Deck 12: Competition and the Invisible Hand

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following to answer questions:

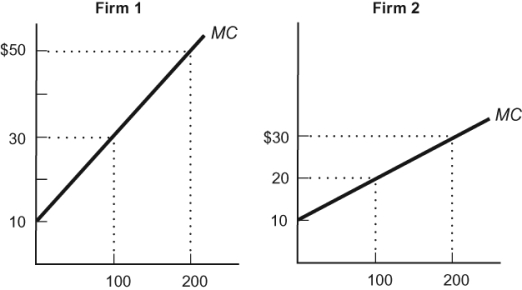

Figure: Marginal Costs 1

(Figure: Marginal Costs 1) This figure shows the production costs of two firms that produce steel beams. If these two firms represent total production in the industry, how should they allocate the production of 100 beams to minimize costs?

A) Firm 2 should produce all of the output.

B) Firm 1 should produce all of the output.

C) Firm 1 should produce 50 beams, and Firm 2 should produce 50 beams.

D) Both Firm 1 and Firm 2 should produce some output, but Firm 2 should produce more than Firm 1.

Figure: Marginal Costs 1

(Figure: Marginal Costs 1) This figure shows the production costs of two firms that produce steel beams. If these two firms represent total production in the industry, how should they allocate the production of 100 beams to minimize costs?

A) Firm 2 should produce all of the output.

B) Firm 1 should produce all of the output.

C) Firm 1 should produce 50 beams, and Firm 2 should produce 50 beams.

D) Both Firm 1 and Firm 2 should produce some output, but Firm 2 should produce more than Firm 1.

Question

Question

Question

Question

Question

Question

Question

Use the following to answer questions:

Figure: Marginal Costs 1

(Figure: Marginal Costs 1) This figure shows the production costs of two firms that produce steel beams. If these two firms represent total production in the industry, how should they allocate the production of 300 beams to minimize costs?

A) Firm 2 should produce all 300 beams.

B) Firm 1 should produce all 300 beams.

C) Firm 1 should produce 150 beams, and Firm 2 should produce 150 beams.

D) Firm 1 should produce 100 beams, and Firm 2 should produce 200 beams.

Figure: Marginal Costs 1

(Figure: Marginal Costs 1) This figure shows the production costs of two firms that produce steel beams. If these two firms represent total production in the industry, how should they allocate the production of 300 beams to minimize costs?

A) Firm 2 should produce all 300 beams.

B) Firm 1 should produce all 300 beams.

C) Firm 1 should produce 150 beams, and Firm 2 should produce 150 beams.

D) Firm 1 should produce 100 beams, and Firm 2 should produce 200 beams.

Question

Use the following to answer questions:

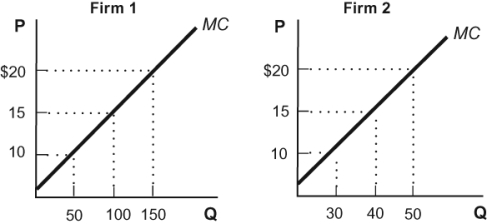

Figure: Marginal Costs 1

Figure: Marginal Costs 2 This figure shows the production costs of two firms that produce bird feeders. If these two firms represent total production in the industry, how should they allocate the production of 200 bird feeders to minimize costs?

This figure shows the production costs of two firms that produce bird feeders. If these two firms represent total production in the industry, how should they allocate the production of 200 bird feeders to minimize costs?

A) Firm 2 should produce all 200 bird feeders.

B) Firm 1 should produce all 200 bird feeders.

C) Firm 1 should produce 150 bird feeders, and Firm 2 should produce 50 bird feeders.

D) Firm 1 should produce 100 bird feeders, and Firm 2 should produce 100 bird feeders.

Figure: Marginal Costs 1

Figure: Marginal Costs 2

This figure shows the production costs of two firms that produce bird feeders. If these two firms represent total production in the industry, how should they allocate the production of 200 bird feeders to minimize costs?A) Firm 2 should produce all 200 bird feeders.

B) Firm 1 should produce all 200 bird feeders.

C) Firm 1 should produce 150 bird feeders, and Firm 2 should produce 50 bird feeders.

D) Firm 1 should produce 100 bird feeders, and Firm 2 should produce 100 bird feeders.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following to answer questions:

Figure: Light Bulbs

(Figure: Light Bulbs) What price of light bulbs would induce the firms in this diagram to minimize total production costs while maintaining the same total output?

A) $0.40

B) $0.80

C) $1.00

D) $1.00 for Firm 1, $0.70 for Firm 2

Figure: Light Bulbs

(Figure: Light Bulbs) What price of light bulbs would induce the firms in this diagram to minimize total production costs while maintaining the same total output?

A) $0.40

B) $0.80

C) $1.00

D) $1.00 for Firm 1, $0.70 for Firm 2

Question

Question

Question

Question

Question

Question

Question

Use the following to answer questions:

Figure: Light Bulbs

(Figure: Light Bulbs) In this diagram, Firm 1 (MC1) and Firm 2 (MC2) are each making 100 million light bulbs. How many light bulbs should each firm make to minimize total production costs while maintaining the same total output?

A) Firm 1: 40 million; Firm 2: 40 million

B) Firm 1: 20 million; Firm 2: 30 million

C) Firm 1: 80 million; Firm 2: 120 million

D) Firm 1: 120 million; Firm 2: 80 million

Figure: Light Bulbs

(Figure: Light Bulbs) In this diagram, Firm 1 (MC1) and Firm 2 (MC2) are each making 100 million light bulbs. How many light bulbs should each firm make to minimize total production costs while maintaining the same total output?

A) Firm 1: 40 million; Firm 2: 40 million

B) Firm 1: 20 million; Firm 2: 30 million

C) Firm 1: 80 million; Firm 2: 120 million

D) Firm 1: 120 million; Firm 2: 80 million

Question

Question

Question

Question

Question

Question

Question

Question

Question

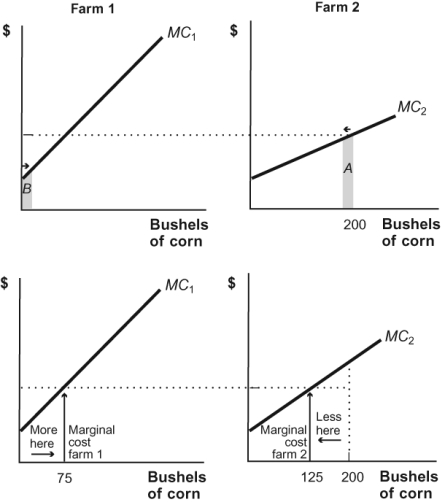

Figure: Two Farms  Refer to the figure. If a farmer owns two farms, Farm 1 and Farm 2, and is under contract to produce 400 bushels of corn for a food processor, should the farmer produce 200 bushels of corn from each farm as shown in this diagram?

Refer to the figure. If a farmer owns two farms, Farm 1 and Farm 2, and is under contract to produce 400 bushels of corn for a food processor, should the farmer produce 200 bushels of corn from each farm as shown in this diagram?

A) Yes, splitting production evenly between farms, or factories, is the method to minimize the costs of production.

B) No, he should produce all 400 bushels from Farm 2, the low-cost farm.

C) No, he should produce more corn from Farm 1 and less corn from Farm 2 so that the marginal cost of the last bushel of corn is equal across both farms.

D) No, he should produce less corn from Farm 1 and more corn from Farm 2 so that the marginal cost of the last bushel of corn is equal across both farms.

Refer to the figure. If a farmer owns two farms, Farm 1 and Farm 2, and is under contract to produce 400 bushels of corn for a food processor, should the farmer produce 200 bushels of corn from each farm as shown in this diagram?A) Yes, splitting production evenly between farms, or factories, is the method to minimize the costs of production.

B) No, he should produce all 400 bushels from Farm 2, the low-cost farm.

C) No, he should produce more corn from Farm 1 and less corn from Farm 2 so that the marginal cost of the last bushel of corn is equal across both farms.

D) No, he should produce less corn from Farm 1 and more corn from Farm 2 so that the marginal cost of the last bushel of corn is equal across both farms.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

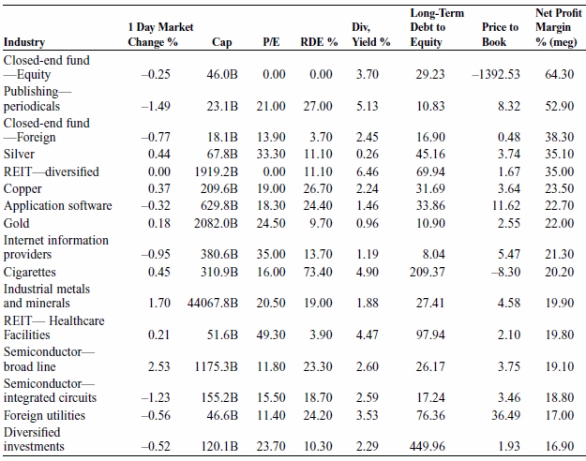

Table: Profit Margins  This table shows that silver, copper, and gold were some of the most profitable industries in July 2011. (For each dollar of sales, profit for these industries is 35.1, 23.5, and 22.0 cents, respectively.) According to the elimination principle, what do you expect to happen to these profit margins in the long run?

This table shows that silver, copper, and gold were some of the most profitable industries in July 2011. (For each dollar of sales, profit for these industries is 35.1, 23.5, and 22.0 cents, respectively.) According to the elimination principle, what do you expect to happen to these profit margins in the long run?

A) Profit margins will increase because of increased entry.

B) Profit margins will increase because of increased exit.

C) Profit margins will decrease because of increased entry.

D) Profit margins will decrease because of increased exit.

This table shows that silver, copper, and gold were some of the most profitable industries in July 2011. (For each dollar of sales, profit for these industries is 35.1, 23.5, and 22.0 cents, respectively.) According to the elimination principle, what do you expect to happen to these profit margins in the long run?A) Profit margins will increase because of increased entry.

B) Profit margins will increase because of increased exit.

C) Profit margins will decrease because of increased entry.

D) Profit margins will decrease because of increased exit.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/144

Play

Full screen (f)

Deck 12: Competition and the Invisible Hand

1

Competitive firms want to produce the quantity such that:

A) P = MC.

B) P > MC.

C) P > AC.

D) P < AC.

A) P = MC.

B) P > MC.

C) P > AC.

D) P < AC.

P = MC.

2

Suppose that you own two farms on which to grow corn. In order to lower the cost of production, you determine to increase production on Farm 1 and reduce it on Farm 2. This implies that the marginal cost of production on Farm 1 is:

A) greater than the marginal cost of production on Farm 2.

B) less than the marginal cost of production on Farm 2.

C) equal to the marginal cost of production on Farm 2.

D) The difference of the marginal costs between the two farms cannot be determined.

A) greater than the marginal cost of production on Farm 2.

B) less than the marginal cost of production on Farm 2.

C) equal to the marginal cost of production on Farm 2.

D) The difference of the marginal costs between the two farms cannot be determined.

less than the marginal cost of production on Farm 2.

3

The pursuit of profits in a competitive market:

A) minimizes total industry costs.

B) minimizes total value of production.

C) leads to higher prices.

D) maximizes producer surplus at the expense of consumer surplus.

A) minimizes total industry costs.

B) minimizes total value of production.

C) leads to higher prices.

D) maximizes producer surplus at the expense of consumer surplus.

minimizes total industry costs.

4

A competitive firm maximizes profit when marginal cost:

A) equals the price.

B) is less than the price.

C) is greater than the price.

D) is minimized.

A) equals the price.

B) is less than the price.

C) is greater than the price.

D) is minimized.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

5

In the long run, competitive firms want to exit industries in which:

A) P = MC.

B) P > MC.

C) P > AC.

D) P < AC.

A) P = MC.

B) P > MC.

C) P > AC.

D) P < AC.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

6

Suppose that Sandy owns a farm in North Carolina and Pat owns a farm in Iowa, and Sandy's farm is generally more productive than Pat's. If both Sandy and Pat sell their corn in the same market, Sandy should produce the output at the marginal cost that is:

A) less than the marginal cost of Pat's production.

B) equal to the marginal cost of Pat's production.

C) greater than the marginal cost of Pat's production.

D) equal to total revenue in the market.

A) less than the marginal cost of Pat's production.

B) equal to the marginal cost of Pat's production.

C) greater than the marginal cost of Pat's production.

D) equal to total revenue in the market.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

7

Outcomes that people neither intend nor design:

A) are always undesirable.

B) can be desirable with the right institutions.

C) are always desirable.

D) are impossible.

A) are always undesirable.

B) can be desirable with the right institutions.

C) are always desirable.

D) are impossible.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

8

A free market can naturally allocate production across firms in an industry to minimize total costs due to:

A) market power.

B) regulation.

C) the invisible hand.

D) externality.

A) market power.

B) regulation.

C) the invisible hand.

D) externality.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

9

Competitive firms want to enter industries in which:

A) P = MC.

B) P < AC.

C) P > AC.

D) P < MC.

A) P = MC.

B) P < AC.

C) P > AC.

D) P < MC.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

10

Use the following to answer questions:

Figure: Marginal Costs 1

(Figure: Marginal Costs 1) This figure shows the production costs of two firms that produce steel beams. If these two firms represent total production in the industry, how should they allocate the production of 100 beams to minimize costs?

A) Firm 2 should produce all of the output.

B) Firm 1 should produce all of the output.

C) Firm 1 should produce 50 beams, and Firm 2 should produce 50 beams.

D) Both Firm 1 and Firm 2 should produce some output, but Firm 2 should produce more than Firm 1.

Figure: Marginal Costs 1

(Figure: Marginal Costs 1) This figure shows the production costs of two firms that produce steel beams. If these two firms represent total production in the industry, how should they allocate the production of 100 beams to minimize costs?

A) Firm 2 should produce all of the output.

B) Firm 1 should produce all of the output.

C) Firm 1 should produce 50 beams, and Firm 2 should produce 50 beams.

D) Both Firm 1 and Firm 2 should produce some output, but Firm 2 should produce more than Firm 1.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following statements is TRUE?

I. A free market minimizes the total costs of producing output.

II. In a free market, P = MC1 = MC2 = . . . MCN.

III. Every firm faces the same price in a competitive market.

A) I and II only

B) III only

C) I and III only

D) I, II, and III

I. A free market minimizes the total costs of producing output.

II. In a free market, P = MC1 = MC2 = . . . MCN.

III. Every firm faces the same price in a competitive market.

A) I and II only

B) III only

C) I and III only

D) I, II, and III

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

12

Profit maximization occurs when:

A) TR > TC.

B) MR = MC.

C) MC = AC.

D) P = AC.

A) TR > TC.

B) MR = MC.

C) MC = AC.

D) P = AC.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

13

If the marginal cost of production at Firm 1 is less than the marginal cost of production at Firm 2 but the overall costs of production are lower on average at Firm 2, then:

A) Firm 2 should produce all of the output.

B) Firm 1 should produce all of the output.

C) Firm 1 should produce output up to the point that its marginal costs of production are equal to the marginal costs of Firm 2.

D) Firm 2 should produce additional output up to the point that its average costs are less than its marginal costs.

A) Firm 2 should produce all of the output.

B) Firm 1 should produce all of the output.

C) Firm 1 should produce output up to the point that its marginal costs of production are equal to the marginal costs of Firm 2.

D) Firm 2 should produce additional output up to the point that its average costs are less than its marginal costs.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

14

Suppose that you own two farms on which to grow corn. Farm 2 has a lower marginal cost of producing corn than Farm 1. To lower total cost of production, you should produce:

A) all on Farm 1.

B) all on Farm 2.

C) some on Farm 1 and some on Farm 2.

D) neither on Farm 1 nor on Farm 2.

A) all on Farm 1.

B) all on Farm 2.

C) some on Farm 1 and some on Farm 2.

D) neither on Farm 1 nor on Farm 2.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following statements is TRUE regarding profit maximization in competitive markets?

I. When all firms pursue profits, none of them achieve profits.

II. When all firms pursue profits, only the most innovative will achieve profits.

III. Production is divided in such a way that total costs of production are minimized.

A) I only

B) II only

C) I and III only

D) II and III only

I. When all firms pursue profits, none of them achieve profits.

II. When all firms pursue profits, only the most innovative will achieve profits.

III. Production is divided in such a way that total costs of production are minimized.

A) I only

B) II only

C) I and III only

D) II and III only

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

16

Since a competitive firm sets MR = P to determine all quantities in the short run, we can conclude that:

A) each firm in the industry faces very large fixed costs.

B) the demand curve faced by each individual competitive firm is perfectly elastic.

C) the demand curve faced by each individual competitive firm is downward sloping.

D) the industry demand curve is perfectly elastic.

A) each firm in the industry faces very large fixed costs.

B) the demand curve faced by each individual competitive firm is perfectly elastic.

C) the demand curve faced by each individual competitive firm is downward sloping.

D) the industry demand curve is perfectly elastic.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

17

Use the following to answer questions:

Figure: Marginal Costs 1

(Figure: Marginal Costs 1) This figure shows the production costs of two firms that produce steel beams. If these two firms represent total production in the industry, how should they allocate the production of 300 beams to minimize costs?

A) Firm 2 should produce all 300 beams.

B) Firm 1 should produce all 300 beams.

C) Firm 1 should produce 150 beams, and Firm 2 should produce 150 beams.

D) Firm 1 should produce 100 beams, and Firm 2 should produce 200 beams.

Figure: Marginal Costs 1

(Figure: Marginal Costs 1) This figure shows the production costs of two firms that produce steel beams. If these two firms represent total production in the industry, how should they allocate the production of 300 beams to minimize costs?

A) Firm 2 should produce all 300 beams.

B) Firm 1 should produce all 300 beams.

C) Firm 1 should produce 150 beams, and Firm 2 should produce 150 beams.

D) Firm 1 should produce 100 beams, and Firm 2 should produce 200 beams.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

18

Use the following to answer questions:

Figure: Marginal Costs 1

Figure: Marginal Costs 2 This figure shows the production costs of two firms that produce bird feeders. If these two firms represent total production in the industry, how should they allocate the production of 200 bird feeders to minimize costs?

A) Firm 2 should produce all 200 bird feeders.

B) Firm 1 should produce all 200 bird feeders.

C) Firm 1 should produce 150 bird feeders, and Firm 2 should produce 50 bird feeders.

D) Firm 1 should produce 100 bird feeders, and Firm 2 should produce 100 bird feeders.

Figure: Marginal Costs 1

Figure: Marginal Costs 2

This figure shows the production costs of two firms that produce bird feeders. If these two firms represent total production in the industry, how should they allocate the production of 200 bird feeders to minimize costs?A) Firm 2 should produce all 200 bird feeders.

B) Firm 1 should produce all 200 bird feeders.

C) Firm 1 should produce 150 bird feeders, and Firm 2 should produce 50 bird feeders.

D) Firm 1 should produce 100 bird feeders, and Firm 2 should produce 100 bird feeders.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

19

In a competitive market with four firms (indicated as Firm 1, Firm 2, Firm 3, and Firm 4), which of the following is the condition that enables all sellers to maximize profit?

A) P = ATC for all firms

B) Profit = Total Revenue - Total Cost for all firms

C) P = MC1 = MC2 = MC3 = MC4

D) MC is minimized in all firms.

A) P = ATC for all firms

B) Profit = Total Revenue - Total Cost for all firms

C) P = MC1 = MC2 = MC3 = MC4

D) MC is minimized in all firms.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

20

For a competitive firm, which of the following conditions describes the profit maximization condition?

I. P = MC

II. MR = MC

III. TR = TC

A) II only

B) I and II only

C) II and III only

D) I, II, and III

I. P = MC

II. MR = MC

III. TR = TC

A) II only

B) I and II only

C) II and III only

D) I, II, and III

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

21

Adam Smith said that each individual is "led by ______ to promote an end which was no part of his intention."

A) an invincible hand

B) an intrinsic hand

C) a visible hand

D) an invisible hand

A) an invincible hand

B) an intrinsic hand

C) a visible hand

D) an invisible hand

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

22

A central planner can only allocate production across firms in a way that minimizes total costs if:

A) the market is a perfectly competitive market.

B) the central planner has perfect information on the firms' costs.

C) free markets fail to achieve this kind of efficiency.

D) the costs of production are equal across all firms.

A) the market is a perfectly competitive market.

B) the central planner has perfect information on the firms' costs.

C) free markets fail to achieve this kind of efficiency.

D) the costs of production are equal across all firms.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

23

A small island nation produces only boxes of macaroni and cheese, most of which it sells in the export market. The world price per box is $10, regardless of the quantity exported. The nation has three macaroni and cheese factories, each of which varies in efficiency, but it's impossible for the government to determine each factory's marginal cost. To profit the most as a country, what should this nation's government do?

A) Order each factory to produce the same quantity.

B) Shut down the two most inefficient factories and produce at the most efficient one until marginal cost is $10.

C) Let the producers compete in the market to determine the optimal quantity and allocation of macaroni and cheese production.

D) Impose a tax on exports and see which factory survives the longest.

A) Order each factory to produce the same quantity.

B) Shut down the two most inefficient factories and produce at the most efficient one until marginal cost is $10.

C) Let the producers compete in the market to determine the optimal quantity and allocation of macaroni and cheese production.

D) Impose a tax on exports and see which factory survives the longest.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

24

Invisible Hand Property 1 says that without any single person in charge, free markets will result in equal ______ and price will be set to it.

A) average costs

B) marginal costs

C) fixed costs

D) demand curves

A) average costs

B) marginal costs

C) fixed costs

D) demand curves

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

25

A student trying to maximize her semester GPA already studies as many hours as possible but can perhaps use that time more efficiently. A marginal hour spent studying economics will raise her GPA by 0.05. A marginal hour spent studying literature will raise her GPA by 0.02. Should she reallocate her time?

A) She should not reallocate her study time at all.

B) With the given information, it is impossible to determine whether she should reallocate her time.

C) She should spend more time studying literature and less time studying economics.

D) She should spend more time studying economics and less time studying literature.

A) She should not reallocate her study time at all.

B) With the given information, it is impossible to determine whether she should reallocate her time.

C) She should spend more time studying literature and less time studying economics.

D) She should spend more time studying economics and less time studying literature.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

26

Consider two farms. Farm 1 produces unlimited bushels for a cost of $5 each. Farm 2 produces unlimited bushels for a cost of $7 each. How should production be allocated between these two farms?

A) Produce 7 bushels on Farm 1 for every 5 bushels on Farm 2.

B) Produce 5 bushels on Farm 1 for every 7 bushels on Farm 2.

C) Produce all bushels on Farm 1.

D) Produce all bushels on Farm 2.

A) Produce 7 bushels on Farm 1 for every 5 bushels on Farm 2.

B) Produce 5 bushels on Farm 1 for every 7 bushels on Farm 2.

C) Produce all bushels on Farm 1.

D) Produce all bushels on Farm 2.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

27

The following are marginal cost curves for selling chicken in a Mom & Pop (MCM) store and in a Big-Box retailer (MCB).

MCM = 2 + 2QM

MCB = 4 + QB

If there are 6 total chickens being sold, how many chickens does each firm sell?

A) Mom & Pop: 0; Big-Box: 6

B) Mom & Pop: 1; Big-Box: 5

C) Mom & Pop: 2; Big-Box: 4

D) Mom & Pop: 3; Big-Box: 3

MCM = 2 + 2QM

MCB = 4 + QB

If there are 6 total chickens being sold, how many chickens does each firm sell?

A) Mom & Pop: 0; Big-Box: 6

B) Mom & Pop: 1; Big-Box: 5

C) Mom & Pop: 2; Big-Box: 4

D) Mom & Pop: 3; Big-Box: 3

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

28

If a competitive market has three firms with marginal costs of MC1 = Q1, MC2 = 0.50Q2, and MC3 = 2Q3 and faces a market price of $10, the total quantity supplied by all three firms is:

A) 15.

B) 20.

C) 25.

D) 35.

A) 15.

B) 20.

C) 25.

D) 35.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

29

If every firm knows its marginal cost but a central planner cannot know every firm's marginal cost, then:

A) central planners will outperform competitive markets.

B) competitive markets will outperform central planners.

C) central planners and competitive markets will perform equally well.

D) it is impossible to say whether central planners or competitive markets will perform better.

A) central planners will outperform competitive markets.

B) competitive markets will outperform central planners.

C) central planners and competitive markets will perform equally well.

D) it is impossible to say whether central planners or competitive markets will perform better.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

30

In a competitive industry:

A) all firms produce at the same marginal cost.

B) some firms have higher marginal cost than others.

C) some firms face different prices than others.

D) all firms have the same marginal cost curve.

A) all firms produce at the same marginal cost.

B) some firms have higher marginal cost than others.

C) some firms face different prices than others.

D) all firms have the same marginal cost curve.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

31

Total costs cannot be minimized if firms:

A) face different prices.

B) have different marginal cost curves.

C) face the same prices.

D) have the same marginal cost curves.

A) face different prices.

B) have different marginal cost curves.

C) face the same prices.

D) have the same marginal cost curves.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

32

What is the Invisible Hand Property 1?

A) Central planners can achieve lower costs of production than self-interested profit-seeking firms.

B) In a free market, the total costs of producing output are minimized because each firm produces up to the point where P = MC.

C) Firms enter industries whenever P > AC.

D) Firms shut down whenever revenues are insufficient to cover variable costs.

A) Central planners can achieve lower costs of production than self-interested profit-seeking firms.

B) In a free market, the total costs of producing output are minimized because each firm produces up to the point where P = MC.

C) Firms enter industries whenever P > AC.

D) Firms shut down whenever revenues are insufficient to cover variable costs.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

33

Use the following to answer questions:

Figure: Light Bulbs

(Figure: Light Bulbs) What price of light bulbs would induce the firms in this diagram to minimize total production costs while maintaining the same total output?

A) $0.40

B) $0.80

C) $1.00

D) $1.00 for Firm 1, $0.70 for Firm 2

Figure: Light Bulbs

(Figure: Light Bulbs) What price of light bulbs would induce the firms in this diagram to minimize total production costs while maintaining the same total output?

A) $0.40

B) $0.80

C) $1.00

D) $1.00 for Firm 1, $0.70 for Firm 2

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

34

In a competitive industry, if the marginal cost of Factory 1 is higher than that of Factory 2, in the short run:

A) both factories are producing too much.

B) either Factory 1 is producing too much or Factory 2 is producing too little or both.

C) either Factory 1 is producing too little or Factory 2 is producing too much or both.

D) both factories are producing too little.

A) both factories are producing too much.

B) either Factory 1 is producing too much or Factory 2 is producing too little or both.

C) either Factory 1 is producing too little or Factory 2 is producing too much or both.

D) both factories are producing too little.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

35

Friedrich Hayek described the Invisible Hand Properties as:

A) "products of human design but not of human action."

B) "products of human action and human design."

C) "products of human action but not of human design."

D) "products of neither human action nor human design."

A) "products of human design but not of human action."

B) "products of human action and human design."

C) "products of human action but not of human design."

D) "products of neither human action nor human design."

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

36

In a perfectly competitive market,:

A) marginal costs will be less than average costs.

B) all firms will produce an equal amount of output.

C) total industry costs of production are minimized.

D) market price will equal the total cost of production.

A) marginal costs will be less than average costs.

B) all firms will produce an equal amount of output.

C) total industry costs of production are minimized.

D) market price will equal the total cost of production.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

37

Consider two farms. Farm 1 produces the first bushel for $5 each, but the marginal cost rises gradually as the quantity increases. Farm 2 produces the first bushel for $7, but marginal cost also rises gradually as the quantity increases. With a market price of $10 a bushel, how should production be allocated between these two farms?

A) Produce on both farms until the marginal cost on each farm rises to $7.

B) Produce on both farms until the marginal cost on each farm rises to $10.

C) Produce all bushels on Farm 1.

D) Produce all bushels on Farm 2.

A) Produce on both farms until the marginal cost on each farm rises to $7.

B) Produce on both farms until the marginal cost on each farm rises to $10.

C) Produce all bushels on Farm 1.

D) Produce all bushels on Farm 2.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

38

The following are marginal cost curves for selling chicken in a Mom & Pop (MCM) store and in a Big-Box retailer (MCB).

MCM = 2 + 2QM

MCB = 4 + QB

If the price of a chicken is $12, how many chickens does each store supply?

A) Mom & Pop: 5; Big-Box: 8

B) Mom & Pop: 1; Big-Box: 1

C) Mom & Pop: 26; Big-Box: 20

D) Mom & Pop: 8; Big-Box: 8

MCM = 2 + 2QM

MCB = 4 + QB

If the price of a chicken is $12, how many chickens does each store supply?

A) Mom & Pop: 5; Big-Box: 8

B) Mom & Pop: 1; Big-Box: 1

C) Mom & Pop: 26; Big-Box: 20

D) Mom & Pop: 8; Big-Box: 8

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

39

A small island nation produces only boxes of macaroni and cheese, most of which it sells in the export market. The world price per box is $10, regardless of the quantity exported. The nation has three macaroni and cheese factories, each of which varies in efficiency and each has rising marginal costs. To profit the most as a country, what would this nation do?

A) Produce at each factory until the marginal cost rises to $10.

B) Produce at each factory, but only as long as the marginal cost is well below $10.

C) Produce only at the most efficient factory until the marginal cost is $10.

D) Produce only at the most efficient factory, but only if the marginal cost is well below $10.

A) Produce at each factory until the marginal cost rises to $10.

B) Produce at each factory, but only as long as the marginal cost is well below $10.

C) Produce only at the most efficient factory until the marginal cost is $10.

D) Produce only at the most efficient factory, but only if the marginal cost is well below $10.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

40

Use the following to answer questions:

Figure: Light Bulbs

(Figure: Light Bulbs) In this diagram, Firm 1 (MC1) and Firm 2 (MC2) are each making 100 million light bulbs. How many light bulbs should each firm make to minimize total production costs while maintaining the same total output?

A) Firm 1: 40 million; Firm 2: 40 million

B) Firm 1: 20 million; Firm 2: 30 million

C) Firm 1: 80 million; Firm 2: 120 million

D) Firm 1: 120 million; Firm 2: 80 million

Figure: Light Bulbs

(Figure: Light Bulbs) In this diagram, Firm 1 (MC1) and Firm 2 (MC2) are each making 100 million light bulbs. How many light bulbs should each firm make to minimize total production costs while maintaining the same total output?

A) Firm 1: 40 million; Firm 2: 40 million

B) Firm 1: 20 million; Firm 2: 30 million

C) Firm 1: 80 million; Firm 2: 120 million

D) Firm 1: 120 million; Firm 2: 80 million

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

41

In the long run, firms will enter industries where price is:

A) greater than average cost.

B) equal to average cost.

C) less than average cost.

D) positive.

A) greater than average cost.

B) equal to average cost.

C) less than average cost.

D) positive.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

42

According to Adam Smith and other economists, the minimization of total costs in a competitive industry:

A) results from the conscious actions of well-intentioned central planners.

B) results from resources being effectively allocated by trade boards.

C) is neither planned nor intended but results from individuals pursuing their own self-interest.

D) arises from a high level of cooperation among businesses, in terms of input and output plans.

A) results from the conscious actions of well-intentioned central planners.

B) results from resources being effectively allocated by trade boards.

C) is neither planned nor intended but results from individuals pursuing their own self-interest.

D) arises from a high level of cooperation among businesses, in terms of input and output plans.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

43

Above-normal profits are eliminated by ______, and below-normal profits are eliminated by ______.

A) entry; entry

B) exit; exit

C) entry; exit

D) exit; entry

A) entry; entry

B) exit; exit

C) entry; exit

D) exit; entry

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

44

Normal profits in a perfectly competitive industry refer to ______ run profits.

A) positive long

B) zero long

C) negative long

D) positive short

A) positive long

B) zero long

C) negative long

D) positive short

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

45

The elimination principle illustrates the idea that:

A) above-normal profits will be eliminated by decreases in demand due to high prices.

B) losses will be eliminated by the innovation of new products.

C) above-normal profits will be eliminated by the entry of new firms into the industry.

D) losses will be eliminated by firms decreasing their costs.

A) above-normal profits will be eliminated by decreases in demand due to high prices.

B) losses will be eliminated by the innovation of new products.

C) above-normal profits will be eliminated by the entry of new firms into the industry.

D) losses will be eliminated by firms decreasing their costs.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

46

Consider industries X and Y. Industry X has total revenue of $100 million and total costs of $77 million. Industry Y has total revenue of $80 million and total costs of $40 million. We should expect that:

A) prices are higher in Industry X.

B) resources will move from Industry Y to Industry X.

C) labor and capital will move from Industry X to Industry Y.

D) firms in both industries will shut down operations.

A) prices are higher in Industry X.

B) resources will move from Industry Y to Industry X.

C) labor and capital will move from Industry X to Industry Y.

D) firms in both industries will shut down operations.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

47

In a competitive market, firms acting in their own interest will ______ total industry costs of production.

A) maximize

B) minimize

C) eliminate

D) exaggerate

A) maximize

B) minimize

C) eliminate

D) exaggerate

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

48

In a perfectly competitive market, each firm produces its last unit at:

A) the same marginal cost.

B) a unique marginal cost.

C) one of two marginal costs.

D) one of several marginal costs.

A) the same marginal cost.

B) a unique marginal cost.

C) one of two marginal costs.

D) one of several marginal costs.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

49

Figure: Two Farms Refer to the figure. If a farmer owns two farms, Farm 1 and Farm 2, and is under contract to produce 400 bushels of corn for a food processor, should the farmer produce 200 bushels of corn from each farm as shown in this diagram?

A) Yes, splitting production evenly between farms, or factories, is the method to minimize the costs of production.

B) No, he should produce all 400 bushels from Farm 2, the low-cost farm.

C) No, he should produce more corn from Farm 1 and less corn from Farm 2 so that the marginal cost of the last bushel of corn is equal across both farms.

D) No, he should produce less corn from Farm 1 and more corn from Farm 2 so that the marginal cost of the last bushel of corn is equal across both farms.

Refer to the figure. If a farmer owns two farms, Farm 1 and Farm 2, and is under contract to produce 400 bushels of corn for a food processor, should the farmer produce 200 bushels of corn from each farm as shown in this diagram?A) Yes, splitting production evenly between farms, or factories, is the method to minimize the costs of production.

B) No, he should produce all 400 bushels from Farm 2, the low-cost farm.

C) No, he should produce more corn from Farm 1 and less corn from Farm 2 so that the marginal cost of the last bushel of corn is equal across both farms.

D) No, he should produce less corn from Farm 1 and more corn from Farm 2 so that the marginal cost of the last bushel of corn is equal across both farms.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

50

A perfectly competitive firm with lower marginal costs will produce ______ a competitor with higher marginal costs.

A) more units than

B) fewer units than

C) the same number of units as

D) higher quality units than

A) more units than

B) fewer units than

C) the same number of units as

D) higher quality units than

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

51

In a competitive industry, entry and exit decisions:

A) allow some firms to earn above-normal profits in the long run.

B) ensure that labor and capital move across industries to optimally balance production.

C) rely on demand signals, not price signals.

D) move capital and labor away from profitable industries in order to maximize the total value of production.

A) allow some firms to earn above-normal profits in the long run.

B) ensure that labor and capital move across industries to optimally balance production.

C) rely on demand signals, not price signals.

D) move capital and labor away from profitable industries in order to maximize the total value of production.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

52

Which of these equations describes the Invisible Hand Property 1 regarding the minimization of total industry costs?

A) P = AC.

B) P = MR.

C) (P - AC)Q.

D) P = MC1 = MC2 = . . . MCN.

A) P = AC.

B) P = MR.

C) (P - AC)Q.

D) P = MC1 = MC2 = . . . MCN.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

53

In a competitive market, the amount of a good produced is such that social surplus is:

A) minimized.

B) zero.

C) hidden.

D) maximized.

A) minimized.

B) zero.

C) hidden.

D) maximized.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

54

In a competitive industry:

A) all firms will earn above-normal profits if demand is high.

B) the opportunity cost of production is zero.

C) profits are only attainable in the long run to those firms able to innovate at the lowest cost.

D) resources move across firms in such a way that the total value of production is maximized.

A) all firms will earn above-normal profits if demand is high.

B) the opportunity cost of production is zero.

C) profits are only attainable in the long run to those firms able to innovate at the lowest cost.

D) resources move across firms in such a way that the total value of production is maximized.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

55

Entrepreneurs have the incentive to:

A) follow the orders of the central planner.

B) move resources into those industries with the lowest marginal costs.

C) minimize marginal costs.

D) move resources out of low-value industries and into high-value industries.

A) follow the orders of the central planner.

B) move resources into those industries with the lowest marginal costs.

C) minimize marginal costs.

D) move resources out of low-value industries and into high-value industries.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

56

When the size of the production is the most efficient:

A) total cost is at the minimum.

B) average cost is at the minimum.

C) marginal cost is at the minimum.

D) fixed cost is at the minimum.

A) total cost is at the minimum.

B) average cost is at the minimum.

C) marginal cost is at the minimum.

D) fixed cost is at the minimum.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

57

In the long run, firms will exit industries where price is:

A) greater than average cost.

B) equal to average cost.

C) less than average cost.

D) positive.

A) greater than average cost.

B) equal to average cost.

C) less than average cost.

D) positive.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

58

In a perfectly competitive market, each firm produces:

A) the same quantity.

B) a potentially different quantity.

C) as much quantity as possible.

D) as little quantity as possible.

A) the same quantity.

B) a potentially different quantity.

C) as much quantity as possible.

D) as little quantity as possible.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

59

In a perfectly competitive market, each firm sells at:

A) the same price.

B) a unique price.

C) one of two price levels.

D) one of several price levels.

A) the same price.

B) a unique price.

C) one of two price levels.

D) one of several price levels.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

60

Since all competitive firms produce wherever marginal cost equals the market price for the product, we can conclude that:

I. all competitive firms produce at the same marginal cost level.

II. all competitive firms produce the same quantity.

III. all competitive firms make normal profit.

A) I only

B) I and II only

C) II and III only

D) All of the answers are correct.

I. all competitive firms produce at the same marginal cost level.

II. all competitive firms produce the same quantity.

III. all competitive firms make normal profit.

A) I only

B) I and II only

C) II and III only

D) All of the answers are correct.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

61

What happens in a competitive industry when more firms enter?

A) Demand decreases and the price declines, which in turn lowers profits.

B) Supply increases and the price declines, which in turn lowers profits.

C) Supply increases and the price rises, which in turn raises profits.

D) Demand increases and the price rises, which in turn raises profits.

A) Demand decreases and the price declines, which in turn lowers profits.

B) Supply increases and the price declines, which in turn lowers profits.

C) Supply increases and the price rises, which in turn raises profits.

D) Demand increases and the price rises, which in turn raises profits.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

62

When resources move from a low-profit industry into a high-profit industry,:

A) supply in the low-profit industry decreases, raising the market price.

B) demand in the low-profit industry decreases, lowering the market price.

C) supply in the high-profit industry decreases, raising the market price.

D) supply in the high-profit industry increases, raising the market price.

A) supply in the low-profit industry decreases, raising the market price.

B) demand in the low-profit industry decreases, lowering the market price.

C) supply in the high-profit industry decreases, raising the market price.

D) supply in the high-profit industry increases, raising the market price.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

63

When resources move from a low-profit industry into a high profit industry:

A) the value of production falls.

B) the profits of the low-profit industry fall and the profits of the high-profit industry rise.

C) the profits of the low-profit industry rise and the profits of the high-profit industry fall.

D) the Invisible Hand Property 2 is violated.

A) the value of production falls.

B) the profits of the low-profit industry fall and the profits of the high-profit industry rise.

C) the profits of the low-profit industry rise and the profits of the high-profit industry fall.

D) the Invisible Hand Property 2 is violated.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

64

The Invisible Hand Property 2 maintains that:

A) the right mix of resources will be found in each industry, maximizing the total value of production.

B) entry barriers prevent profit signals from working in competitive markets.

C) resources are allocated by greatest need for the greatest number.

D) production costs are minimized.

A) the right mix of resources will be found in each industry, maximizing the total value of production.

B) entry barriers prevent profit signals from working in competitive markets.

C) resources are allocated by greatest need for the greatest number.

D) production costs are minimized.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

65

The greatest use of our limited resources occurs when:

A) the price of all goods is the same.

B) profits in every industry are the same.

C) the price of goods varies.

D) profits vary by industry.

A) the price of all goods is the same.

B) profits in every industry are the same.

C) the price of goods varies.

D) profits vary by industry.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

66

In a free market, if the profit rate in the car industry were higher than in the computer industry, this is a signal that:

A) consumers should spend more on computers and less on cars.

B) consumers should spend more on cars and less on computers.

C) entrepreneurs should move resources from the computer industry to the car industry.

D) entrepreneurs should move resources from the car industry to the computer industry.

A) consumers should spend more on computers and less on cars.

B) consumers should spend more on cars and less on computers.

C) entrepreneurs should move resources from the computer industry to the car industry.

D) entrepreneurs should move resources from the car industry to the computer industry.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following best help entrepreneurs identify low-value industries versus high-value industries?

A) marginal costs

B) price signals

C) central planner

D) total costs

A) marginal costs

B) price signals

C) central planner

D) total costs

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

68

The value of output is maximized in a competitive market because:

A) entrepreneurs are always on the lookout to move resources into higher-value uses, in an effort to create more profit for themselves.

B) government taxation reduces the profit-motive of entrepreneurs.

C) social planners are better able to plan and make resource decisions when there are many buyers and sellers.

D) it is easy for an industry dominated by a single firm to achieve economies of scale, producing output at a low-cost.

A) entrepreneurs are always on the lookout to move resources into higher-value uses, in an effort to create more profit for themselves.

B) government taxation reduces the profit-motive of entrepreneurs.

C) social planners are better able to plan and make resource decisions when there are many buyers and sellers.

D) it is easy for an industry dominated by a single firm to achieve economies of scale, producing output at a low-cost.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

69

If an industry is highly profitable, it is an indication that:

A) the marginal value of resources is high, and more resources need to flow into the industry.

B) the marginal value of resources is low, and resources need to flow out of the industry.

C) labor and, to a limited extent, capital are being exploited.

D) firms are using high-value inputs to create low-value outputs.

A) the marginal value of resources is high, and more resources need to flow into the industry.

B) the marginal value of resources is low, and resources need to flow out of the industry.

C) labor and, to a limited extent, capital are being exploited.

D) firms are using high-value inputs to create low-value outputs.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

70

Monopolists earn ______ profits in the long run.

A) normal

B) above-normal

C) below-normal

D) abnormal

A) normal

B) above-normal

C) below-normal

D) abnormal

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

71

In competitive markets,:

A) firms will earn zero economic profits in the long run.

B) free markets may not always minimize total industry costs.

C) firms with the lowest marginal costs will earn above normal profits even in the long run.

D) firms will earn positive economic profits in the long run.

A) firms will earn zero economic profits in the long run.

B) free markets may not always minimize total industry costs.

C) firms with the lowest marginal costs will earn above normal profits even in the long run.

D) firms will earn positive economic profits in the long run.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following best illustrates how resources move from low-value industries to high-value industries in competitive markets?

A) Entrepreneurs will always find the market in which price is the highest and increase production in it.

B) The invisible hand will always equate prices in the long run.

C) Entrepreneurs will move production from low-profit industries to high-profit industries.

D) Firms will always be able to recognize high- and low- value industries simply by looking at their costs of production.

A) Entrepreneurs will always find the market in which price is the highest and increase production in it.

B) The invisible hand will always equate prices in the long run.

C) Entrepreneurs will move production from low-profit industries to high-profit industries.

D) Firms will always be able to recognize high- and low- value industries simply by looking at their costs of production.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

73

Under perfect competition, the rate of profit tends to be ______ in all industries, so the marginal value of resources is ______ in all industries.

A) different; different

B) the same; the same

C) the same; different

D) different; the same

A) different; different

B) the same; the same

C) the same; different

D) different; the same

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

74

The iconic blue-and-white Chinese porcelain sold to people all over the world (particularly between the fourteenth and the sixteenth centuries) was so successful, entrepreneurs in Persia, Netherlands, Syria, Iberia, Mexico, and many other areas attempted to copy it. The actual process for creating such high-quality ceramics was kept secret, but in 1708 a German alchemist finally found a way to replicate the ancient art. What do you expect happened to the price of porcelain after 1708, and why?

A) It should have fallen because of the increased competition.

B) It should have fallen because of the lower cost to create Chinese porcelain.

C) It should have risen because of the greater difficulty in keeping the method a secret.

D) It should not have changed at all because demand and supply will react accordingly.

A) It should have fallen because of the increased competition.

B) It should have fallen because of the lower cost to create Chinese porcelain.

C) It should have risen because of the greater difficulty in keeping the method a secret.

D) It should not have changed at all because demand and supply will react accordingly.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

75

High profits mean outputs of ______ value are being created from inputs of ______ value.

A) low; low

B) high; high

C) low; high

D) high; low

A) low; low

B) high; high

C) low; high

D) high; low

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

76

According to economist Joseph Schumpeter, competition is about pushing price:

A) above marginal cost.

B) below marginal cost.

C) to marginal cost.

D) to zero.

A) above marginal cost.

B) below marginal cost.

C) to marginal cost.

D) to zero.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

77

If P > AC in a given industry, then:

A) there are too many resources in that industry.

B) there are too few resources in that industry.

C) the industry has the optimal amount of resources.

D) it is not possible to know whether the industry has the optimal amount of resources.

A) there are too many resources in that industry.

B) there are too few resources in that industry.

C) the industry has the optimal amount of resources.

D) it is not possible to know whether the industry has the optimal amount of resources.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

78

The Invisible Hand Property 2 suggests that:

A) profits across competitive industries will be different.

B) profits across competitive industries will be identical.

C) unprofitable industries will grow at the expense of other more profitable industries.

D) capital and labor can only move within a given industry.

A) profits across competitive industries will be different.

B) profits across competitive industries will be identical.

C) unprofitable industries will grow at the expense of other more profitable industries.

D) capital and labor can only move within a given industry.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

79

Table: Profit Margins This table shows that silver, copper, and gold were some of the most profitable industries in July 2011. (For each dollar of sales, profit for these industries is 35.1, 23.5, and 22.0 cents, respectively.) According to the elimination principle, what do you expect to happen to these profit margins in the long run?

A) Profit margins will increase because of increased entry.

B) Profit margins will increase because of increased exit.

C) Profit margins will decrease because of increased entry.

D) Profit margins will decrease because of increased exit.

This table shows that silver, copper, and gold were some of the most profitable industries in July 2011. (For each dollar of sales, profit for these industries is 35.1, 23.5, and 22.0 cents, respectively.) According to the elimination principle, what do you expect to happen to these profit margins in the long run?A) Profit margins will increase because of increased entry.

B) Profit margins will increase because of increased exit.

C) Profit margins will decrease because of increased entry.

D) Profit margins will decrease because of increased exit.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

80

If P < AC in a given industry, then:

A) there are too many resources in that industry.

B) there are too few resources in that industry.

C) the industry has the optimal amount of resources.

D) it is not possible to determine whether the industry has the optimal amount of resources.

A) there are too many resources in that industry.

B) there are too few resources in that industry.

C) the industry has the optimal amount of resources.

D) it is not possible to determine whether the industry has the optimal amount of resources.

Unlock Deck

Unlock for access to all 144 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 144 flashcards in this deck.