Deck 6: Cash and Receivables

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

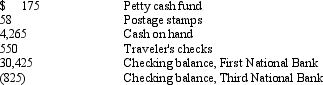

Given the following information:

The total amount of cash that should appear on the balance sheet is

A) $34,648

B) $34,590

C) $34,040

D) $35,415

The total amount of cash that should appear on the balance sheet is

A) $34,648

B) $34,590

C) $34,040

D) $35,415

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

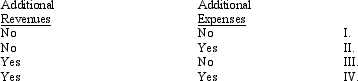

The estimate of bad debt expense may be based on the historical relationships between actual bad debts incurred and

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

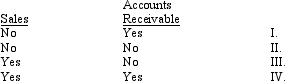

When a company decides to sell its goods on credit, it should evaluate the effect on profit of

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Question

Question

Question

Question

Question

Question

Question

Based on the following information:

If bad debts are estimated to be 3% of net credit sales, the adjusting entry to recognize uncollectible accounts will include a debit to expense for

If bad debts are estimated to be 3% of net credit sales, the adjusting entry to recognize uncollectible accounts will include a debit to expense for

A) $76,020

B) $75,270

C) $76,050

D) $75,300

If bad debts are estimated to be 3% of net credit sales, the adjusting entry to recognize uncollectible accounts will include a debit to expense forA) $76,020

B) $75,270

C) $76,050

D) $75,300

Question

Question

Question

Based on the following information:

If bad debts are estimated to be 1 1/2% of ending accounts receivable, the adjusting entry to recognize bad debts will include a debit to Bad Debt Expense for

A) $170

B) $190

C) $210

D) $250

If bad debts are estimated to be 1 1/2% of ending accounts receivable, the adjusting entry to recognize bad debts will include a debit to Bad Debt Expense for

A) $170

B) $190

C) $210

D) $250

Question

Question

Question

Question

Question

Question

Freeman Corporation estimates uncollectible accounts using a percentage of outstanding accounts receivable. After the year-end adjustment for bad debt expense was made, the company's records reflected the following information (in 000's):

The bad debt expense for the year was

A) $1,100

B) $1,400

C) $1,500

D) $3,000

The bad debt expense for the year was

A) $1,100

B) $1,400

C) $1,500

D) $3,000

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/160

Play

Full screen (f)

Deck 6: Cash and Receivables

1

Which item is not considered cash and cash equivalents on the balance sheet?

A) unrestricted funds on deposit with the bank

B) money market funds

C) post dated checks

D) bank drafts

A) unrestricted funds on deposit with the bank

B) money market funds

C) post dated checks

D) bank drafts

C

2

A bank reconciliation is a analysis of the difference between the account records and the bank records to ensure the accurate ending cash balance.

True

3

Which of the following would not be considered a cash equivalent?

A) travel advances

B) commercial paper

C) treasury bills

D) money market fund securities

A) travel advances

B) commercial paper

C) treasury bills

D) money market fund securities

A

4

At all times the amount of funds less the expenditure vouchers should be equal to the original amount in the petty cash fund.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following would be included in cash and cash equivalents on the balance sheet?

A) sinking fund

B) bank overdrafts

C) commercial paper

D) compensating balances

A) sinking fund

B) bank overdrafts

C) commercial paper

D) compensating balances

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

6

Items classified as "cash" on the balance sheet

A) are limited to coins, currency, or bank drafts

B) must be available to pay current obligations

C) may be subject to contractual restrictions

D) do not include negotiable checks or bank drafts

A) are limited to coins, currency, or bank drafts

B) must be available to pay current obligations

C) may be subject to contractual restrictions

D) do not include negotiable checks or bank drafts

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

7

In a transfer without recourse the transferor retains the risk of ownership and bears any loss from nonpayment.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

8

The two forms of financing agreements that companies use to obtain cash from accounts receivables are pledging and assigning.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

9

Check 21 is a law that allows merchants to scan digital copies of checks to the bank instead of remitting the actual check.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

10

If a company chooses to report its assets using the fair value option they must report any unrealized gains or losses resulting from changes in fair value on its balance sheet.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

11

When the percentage of credit sales is used the accounts receivable are reported at their net realizable value.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

12

Trade receivables are a sub classification of accounts receivable.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

13

A company is not required to disclose all policies related to their receivables but only ones that might be helpful to an external user.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

14

The direct write off method is generally not allowed under GAAP because management selects the period of write off thus allowing earnings management. Where as an estimation of uncollectible accounts an entry is necessary each period to accurately match revenues and expenses.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

15

To classify a receivable as a current asset it must be collected within one year or the normal operating cycle of the business, whichever is shorter.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

16

When the gross method of recording sales and accounts receivables is used it overstates sales and receivables because of this most companies do not use this method.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

17

A key element in internal control over cash receipts utilizes two people (dual control).

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

18

A sinking fund established for the purpose of paying off long term bonds would be recorded on the balance sheet as a cash equivalent.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

19

A compensating balance used to secure a short term loan should be recorded against its short term borrowing in current assets separate from cash.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

20

GAAP requires receivable to be recorded and reported at their present value, but excludes accounts receivables from this rule.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

21

Cash control systems are designed to

A) insure adequate cash is available to meet maturing obligations

B) insure that the proper amount of unused cash is invested

C) safeguard cash

D) protect the organization against business failure by keeping the organization liquid

A) insure adequate cash is available to meet maturing obligations

B) insure that the proper amount of unused cash is invested

C) safeguard cash

D) protect the organization against business failure by keeping the organization liquid

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

22

In order to be classified as a cash equivalent, an investment must have a maturity date of

A) more than six months

B) three to six months

C) six to twelve months

D) three months or less

A) more than six months

B) three to six months

C) six to twelve months

D) three months or less

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following is not considered cash for financial statement reporting

A) cash, coins, and currency

B) travelers checks

C) sinking fund

D) negotiable instruments

A) cash, coins, and currency

B) travelers checks

C) sinking fund

D) negotiable instruments

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

24

Most trade receivables are initially recorded at their

A) maturity values

B) discounted values

C) present values

D) net realizable values

A) maturity values

B) discounted values

C) present values

D) net realizable values

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following would be reported as a liability?

A) demand deposits

B) bank overdrafts

C) certificates of deposit

D) travel advances

A) demand deposits

B) bank overdrafts

C) certificates of deposit

D) travel advances

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

26

All of the following are necessary components of internal control over cash except

A) a petty cash system

B) a cash reserve

C) a bank reconciliation

D) the daily deposit of all receipts in the company's bank account

A) a petty cash system

B) a cash reserve

C) a bank reconciliation

D) the daily deposit of all receipts in the company's bank account

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

27

Given the following information:

The total amount of cash that should appear on the balance sheet is

A) $34,648

B) $34,590

C) $34,040

D) $35,415

The total amount of cash that should appear on the balance sheet is

A) $34,648

B) $34,590

C) $34,040

D) $35,415

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

28

What two functions are cash control systems subdivided into?

A) Control over cash and control over purchase orders.

B) Control over checks and control over invoicing.

C) Control over receipts and control over the bank account.

D) Control over receipts and control over payments.

A) Control over cash and control over purchase orders.

B) Control over checks and control over invoicing.

C) Control over receipts and control over the bank account.

D) Control over receipts and control over payments.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

29

Compensating balance agreements that do not legally restrict the amount of funds shown on the balance sheet should be reported in the

A) current asset section

B) long-term investment section

C) other asset section

D) notes of the financial statements

A) current asset section

B) long-term investment section

C) other asset section

D) notes of the financial statements

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

30

Cash planning is important because a company wants to

A) ensure that it has adequate cash available to meet maturing obligations

B) ensure the safeguarding of its available cash

C) forecast all available cash surpluses

D) prepare a cash budget so it can invest all cash

A) ensure that it has adequate cash available to meet maturing obligations

B) ensure the safeguarding of its available cash

C) forecast all available cash surpluses

D) prepare a cash budget so it can invest all cash

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

31

Current accounts receivables are receivables that are expected to be collected within

A) one year

B) the current operating cycle

C) one year or the current operating cycle, whichever is longer

D) one year or the current operating cycle, whichever is shorter

A) one year

B) the current operating cycle

C) one year or the current operating cycle, whichever is longer

D) one year or the current operating cycle, whichever is shorter

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following would not be a contractual restriction to the cash available to pay current obligations?

A) Sinking fund

B) Certificate of Deposit

C) Post dated checks

D) negotiable instruments

A) Sinking fund

B) Certificate of Deposit

C) Post dated checks

D) negotiable instruments

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

33

Nontrade receivables, such as deposits with utility companies or advances to subsidiary companies, should be

A) recorded in separate accounts and reported as noncurrent assets on the balance sheet

B) recorded along with trade receivables in one account and included as part of the total receivables balance on the balance sheet

C) recorded in separate accounts and separately reported on the balance sheet

D) recorded in separate accounts and reported as an offset to retained earnings on the balance sheet

A) recorded in separate accounts and reported as noncurrent assets on the balance sheet

B) recorded along with trade receivables in one account and included as part of the total receivables balance on the balance sheet

C) recorded in separate accounts and separately reported on the balance sheet

D) recorded in separate accounts and reported as an offset to retained earnings on the balance sheet

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following statements concerning compensating balance agreements is not true?

A) They reduce the amount of cash available to the borrower.

B) They always involve legal restrictions on the cash received.

C) They increase the effective interest rate to the borrower.

D) They must be disclosed in the financial statements' footnotes.

A) They reduce the amount of cash available to the borrower.

B) They always involve legal restrictions on the cash received.

C) They increase the effective interest rate to the borrower.

D) They must be disclosed in the financial statements' footnotes.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

35

Compensating balance agreements that legally restrict cash should

A) only be described in the footnotes to the financial statements

B) be separately reported in the current assets portion of the balance sheet if they are against short-term borrowings

C) be separately classified as noncurrent assets on the balance sheet if they are against short-term borrowings

D) not be shown on the balance sheet

A) only be described in the footnotes to the financial statements

B) be separately reported in the current assets portion of the balance sheet if they are against short-term borrowings

C) be separately classified as noncurrent assets on the balance sheet if they are against short-term borrowings

D) not be shown on the balance sheet

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

36

Which is not a key element of internal control over cash receipts?

A) daily recording of all cash receipts in the accounting records

B) daily entry in a voucher register

C) immediate counting by the person opening the mail or using the cash register

D) daily bank deposits

A) daily recording of all cash receipts in the accounting records

B) daily entry in a voucher register

C) immediate counting by the person opening the mail or using the cash register

D) daily bank deposits

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

37

All of the following are nontrade receivables except

A) declared dividends

B) advances to executives and employees

C) travel advances to employees

D) deposits paid to utility companies

A) declared dividends

B) advances to executives and employees

C) travel advances to employees

D) deposits paid to utility companies

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following is a key element of internal control over cash payments?

A) periodically reconciling the cash account balance on the company's books to the bank statement balance

B) making daily bank deposits

C) requiring that all petty cash vouchers be approved by two signatures

D) authorizing and verifying that all cash received is recorded daily

A) periodically reconciling the cash account balance on the company's books to the bank statement balance

B) making daily bank deposits

C) requiring that all petty cash vouchers be approved by two signatures

D) authorizing and verifying that all cash received is recorded daily

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following is a key element of internal control over cash payments?

A) Making all payments by check.

B) Authorize and sign checks only after the expenditure is approved.

C) Reconcile the bank account.

D) All of these choices

A) Making all payments by check.

B) Authorize and sign checks only after the expenditure is approved.

C) Reconcile the bank account.

D) All of these choices

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

40

Cash control systems are the methods and procedures used to ensure

A) that current obligations are met

B) that excess cash does not exist

C) the safeguarding of cash

D) that unused cash is invested

A) that current obligations are met

B) that excess cash does not exist

C) the safeguarding of cash

D) that unused cash is invested

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

41

Theoretically, the amount of estimated future returns and allowances on credit sales should be recorded during the period of the sale so as not to overstate sales and ending accounts receivable. In practice, these estimates are rarely recorded because

A) the amount of such returns and allowances tends to fluctuate too greatly from period to period

B) there is too much uncertainty surrounding such estimates

C) such estimates are not allowed according to generally accepted accounting principles

D) the amount of such returns and allowances is usually not material

A) the amount of such returns and allowances tends to fluctuate too greatly from period to period

B) there is too much uncertainty surrounding such estimates

C) such estimates are not allowed according to generally accepted accounting principles

D) the amount of such returns and allowances is usually not material

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following would not be reported on the financial statements?

A) sales discount taken

B) trade receivables

C) trade discounts

D) sales discounts not taken

A) sales discount taken

B) trade receivables

C) trade discounts

D) sales discounts not taken

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

43

Which of the following is an advantage of using the net price method for recording cash discounts on credit sales?

A) It eases communication with customers about their balances.

B) It properly reflects current period sales revenue.

C) It simplifies recording of sales returns and allowances.

D) It requires less record keeping than the gross method.

A) It eases communication with customers about their balances.

B) It properly reflects current period sales revenue.

C) It simplifies recording of sales returns and allowances.

D) It requires less record keeping than the gross method.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following methods may not be appropriate for estimating bad debt expense?

A) percentage of net credit sales

B) percentage of outstanding accounts receivable

C) aging of accounts receivable

D) direct write off method

A) percentage of net credit sales

B) percentage of outstanding accounts receivable

C) aging of accounts receivable

D) direct write off method

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

45

When the net price method is used to record credit sales, the sales discounts not taken account is reported as a(n)

A) addition to sales returns and allowances on the income statement

B) deduction from gross sales on the income statement

C) deduction from selling expenses on the income statement

D) addition to other revenue on the income statement

A) addition to sales returns and allowances on the income statement

B) deduction from gross sales on the income statement

C) deduction from selling expenses on the income statement

D) addition to other revenue on the income statement

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

46

Which of the following is not a disadvantage of using the direct write-off method for recording uncollectible accounts?

A) reports actual losses

B) violates the matching principle

C) allows manipulation of income

D) overstates accounts receivable

A) reports actual losses

B) violates the matching principle

C) allows manipulation of income

D) overstates accounts receivable

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

47

An advantage of basing bad debt expense on the historical relationship between bad debts and net credit sales is that

A) it provides the best estimate of the net realizable value of accounts receivable

B) it provides the best information to the credit department to use in its collection activities

C) it best adheres to the matching concept

D) it considers the balance in the allowance account when making the bad debt expense estimate

A) it provides the best estimate of the net realizable value of accounts receivable

B) it provides the best information to the credit department to use in its collection activities

C) it best adheres to the matching concept

D) it considers the balance in the allowance account when making the bad debt expense estimate

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

48

The most theoretically sound method of accounting for cash discounts on credit sales is the

A) net price method

B) discounted price method

C) gross price method

D) net present value method

A) net price method

B) discounted price method

C) gross price method

D) net present value method

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

49

The estimate of bad debt expense may be based on the historical relationships between actual bad debts incurred and

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

50

When an uncollectible account is written off under the estimated allowance method, it

A) decreases net income

B) increases working capital

C) increases the accounts receivable net realizable value

D) leaves total assets unchanged

A) decreases net income

B) increases working capital

C) increases the accounts receivable net realizable value

D) leaves total assets unchanged

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

51

Revenue from a credit sale may be deferred because

A) realization has occurred

B) the collectibility of the receivable is not reasonably assured

C) a right of return exists

D) both the collectibility is not reasonably assured and a right of return exists

A) realization has occurred

B) the collectibility of the receivable is not reasonably assured

C) a right of return exists

D) both the collectibility is not reasonably assured and a right of return exists

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

52

When a company writes off an account receivable using the direct write-off method, the effect of this write-off on the financial statements is to

A) increase the net realizable value of accounts receivable

B) reduce total expenses

C) reduce total assets

D) increase working capital

A) increase the net realizable value of accounts receivable

B) reduce total expenses

C) reduce total assets

D) increase working capital

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

53

When aging of accounts receivable is used, each age group is multiplied by its own estimated uncollectible percentage to determine each age group's estimated uncollectible amount. The sum of the amounts thus determined

A) is the bad debt expense for the year

B) is the correct balance for the allowance for doubtful accounts at year-end

C) is the amount added to the existing credit balance in the allowance account to determine the bad debt expense for the year

D) is the amount that should be written off as uncollectible for the year

A) is the bad debt expense for the year

B) is the correct balance for the allowance for doubtful accounts at year-end

C) is the amount added to the existing credit balance in the allowance account to determine the bad debt expense for the year

D) is the amount that should be written off as uncollectible for the year

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

54

During 2016, a company wrote off $7,500 in uncollectible accounts receivable. At the end of the year, they estimated bad debt expense using a percent of gross sales. In 2017, the company recovered a $1,500 account that was written off in 2016. The recording of this recovery would include a

A) debit to Retained Earnings

B) net change to gross accounts receivable

C) credit to Allowance for Doubtful Accounts

D) credit to Prior-Period Adjustments

A) debit to Retained Earnings

B) net change to gross accounts receivable

C) credit to Allowance for Doubtful Accounts

D) credit to Prior-Period Adjustments

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

55

Bad debt expense is normally reported on the income statement as a(n)

A) operating expense

B) offset against gross sales

C) financial expense in the other items section

D) contra-revenue amount

A) operating expense

B) offset against gross sales

C) financial expense in the other items section

D) contra-revenue amount

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

56

A disadvantage of using the gross price method to account for cash discounts extended by the seller to its customer is that

A) the method reports accounts receivable at the net realizable value

B) the method overstates the current sales and the accounts receivable at the end of the period

C) the method requires more bookkeeping than the net price method

D) the method enables sales returns and allowances to be recorded at gross instead of net amounts

A) the method reports accounts receivable at the net realizable value

B) the method overstates the current sales and the accounts receivable at the end of the period

C) the method requires more bookkeeping than the net price method

D) the method enables sales returns and allowances to be recorded at gross instead of net amounts

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

57

Puzzle Company sold merchandise on credit with a list price of $75,000. Terms were 3/10, n/30. Given the indicated sales discounts methods in the responses, which entry is correct?

A) Gross Price Method

Accounts Receivable 72,750

Sales 72,750

B) Net Price Method

Accounts Receivable 72,750

Sales 72,750

C) Net Price Method

Accounts Receivable 75,000

Sales 75,000

D) Gross Price Method

Accounts Receivable 72,000

Sales 72,000

A) Gross Price Method

Accounts Receivable 72,750

Sales 72,750

B) Net Price Method

Accounts Receivable 72,750

Sales 72,750

C) Net Price Method

Accounts Receivable 75,000

Sales 75,000

D) Gross Price Method

Accounts Receivable 72,000

Sales 72,000

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

58

In accounting for sales discounts, most companies use the

A) allowance method

B) gross price method

C) percentage of price method

D) net price method

A) allowance method

B) gross price method

C) percentage of price method

D) net price method

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

59

The sales returns and allowances account is reported as a

A) contra-revenue account on the income statement

B) current liability on the balance sheet

C) deduction from accounts receivable on the balance sheet

D) selling expense on the income statement

A) contra-revenue account on the income statement

B) current liability on the balance sheet

C) deduction from accounts receivable on the balance sheet

D) selling expense on the income statement

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

60

When a company decides to sell its goods on credit, it should evaluate the effect on profit of

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

61

The method for estimating bad debts that results in the accounts receivable being properly reported at its estimated net realizable value is the

A) aging of accounts receivable method

B) percentage of net sales method

C) percentage of sales method

D) percentage of outstanding accounts payable method

A) aging of accounts receivable method

B) percentage of net sales method

C) percentage of sales method

D) percentage of outstanding accounts payable method

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

62

Prior to the adjusting entry for bad debt expense, Blueberry, Inc.'s balances for Accounts Receivable and Allowances for Doubtful Accounts were $750,000 (debit) and $5,500 (credit), respectively. After the bad debt expense entry was posted, the net realizable value of accounts receivable was $675,000. Bad debt expense for the year

A) cannot be determined from the information given

B) was $69,500

C) was $75,000

D) was $80,500

A) cannot be determined from the information given

B) was $69,500

C) was $75,000

D) was $80,500

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

63

Which of the following conditions must be met by a company (the transferor) to record the transfer of accounts receivable for which it surrenders control to another company as a sale?

A) The transferred assets have been isolated from the transferor (i.e., put beyond the reach of the transferor).

B) The transferee obtains the right to exchange (e.g., sell) the transferred assets.

C) The transferor does not maintain effective control over the transferred assets through an agreement that entitles and obligates the transferor to repurchase the transferred assets before their maturity.

D) All of these conditions must be met.

A) The transferred assets have been isolated from the transferor (i.e., put beyond the reach of the transferor).

B) The transferee obtains the right to exchange (e.g., sell) the transferred assets.

C) The transferor does not maintain effective control over the transferred assets through an agreement that entitles and obligates the transferor to repurchase the transferred assets before their maturity.

D) All of these conditions must be met.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

64

Which of the following is an example of a factoring agreement?

A) using a Neiman Marcus charge card for retail purchases

B) using a Sears charge card for retail purchases

C) using a JCPenney charge card for retail purchases

D) using an American Express card for retail purchases

A) using a Neiman Marcus charge card for retail purchases

B) using a Sears charge card for retail purchases

C) using a JCPenney charge card for retail purchases

D) using an American Express card for retail purchases

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

65

Trainor Company estimates bad debt expense using a percentage of credit sales (5%). The company began its current year with an $8,500 balance in the allowance account. During the current year, $10,500 of accounts receivable were written off, and $1,200 of previously written off accounts were collected. Credit sales for the year were $255,000. The bad debt expense for the year was

A) $10,500

B) $ 8,500

C) $ 12,750

D) $ 11,550

A) $10,500

B) $ 8,500

C) $ 12,750

D) $ 11,550

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

66

Which of the following is NOT a basic form of a financing agreement to obtain cash from accounts receivable?

A) factoring

B) assigning

C) consigning

D) pledging

A) factoring

B) assigning

C) consigning

D) pledging

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

67

Based on the following information:

If bad debts are estimated to be 3% of net credit sales, the adjusting entry to recognize uncollectible accounts will include a debit to expense for

A) $76,020

B) $75,270

C) $76,050

D) $75,300

If bad debts are estimated to be 3% of net credit sales, the adjusting entry to recognize uncollectible accounts will include a debit to expense forA) $76,020

B) $75,270

C) $76,050

D) $75,300

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

68

The method for estimating bad debts that results in current revenues and anticipated current expenses being matched is the

A) percentage of outstanding accounts receivable method

B) percentage of sales method

C) aging of accounts receivable method

D) direct write-off method

A) percentage of outstanding accounts receivable method

B) percentage of sales method

C) aging of accounts receivable method

D) direct write-off method

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

69

A company records the transfer of accounts receivable as a sale if

A) the transferee obtains the right to exchange

B) the transferred assets have been isolated from the transferor

C) the transferor can repurchase the transferred assets before their maturity

D) all of the above conditions are met

A) the transferee obtains the right to exchange

B) the transferred assets have been isolated from the transferor

C) the transferor can repurchase the transferred assets before their maturity

D) all of the above conditions are met

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

70

Based on the following information:

If bad debts are estimated to be 1 1/2% of ending accounts receivable, the adjusting entry to recognize bad debts will include a debit to Bad Debt Expense for

A) $170

B) $190

C) $210

D) $250

If bad debts are estimated to be 1 1/2% of ending accounts receivable, the adjusting entry to recognize bad debts will include a debit to Bad Debt Expense for

A) $170

B) $190

C) $210

D) $250

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

71

Which of the following is not a basic form of financing agreement to obtain cash from accounts receivable?

A) assigning

B) pledging

C) deferring

D) factoring

A) assigning

B) pledging

C) deferring

D) factoring

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

72

Under the allowance method of recording bad debts, which of the following entries, if any, would be made to write off actual uncollectible accounts of $5,500?

A) Allowance for Doubtful Accounts 5,500 Accounts Receivable 5,500

B) Bad Debt Expense 5,500 Allowance for Doubtful Accounts 5,500

C) Bad Debt Expense 5,500

Accounts Receivable 5,500

D) No entry is needed.

A) Allowance for Doubtful Accounts 5,500 Accounts Receivable 5,500

B) Bad Debt Expense 5,500 Allowance for Doubtful Accounts 5,500

C) Bad Debt Expense 5,500

Accounts Receivable 5,500

D) No entry is needed.

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

73

Splitter Corporation had total sales in the current year of $750,000 and credit sales of $650,000. The Accounts Receivable balance was $450,000 on the balance sheet date and the Allowance for Doubtful Accounts had a credit balance of $10,000 before adjusting entries. Bad debt expense is estimated as 2% of credit sales. The adjusting entry to record estimated bad debt expense would include a

A) $ 3,000 debit to Bad Debt Expense

B) $13,000 debit to Bad Debt Expense

C) $13,000 credit to Bad Debt Expense

D) $ 3,000 credit to Bad Debt Expense

A) $ 3,000 debit to Bad Debt Expense

B) $13,000 debit to Bad Debt Expense

C) $13,000 credit to Bad Debt Expense

D) $ 3,000 credit to Bad Debt Expense

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

74

A disadvantage of basing bad debt expense on the historical relationship between actual bad debts and the outstanding accounts receivable balance at the end of the year is that

A) it may not appropriately match current expenses against current revenues

B) it provides a reasonable estimate of the accounts receivable net realizable value

C) it is not a generally accepted accounting procedure

D) it is an income statement approach

A) it may not appropriately match current expenses against current revenues

B) it provides a reasonable estimate of the accounts receivable net realizable value

C) it is not a generally accepted accounting procedure

D) it is an income statement approach

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

75

If a company usually sells its accounts receivable, it records any factoring commissions as a(n)

A) loss

B) expense

C) receivable

D) liability

A) loss

B) expense

C) receivable

D) liability

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

76

Freeman Corporation estimates uncollectible accounts using a percentage of outstanding accounts receivable. After the year-end adjustment for bad debt expense was made, the company's records reflected the following information (in 000's):

The bad debt expense for the year was

A) $1,100

B) $1,400

C) $1,500

D) $3,000

The bad debt expense for the year was

A) $1,100

B) $1,400

C) $1,500

D) $3,000

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

77

When accounting for uncollectible accounts,

A) if the percentage of sales method is in use, any existing balance in the Allowance for Doubtful Accounts is the amount used in the adjusting entry

B) in current accounting practice, the most frequently used method of recognizing bad debts is the direct write-off method

C) writing off a specific receivable does not reduce the current ratio if the percentage of ending accounts receivable method is in use

D) an aging analysis results in reporting accounts receivable at their historical cost on the balance sheet

A) if the percentage of sales method is in use, any existing balance in the Allowance for Doubtful Accounts is the amount used in the adjusting entry

B) in current accounting practice, the most frequently used method of recognizing bad debts is the direct write-off method

C) writing off a specific receivable does not reduce the current ratio if the percentage of ending accounts receivable method is in use

D) an aging analysis results in reporting accounts receivable at their historical cost on the balance sheet

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

78

Which of the following would not be a valid contributing justification for expanding your selling model to include selling goods on account?

A) market share increases

B) revenues generated always exceed the costs incurred

C) improved customer loyalty

D) customer convenience

A) market share increases

B) revenues generated always exceed the costs incurred

C) improved customer loyalty

D) customer convenience

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

79

When a company factors its accounts receivable, it

A) enters into a lending agreement with the institution to receive cash on specific customer accounts

B) sells individual accounts to a financial institution

C) uses these accounts only as a collateral for a loan

D) transfers the accounts but retains title of the accounts until the loan is paid

A) enters into a lending agreement with the institution to receive cash on specific customer accounts

B) sells individual accounts to a financial institution

C) uses these accounts only as a collateral for a loan

D) transfers the accounts but retains title of the accounts until the loan is paid

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

80

Pineapple's Fruit Smoothies began the year with a $4,200 credit balance in its Allowances for Doubtful Accounts. During the year, it accrued $21,500 of bad debt expense and wrote off accounts totaling $28,000. At year-end, a percentage of the outstanding accounts receivable indicated that a $4,800 allowance should be provided for on that date. The year-end adjustment for bad debt expense should be

A) $7,100

B) $4,800

C) $3,000

D) $2,300

A) $7,100

B) $4,800

C) $3,000

D) $2,300

Unlock Deck

Unlock for access to all 160 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 160 flashcards in this deck.