced, multiplied by the standard labor rate.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

35

Comparing "what did happen" with "what should have happened" aids in the performance evaluation of a company.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

36

The variable overhead spending variance is also called the variable overhead efficiency variance.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

37

A production manager usually is responsible for direct materials used and direct labor hours used.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

38

The flexible budget formula is an equation that determines unexpected costs at any level of output.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

39

The final step in variance analysis is determining the cause of the variance.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

40

In a standard costing system, standard costs eventually flow into the

A) Cost of Goods Sold account.

B) Standard Cost account.

C) Selling and Administrative Expenses account.

D) Sales account.

A) Cost of Goods Sold account.

B) Standard Cost account.

C) Selling and Administrative Expenses account.

D) Sales account.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

41

A standard costing system

A) is not typically used by management for cost planning and cost control purposes.

B) is a system in which all costs affecting the three inventory accounts and the Cost of Goods Sold account are stated in terms of actual costs incurred.

C) depends on actual costs rather than planned costs.

D) is employed with an existing job order costing or process costing system and is not a full cost accounting system in itself.

A) is not typically used by management for cost planning and cost control purposes.

B) is a system in which all costs affecting the three inventory accounts and the Cost of Goods Sold account are stated in terms of actual costs incurred.

C) depends on actual costs rather than planned costs.

D) is employed with an existing job order costing or process costing system and is not a full cost accounting system in itself.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

42

The use of realistic predetermined unit costs to facilitate product costing, cost control, cost flow, and inventory valuation is a description of the

A) flexible budget concept.

B) budgetary control concept.

C) capacity level concept.

D) standard cost accounting concept.

A) flexible budget concept.

B) budgetary control concept.

C) capacity level concept.

D) standard cost accounting concept.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

43

Standard unit costs generally do not include which of the following?

A) Direct materials costs

B) Indirect materials costs

C) President's salary

D) Depreciation on machinery

A) Direct materials costs

B) Indirect materials costs

C) President's salary

D) Depreciation on machinery

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

44

Service organizations do not develop standards for

A) any service costs.

B) overhead.

C) direct materials.

D) labor.

A) any service costs.

B) overhead.

C) direct materials.

D) labor.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

45

One drawback of using standard costing is that it is

A) expensive to use.

B) difficult to implement.

C) often inaccurate.

D) not applicable to most manufacturing systems.

A) expensive to use.

B) difficult to implement.

C) often inaccurate.

D) not applicable to most manufacturing systems.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

46

Ewing Corporation's controller has developed the cost and usage data listed below in preparation of standard unit cost information for the coming year. The total standard unit cost is

A) $105.

B) $150.

C) $260.

D) $34.

The total standard unit cost isA) $105.

B) $150.

C) $260.

D) $34.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

47

A standard cost accounting system can be used for

A) direct materials.

B) overhead.

C) direct labor.

D) all of these.

A) direct materials.

B) overhead.

C) direct labor.

D) all of these.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following provides an explanation of why the variable overhead rate is separated from the fixed overhead rate in standard costing?

A) There is no justifiable reason; their separation is merely to simplify entries.

B) Both calculations divide by the same direct labor hours, but the numerator is different for each calculation.

C) The variable overhead rate is calculated using actual direct labor hours, whereas the fixed overhead rate is calculated using normal capacity direct labor hours.

D) Different application bases are generally appropriate.

A) There is no justifiable reason; their separation is merely to simplify entries.

B) Both calculations divide by the same direct labor hours, but the numerator is different for each calculation.

C) The variable overhead rate is calculated using actual direct labor hours, whereas the fixed overhead rate is calculated using normal capacity direct labor hours.

D) Different application bases are generally appropriate.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

49

Standard costs are useful for all but which of the following?

A) Determining actual costs

B) Preparing budgets and forecasts

C) Evaluating the performance of workers and management

D) Helping to develop appropriate selling prices

A) Determining actual costs

B) Preparing budgets and forecasts

C) Evaluating the performance of workers and management

D) Helping to develop appropriate selling prices

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

50

Ewing Corporation's controller has developed the cost and usage data listed below in preparation of standard unit cost information for the coming year. The standard unit cost for direct labor is

A) $45.

B) $27.

C) $135.

D) $9.

The standard unit cost for direct labor isA) $45.

B) $27.

C) $135.

D) $9.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

51

A purpose of standard costing is to

A) control costs.

B) allocate costs more accurately.

C) replace subjective decision making.

D) compute the breakeven point.

A) control costs.

B) allocate costs more accurately.

C) replace subjective decision making.

D) compute the breakeven point.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

52

Standard costs for company products are typically used for all except which of the following?

A) Variance analysis and cost control

B) Computing production costs in operating budgets

C) Determining actual costs per unit

D) Determining the cost of goods completed and transferred to finished goods inventory

A) Variance analysis and cost control

B) Computing production costs in operating budgets

C) Determining actual costs per unit

D) Determining the cost of goods completed and transferred to finished goods inventory

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

53

In standard costing,

A) the standards are developed only for overhead costs.

B) the standards are developed primarily from past costs.

C) comparisons with actual costs usually are not performed.

D) debit and credit entries to inventory accounts are made at standard costs.

A) the standards are developed only for overhead costs.

B) the standards are developed primarily from past costs.

C) comparisons with actual costs usually are not performed.

D) debit and credit entries to inventory accounts are made at standard costs.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

54

Ewing Corporation's controller has developed the cost and usage data listed below in preparation of standard unit cost information for the coming year. The standard unit cost for overhead is

A) $15.

B) $25.

C) $50.

D) $75.

The standard unit cost for overhead isA) $15.

B) $25.

C) $50.

D) $75.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

55

Under which of the following circumstances would the base used to calculate the variable overhead rate be the same as that used for the fixed overhead rate?

A) When actual labor hours are the same as budgeted labor hours

B) When standard indirect labor hours agree with standard direct labor hours

C) In most circumstances; the base used for each calculation is normally the same.

D) When the number of labor hours expected to be incurred for the period is the same as normal capacity direct labor hours

A) When actual labor hours are the same as budgeted labor hours

B) When standard indirect labor hours agree with standard direct labor hours

C) In most circumstances; the base used for each calculation is normally the same.

D) When the number of labor hours expected to be incurred for the period is the same as normal capacity direct labor hours

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

56

Ewing Corporation's controller has developed the cost and usage data listed below in preparation of standard unit cost information for the coming year. The standard unit cost for direct materials is

A) $30.

B) $10.

C) $50.

D) $27.

The standard unit cost for direct materials isA) $30.

B) $10.

C) $50.

D) $27.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

57

Using the following information, compute the standard unit cost of a 20 pound bag of dog food:

A) $2.55

B) $2.21

C) $2.15

D) $2.80

A) $2.55

B) $2.21

C) $2.15

D) $2.80

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

58

An expression of the hourly labor pay cost per function or job classification that is expected to exist during the next accounting period is the definition of a

A) direct labor time standard.

B) direct materials quantity standard.

C) direct labor rate standard.

D) variable overhead rate.

A) direct labor time standard.

B) direct materials quantity standard.

C) direct labor rate standard.

D) variable overhead rate.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

59

Multiplying the standard price of direct materials by the standard quantity for direct materials yields

A) the direct materials price variance.

B) the direct materials quantity variance.

C) the standard direct materials cost.

D) nothing; the two components should be added together.

A) the direct materials price variance.

B) the direct materials quantity variance.

C) the standard direct materials cost.

D) nothing; the two components should be added together.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

60

A(n) ________ cost is synonymous with the product cost calculated in a conventional standard cost accounting system.

A) fixed

B) direct

C) joint

D) expected

A) fixed

B) direct

C) joint

D) expected

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

61

Using the standard costs of $5 per pound for a 10 pound bag of chocolate and the following actual cost and usage data, compute the direct materials variance.

A) $45,000 (F)

B) $45,000 (U)

C) $54,000 (F)

D) $99,000 (F)

A) $45,000 (F)

B) $45,000 (U)

C) $54,000 (F)

D) $99,000 (F)

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

62

During the current month, Ringo Company started 50,000 units of product and transferred 40,000 fully completed units to finished goods. The final work in process inventory was 40 percent complete as to labor operations. There was no initial work in process, and actual labor hours were 180,000 for the period. Each unit should have required 4 direct labor hours to be produced at standard. The total standard hours allowed for the period are

A) 180,000.

B) 176,000.

C) 171,000.

D) 186,000.

A) 180,000.

B) 176,000.

C) 171,000.

D) 186,000.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

63

A flexible budget is most useful

A) for budgeting and planning purposes.

B) when actual output equals budgeted output.

C) as a cost control tool to help evaluate performance.

D) when a product's cost structure includes variable costs only.

A) for budgeting and planning purposes.

B) when actual output equals budgeted output.

C) as a cost control tool to help evaluate performance.

D) when a product's cost structure includes variable costs only.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

64

Using the labor time standard of 0.5 labor hour per unit and a labor cost standard of $10 per labor hour for a 10 pound bag of chocolate and the following actual cost and usage data, compute the direct labor variance. Direct labor haurs used hours

Total cost of direct labor

Number of good urits produced units

A) $3,960 (F)

B) $8,460 (U)

C) $3,960 (U)

D) $8,460 (F)

Total cost of direct labor

Number of good urits produced units

A) $3,960 (F)

B) $8,460 (U)

C) $3,960 (U)

D) $8,460 (F)

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

65

The formula used to compute budgeted total cost at any level of activity is presented in the

A) flexible budget.

B) performance report.

C) static budget.

D) cash flow forecast.

A) flexible budget.

B) performance report.

C) static budget.

D) cash flow forecast.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

66

The difference between actual quantity used and standard quantity multiplied by standard price is the equation for computing the

A) direct labor efficiency variance.

B) direct materials price variance.

C) direct labor rate variance.

D) direct materials quantity variance.

A) direct labor efficiency variance.

B) direct materials price variance.

C) direct labor rate variance.

D) direct materials quantity variance.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

67

The direct materials price variance is best measured and reported to appropriate management personnel at the time

A) purchased quantities exceed standard order size.

B) quarterly financial statements are prepared.

C) shipments are received and recorded as purchases.

D) direct materials are issued to production areas.

A) purchased quantities exceed standard order size.

B) quarterly financial statements are prepared.

C) shipments are received and recorded as purchases.

D) direct materials are issued to production areas.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

68

Variance analysis includes all of the following except

A) taking corrective action.

B) investigating all variances.

C) developing performance measures to track activities causing the variance.

D) identification of the cause.

A) taking corrective action.

B) investigating all variances.

C) developing performance measures to track activities causing the variance.

D) identification of the cause.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

69

Using the standard costs of $5 per pound for a 10 pound bag of chocolate and the following actual cost and usage data, compute the direct materials quantity variance.

A) $45,000 (F)

B) $45,000 (U)

C) $54,000 (F)

D) $99,000 (F)

A) $45,000 (F)

B) $45,000 (U)

C) $54,000 (F)

D) $99,000 (F)

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

70

The direct materials standards for the main product of Duchess Company are 8 grams of direct materials per product at a cost of $3 per gram. During April, 969 grams of direct materials were used to produce 120 products at a direct materials cost of $2,900. The direct materials quantity variance for April was

A) $57 (U).

B) $77 (U).

C) $27 (U).

D) $97 (F).

A) $57 (U).

B) $77 (U).

C) $27 (U).

D) $97 (F).

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

71

If a company's flexible budget formula is $9.50 per unit plus $67,900, what would be the total budget for evaluating operating performance if 23,850 units were sold and 28,460 units were produced?

A) $294,475

B) $338,270

C) $309,335

D) $226,575

A) $294,475

B) $338,270

C) $309,335

D) $226,575

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

72

A direct labor rate variance would occur in which of the following situations?

A) When a production employee takes an unplanned break

B) When a production employee spends more time producing one product than was expected

C) When a low-paid production employee performs a task higher than his or her assigned level

D) When a production employee incurs overtime hours at the same hourly rate as regular pay

A) When a production employee takes an unplanned break

B) When a production employee spends more time producing one product than was expected

C) When a low-paid production employee performs a task higher than his or her assigned level

D) When a production employee incurs overtime hours at the same hourly rate as regular pay

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

73

Using the standard costs of $5 per pound for a 10 pound bag of chocolate and the following actual cost and usage data, compute the direct materials price variance.

A) $45,000 (F)

B) $45,000 (U)

C) $54,000 (F)

D) $99,000 (F)

A) $45,000 (F)

B) $45,000 (U)

C) $54,000 (F)

D) $99,000 (F)

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

74

If the actual amount of direct materials used equals the standard amount of direct materials that should have been used, the difference between the standard cost and actual cost of direct materials is called the

A) price variance.

B) rate variance.

C) quantity variance.

D) efficiency variance.

A) price variance.

B) rate variance.

C) quantity variance.

D) efficiency variance.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

75

"The difference between actual hours worked and standard hours allowed for the good units produced, multiplied by the standard labor rate" is a description of the

A) direct labor rate variance.

B) direct labor efficiency variance.

C) total direct labor cost variance.

D) direct labor quantity variance.

A) direct labor rate variance.

B) direct labor efficiency variance.

C) total direct labor cost variance.

D) direct labor quantity variance.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

76

The primary difference between a fixed (static) budget and a flexible budget is that a fixed budget

A) cannot be changed after the period begins, whereas a flexible budget can be changed after the period begins.

B) is concerned only with future acquisitions of fixed assets, whereas a flexible budget is concerned with expenses that vary with sales.

C) is a plan for a single level of production, whereas a flexible budget is several plans (one for each of several production levels).

D) includes only fixed costs, whereas a flexible budget includes only variable costs.

A) cannot be changed after the period begins, whereas a flexible budget can be changed after the period begins.

B) is concerned only with future acquisitions of fixed assets, whereas a flexible budget is concerned with expenses that vary with sales.

C) is a plan for a single level of production, whereas a flexible budget is several plans (one for each of several production levels).

D) includes only fixed costs, whereas a flexible budget includes only variable costs.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

77

Using the labor time standard of 0.5 labor hour per unit and a labor cost standard of $10 per labor hour for a 10 pound bag of chocolate and the following actual cost and usage data, compute the direct labor rate variance. Direct labor haurs used hours

Total cost of direct labor

Number of good urits produced units

A) $4,500 (U)

B) $4,500 (F)

C) $3,960 (F)

D) $3,960 (U)

Total cost of direct labor

Number of good urits produced units

A) $4,500 (U)

B) $4,500 (F)

C) $3,960 (F)

D) $3,960 (U)

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

78

A summary of expected costs for a range of activity levels that is geared to changes in the level of productive output is the definition of a

A) continuous budget.

B) flexible budget.

C) master budget.

D) period budget.

A) continuous budget.

B) flexible budget.

C) master budget.

D) period budget.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

79

Suppose the standard for a given cost during a period was $80,000. The actual cost for the period was $72,000. Under what circumstances would you consider the variance from budget to be a positive performance indication?

A) The cost is fixed, and actual production was 90 percent of the standard level of budgeted production.

B) The cost is variable, and the standard cost noted above is the cost at a production level lower than the actual production level.

C) The cost is variable, and actual production was 90 percent of the standard level of production.

D) The cost is variable, and actual production was 75 percent of the standard level of production.

A) The cost is fixed, and actual production was 90 percent of the standard level of budgeted production.

B) The cost is variable, and the standard cost noted above is the cost at a production level lower than the actual production level.

C) The cost is variable, and actual production was 90 percent of the standard level of production.

D) The cost is variable, and actual production was 75 percent of the standard level of production.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

80

Lucas Company has set standards for the manufacturing of clay pots to be 2 pounds of direct materials, per pot, at a cost of $3 per pound. During the current period, 600 pounds of direct materials were purchased for $1872. All of the direct materials were used to manufacture 295 pots. Lucas's direct materials price variance was

A) $102 (U).

B) $72 (U).

C) $102 (F).

D) zero.

A) $102 (U).

B) $72 (U).

C) $102 (F).

D) zero.

Unlock Deck

Unlock for access to all 120 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 120 flashcards in this deck.