Deck 10: Foreign Currency Transactions

Full screen (f)

Question

Question

On July 1, 2020, CANCO purchased inventory from its main U.S. supplier, RNB Enterprises, at a cost of US$12,000. CANCO's year end is on July 31. Payment of US$12,000 for the inventory is due on August 31, 2020. Some important dates regarding this transaction, as well as the exchange rates in effect at each of these dates are shown below:

At what amount would CANCO record its inventory purchase from RNB on July 1, 2020?

At what amount would CANCO record its inventory purchase from RNB on July 1, 2020?

A) CDN$15,900

B) CDN$16,440

C) CDN$16,140

D) US$12,000

At what amount would CANCO record its inventory purchase from RNB on July 1, 2020?A) CDN$15,900

B) CDN$16,440

C) CDN$16,140

D) US$12,000

Question

Question

Question

On January 1, 2020, Canadian Music International (CMI), a manufacturer of high-end recording equipment based in Toronto, shipped US$120,000 worth of inventory to its main U.S. distributor in Chicago, with full payment of these goods due by February 28, 2020. CMI has a January 31 year end. A list of significant dates and exchange rates is shown below.  The invoice price billed by CMI was US$120,000.

The invoice price billed by CMI was US$120,000.

What is the amount of CMI's foreign exchange gain or loss at year-end?

A) CDN$120 loss

B) CDN$480 gain

C) CDN$120 gain

D) Nil; foreign exchange gains or losses are deferred to settlement

The invoice price billed by CMI was US$120,000.What is the amount of CMI's foreign exchange gain or loss at year-end?

A) CDN$120 loss

B) CDN$480 gain

C) CDN$120 gain

D) Nil; foreign exchange gains or losses are deferred to settlement

Question

On July 1, 2020, CANCO purchased inventory from its main U.S. supplier, RNB Enterprises, at a cost of US$12,000. CANCO's year end is on July 31. Payment of US$12,000 for the inventory is due on August 31, 2020. Some important dates regarding this transaction, as well as the exchange rates in effect at each of these dates are shown below:

At what amount would CANCO record its liability to RNB at the time of the inventory purchase?

At what amount would CANCO record its liability to RNB at the time of the inventory purchase?

A) CDN$15,900

B) CDN$16,440

C) CDN$16,140

D) US$12,000

At what amount would CANCO record its liability to RNB at the time of the inventory purchase?A) CDN$15,900

B) CDN$16,440

C) CDN$16,140

D) US$12,000

Question

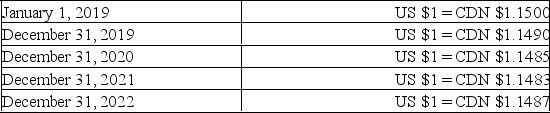

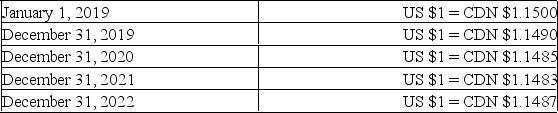

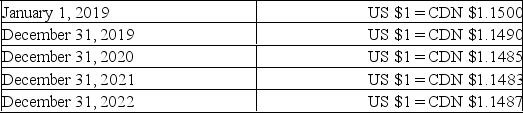

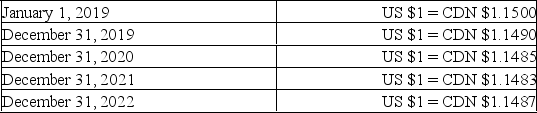

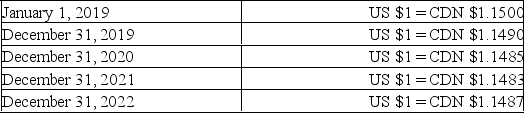

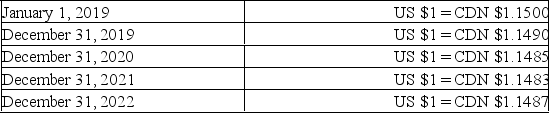

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

The average rates in effect for 2019 and 2020 were as follows:

What is the amount of interest expense (in Canadian Dollars) recorded for 2019?

What is the amount of interest expense (in Canadian Dollars) recorded for 2019?

A) $250,000

B) $287,250

C) $287,325

D) $372,500

The average rates in effect for 2019 and 2020 were as follows: What is the amount of interest expense (in Canadian Dollars) recorded for 2019?A) $250,000

B) $287,250

C) $287,325

D) $372,500

Question

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

The average rates in effect for 2019 and 2020 were as follows:

At what amount (in Canadian Dollars) would XYZ record its initial Loan Liability on January 1, 2019?

At what amount (in Canadian Dollars) would XYZ record its initial Loan Liability on January 1, 2019?

A) $5,471,500

B) $5,476,500

C) $5,747,500

D) $5,750,000

The average rates in effect for 2019 and 2020 were as follows: At what amount (in Canadian Dollars) would XYZ record its initial Loan Liability on January 1, 2019?A) $5,471,500

B) $5,476,500

C) $5,747,500

D) $5,750,000

Question

On July 1, 2020, CANCO purchased inventory from its main U.S. supplier, RNB Enterprises, at a cost of US$12,000. CANCO's year end is on July 31. Payment of US$12,000 for the inventory is due on August 31, 2020. Some important dates regarding this transaction, as well as the exchange rates in effect at each of these dates are shown below:

What was the amount in Canadian dollars paid by CANCO to RNB on the settlement date?

What was the amount in Canadian dollars paid by CANCO to RNB on the settlement date?

A) CDN$15,900

B) CDN$16,440

C) CDN$16,140

D) CDN$12,000

What was the amount in Canadian dollars paid by CANCO to RNB on the settlement date?A) CDN$15,900

B) CDN$16,440

C) CDN$16,140

D) CDN$12,000

Question

Question

On July 1, 2020, CANCO purchased inventory from its main U.S. supplier, RNB Enterprises, at a cost of US$12,000. CANCO's year end is on July 31. Payment of US$12,000 for the inventory is due on August 31, 2020. Some important dates regarding this transaction, as well as the exchange rates in effect at each of these dates are shown below:

What would be the amount of the foreign exchange gain or loss recorded for the year end, July 31, 2020?

What would be the amount of the foreign exchange gain or loss recorded for the year end, July 31, 2020?

A) A CDN$300 exchange loss.

B) A CDN$540 exchange gain.

C) A CDN$300 exchange gain.

D) Nil. Any exchange gain or loss is deferred until settlement.

What would be the amount of the foreign exchange gain or loss recorded for the year end, July 31, 2020?A) A CDN$300 exchange loss.

B) A CDN$540 exchange gain.

C) A CDN$300 exchange gain.

D) Nil. Any exchange gain or loss is deferred until settlement.

Question

Question

Question

On July 1, 2020, CANCO purchased inventory from its main U.S. supplier, RNB Enterprises, at a cost of US$12,000. CANCO's year end is on July 31. Payment of US$12,000 for the inventory is due on August 31, 2020. Some important dates regarding this transaction, as well as the exchange rates in effect at each of these dates are shown below:

What would be the amount of the foreign exchange gain or loss recorded at the settlement date?

What would be the amount of the foreign exchange gain or loss recorded at the settlement date?

A) A CDN$300 exchange loss.

B) A CDN$240 exchange gain.

C) A CDN$300 exchange gain.

D) Nil. Any exchange gain or loss is deferred until settlement.

What would be the amount of the foreign exchange gain or loss recorded at the settlement date?A) A CDN$300 exchange loss.

B) A CDN$240 exchange gain.

C) A CDN$300 exchange gain.

D) Nil. Any exchange gain or loss is deferred until settlement.

Question

Question

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

The average rates in effect for 2019 and 2020 were as follows:

What is the amount of interest paid (in Canadian Dollars) during 2019?

What is the amount of interest paid (in Canadian Dollars) during 2019?

A) $250,000

B) $287,250

C) $287,325

D) $372,500

The average rates in effect for 2019 and 2020 were as follows: What is the amount of interest paid (in Canadian Dollars) during 2019?A) $250,000

B) $287,250

C) $287,325

D) $372,500

Question

On January 1, 2020, Canadian Music International (CMI), a manufacturer of high-end recording equipment based in Toronto, shipped US$120,000 worth of inventory to its main U.S. distributor in Chicago, with full payment of these goods due by February 28, 2020. CMI has a January 31 year end. A list of significant dates and exchange rates is shown below.  The invoice price billed by CMI was US$120,000.

The invoice price billed by CMI was US$120,000.

What is the total amount of CMI's foreign exchange gain or loss on this transaction?

A) CDN$360 loss

B) CDN$120 gain

C) CDN$360 gain

D) CDN$480 gain

The invoice price billed by CMI was US$120,000.What is the total amount of CMI's foreign exchange gain or loss on this transaction?

A) CDN$360 loss

B) CDN$120 gain

C) CDN$360 gain

D) CDN$480 gain

Question

On January 1, 2020, Canadian Music International (CMI), a manufacturer of high-end recording equipment based in Toronto, shipped US$120,000 worth of inventory to its main U.S. distributor in Chicago, with full payment of these goods due by February 28, 2020. CMI has a January 31 year end. A list of significant dates and exchange rates is shown below.  The invoice price billed by CMI was US$120,000.

The invoice price billed by CMI was US$120,000.

What is the amount of cash (in Canadian funds) received by CMI on the settlement date?

A) CDN$136,920

B) CDN$137,040

C) CDN$137,400

D) CDN$137,880

The invoice price billed by CMI was US$120,000.What is the amount of cash (in Canadian funds) received by CMI on the settlement date?

A) CDN$136,920

B) CDN$137,040

C) CDN$137,400

D) CDN$137,880

Question

Question

On January 1, 2020, Canadian Music International (CMI), a manufacturer of high-end recording equipment based in Toronto, shipped US$120,000 worth of inventory to its main U.S. distributor in Chicago, with full payment of these goods due by February 28, 2020. CMI has a January 31 year end. A list of significant dates and exchange rates is shown below.  The invoice price billed by CMI was US$120,000.

The invoice price billed by CMI was US$120,000.

At what value would CMI record the initial sale to its American distributor?

A) CDN$137,400

B) US$120,000

C) CDN$120,000

D) CDN$136,920

The invoice price billed by CMI was US$120,000.At what value would CMI record the initial sale to its American distributor?

A) CDN$137,400

B) US$120,000

C) CDN$120,000

D) CDN$136,920

Question

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

The average rates in effect for 2019 and 2020 were as follows:

What is the amount of interest expense (in Canadian Dollars) recorded for 2020?

What is the amount of interest expense (in Canadian Dollars) recorded for 2020?

A) $249,920

B) $250,080

C) $287,175

D) $287,250

The average rates in effect for 2019 and 2020 were as follows: What is the amount of interest expense (in Canadian Dollars) recorded for 2020?A) $249,920

B) $250,080

C) $287,175

D) $287,250

Question

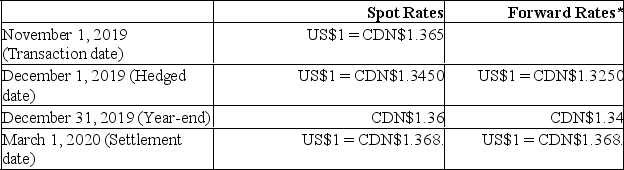

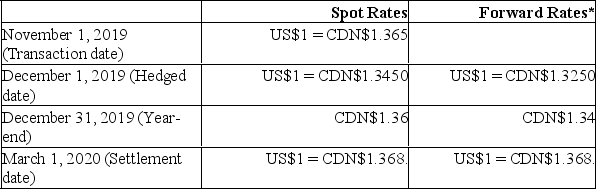

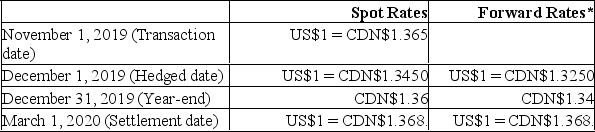

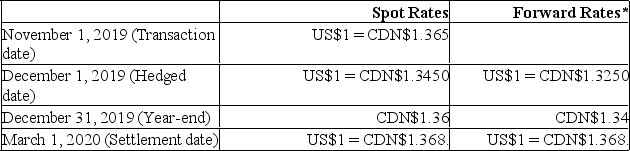

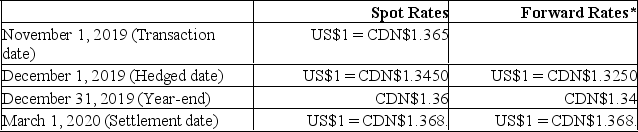

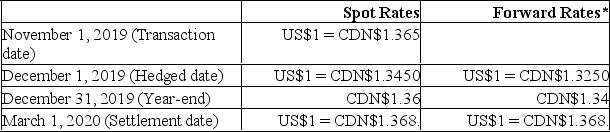

RXN's year-end is on December 31. On November 1, 2019 when the U.S. dollar was worth CDN$1.365, RXN sold merchandise to an American client for US$300,000. Full payment of this invoice was expected by March 1, 2020. On December 1, the spot rate was CDN$1.3450, and the three-month forward rate was CDN$1.3250. In order to minimize its Foreign Exchange risk and exposure, RXN entered into a forward contract with its bank on December 1, 2019 to deliver US$300,000 in three months' time. The spot rate at year-end was CDN$1.36 and the forward rate from December 31, 2019 to March 1, 2020 was CDN$1.34. On March 1, 2020, RXN received the US$300,000 from its client and settled its contract with the bank. The forward contract was to be accounted for as a fair value hedge of the US dollar receivable.

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020

*for contracts expiring on March 1, 2020

How much (in Canadian Dollars) will RXN expect to receive from the bank when its forward contract is settled?

A) $397,500

B) $403,500

C) $402,000

D) $409,500

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020How much (in Canadian Dollars) will RXN expect to receive from the bank when its forward contract is settled?

A) $397,500

B) $403,500

C) $402,000

D) $409,500

Question

Question

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

The average rates in effect for 2019 and 2020 were as follows:

What is the amount of interest paid (in Canadian Dollars) during 2020?

What is the amount of interest paid (in Canadian Dollars) during 2020?

A) $250,000

B) $287,125

C) $287,330

D) $372,500

The average rates in effect for 2019 and 2020 were as follows: What is the amount of interest paid (in Canadian Dollars) during 2020?A) $250,000

B) $287,125

C) $287,330

D) $372,500

Question

Question

Question

RXN's year-end is on December 31. On November 1, 2019 when the U.S. dollar was worth CDN$1.365, RXN sold merchandise to an American client for US$300,000. Full payment of this invoice was expected by March 1, 2020. On December 1, the spot rate was CDN$1.3450 and the three-month forward rate was CDN$1.3250. In order to minimize its Foreign Exchange risk and exposure, RXN entered into a forward contract with its bank on December 1, 2019 to deliver US$300,000 in three months' time. The spot rate at year-end was CDN$1.36 and the forward rate from December 31, 2019 to March 1, 2020 was CDN$1.34. On March 1, 2020, RXN received the US$300,000 from its client and settled its contract with the bank. The forward contract was to be accounted for as a fair value hedge of the US dollar receivable.

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020

*for contracts expiring on March 1, 2020

What is the amount of the exchange gain or loss from the recognition of the hedge discount recognized during 2019?

A) A loss of CDN$4,500.

B) A loss of CDN$3,000.

C) A gain of $ CDN4,500.

D) Nil.

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020What is the amount of the exchange gain or loss from the recognition of the hedge discount recognized during 2019?

A) A loss of CDN$4,500.

B) A loss of CDN$3,000.

C) A gain of $ CDN4,500.

D) Nil.

Question

RXN's year-end is on December 31. On November 1, 2019 when the U.S. dollar was worth CDN$1.365, RXN sold merchandise to an American client for US$300,000. Full payment of this invoice was expected by March 1, 2020. On December 1, the spot rate was CDN$1.3450, and the three-month forward rate was CDN$1.3250. In order to minimize its Foreign Exchange risk and exposure, RXN entered into a forward contract with its bank on December 1, 2019 to deliver US$300,000 in three months' time. The spot rate at year-end was CDN$1.36 and the forward rate from December 31, 2019 to March 1, 2020 was CDN$1.34. On March 1, 2020, RXN received the US$300,000 from its client and settled its contract with the bank. The forward contract was to be accounted for as a fair value hedge of the US dollar receivable.

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020

*for contracts expiring on March 1, 2020

What is the amount of the discount on the forward contract?

A) CDN$1,000

B) CDN$1,500

C) CDN$3,000

D) CDN$6,000

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020What is the amount of the discount on the forward contract?

A) CDN$1,000

B) CDN$1,500

C) CDN$3,000

D) CDN$6,000

Question

Question

RXN's year-end is on December 31. On November 1, 2019 when the U.S. dollar was worth CDN$1.365, RXN sold merchandise to an American client for US$300,000. Full payment of this invoice was expected by March 1, 2020. On December 1, the spot rate was CDN$1.3450 and the three-month forward rate was CDN$1.3250. In order to minimize its Foreign Exchange risk and exposure, RXN entered into a forward contract with its bank on December 1, 2019 to deliver US$300,000 in three months' time. The spot rate at year-end was CDN$1.36 and the forward rate from December 31, 2019 to March 1, 2020 was CDN$1.34. On March 1, 2020, RXN received the US$300,000 from its client and settled its contract with the bank. The forward contract was to be accounted for as a fair value hedge of the US dollar receivable.

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020

*for contracts expiring on March 1, 2020

At what amount (in Canadian Dollars) would the forward contract with the bank be recorded, if recorded gross?

A) $397,500

B) $403,500

C) $402,000

D) $409,500

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020At what amount (in Canadian Dollars) would the forward contract with the bank be recorded, if recorded gross?

A) $397,500

B) $403,500

C) $402,000

D) $409,500

Question

Question

Question

Question

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

The average rates in effect for 2019 and 2020 were as follows:

What is the amount of foreign exchange gain or loss recognized on the 2020 Income Statement as a result of revaluing the loan payable?

What is the amount of foreign exchange gain or loss recognized on the 2020 Income Statement as a result of revaluing the loan payable?

A) $2,500 loss

B) $800 loss

C) $800 gain

D) $2,500 gain

The average rates in effect for 2019 and 2020 were as follows: What is the amount of foreign exchange gain or loss recognized on the 2020 Income Statement as a result of revaluing the loan payable?A) $2,500 loss

B) $800 loss

C) $800 gain

D) $2,500 gain

Question

RXN's year-end is on December 31. On November 1, 2019 when the U.S. dollar was worth CDN$1.365, RXN sold merchandise to an American client for US$300,000. Full payment of this invoice was expected by March 1, 2020. On December 1, the spot rate was CDN$1.3450, and the three-month forward rate was CDN$1.3250. In order to minimize its Foreign Exchange risk and exposure, RXN entered into a forward contract with its bank on December 1, 2019 to deliver US$300,000 in three months' time. The spot rate at year-end was CDN$1.36 and the forward rate from December 31, 2019 to March 1, 2020 was CDN$1.34. On March 1, 2020, RXN received the US$300,000 from its client and settled its contract with the bank. The forward contract was to be accounted for as a fair value hedge of the US dollar receivable.

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020

*for contracts expiring on March 1, 2020

At what amount (in Canadian Dollars) would RXN's sale be recorded initially?

A) $403,500

B) $408,000

C) $409,500

D) $410,400

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020At what amount (in Canadian Dollars) would RXN's sale be recorded initially?

A) $403,500

B) $408,000

C) $409,500

D) $410,400

Question

Question

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

The average rates in effect for 2019 and 2020 were as follows:

By what amount (in Canadian Dollars) would XYZ have to adjust its Loan Liability on December 31, 2020 as a result of the year's foreign exchange rate fluctuations?

By what amount (in Canadian Dollars) would XYZ have to adjust its Loan Liability on December 31, 2020 as a result of the year's foreign exchange rate fluctuations?

A) $3,500 decrease

B) $2,500 decrease

C) $2,500 increase

D) Nil

The average rates in effect for 2019 and 2020 were as follows: By what amount (in Canadian Dollars) would XYZ have to adjust its Loan Liability on December 31, 2020 as a result of the year's foreign exchange rate fluctuations?A) $3,500 decrease

B) $2,500 decrease

C) $2,500 increase

D) Nil

Question

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

The average rates in effect for 2019 and 2020 were as follows:

What is the amount of the foreign exchange gain or loss recognized on the 2019 Income Statement as a result of revaluing the loan payable?

What is the amount of the foreign exchange gain or loss recognized on the 2019 Income Statement as a result of revaluing the loan payable?

A) A CDN$10,000 loss

B) A CDN$5,000 loss

C) A CDN$5,000 gain

D) A CDN$10,000 gain

The average rates in effect for 2019 and 2020 were as follows: What is the amount of the foreign exchange gain or loss recognized on the 2019 Income Statement as a result of revaluing the loan payable?A) A CDN$10,000 loss

B) A CDN$5,000 loss

C) A CDN$5,000 gain

D) A CDN$10,000 gain

Question

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

The average rates in effect for 2019 and 2020 were as follows:

By what amount (in Canadian Dollars) would XYZ have to adjust its Loan Liability on December 31, 2019 as a result of the year's foreign exchange rate fluctuations?

By what amount (in Canadian Dollars) would XYZ have to adjust its Loan Liability on December 31, 2019 as a result of the year's foreign exchange rate fluctuations?

A) A $5,000 decrease.

B) A $2,500 decrease

C) A $5,000 increase.

D) Nil.

The average rates in effect for 2019 and 2020 were as follows: By what amount (in Canadian Dollars) would XYZ have to adjust its Loan Liability on December 31, 2019 as a result of the year's foreign exchange rate fluctuations?A) A $5,000 decrease.

B) A $2,500 decrease

C) A $5,000 increase.

D) Nil.

Question

RXN's year-end is on December 31. On November 1, 2019 when the U.S. dollar was worth CDN$1.365, RXN sold merchandise to an American client for US$300,000. Full payment of this invoice was expected by March 1, 2020. On December 1, the spot rate was CDN$1.3450, and the three-month forward rate was CDN$1.3250. In order to minimize its Foreign Exchange risk and exposure, RXN entered into a forward contract with its bank on December 1, 2019 to deliver US$300,000 in three months' time. The spot rate at year-end was CDN$1.36 and the forward rate from December 31, 2019 to March 1, 2020 was CDN$1.34. On March 1, 2020, RXN received the US$300,000 from its client and settled its contract with the bank. The forward contract was to be accounted for as a fair value hedge of the US dollar receivable.

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020

*for contracts expiring on March 1, 2020

What is the amount of RXN's foreign exchange gain or loss prior to its hedge?

A) A CDN$6,000 loss.

B) A CDN$6,000 gain.

C) A CDN$4,500 gain.

D) Nil

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020What is the amount of RXN's foreign exchange gain or loss prior to its hedge?

A) A CDN$6,000 loss.

B) A CDN$6,000 gain.

C) A CDN$4,500 gain.

D) Nil

Question

Question

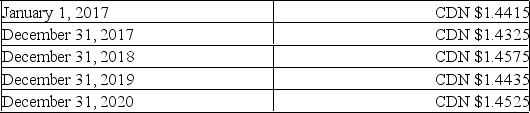

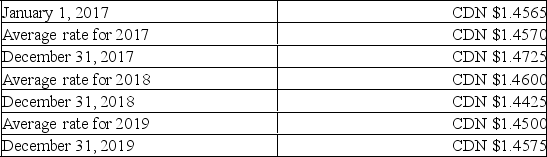

Prairie Dog Inc. borrowed US$10,000,000 on January 1, 2017 at an annual rate of 8%. The loan is due December 31, 2020 and interest is payable annually each December 31. The exchange rates on selected dates throughout the life of the loan are shown below:

Assume that the average annual exchange rate was equal to the December 31st spot rates.

Assume that the average annual exchange rate was equal to the December 31st spot rates.

Calculate the exchange gains or losses that would be reported in the net income of the company for each year over the life of the loan.

Assume that the average annual exchange rate was equal to the December 31st spot rates.Calculate the exchange gains or losses that would be reported in the net income of the company for each year over the life of the loan.

Question

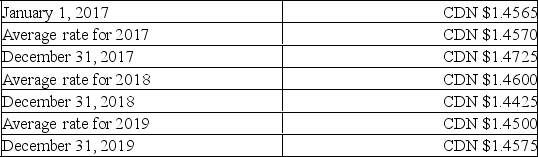

Compucat is a Canadian manufacturing company that produces inexpensive personal and laptop computers. The company has been generating progressively more of its sales from foreign markets. During 2019, the company started purchasing most of its components from a supplier in Germany.

To deal with the uncertainty associated with foreign exchange fluctuations, all of Compucat's foreign currency denominated receivables and payables are hedged with contracts with the company's bank. Compucat's year-end is on December 31. The following transactions took place in 2019:

On September 1, 2019, Compucat purchased components from its German supplier for 100,000 Euros. On that date AMC entered into a forward contract for 100,000 Euros at the 60 day forward rate of 1 Euro = CDN$1.50. The forward contract was designated as a fair value hedge of the amount payable to the German supplier. Compucat settled with the bank and paid its supplier in full on December 1, 2019.

On December 1, 2019 Compucat also shipped a batch of laptop computers to an American client for US$250,000. The invoice required that Compucat receive its payment in full by January 31, 2019. On the date of the sale, the company entered into a forward contract for US$250,000 at the two-month forward rate of US$1 = CDN$1.25. This forward contract was designated to be a fair value hedge of the amount due from the American customer.

The dates and exchange rates relevant to these transactions are shown below.

Prepare the 2019 journal entries to record the above transactions assuming Compucat uses the gross method. In addition, prepare any adjusting journal entries that you deem necessary.

Prepare the 2019 journal entries to record the above transactions assuming Compucat uses the gross method. In addition, prepare any adjusting journal entries that you deem necessary.

To deal with the uncertainty associated with foreign exchange fluctuations, all of Compucat's foreign currency denominated receivables and payables are hedged with contracts with the company's bank. Compucat's year-end is on December 31. The following transactions took place in 2019:

On September 1, 2019, Compucat purchased components from its German supplier for 100,000 Euros. On that date AMC entered into a forward contract for 100,000 Euros at the 60 day forward rate of 1 Euro = CDN$1.50. The forward contract was designated as a fair value hedge of the amount payable to the German supplier. Compucat settled with the bank and paid its supplier in full on December 1, 2019.

On December 1, 2019 Compucat also shipped a batch of laptop computers to an American client for US$250,000. The invoice required that Compucat receive its payment in full by January 31, 2019. On the date of the sale, the company entered into a forward contract for US$250,000 at the two-month forward rate of US$1 = CDN$1.25. This forward contract was designated to be a fair value hedge of the amount due from the American customer.

The dates and exchange rates relevant to these transactions are shown below.

Prepare the 2019 journal entries to record the above transactions assuming Compucat uses the gross method. In addition, prepare any adjusting journal entries that you deem necessary. Question

Question

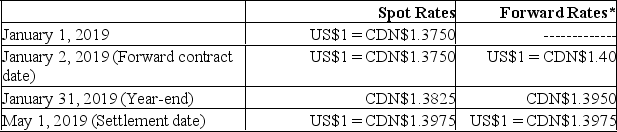

ABC Inc. sells thermal compressors throughout the world. On January 1, 2019, the company sold 500 compressors to an American supplier at a total cost US$60,000 when the spot rate was US$1 = CDN$1.3750. Payment on the invoice was due by May 1, 2019. ABC entered into a 4-month hedge with its bank at a forward rate of CDN$1.40 on January 2, 2019. The forward contract was declared to be a fair value hedge of the fair value of the receivable from the American customer. ABC's year-end is on January 31, and on that date in 2019, the spot rate in effect was CDN$1.3825 and the forward rate to May 1, 2019 was CDN$1.3950.

ABC received payment from its supplier on May 1, 2019 when the spot rate was US$1 = CDN$1.3975.

A summary of the significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on May 1, 2019

*for contracts expiring on May 1, 2019

Assuming that the forward element and spot elements on the forward contract are accounted for separately, which journal entry is required to amortize the discount or premium?

A.

B.

C.

D. No journal entry required

ABC received payment from its supplier on May 1, 2019 when the spot rate was US$1 = CDN$1.3975.

A summary of the significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on May 1, 2019Assuming that the forward element and spot elements on the forward contract are accounted for separately, which journal entry is required to amortize the discount or premium?

A.

B.

C.

D. No journal entry required

Question

Question

Prairie Dog Inc. borrowed US$10,000,000 on January 1, 2017 at an annual rate of 8%. The loan is due December 31, 2020 and interest is payable annually each December 31. The exchange rates on selected dates throughout the life of the loan are shown below:

Assume that the average annual exchange rate was equal to the December 31st spot rates.

Assume that the average annual exchange rate was equal to the December 31st spot rates.

Prepare the journal entries for 2017.

Assume that the average annual exchange rate was equal to the December 31st spot rates.Prepare the journal entries for 2017.

Question

Canada Corp. sells raw lumber to a number of countries around the world. On December 1, 2019 the company shipped some lumber to a client in Japan. The selling price was established at 500,000 Yen with payment to be received on March 1, 2020.

On December 3, 2019 the company entered into a hedge with a Canadian Bank at the 90 day forward rate of 1 Yen = CDN$1.185. The forward contract was designated as a fair value hedge of the receivable from the Japanese customer.

Canada Corp received the payment from its Japanese client on March 1, 2020. Canada Corp's year end is on December 31.

Selected spot rates were as follows:

The two-month forward rate on December 31, 2019 was 1Yen = CDN$1.1800.

The two-month forward rate on December 31, 2019 was 1Yen = CDN$1.1800.

The two-month forward rate on December 31, 2019 was 1Yen = CDN$1.1800.

Prepare a partial Balance Sheet for Canada Corp on December 31, 2019 showing the account receivable from the Japanese client as well as the accounts associated with the hedge. Assume Canada Corp used the gross method to record the forward contract.

On December 3, 2019 the company entered into a hedge with a Canadian Bank at the 90 day forward rate of 1 Yen = CDN$1.185. The forward contract was designated as a fair value hedge of the receivable from the Japanese customer.

Canada Corp received the payment from its Japanese client on March 1, 2020. Canada Corp's year end is on December 31.

Selected spot rates were as follows:

The two-month forward rate on December 31, 2019 was 1Yen = CDN$1.1800.The two-month forward rate on December 31, 2019 was 1Yen = CDN$1.1800.

Prepare a partial Balance Sheet for Canada Corp on December 31, 2019 showing the account receivable from the Japanese client as well as the accounts associated with the hedge. Assume Canada Corp used the gross method to record the forward contract.

Question

Canada Corp. sells raw lumber to a number of countries around the world. On December 1, 2019 the company shipped some lumber to a client in Japan. The selling price was established at 500,000 Yen with payment to be received on March 1, 2020.

On December 3, 2019 the company entered into a hedge with a Canadian Bank at the 90 day forward rate of 1 Yen = CDN$1.185. The forward contract was designated as a fair value hedge of the receivable from the Japanese customer.

Canada Corp received the payment from its Japanese client on March 1, 2020. Canada Corp's year end is on December 31.

Selected spot rates were as follows:

The two-month forward rate on December 31, 2019 was 1Yen = CDN$1.1800.

The two-month forward rate on December 31, 2019 was 1Yen = CDN$1.1800.

The two-month forward rate on December 31, 2019 was 1Yen = CDN$1.1800.

Prepare the journal entries to record the receipt of the 500,000 Yen on March 1, 2020, assuming that Canada Corp did not enter into a hedge transaction in December 2019.

On December 3, 2019 the company entered into a hedge with a Canadian Bank at the 90 day forward rate of 1 Yen = CDN$1.185. The forward contract was designated as a fair value hedge of the receivable from the Japanese customer.

Canada Corp received the payment from its Japanese client on March 1, 2020. Canada Corp's year end is on December 31.

Selected spot rates were as follows:

The two-month forward rate on December 31, 2019 was 1Yen = CDN$1.1800.The two-month forward rate on December 31, 2019 was 1Yen = CDN$1.1800.

Prepare the journal entries to record the receipt of the 500,000 Yen on March 1, 2020, assuming that Canada Corp did not enter into a hedge transaction in December 2019.

Question

Question

Question

Question

Question

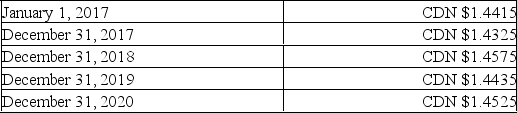

On January 1, 2017, GRL Inc. purchased, in U.S. Funds $500,000 of Bonds of the OBY Company. On that date, the Bonds were trading at par. These Bonds pay 10% interest annually each December 31. The Bonds mature on December 31, 2019. The following exchange rates were applicable between 2017 and 2019. The rates indicate the cost (in Canadian dollars) of purchasing 1 U.S. dollar:

Compute the carrying value of the investment at the end of each year:

Compute the carrying value of the investment at the end of each year:

Compute the carrying value of the investment at the end of each year: Question

On July 1, 2019, Great White North (GWN) Inc. purchased merchandise from a supplier in the U.S. for US$800,000 with terms requiring full payment by October 31, 2019. On July 2, 2019, GWN entered into a forward contract to purchase US$800,000 on October 31, 2019 at a rate of CDN$1.2275. The forward contract was designated as a hedge of the fair value of the amount due to the supplier.

On October 31, 2019, GWN paid its supplier in full. Selected dates and spot rates are shown below:

GWN has a July 31st year end. On that date the forward rate for US dollars for three months was CDN $1.2225.

GWN has a July 31st year end. On that date the forward rate for US dollars for three months was CDN $1.2225.

Prepare any and all journal entries you deem necessary to record the above transaction assuming the forward contract is segregated between the spot element and the forward element. GWN uses the net method to record the forward contract.

On October 31, 2019, GWN paid its supplier in full. Selected dates and spot rates are shown below:

GWN has a July 31st year end. On that date the forward rate for US dollars for three months was CDN $1.2225.Prepare any and all journal entries you deem necessary to record the above transaction assuming the forward contract is segregated between the spot element and the forward element. GWN uses the net method to record the forward contract.

Question

Question

Question

Canada Corp. sells raw lumber to a number of countries around the world. On December 1, 2019 the company shipped some lumber to a client in Japan. The selling price was established at 500,000 Yen with payment to be received on March 1, 2020.

On December 3, 2019 the company entered into a hedge with a Canadian Bank at the 90 day forward rate of 1 Yen = CDN$1.185. The forward contract was designated as a fair value hedge of the receivable from the Japanese customer.

Canada Corp received the payment from its Japanese client on March 1, 2020. Canada Corp's year end is on December 31.

Selected spot rates were as follows:

The two-month forward rate on December 31, 2019 was 1Yen = CDN$1.1800.

The two-month forward rate on December 31, 2019 was 1Yen = CDN$1.1800.

Assuming Canada Corp. used the gross method to record the forward contract, prepare any and all journal entries arising from this transaction.

On December 3, 2019 the company entered into a hedge with a Canadian Bank at the 90 day forward rate of 1 Yen = CDN$1.185. The forward contract was designated as a fair value hedge of the receivable from the Japanese customer.

Canada Corp received the payment from its Japanese client on March 1, 2020. Canada Corp's year end is on December 31.

Selected spot rates were as follows:

The two-month forward rate on December 31, 2019 was 1Yen = CDN$1.1800.Assuming Canada Corp. used the gross method to record the forward contract, prepare any and all journal entries arising from this transaction.

Question

Compucat is a Canadian manufacturing company that produces inexpensive personal and laptop computers. The company has been generating progressively more of its sales from foreign markets. During 2019, the company started purchasing most of its components from a supplier in Germany.

To deal with the uncertainty associated with foreign exchange fluctuations, all of Compucat's foreign currency denominated receivables and payables are hedged with contracts with the company's bank. Compucat's year-end is on December 31. The following transactions took place in 2019:

On September 1, 2019, Compucat purchased components from its German supplier for 100,000 Euros. On that date AMC entered into a forward contract for 100,000 Euros at the 60 day forward rate of 1 Euro = CDN$1.50. The forward contract was designated as a fair value hedge of the amount payable to the German supplier. Compucat settled with the bank and paid its supplier in full on December 1, 2019.

On December 1, 2019 Compucat also shipped a batch of laptop computers to an American client for US$250,000. The invoice required that Compucat receive its payment in full by January 31, 2019. On the date of the sale, the company entered into a forward contract for US$250,000 at the two-month forward rate of US$1 = CDN$1.25. This forward contract was designated to be a fair value hedge of the amount due from the American customer.

The dates and exchange rates relevant to these transactions are shown below.

Prepare the December 31, 2019 Balance Sheet Presentation of the Receivable from the American client and the accounts associated with the hedge. Assume Compucat used the gross method to record the forward contract.

Prepare the December 31, 2019 Balance Sheet Presentation of the Receivable from the American client and the accounts associated with the hedge. Assume Compucat used the gross method to record the forward contract.

To deal with the uncertainty associated with foreign exchange fluctuations, all of Compucat's foreign currency denominated receivables and payables are hedged with contracts with the company's bank. Compucat's year-end is on December 31. The following transactions took place in 2019:

On September 1, 2019, Compucat purchased components from its German supplier for 100,000 Euros. On that date AMC entered into a forward contract for 100,000 Euros at the 60 day forward rate of 1 Euro = CDN$1.50. The forward contract was designated as a fair value hedge of the amount payable to the German supplier. Compucat settled with the bank and paid its supplier in full on December 1, 2019.

On December 1, 2019 Compucat also shipped a batch of laptop computers to an American client for US$250,000. The invoice required that Compucat receive its payment in full by January 31, 2019. On the date of the sale, the company entered into a forward contract for US$250,000 at the two-month forward rate of US$1 = CDN$1.25. This forward contract was designated to be a fair value hedge of the amount due from the American customer.

The dates and exchange rates relevant to these transactions are shown below.

Prepare the December 31, 2019 Balance Sheet Presentation of the Receivable from the American client and the accounts associated with the hedge. Assume Compucat used the gross method to record the forward contract. Question

On January 1, 2017, GRL Inc. purchased, in U.S. Funds $500,000 of Bonds of the OBY Company. On that date, the Bonds were trading at par. These Bonds pay 10% interest annually each December 31. The Bonds mature on December 31, 2019. The following exchange rates were applicable between 2017 and 2019. The rates indicate the cost (in Canadian dollars) of purchasing 1 U.S. dollar:

Prepare GRL's journal entries for each of 2017, 2018 and 2019.

Prepare GRL's journal entries for each of 2017, 2018 and 2019.

Prepare GRL's journal entries for each of 2017, 2018 and 2019. Question

Maplehauff Inc. sells lumber to a number of clients around the world. On December 1, 2019 the company shipped some lumber to a client in the U.S. The selling price was established at US$600,000 with payment to be received on March 1, 2020. On December 3, 2019 the company entered into a hedge with a Canadian Bank at the 90 day forward rate of US$1 = CDN$1.275. The forward contract was designated as a cash flow hedge of the amount due from the American customer. Maplehauff uses the net method to record the forward contract.

Maplehauff Inc. received the payment from its American client on March 1, 2020. The company's year-end is on December 31. The two-month forward rate for US dollars was CDN$1.255 on that date.

Selected spot rates were as follows:

Prepare any and all journal entries arising from this transaction.

Prepare any and all journal entries arising from this transaction.

Maplehauff Inc. received the payment from its American client on March 1, 2020. The company's year-end is on December 31. The two-month forward rate for US dollars was CDN$1.255 on that date.

Selected spot rates were as follows:

Prepare any and all journal entries arising from this transaction. Question

Maplehauff Inc. sells lumber to a number of clients around the world. On December 1, 2019 the company shipped some lumber to a client in the U.S. The selling price was established at US$600,000 with payment to be received on March 1, 2020. On December 3, 2019 the company entered into a hedge with a Canadian Bank at the 90 day forward rate of US$1 = CDN$1.275. The forward contract was designated as a cash flow hedge of the amount due from the American customer. Maplehauff uses the net method to record the forward contract.

Maplehauff Inc. received the payment from its American client on March 1, 2020. The company's year-end is on December 31. The two-month forward rate for US dollars was CDN$1.255 on that date.

Selected spot rates were as follows:

Prepare the journal entries to record the receipt of the US$600,000 on March 1, 2020, assuming that Maplehauff Inc did not enter into a hedge transaction in December 2019.

Prepare the journal entries to record the receipt of the US$600,000 on March 1, 2020, assuming that Maplehauff Inc did not enter into a hedge transaction in December 2019.

Maplehauff Inc. received the payment from its American client on March 1, 2020. The company's year-end is on December 31. The two-month forward rate for US dollars was CDN$1.255 on that date.

Selected spot rates were as follows:

Prepare the journal entries to record the receipt of the US$600,000 on March 1, 2020, assuming that Maplehauff Inc did not enter into a hedge transaction in December 2019. Question

On July 1, 2019, Great White North (GWN) Inc. purchased merchandise from a supplier in the U.S. for US$800,000 with terms requiring full payment by October 31, 2019. On July 2, 2019, GWN entered into a forward contract to purchase US$800,000 on October 31, 2019 at a rate of CDN$1.2275. The forward contract was designated as a hedge of the fair value of the amount due to the supplier.

On October 31, 2019, GWN paid its supplier in full. Selected dates and spot rates are shown below:

GWN has a July 31st year end. On that date the forward rate for US dollars for three months was CDN $1.2225.

GWN has a July 31st year end. On that date the forward rate for US dollars for three months was CDN $1.2225.

Prepare a July 31, 2019 Partial Trial Balance, indicating how each account balance would appear on the company's financial statements.

On October 31, 2019, GWN paid its supplier in full. Selected dates and spot rates are shown below:

GWN has a July 31st year end. On that date the forward rate for US dollars for three months was CDN $1.2225.Prepare a July 31, 2019 Partial Trial Balance, indicating how each account balance would appear on the company's financial statements.

Question

On July 1, 2019, Great White North (GWN) Inc. purchased merchandise from a supplier in the U.S. for US$800,000 with terms requiring full payment by October 31, 2019. On July 2, 2019, GWN entered into a forward contract to purchase US$800,000 on October 31, 2019 at a rate of CDN$1.2275. The forward contract was designated as a hedge of the fair value of the amount due to the supplier.

On October 31, 2019, GWN paid its supplier in full. Selected dates and spot rates are shown below:

GWN has a July 31st year end. On that date the forward rate for US dollars for three months was CDN $1.2225.

GWN has a July 31st year end. On that date the forward rate for US dollars for three months was CDN $1.2225.

Prepare the journal entries assuming that no forward contract was entered into.

On October 31, 2019, GWN paid its supplier in full. Selected dates and spot rates are shown below:

GWN has a July 31st year end. On that date the forward rate for US dollars for three months was CDN $1.2225.Prepare the journal entries assuming that no forward contract was entered into.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/65

Play

Full screen (f)

Deck 10: Foreign Currency Transactions

1

Which of the following statements is correct?

A) The historical rate is the exchange rate on the date of the transaction and the closing rate is the exchange rate at the end of the reporting period.

B) The historical rate is the exchange rate on the date of the transaction and the closing rate is the rate on which any hedge transactions mature.

C) The spot rate is the rate on the date of the transaction and the relevant forward rate is the exchange rate used at the end of the reporting period.

D) The average rate is the exchange rate used for all transactions on transaction date.

A) The historical rate is the exchange rate on the date of the transaction and the closing rate is the exchange rate at the end of the reporting period.

B) The historical rate is the exchange rate on the date of the transaction and the closing rate is the rate on which any hedge transactions mature.

C) The spot rate is the rate on the date of the transaction and the relevant forward rate is the exchange rate used at the end of the reporting period.

D) The average rate is the exchange rate used for all transactions on transaction date.

A

2

On July 1, 2020, CANCO purchased inventory from its main U.S. supplier, RNB Enterprises, at a cost of US$12,000. CANCO's year end is on July 31. Payment of US$12,000 for the inventory is due on August 31, 2020. Some important dates regarding this transaction, as well as the exchange rates in effect at each of these dates are shown below:

At what amount would CANCO record its inventory purchase from RNB on July 1, 2020?

A) CDN$15,900

B) CDN$16,440

C) CDN$16,140

D) US$12,000

At what amount would CANCO record its inventory purchase from RNB on July 1, 2020?A) CDN$15,900

B) CDN$16,440

C) CDN$16,140

D) US$12,000

B

3

At the end of each reporting period, monetary items denominated in a foreign currency must be translated at what rate?

A) The exchange rate in effect at the time of settlement of the contract.

B) The historical rate.

C) The closing rate.

D) The forward contract rate.

A) The exchange rate in effect at the time of settlement of the contract.

B) The historical rate.

C) The closing rate.

D) The forward contract rate.

C

4

Which of the following is NOT currently a cause of fluctuation in foreign exchange rates?

A) Inflation rates.

B) The pegging of a currency to the American (U.S.) dollar.

C) Interest rates.

D) Trade surpluses and deficits.

A) Inflation rates.

B) The pegging of a currency to the American (U.S.) dollar.

C) Interest rates.

D) Trade surpluses and deficits.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

5

On January 1, 2020, Canadian Music International (CMI), a manufacturer of high-end recording equipment based in Toronto, shipped US$120,000 worth of inventory to its main U.S. distributor in Chicago, with full payment of these goods due by February 28, 2020. CMI has a January 31 year end. A list of significant dates and exchange rates is shown below. The invoice price billed by CMI was US$120,000.

What is the amount of CMI's foreign exchange gain or loss at year-end?

A) CDN$120 loss

B) CDN$480 gain

C) CDN$120 gain

D) Nil; foreign exchange gains or losses are deferred to settlement

The invoice price billed by CMI was US$120,000.What is the amount of CMI's foreign exchange gain or loss at year-end?

A) CDN$120 loss

B) CDN$480 gain

C) CDN$120 gain

D) Nil; foreign exchange gains or losses are deferred to settlement

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

6

On July 1, 2020, CANCO purchased inventory from its main U.S. supplier, RNB Enterprises, at a cost of US$12,000. CANCO's year end is on July 31. Payment of US$12,000 for the inventory is due on August 31, 2020. Some important dates regarding this transaction, as well as the exchange rates in effect at each of these dates are shown below:

At what amount would CANCO record its liability to RNB at the time of the inventory purchase?

A) CDN$15,900

B) CDN$16,440

C) CDN$16,140

D) US$12,000

At what amount would CANCO record its liability to RNB at the time of the inventory purchase?A) CDN$15,900

B) CDN$16,440

C) CDN$16,140

D) US$12,000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

7

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

What is the amount of interest expense (in Canadian Dollars) recorded for 2019?

A) $250,000

B) $287,250

C) $287,325

D) $372,500

The average rates in effect for 2019 and 2020 were as follows: What is the amount of interest expense (in Canadian Dollars) recorded for 2019?A) $250,000

B) $287,250

C) $287,325

D) $372,500

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

8

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

At what amount (in Canadian Dollars) would XYZ record its initial Loan Liability on January 1, 2019?

A) $5,471,500

B) $5,476,500

C) $5,747,500

D) $5,750,000

The average rates in effect for 2019 and 2020 were as follows: At what amount (in Canadian Dollars) would XYZ record its initial Loan Liability on January 1, 2019?A) $5,471,500

B) $5,476,500

C) $5,747,500

D) $5,750,000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

9

On July 1, 2020, CANCO purchased inventory from its main U.S. supplier, RNB Enterprises, at a cost of US$12,000. CANCO's year end is on July 31. Payment of US$12,000 for the inventory is due on August 31, 2020. Some important dates regarding this transaction, as well as the exchange rates in effect at each of these dates are shown below:

What was the amount in Canadian dollars paid by CANCO to RNB on the settlement date?

A) CDN$15,900

B) CDN$16,440

C) CDN$16,140

D) CDN$12,000

What was the amount in Canadian dollars paid by CANCO to RNB on the settlement date?A) CDN$15,900

B) CDN$16,440

C) CDN$16,140

D) CDN$12,000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

10

The rate charged by commercial banks for the purchase of any foreign currency (in Canadian dollars) on any given day would be based on which of the following?

A) The average rate.

B) The closing rate.

C) The spot rate.

D) The forward rate.

A) The average rate.

B) The closing rate.

C) The spot rate.

D) The forward rate.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

11

On July 1, 2020, CANCO purchased inventory from its main U.S. supplier, RNB Enterprises, at a cost of US$12,000. CANCO's year end is on July 31. Payment of US$12,000 for the inventory is due on August 31, 2020. Some important dates regarding this transaction, as well as the exchange rates in effect at each of these dates are shown below:

What would be the amount of the foreign exchange gain or loss recorded for the year end, July 31, 2020?

A) A CDN$300 exchange loss.

B) A CDN$540 exchange gain.

C) A CDN$300 exchange gain.

D) Nil. Any exchange gain or loss is deferred until settlement.

What would be the amount of the foreign exchange gain or loss recorded for the year end, July 31, 2020?A) A CDN$300 exchange loss.

B) A CDN$540 exchange gain.

C) A CDN$300 exchange gain.

D) Nil. Any exchange gain or loss is deferred until settlement.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following statements accurately describes the manner in which transactions must be translated under IAS 21 The Effects of Changes in Foreign Exchange Rates?

A) All individual transactions must be translated into the functional currency of the reporting entity.

B) All individual transactions must be converted into the local currency of the reporting entity.

C) All individual transactions are to be reported into the currency of the jurisdiction where the majority of shareholders reside.

D) All individual transactions may be reported into the currency of the country where the corporation does the majority of its business.

A) All individual transactions must be translated into the functional currency of the reporting entity.

B) All individual transactions must be converted into the local currency of the reporting entity.

C) All individual transactions are to be reported into the currency of the jurisdiction where the majority of shareholders reside.

D) All individual transactions may be reported into the currency of the country where the corporation does the majority of its business.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

13

On January 1, 2020, Canadian Music International (CMI), a manufacturer of high-end recording equipment based in Toronto, shipped US$120,000 worth of inventory to its main U.S. distributor in Chicago, with full payment of these goods due by February 28, 2020. CMI has a January 31 year end. A list of significant dates and exchange rates is shown below. The invoice price billed by CMI was US$120,000.

What is the amount of CMI's foreign exchange gain or loss on February 28th?

A) CDN$360 loss.

B) CDN$120 gain.

C) CDN$360 gain.

D) CDN$480 gain.

What is the amount of CMI's foreign exchange gain or loss on February 28th?

A) CDN$360 loss.

B) CDN$120 gain.

C) CDN$360 gain.

D) CDN$480 gain.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

14

On July 1, 2020, CANCO purchased inventory from its main U.S. supplier, RNB Enterprises, at a cost of US$12,000. CANCO's year end is on July 31. Payment of US$12,000 for the inventory is due on August 31, 2020. Some important dates regarding this transaction, as well as the exchange rates in effect at each of these dates are shown below:

What would be the amount of the foreign exchange gain or loss recorded at the settlement date?

A) A CDN$300 exchange loss.

B) A CDN$240 exchange gain.

C) A CDN$300 exchange gain.

D) Nil. Any exchange gain or loss is deferred until settlement.

What would be the amount of the foreign exchange gain or loss recorded at the settlement date?A) A CDN$300 exchange loss.

B) A CDN$240 exchange gain.

C) A CDN$300 exchange gain.

D) Nil. Any exchange gain or loss is deferred until settlement.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

15

Some gains and losses arising on a revaluation of property plant and equipment are to be included in other comprehensive income. When the asset is measured in a foreign currency, how would exchange differences be treated?

A) As an item to be included in income or loss for the year.

B) As a reduction or increase in the carry cost of the asset.

C) As a contra account to be fully disclosed and to show the impact of foreign exchange differences.

D) The differences should be included in the calculation of other comprehensive income.

A) As an item to be included in income or loss for the year.

B) As a reduction or increase in the carry cost of the asset.

C) As a contra account to be fully disclosed and to show the impact of foreign exchange differences.

D) The differences should be included in the calculation of other comprehensive income.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

16

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

What is the amount of interest paid (in Canadian Dollars) during 2019?

A) $250,000

B) $287,250

C) $287,325

D) $372,500

The average rates in effect for 2019 and 2020 were as follows: What is the amount of interest paid (in Canadian Dollars) during 2019?A) $250,000

B) $287,250

C) $287,325

D) $372,500

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

17

On January 1, 2020, Canadian Music International (CMI), a manufacturer of high-end recording equipment based in Toronto, shipped US$120,000 worth of inventory to its main U.S. distributor in Chicago, with full payment of these goods due by February 28, 2020. CMI has a January 31 year end. A list of significant dates and exchange rates is shown below. The invoice price billed by CMI was US$120,000.

What is the total amount of CMI's foreign exchange gain or loss on this transaction?

A) CDN$360 loss

B) CDN$120 gain

C) CDN$360 gain

D) CDN$480 gain

The invoice price billed by CMI was US$120,000.What is the total amount of CMI's foreign exchange gain or loss on this transaction?

A) CDN$360 loss

B) CDN$120 gain

C) CDN$360 gain

D) CDN$480 gain

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

18

On January 1, 2020, Canadian Music International (CMI), a manufacturer of high-end recording equipment based in Toronto, shipped US$120,000 worth of inventory to its main U.S. distributor in Chicago, with full payment of these goods due by February 28, 2020. CMI has a January 31 year end. A list of significant dates and exchange rates is shown below. The invoice price billed by CMI was US$120,000.

What is the amount of cash (in Canadian funds) received by CMI on the settlement date?

A) CDN$136,920

B) CDN$137,040

C) CDN$137,400

D) CDN$137,880

The invoice price billed by CMI was US$120,000.What is the amount of cash (in Canadian funds) received by CMI on the settlement date?

A) CDN$136,920

B) CDN$137,040

C) CDN$137,400

D) CDN$137,880

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following statements is correct?

A) In Canada, the cost of a unit of foreign currency in Canadian dollars is a direct quotation, while the cost in that foreign currency of purchasing one Canadian dollar is referred to as an indirect quotation.

B) In Canada, the cost of a unit of foreign currency in Canadian dollars is an indirect quotation, while the cost in that foreign currency of purchasing one Canadian dollar is referred to as a direct quotation.

C) In Canada, the cost of a unit of foreign currency in Canadian dollars is a direct quotation, and the cost in that foreign currency of purchasing one Canadian dollar is also referred to as a direct quotation.

D) In Canada, the cost of a unit of foreign currency in Canadian dollars is an indirect quotation, while the cost in that foreign currency of purchasing one Canadian dollar is also referred to as an indirect quotation.

A) In Canada, the cost of a unit of foreign currency in Canadian dollars is a direct quotation, while the cost in that foreign currency of purchasing one Canadian dollar is referred to as an indirect quotation.

B) In Canada, the cost of a unit of foreign currency in Canadian dollars is an indirect quotation, while the cost in that foreign currency of purchasing one Canadian dollar is referred to as a direct quotation.

C) In Canada, the cost of a unit of foreign currency in Canadian dollars is a direct quotation, and the cost in that foreign currency of purchasing one Canadian dollar is also referred to as a direct quotation.

D) In Canada, the cost of a unit of foreign currency in Canadian dollars is an indirect quotation, while the cost in that foreign currency of purchasing one Canadian dollar is also referred to as an indirect quotation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

20

On January 1, 2020, Canadian Music International (CMI), a manufacturer of high-end recording equipment based in Toronto, shipped US$120,000 worth of inventory to its main U.S. distributor in Chicago, with full payment of these goods due by February 28, 2020. CMI has a January 31 year end. A list of significant dates and exchange rates is shown below. The invoice price billed by CMI was US$120,000.

At what value would CMI record the initial sale to its American distributor?

A) CDN$137,400

B) US$120,000

C) CDN$120,000

D) CDN$136,920

The invoice price billed by CMI was US$120,000.At what value would CMI record the initial sale to its American distributor?

A) CDN$137,400

B) US$120,000

C) CDN$120,000

D) CDN$136,920

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

21

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

What is the amount of interest expense (in Canadian Dollars) recorded for 2020?

A) $249,920

B) $250,080

C) $287,175

D) $287,250

The average rates in effect for 2019 and 2020 were as follows: What is the amount of interest expense (in Canadian Dollars) recorded for 2020?A) $249,920

B) $250,080

C) $287,175

D) $287,250

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

22

RXN's year-end is on December 31. On November 1, 2019 when the U.S. dollar was worth CDN$1.365, RXN sold merchandise to an American client for US$300,000. Full payment of this invoice was expected by March 1, 2020. On December 1, the spot rate was CDN$1.3450, and the three-month forward rate was CDN$1.3250. In order to minimize its Foreign Exchange risk and exposure, RXN entered into a forward contract with its bank on December 1, 2019 to deliver US$300,000 in three months' time. The spot rate at year-end was CDN$1.36 and the forward rate from December 31, 2019 to March 1, 2020 was CDN$1.34. On March 1, 2020, RXN received the US$300,000 from its client and settled its contract with the bank. The forward contract was to be accounted for as a fair value hedge of the US dollar receivable.

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020

How much (in Canadian Dollars) will RXN expect to receive from the bank when its forward contract is settled?

A) $397,500

B) $403,500

C) $402,000

D) $409,500

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020How much (in Canadian Dollars) will RXN expect to receive from the bank when its forward contract is settled?

A) $397,500

B) $403,500

C) $402,000

D) $409,500

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

23

On July 1, 2019, North Inc., based in Alberta, ordered merchandise from an American supplier for US$600,000. Delivery was scheduled for the month of October, with payment to be made in full on November 15, 2019. Once the order was placed, North entered into a forward contract with its bank to purchase US$600,000 on the settlement date at the forward rate of CDN$1.3625. The forward contract was designated as a cash flow hedge of the cash flow required to settle with the American supplier.

The merchandise was received on October 1, 2019, when the spot rate was US$1 = CDN$1.3575. On October 31, the company's year-end, the spot rate was $1.3690. North purchased the U.S. dollars to pay its supplier on November 15, 2019 when the spot rate was CDN$1.3725. The forward rate to November 15, 2019, was CDN$1.365 on October 1 and CDN$1.37 on October 31.

A summary of the significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on November 15, 2019

What is the amount of the liability to the bank recorded on the commitment date if the forward contract is recorded using the gross method?

A) $806,700

B) $817,500

C) $819,000

D) NIL

The merchandise was received on October 1, 2019, when the spot rate was US$1 = CDN$1.3575. On October 31, the company's year-end, the spot rate was $1.3690. North purchased the U.S. dollars to pay its supplier on November 15, 2019 when the spot rate was CDN$1.3725. The forward rate to November 15, 2019, was CDN$1.365 on October 1 and CDN$1.37 on October 31.

A summary of the significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on November 15, 2019

What is the amount of the liability to the bank recorded on the commitment date if the forward contract is recorded using the gross method?

A) $806,700

B) $817,500

C) $819,000

D) NIL

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

24

XYZ Corp. has a calendar year end. On January 1, 2019, the company borrowed $5,000,000 U.S. dollars from an American Bank. The loan is to be repaid on December 31, 2022 and requires interest at 5% to be paid every December 31. The loan and applicable interest are both to be repaid in U.S. dollars. XYZ does not hedge to minimize its foreign exchange risk. The following exchange rates were in effect throughout the term of the loan:

The average rates in effect for 2019 and 2020 were as follows:

What is the amount of interest paid (in Canadian Dollars) during 2020?

A) $250,000

B) $287,125

C) $287,330

D) $372,500

The average rates in effect for 2019 and 2020 were as follows: What is the amount of interest paid (in Canadian Dollars) during 2020?A) $250,000

B) $287,125

C) $287,330

D) $372,500

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

25

RXN's year-end is on December 31. On November 1, 2019 when the U.S. dollar was worth CDN$1.365, RXN sold merchandise to an American client for US$300,000. Full payment of this invoice was expected by March 1, 2020. On December 1, the spot rate was CDN$1.3450 and the three-month forward rate was CDN$1.3250. In order to minimize its Foreign Exchange risk and exposure, RXN entered into a forward contract with its bank on December 1, 2019 to deliver US$300,000 in three months' time. The spot rate at year-end was CDN$1.36 and the forward rate from December 31, 2019 to March 1, 2020 was CDN$1.34. On March 1, 2020, RXN received the US$300,000 from its client and settled its contract with the bank. The forward contract was to be accounted for as a fair value hedge of the US dollar receivable.

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020

Assuming that the accounts receivable balance was not adjusted on December 1, 2019, what adjustment (if any) would be required to RXN's year-end accounts receivable balance?

A) A CDN$3,000 decrease.

B) A CDN$1,500 decrease.

C) A CDN$3,000 increase.

D) No adjustment is required.

Significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on March 1, 2020

Assuming that the accounts receivable balance was not adjusted on December 1, 2019, what adjustment (if any) would be required to RXN's year-end accounts receivable balance?

A) A CDN$3,000 decrease.

B) A CDN$1,500 decrease.

C) A CDN$3,000 increase.

D) No adjustment is required.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

26

On July 1, 2019, North Inc., based in Alberta, ordered merchandise from an American supplier for US$600,000. Delivery was scheduled for the month of October, with payment to be made in full on November 15, 2019. Once the order was placed, North entered into a forward contract with its bank to purchase US$600,000 on the settlement date at the forward rate of CDN$1.3625. The forward contract was designated as a cash flow hedge of the cash flow required to settle with the American supplier.

The merchandise was received on October 1, 2019, when the spot rate was US$1 = CDN$1.3575. On October 31, the company's year-end, the spot rate was $1.3690. North purchased the U.S. dollars to pay its supplier on November 15, 2019 when the spot rate was CDN$1.3725. The forward rate to November 15, 2019, was CDN$1.365 on October 1 and CDN$1.37 on October 31.

A summary of the significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on November 15, 2019

What is the journal entry required to record the ordering of North's merchandise?

A) No entry is required.

B)

C)

D)

The merchandise was received on October 1, 2019, when the spot rate was US$1 = CDN$1.3575. On October 31, the company's year-end, the spot rate was $1.3690. North purchased the U.S. dollars to pay its supplier on November 15, 2019 when the spot rate was CDN$1.3725. The forward rate to November 15, 2019, was CDN$1.365 on October 1 and CDN$1.37 on October 31.

A summary of the significant dates and exchange rates pertaining to this transaction are as follows:

*for contracts expiring on November 15, 2019

What is the journal entry required to record the ordering of North's merchandise?

A) No entry is required.

B)

C)

D)

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

27