Deck 11: Costs and Profit Maximization Under Competition

Full screen (f)

Question

Question

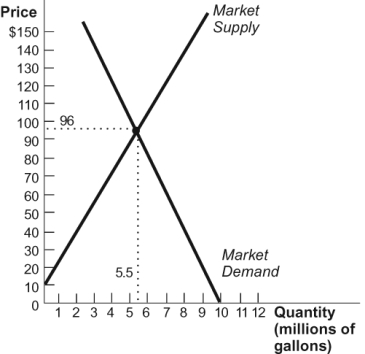

Figure: World Market for Maple Syrup  Refer to the figure. If you are one of literally thousands of maple syrup producers and you wanted to increase your maple syrup production from 100 gallons to 110 gallons, what price would you charge?

Refer to the figure. If you are one of literally thousands of maple syrup producers and you wanted to increase your maple syrup production from 100 gallons to 110 gallons, what price would you charge?

A) $100

B) $110

C) $96

D) $10

Refer to the figure. If you are one of literally thousands of maple syrup producers and you wanted to increase your maple syrup production from 100 gallons to 110 gallons, what price would you charge?A) $100

B) $110

C) $96

D) $10

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Figure: Profit Maximizing Output  Use the figure. The profit-maximizing output for this firm is:

Use the figure. The profit-maximizing output for this firm is:

A) 40.

B) 3.

C) 6.

D) 9.

Use the figure. The profit-maximizing output for this firm is:A) 40.

B) 3.

C) 6.

D) 9.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

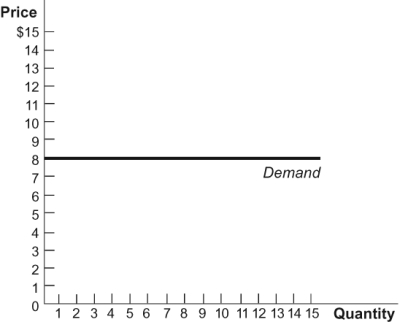

Figure: Elastic Demand  If the total cost of producing 11 units of output in this figure is $16, the firm's economic profit at 11 units of output is:

If the total cost of producing 11 units of output in this figure is $16, the firm's economic profit at 11 units of output is:

A) $8.

B) -$8.

C) $72.

D) $104.

If the total cost of producing 11 units of output in this figure is $16, the firm's economic profit at 11 units of output is:A) $8.

B) -$8.

C) $72.

D) $104.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following to answer questions:

Figure: Maximizing Profit

The change in total cost from producing the eighth unit of output is ______, and the change in total revenue from producing the seventh unit of output is ______.

A) $5; $14

B) $10; $70

C) $7; $6.50

D) $3.50; $6.50

Figure: Maximizing Profit

The change in total cost from producing the eighth unit of output is ______, and the change in total revenue from producing the seventh unit of output is ______.

A) $5; $14

B) $10; $70

C) $7; $6.50

D) $3.50; $6.50

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following to answer questions:

Figure: Maximizing Profit

(Figure: Maximizing Profit) What is the firm's profit-maximizing level of output?

A) 4

B) 7

C) 9

D) 12

Figure: Maximizing Profit

(Figure: Maximizing Profit) What is the firm's profit-maximizing level of output?

A) 4

B) 7

C) 9

D) 12

Question

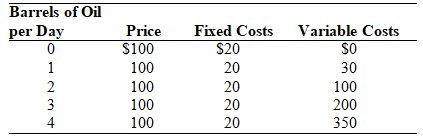

Table: Profit Maximization 2

The firm in this table can earn a maximum profit of ______, which occurs at an output of ______ barrels per day.

A) $380; 4

B) $80; 3

C) $100; 0

D) $200; 2

The firm in this table can earn a maximum profit of ______, which occurs at an output of ______ barrels per day.

A) $380; 4

B) $80; 3

C) $100; 0

D) $200; 2

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/217

Play

Full screen (f)

Deck 11: Costs and Profit Maximization Under Competition

1

Firms in a perfectly competitive industry maximize profits by:

A) eliminating the competition.

B) producing a higher quality good and setting a price higher than the competition.

C) setting a price equal to the market price.

D) setting a price less than the market price and undercutting the competition.

A) eliminating the competition.

B) producing a higher quality good and setting a price higher than the competition.

C) setting a price equal to the market price.

D) setting a price less than the market price and undercutting the competition.

setting a price equal to the market price.

2

Figure: World Market for Maple Syrup Refer to the figure. If you are one of literally thousands of maple syrup producers and you wanted to increase your maple syrup production from 100 gallons to 110 gallons, what price would you charge?

A) $100

B) $110

C) $96

D) $10

Refer to the figure. If you are one of literally thousands of maple syrup producers and you wanted to increase your maple syrup production from 100 gallons to 110 gallons, what price would you charge?A) $100

B) $110

C) $96

D) $10

$96

3

If a single supplier produces a good with many good substitutes, then:

A) it will have little control over the market price.

B) the demand curve for its output will be downward sloping.

C) the price it chooses to set must be less than the market price in order to sell additional output.

D) the market demand will be perfectly elastic.

A) it will have little control over the market price.

B) the demand curve for its output will be downward sloping.

C) the price it chooses to set must be less than the market price in order to sell additional output.

D) the market demand will be perfectly elastic.

it will have little control over the market price.

4

A perfectly competitive industry exists under which of the following conditions?

I. The product sold is similar across firms.

II. There are many sellers, each small relative to the total market.

III. There are many sellers, each with total assets less than $2 million.

IV. The threat of competition exists from potential sellers that have not yet entered the market.

A) I and II only

B) I, II, and III only

C) I, III, and IV only

D) I, II, and IV only

I. The product sold is similar across firms.

II. There are many sellers, each small relative to the total market.

III. There are many sellers, each with total assets less than $2 million.

IV. The threat of competition exists from potential sellers that have not yet entered the market.

A) I and II only

B) I, II, and III only

C) I, III, and IV only

D) I, II, and IV only

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

5

In Texas, what does the term nodding donkey mean?

A) a donkey that is well-fed

B) an oil pump

C) a ranger

D) a cowboy

A) a donkey that is well-fed

B) an oil pump

C) a ranger

D) a cowboy

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

6

In a highly competitive industry, demand for a firm's product is:

A) perfectly elastic.

B) slightly elastic.

C) unit elastic.

D) perfectly inelastic.

A) perfectly elastic.

B) slightly elastic.

C) unit elastic.

D) perfectly inelastic.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

7

When there are many buyers and sellers of a good and the product sold is identical across firms,:

A) the demand curve for each firm's output is perfectly elastic.

B) the industry demand curve is perfectly elastic.

C) the demand curve for each firm's output is perfectly inelastic.

D) the industry demand curve is perfectly inelastic.

A) the demand curve for each firm's output is perfectly elastic.

B) the industry demand curve is perfectly elastic.

C) the demand curve for each firm's output is perfectly inelastic.

D) the industry demand curve is perfectly inelastic.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

8

When there are many buyers and sellers of a good and the product sold is identical across firms,:

A) the demand curve for each firm's output is somewhat elastic.

B) the industry demand curve is somewhat elastic.

C) the demand curve for each firm's output is perfectly inelastic.

D) the industry demand curve is perfectly inelastic

A) the demand curve for each firm's output is somewhat elastic.

B) the industry demand curve is somewhat elastic.

C) the demand curve for each firm's output is perfectly inelastic.

D) the industry demand curve is perfectly inelastic

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

9

The short run is defined as:

A) the period before any changes in a firm's output can be made.

B) less than six months.

C) less than one year.

D) the period before entry or exit can occur.

A) the period before any changes in a firm's output can be made.

B) less than six months.

C) less than one year.

D) the period before entry or exit can occur.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

10

When competitive firms do not have influence over the price of their product, all of the following are true EXCEPT which condition?

A) The product they produce is similar across sellers.

B) The product appeals more strongly to some consumers than others.

C) There are many potential sellers.

D) There are many buyers and sellers, each small relative to the total market.

A) The product they produce is similar across sellers.

B) The product appeals more strongly to some consumers than others.

C) There are many potential sellers.

D) There are many buyers and sellers, each small relative to the total market.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

11

Firms in competitive industries:

I. can only charge a price equal to the market price.

II. cannot charge any more than the market price.

III. will earn less profit if they charge less than the market price.

A) I only

B) I and III only

C) II only

D) I, II, and III

I. can only charge a price equal to the market price.

II. cannot charge any more than the market price.

III. will earn less profit if they charge less than the market price.

A) I only

B) I and III only

C) II only

D) I, II, and III

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

12

A market is considered perfectly competitive if:

I. there is a lot of product differentiation among sellers.

II. there are many sellers, each small relative to the total market.

III. the product sold is similar across sellers.

IV. there are only a few buyers.

A) I and II only

B) I, II, and III only

C) II and III only

D) II, III, and IV only

I. there is a lot of product differentiation among sellers.

II. there are many sellers, each small relative to the total market.

III. the product sold is similar across sellers.

IV. there are only a few buyers.

A) I and II only

B) I, II, and III only

C) II and III only

D) II, III, and IV only

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

13

In the small town of Wellsville, there is only one grocery store. Given that everyone needs food, we would expect that this grocery store:

A) is a monopoly and hence highly profitable.

B) charges exorbitant prices.

C) prices competitively.

D) faces a perfectly inelastic demand.

A) is a monopoly and hence highly profitable.

B) charges exorbitant prices.

C) prices competitively.

D) faces a perfectly inelastic demand.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

14

An industry is said to be perfectly competitive when:

A) demand in the industry is high.

B) each firm has virtually no influence over the price of its product.

C) there are many buyers and sellers, and each is large relative to the total market.

D) supply in the industry is highly elastic.

A) demand in the industry is high.

B) each firm has virtually no influence over the price of its product.

C) there are many buyers and sellers, and each is large relative to the total market.

D) supply in the industry is highly elastic.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

15

To maximize profits, a firm in a highly competitive industry should set its price:

A) higher than the market price.

B) lower than the market price.

C) at the market price.

D) it depends: sometimes at the market price but sometimes higher or lower.

A) higher than the market price.

B) lower than the market price.

C) at the market price.

D) it depends: sometimes at the market price but sometimes higher or lower.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

16

If a single supplier produces such a small portion of the total market output that changes in its production have no impact on the overall market price,:

A) the firm will eventually be forced out of business.

B) demand for the firm's output is perfectly elastic.

C) the firm's supply curve is perfectly inelastic.

D) the market supply curve is horizontal.

A) the firm will eventually be forced out of business.

B) demand for the firm's output is perfectly elastic.

C) the firm's supply curve is perfectly inelastic.

D) the market supply curve is horizontal.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following best illustrates a product sold in a perfectly competitive market?

A) soft drinks

B) jeans

C) eggs

D) televisions

A) soft drinks

B) jeans

C) eggs

D) televisions

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following is NOT a key decision that a firm must make?

A) what price to set

B) what quantity to produce

C) where to produce

D) when to enter and exit an industry

A) what price to set

B) what quantity to produce

C) where to produce

D) when to enter and exit an industry

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

19

At a ski resort located over one hour from the nearest large town, there is only one grocery store and it charges prices more than 200% percent above the typical retail prices. In the long run, we would expect that:

A) another store will open that will charge equally high prices since competition is low.

B) the store will continue to earn high profits even in the long run since the size of the market is small.

C) demand will decrease since people will not want to pay the high prices.

D) another store will open that will charge lower prices.

A) another store will open that will charge equally high prices since competition is low.

B) the store will continue to earn high profits even in the long run since the size of the market is small.

C) demand will decrease since people will not want to pay the high prices.

D) another store will open that will charge lower prices.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

20

Economists call the time after all exit or entry has occurred:

A) the short run.

B) the medium run.

C) the long run.

D) the marginal run.

A) the short run.

B) the medium run.

C) the long run.

D) the marginal run.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

21

Marginal cost is:

A) the change in total cost from producing one more unit of output.

B) total cost divided by the change in total output.

C) the change in total output divided by the change in total cost.

D) average cost times output.

A) the change in total cost from producing one more unit of output.

B) total cost divided by the change in total output.

C) the change in total output divided by the change in total cost.

D) average cost times output.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

22

A market becomes more competitive as the product becomes ______ homogeneous and there are ______ potential sellers.

A) more and more; more

B) less and less; more

C) more and more; fewer

D) less and less; fewer

A) more and more; more

B) less and less; more

C) more and more; fewer

D) less and less; fewer

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

23

In the long run, demand is ______ the short run.

A) more elastic than in

B) less elastic than in

C) equally elastic as in

D) indeterminately different in elasticity as compared with

A) more elastic than in

B) less elastic than in

C) equally elastic as in

D) indeterminately different in elasticity as compared with

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

24

When a firm expands output from 10 to 11 units and total revenue increases from $100 to $110, marginal revenue of the eleventh unit is:

A) $110.

B) $11.

C) $10.

D) $210.

A) $110.

B) $11.

C) $10.

D) $210.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

25

A flat firm-level demand curve means:

A) full market pricing power.

B) limited market pricing power.

C) no market pricing power.

D) seasonal market pricing power.

A) full market pricing power.

B) limited market pricing power.

C) no market pricing power.

D) seasonal market pricing power.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

26

The demand curve for oil from OPEC is:

A) flat.

B) vertical.

C) upward-sloping.

D) downward-sloping.

A) flat.

B) vertical.

C) upward-sloping.

D) downward-sloping.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

27

Figure: Profit Maximizing Output Use the figure. The profit-maximizing output for this firm is:

A) 40.

B) 3.

C) 6.

D) 9.

Use the figure. The profit-maximizing output for this firm is:A) 40.

B) 3.

C) 6.

D) 9.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

28

In competitive markets, the demand curve faced by the individual firm is:

A) equal to the market demand curve.

B) perfectly elastic.

C) perfectly inelastic.

D) downward sloping.

A) equal to the market demand curve.

B) perfectly elastic.

C) perfectly inelastic.

D) downward sloping.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

29

Fewer potential sellers make a firm-level demand curve ______ in the ______.

A) flatter; short run

B) flatter; long run

C) steeper; short run

D) steeper; long run

A) flatter; short run

B) flatter; long run

C) steeper; short run

D) steeper; long run

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

30

The marginal revenue (MR) for a firm is a constant $45, and the firm's marginal cost (MC) is given by MC = 1.5Q (where Q is quantity of output). What is the firm's profit-maximizing level of output?

A) 67.5

B) 30

C) 45

D) 15

A) 67.5

B) 30

C) 45

D) 15

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

31

According to the text, the demand curve for oil from a particular stripper well is:

A) flat.

B) vertical.

C) upward-sloping.

D) downward-sloping.

A) flat.

B) vertical.

C) upward-sloping.

D) downward-sloping.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

32

The amount of money that the firm pays for its inputs is called:

A) marginal cost.

B) total cost.

C) variable cost.

D) fixed cost.

A) marginal cost.

B) total cost.

C) variable cost.

D) fixed cost.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

33

Profit is defined as:

A) net revenue minus depreciation.

B) average revenue minus average total cost.

C) marginal revenue minus marginal cost.

D) total revenue minus total cost.

A) net revenue minus depreciation.

B) average revenue minus average total cost.

C) marginal revenue minus marginal cost.

D) total revenue minus total cost.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

34

If Homer operates a small bakery and sells donuts for $4/dozen, he should:

A) sell an additional dozen donuts as long as the marginal cost of producing an additional dozen donuts is less than $4.

B) sell an additional dozen donuts as long as the total cost of producing an additional dozen donuts is less than $4.

C) only sell more donuts if his total revenue is greater than his total cost.

D) sell an additional dozen donuts so long as the fixed cost of production is greater than $4.

A) sell an additional dozen donuts as long as the marginal cost of producing an additional dozen donuts is less than $4.

B) sell an additional dozen donuts as long as the total cost of producing an additional dozen donuts is less than $4.

C) only sell more donuts if his total revenue is greater than his total cost.

D) sell an additional dozen donuts so long as the fixed cost of production is greater than $4.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

35

A market becomes more competitive as there are ______ buyers and ______ sellers.

A) fewer; fewer

B) fewer; more

C) more; fewer

D) more; more

A) fewer; fewer

B) fewer; more

C) more; fewer

D) more; more

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

36

Which of the following best describes a competitive industry?

A) Its firms sell similar products and have little control over their prices; there are many buyers and sellers and each is relatively small compared with the overall market.

B) Its firms sell similar products and have direct control over their prices; there are many buyers and sellers and each is relatively small compared with the overall market.

C) Its firms have little control over the price of their product; the demand curve for each firm's product is downward sloping; there are many firms.

D) Its firms sell differentiated products and there are few potential sellers. They have little control over the price of their product; there are many relatively small buyers.

A) Its firms sell similar products and have little control over their prices; there are many buyers and sellers and each is relatively small compared with the overall market.

B) Its firms sell similar products and have direct control over their prices; there are many buyers and sellers and each is relatively small compared with the overall market.

C) Its firms have little control over the price of their product; the demand curve for each firm's product is downward sloping; there are many firms.

D) Its firms sell differentiated products and there are few potential sellers. They have little control over the price of their product; there are many relatively small buyers.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

37

In a perfectly competitive market, firm level demand is:

A) flat.

B) vertical.

C) positively sloped.

D) negatively sloped.

A) flat.

B) vertical.

C) positively sloped.

D) negatively sloped.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following statements is TRUE? Economists normally assume that the goal of the firm is to:

I. sell as much of their product as possible.

II. set the price of their product as high as possible.

III. maximize profit.

A) I and II only

B) II and III only

C) I and III only

D) III only

I. sell as much of their product as possible.

II. set the price of their product as high as possible.

III. maximize profit.

A) I and II only

B) II and III only

C) I and III only

D) III only

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

39

The total amount of money that a firm receives from sales of its output is called:

A) gross profit.

B) net profit.

C) total revenue.

D) net revenue.

A) gross profit.

B) net profit.

C) total revenue.

D) net revenue.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

40

More potential sellers ______ the elasticity of ______ firm-level demand.

A) increase; short-run

B) decrease; short-run

C) increase; long-run

D) decrease; long-run

A) increase; short-run

B) decrease; short-run

C) increase; long-run

D) decrease; long-run

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

41

Total profit for a given quantity of output can be calculated as:

A) Total Revenue - Total Costs.

B) Marginal Revenue - Marginal Cost.

C) Total Revenue - Marginal Revenue.

D) Marginal Profit + Marginal Revenue.

A) Total Revenue - Total Costs.

B) Marginal Revenue - Marginal Cost.

C) Total Revenue - Marginal Revenue.

D) Marginal Profit + Marginal Revenue.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

42

For a small firm in an extremely competitive industry, marginal revenue is always equal to price because:

A) the firm has no ability to influence the market price.

B) each firm has large economies of scale.

C) each firm has large fixed costs.

D) if consumers increase their demand for the product, producer surplus falls.

A) the firm has no ability to influence the market price.

B) each firm has large economies of scale.

C) each firm has large fixed costs.

D) if consumers increase their demand for the product, producer surplus falls.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

43

Price times quantity minus total cost equals:

A) total revenue.

B) fixed costs.

C) marginal revenue.

D) profit.

A) total revenue.

B) fixed costs.

C) marginal revenue.

D) profit.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

44

Total cost incorporates:

A) implicit and explicit cost.

B) implicit cost only.

C) explicit cost only.

D) neither explicit nor implicit cost.

A) implicit and explicit cost.

B) implicit cost only.

C) explicit cost only.

D) neither explicit nor implicit cost.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

45

As the price of a good fluctuates, a profit-maximizing firm will expand or contract production along its:

A) average cost curve.

B) average product curve.

C) marginal cost curve.

D) marginal product curve.

A) average cost curve.

B) average product curve.

C) marginal cost curve.

D) marginal product curve.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

46

Which of the following statements is TRUE?

A) Accounting profit is usually smaller than economic profit.

B) Unlike implicit costs, explicit costs require monetary outlays.

C) Knowledge about explicit costs is more useful for making business decisions than knowledge about implicit costs.

D) Implicit costs equal explicit costs for for-profit firms.

A) Accounting profit is usually smaller than economic profit.

B) Unlike implicit costs, explicit costs require monetary outlays.

C) Knowledge about explicit costs is more useful for making business decisions than knowledge about implicit costs.

D) Implicit costs equal explicit costs for for-profit firms.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

47

Total cost equals fixed cost ______ variable cost.

A) times

B) minus

C) plus

D) divided by

A) times

B) minus

C) plus

D) divided by

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

48

In their calculation of profit, accountants typically do not take into account:

A) variable costs.

B) fixed costs.

C) opportunity costs.

D) explicit costs.

A) variable costs.

B) fixed costs.

C) opportunity costs.

D) explicit costs.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

49

Damien produces 400 gallons of milk a day in a very competitive industry. The market price for a gallon of milk is $2. Damien's marginal revenue per gallon of milk is:

A) $200.

B) $800.

C) $2.

D) $0.

A) $200.

B) $800.

C) $2.

D) $0.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

50

When deciding on the profit maximizing level of output, firms compare ______ of an additional unit of output to the ______.

A) marginal revenue; total cost of production

B) average revenue; total cost of production

C) marginal revenue; marginal cost of producing the additional unit of output

D) average revenue; average cost of producing the additional unit of output

A) marginal revenue; total cost of production

B) average revenue; total cost of production

C) marginal revenue; marginal cost of producing the additional unit of output

D) average revenue; average cost of producing the additional unit of output

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

51

Marcie quit her job as a preschool teacher, which paid an annual salary of $28,000, and became a street food vendor. She used $8,000 out of her savings account that paid a 4% annual interest rate to buy a street cart to sell food. In her first year of operations, she spent $10,000 on food and supplies (napkins, cups, plates, etc.) and earned total revenue of $45,000. Marcie's accounting profit is ______ and economic profit is ______.

A) $28,000; $20,000

B) $35,000; -$1,000

C) $27,000; $17,000

D) $35,000; $6,680

A) $28,000; $20,000

B) $35,000; -$1,000

C) $27,000; $17,000

D) $35,000; $6,680

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

52

Economic profit differs from accounting profits because of its inclusion of:

A) explicit costs.

B) incidental costs.

C) potential costs.

D) implicit costs.

A) explicit costs.

B) incidental costs.

C) potential costs.

D) implicit costs.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

53

To maximize profit, firms should keep producing as long as marginal revenue is:

A) greater than marginal cost.

B) equal to marginal cost.

C) less than marginal cost.

D) greater than total cost.

A) greater than marginal cost.

B) equal to marginal cost.

C) less than marginal cost.

D) greater than total cost.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following is an example of an implicit cost of production?

A) cost of raw materials

B) cost of labor

C) opportunity cost

D) fixed costs

A) cost of raw materials

B) cost of labor

C) opportunity cost

D) fixed costs

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

55

Figure: Elastic Demand If the total cost of producing 11 units of output in this figure is $16, the firm's economic profit at 11 units of output is:

A) $8.

B) -$8.

C) $72.

D) $104.

If the total cost of producing 11 units of output in this figure is $16, the firm's economic profit at 11 units of output is:A) $8.

B) -$8.

C) $72.

D) $104.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

56

When opportunity cost is positive, economic profit ______ accounting profit.

A) is greater than

B) is less than

C) equals

D) eliminates

A) is greater than

B) is less than

C) equals

D) eliminates

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

57

Tom opens a sandwich shop; which of the following is NOT an economic cost (total cost) of running his business?

A) his forgone earnings as a book editor, his next best opportunity for employment

B) the interest income he could have earned on the money he invested in his business from savings

C) the wages that he pays his workers

D) the expenses for his own lunch every day

A) his forgone earnings as a book editor, his next best opportunity for employment

B) the interest income he could have earned on the money he invested in his business from savings

C) the wages that he pays his workers

D) the expenses for his own lunch every day

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

58

Stock market investors should ultimately focus on a company's:

A) economic profit.

B) accounting profit.

C) total revenue.

D) total costs.

A) economic profit.

B) accounting profit.

C) total revenue.

D) total costs.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

59

In late November of 2010, a share of Microsoft sold for about $25 and a share of McDonald's sold for about $80. In late June of 2011, Microsoft shares were about $26 and McDonald's shares were about $85. If these two companies were the only choices available, what is your economic profit if you invest $400 in Microsoft?

A) -$25

B) -$9

C) $9

D) $16

A) -$25

B) -$9

C) $9

D) $16

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

60

To maximize profit, a firm in a competitive market increases output until:

A) P = TC.

B) P = AR.

C) P = MC.

D) P = AC.

A) P = TC.

B) P = AR.

C) P = MC.

D) P = AC.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

61

Julius builds dining chairs that he sells for $200 a chair. His fixed costs are $1,000 (for workshop equipment). Each chair costs him $50 in materials to produce plus an extra $25 for each previous chair made that day which reflects Julius' increasing exhaustion. (Thus, the first chair cost $50, the second costs $75, the third cost $100, etc.) Assume time requirements in producing a chair are not a factor. How many chairs should Julius produce each day?

A) 2

B) 5

C) 7

D) 12

A) 2

B) 5

C) 7

D) 12

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

62

To maximize profits, firms produce the level of output that:

A) equates total revenue and total cost.

B) equates marginal revenue with marginal cost.

C) minimizes costs.

D) maximizes revenues.

A) equates total revenue and total cost.

B) equates marginal revenue with marginal cost.

C) minimizes costs.

D) maximizes revenues.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

63

Total revenue is equal to:

A) price minus quantity.

B) price plus quantity.

C) price times quantity.

D) price divided by quantity.

A) price minus quantity.

B) price plus quantity.

C) price times quantity.

D) price divided by quantity.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

64

Firm profit is defined as:

A) total revenue plus total cost.

B) total revenue minus total cost.

C) marginal revenue plus marginal cost.

D) marginal revenue minus marginal cost.

A) total revenue plus total cost.

B) total revenue minus total cost.

C) marginal revenue plus marginal cost.

D) marginal revenue minus marginal cost.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

65

Use the following to answer questions:

Figure: Maximizing Profit

The change in total cost from producing the eighth unit of output is ______, and the change in total revenue from producing the seventh unit of output is ______.

A) $5; $14

B) $10; $70

C) $7; $6.50

D) $3.50; $6.50

Figure: Maximizing Profit

The change in total cost from producing the eighth unit of output is ______, and the change in total revenue from producing the seventh unit of output is ______.

A) $5; $14

B) $10; $70

C) $7; $6.50

D) $3.50; $6.50

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

66

Which of the following is TRUE?

A) Price times quantity equals profit.

B) Profit equals marginal revenue minus marginal cost.

C) Profit equals total revenue minus average cost.

D) Profit equals (price minus average cost) times quantity.

A) Price times quantity equals profit.

B) Profit equals marginal revenue minus marginal cost.

C) Profit equals total revenue minus average cost.

D) Profit equals (price minus average cost) times quantity.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

67

When the level of production is relatively low, the average cost per unit of output would ________ if output increased.

A) increase

B) decrease

C) either increase or decrease depending on marginal cost

D) remain constant

A) increase

B) decrease

C) either increase or decrease depending on marginal cost

D) remain constant

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

68

A firm maximizes profits when:

A) total revenue equals total cost.

B) average revenue equals average cost.

C) marginal revenue equals marginal cost.

D) fixed revenue equals fixed cost.

A) total revenue equals total cost.

B) average revenue equals average cost.

C) marginal revenue equals marginal cost.

D) fixed revenue equals fixed cost.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

69

Why can't marginal cost decrease forever?

A) At some point, firms encounter physical limits of production.

B) Demand is not infinite.

C) Marginal cost can't increase forever either, and there must be symmetry.

D) Marginal cost is always constant.

A) At some point, firms encounter physical limits of production.

B) Demand is not infinite.

C) Marginal cost can't increase forever either, and there must be symmetry.

D) Marginal cost is always constant.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

70

Which of the following statements is FALSE?

A) AC = TC/Q

B) A firm that produces 100 units at a total cost of $500 has an average cost of $5 per unit.

C) Firms will earn positive profits if price exceeds average cost.

D) When marginal cost is below average cost, average cost is rising.

A) AC = TC/Q

B) A firm that produces 100 units at a total cost of $500 has an average cost of $5 per unit.

C) Firms will earn positive profits if price exceeds average cost.

D) When marginal cost is below average cost, average cost is rising.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

71

Programs such as Steam distribute more and more video games. Purchasers buy the game and download it immediately to their computer. If the entire system is automated, estimate the marginal cost of producing and selling video games this way (ignore electricity costs).

A) zero

B) the price of the game

C) proportional to the cost to make the game

D) None of the answers is correct.

A) zero

B) the price of the game

C) proportional to the cost to make the game

D) None of the answers is correct.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

72

Price equals marginal revenue for a competitive firm because:

A) total revenue is constant.

B) marginal cost is constant.

C) the production of marginal units affects the value of other units.

D) the price does not change when the firm changes output.

A) total revenue is constant.

B) marginal cost is constant.

C) the production of marginal units affects the value of other units.

D) the price does not change when the firm changes output.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

73

Which of the following is an example of a fixed cost?

A) The cost of fabric for making backpacks

B) The profits gained from opening a bakery instead of an ice cream store

C) Research and development costs for a new medicine

D) Water used to make lemonade at a lemonade stand

A) The cost of fabric for making backpacks

B) The profits gained from opening a bakery instead of an ice cream store

C) Research and development costs for a new medicine

D) Water used to make lemonade at a lemonade stand

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

74

The change in total revenue from selling an additional unit is called:

A) average revenue.

B) marginal revenue.

C) marginal cost.

D) variable cost.

A) average revenue.

B) marginal revenue.

C) marginal cost.

D) variable cost.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

75

Profit can be shown graphically by depicting a firm's costs and revenues, and it is determined mathematically by calculating the:

A) distance from price to average cost.

B) area of the box that is price times quantity.

C) area of the box that is (price minus average cost) times the quantity.

D) area of the box that is average cost times quantity.

A) distance from price to average cost.

B) area of the box that is price times quantity.

C) area of the box that is (price minus average cost) times the quantity.

D) area of the box that is average cost times quantity.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

76

If marginal revenue is less than marginal cost, a firm should:

A) hold output steady.

B) increase output.

C) decrease output.

D) lower its price.

A) hold output steady.

B) increase output.

C) decrease output.

D) lower its price.

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

77

Perfectly competitive firms produce at the quantity where marginal revenue ______ marginal cost.

A) is greater than

B) equals

C) is less than

D) is equal to zero rather than

A) is greater than

B) equals

C) is less than

D) is equal to zero rather than

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

78

Which of the following statements is TRUE?

I. If a competitive firm sells its product at a price of $80, the firm should increase production from 100 to 101 units if the total cost rises from $2,000 to $2,066.

II. If the marginal cost of the tenth unit is $14 and the marginal revenue is $10, the firm should produce the tenth unit to increase profits by $4.

III. For competitive firms, profits are maximized at MR = MC or P = MC, since P = MR.

A) I and III only

B) II only

C) I, II, and III

D) III only

I. If a competitive firm sells its product at a price of $80, the firm should increase production from 100 to 101 units if the total cost rises from $2,000 to $2,066.

II. If the marginal cost of the tenth unit is $14 and the marginal revenue is $10, the firm should produce the tenth unit to increase profits by $4.

III. For competitive firms, profits are maximized at MR = MC or P = MC, since P = MR.

A) I and III only

B) II only

C) I, II, and III

D) III only

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

79

Use the following to answer questions:

Figure: Maximizing Profit

(Figure: Maximizing Profit) What is the firm's profit-maximizing level of output?

A) 4

B) 7

C) 9

D) 12

Figure: Maximizing Profit

(Figure: Maximizing Profit) What is the firm's profit-maximizing level of output?

A) 4

B) 7

C) 9

D) 12

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

80

Table: Profit Maximization 2

The firm in this table can earn a maximum profit of ______, which occurs at an output of ______ barrels per day.

A) $380; 4

B) $80; 3

C) $100; 0

D) $200; 2

The firm in this table can earn a maximum profit of ______, which occurs at an output of ______ barrels per day.

A) $380; 4

B) $80; 3

C) $100; 0

D) $200; 2

Unlock Deck

Unlock for access to all 217 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 217 flashcards in this deck.