Deck 4: Consolidation of Non-Wholly Owned Subsidiaries

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

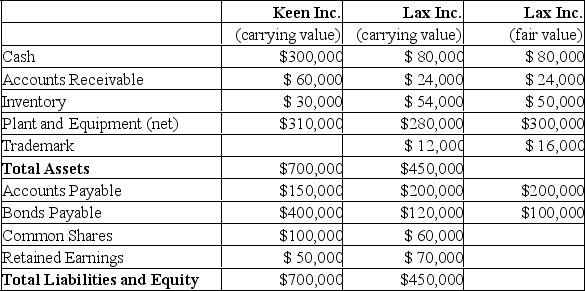

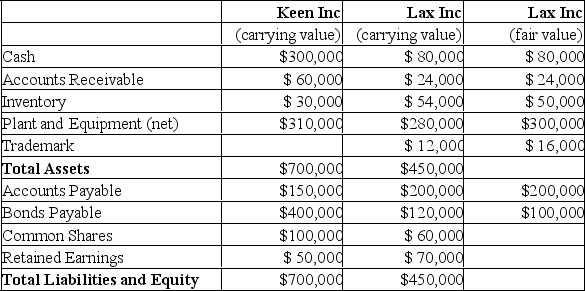

Keen Inc. and Lax Inc. had the following balance sheets on October 31, 2019:

Assuming that Keen Inc. purchases 80% of Lax Inc. for cash of $240,000 on November 1, 2019, prepare the consolidated balance sheet on the date of acquisition under the Fair Value Enterprise Method.

Assuming that Keen Inc. purchases 80% of Lax Inc. for cash of $240,000 on November 1, 2019, prepare the consolidated balance sheet on the date of acquisition under the Fair Value Enterprise Method.

Assuming that Keen Inc. purchases 80% of Lax Inc. for cash of $240,000 on November 1, 2019, prepare the consolidated balance sheet on the date of acquisition under the Fair Value Enterprise Method. Question

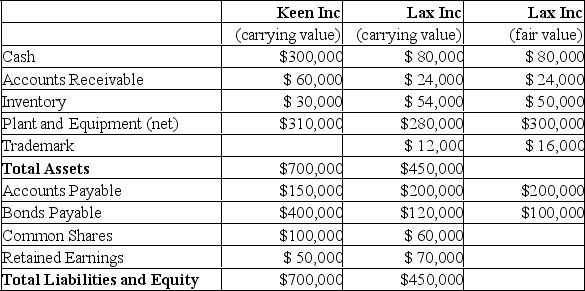

Keen Inc and Lax Inc had the following balance sheets on October 31, 2019:

Assuming that Keen Purchases 100% of Lax for a consideration of $100,000 on September 1, 2019, and accounts for its investment using the cost method, prepare (under the Fair Value Enterprise Method):

Assuming that Keen Purchases 100% of Lax for a consideration of $100,000 on September 1, 2019, and accounts for its investment using the cost method, prepare (under the Fair Value Enterprise Method):

a) the journal entry that Keen Inc. would make to record the acquisition;

b) the elimination entry necessary to produce consolidated balance sheet on the acquisition date.

Assuming that Keen Purchases 100% of Lax for a consideration of $100,000 on September 1, 2019, and accounts for its investment using the cost method, prepare (under the Fair Value Enterprise Method):a) the journal entry that Keen Inc. would make to record the acquisition;

b) the elimination entry necessary to produce consolidated balance sheet on the acquisition date.

Question

Question

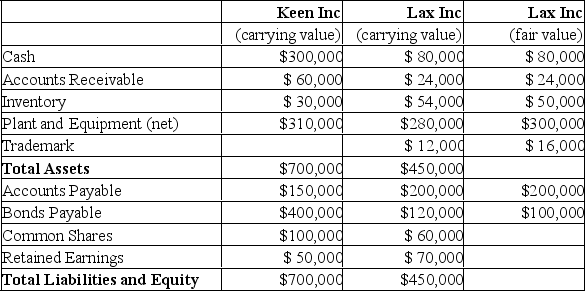

Keen Inc and Lax Inc had the following balance sheets on October 31, 2019:

Assuming that Keen Purchases 80% of Lax for a cash consideration of $240,000 on November 1, 2019, prepare (under the Fair Value Enterprise Method):

Assuming that Keen Purchases 80% of Lax for a cash consideration of $240,000 on November 1, 2019, prepare (under the Fair Value Enterprise Method):

a) the journal entry that Keen Inc. would make to record the acquisition;

b) the elimination entry necessary to produce consolidated balance sheet on the acquisition date.

Assuming that Keen Purchases 80% of Lax for a cash consideration of $240,000 on November 1, 2019, prepare (under the Fair Value Enterprise Method):a) the journal entry that Keen Inc. would make to record the acquisition;

b) the elimination entry necessary to produce consolidated balance sheet on the acquisition date.

Question

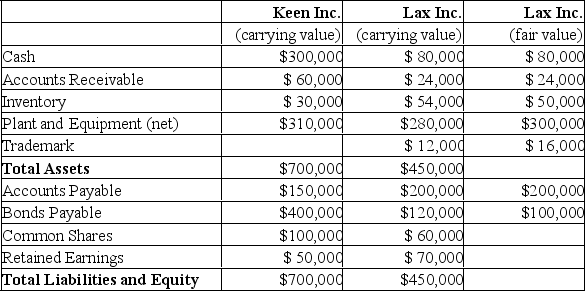

Keen Inc. and Lax Inc. had the following balance sheets on October 31, 2019:

On November 1, 2019, Keen acquired 80% of Lax Inc. for cash consideration of $240,000. Assume that the following draft balance sheet was prepared by a co-worker on the date of acquisition. Assuming this balance sheet is devoid of technical errors, what can be concluded about the balance sheet below?

On November 1, 2019, Keen acquired 80% of Lax Inc. for cash consideration of $240,000. Assume that the following draft balance sheet was prepared by a co-worker on the date of acquisition. Assuming this balance sheet is devoid of technical errors, what can be concluded about the balance sheet below?

On November 1, 2019, Keen acquired 80% of Lax Inc. for cash consideration of $240,000. Assume that the following draft balance sheet was prepared by a co-worker on the date of acquisition. Assuming this balance sheet is devoid of technical errors, what can be concluded about the balance sheet below? Question

Question

Question

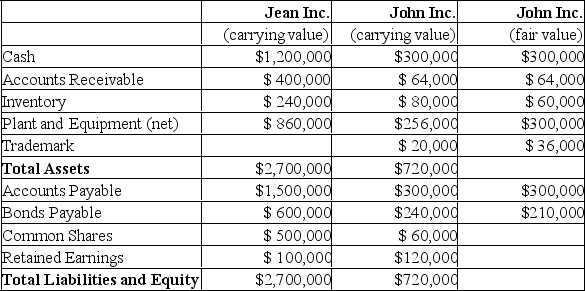

Jean and John Inc had the following balance sheets on August 31, 2019:

On August 31, 2019, Jean's date of acquisition, Jean Inc. purchased 90% of John Inc. for cash consideration of $400,000.

On August 31, 2019, Jean's date of acquisition, Jean Inc. purchased 90% of John Inc. for cash consideration of $400,000.

Assuming the above balance sheets were prepared immediately before the acquisition, prepare Jean Inc's consolidated balance sheet on the date of acquisition using the Fair Value Enterprise Method.

On August 31, 2019, Jean's date of acquisition, Jean Inc. purchased 90% of John Inc. for cash consideration of $400,000.Assuming the above balance sheets were prepared immediately before the acquisition, prepare Jean Inc's consolidated balance sheet on the date of acquisition using the Fair Value Enterprise Method.

Question

Question

Question

Keen Inc. and Lax Inc. had the following balance sheets on October 31, 2019:

Assuming that Keen Inc. purchases 100% of Lax Inc. for cash of $200,000 on November 1, 2019, prepare the consolidated balance sheet on the date of acquisition under the Fair Value Enterprise Method.

Assuming that Keen Inc. purchases 100% of Lax Inc. for cash of $200,000 on November 1, 2019, prepare the consolidated balance sheet on the date of acquisition under the Fair Value Enterprise Method.

Assuming that Keen Inc. purchases 100% of Lax Inc. for cash of $200,000 on November 1, 2019, prepare the consolidated balance sheet on the date of acquisition under the Fair Value Enterprise Method. Question

Question

Question

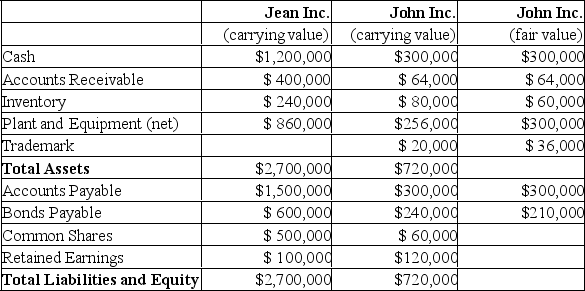

Jean Inc and John Inc had the following balance sheets on August 31, 2019:

On August 31, 2019, Jean's date of acquisition, Jean Inc. purchased 90% of John Inc. for cash consideration of $400,000.

On August 31, 2019, Jean's date of acquisition, Jean Inc. purchased 90% of John Inc. for cash consideration of $400,000.

Assuming the above balance sheets were prepared immediately before the acquisition, prepare Jean Inc's consolidated balance sheet on the date of acquisition using the Proportionate Consolidation Method.

On August 31, 2019, Jean's date of acquisition, Jean Inc. purchased 90% of John Inc. for cash consideration of $400,000.Assuming the above balance sheets were prepared immediately before the acquisition, prepare Jean Inc's consolidated balance sheet on the date of acquisition using the Proportionate Consolidation Method.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/60

Play

Full screen (f)

Deck 4: Consolidation of Non-Wholly Owned Subsidiaries

1

On the date of formation of a 100% owned subsidiary by the parent, which of the following statements pertaining to consolidated financial statements is TRUE?

A) It is possible to prepare consolidated financial statements that include all the assets and liabilities of the subsidiary.

B) Consolidated financial statements are difficult to prepare because the assets and liabilities of the subsidiary have yet to be determined.

C) Consolidation requires the elimination of the parent's investment account against the subsidiary's share capital.

D) Consolidation will not be required since a new legal entity will have been formed.

A) It is possible to prepare consolidated financial statements that include all the assets and liabilities of the subsidiary.

B) Consolidated financial statements are difficult to prepare because the assets and liabilities of the subsidiary have yet to be determined.

C) Consolidation requires the elimination of the parent's investment account against the subsidiary's share capital.

D) Consolidation will not be required since a new legal entity will have been formed.

C

2

One weakness associated with the fair value enterprise method is that:

A) it is inconsistent with the historical cost principle.

B) non-controlling interest (NCI) is computed using the fair market values of the subsidiary's net assets.

C) non-controlling interest (NCI) is computed using the book values of the subsidiary's net assets.

D) the implied value based on the parent's acquisition cost may be unrealistic when the parent purchases significantly less than 100% of the subsidiary's voting shares.

A) it is inconsistent with the historical cost principle.

B) non-controlling interest (NCI) is computed using the fair market values of the subsidiary's net assets.

C) non-controlling interest (NCI) is computed using the book values of the subsidiary's net assets.

D) the implied value based on the parent's acquisition cost may be unrealistic when the parent purchases significantly less than 100% of the subsidiary's voting shares.

D

3

Contingent consideration will be classified as a liability when:

A) it will be paid in the form of additional equity.

B) it will be paid in the form of cash or another asset.

C) the form of payment will be determined at a future date.

D) the acquirer decides the appropriate time to make a payment.

A) it will be paid in the form of additional equity.

B) it will be paid in the form of cash or another asset.

C) the form of payment will be determined at a future date.

D) the acquirer decides the appropriate time to make a payment.

B

4

Under the parent company method, which of the following statements pertaining to consolidated financial statements is TRUE?

A) The consolidated balance sheet is prepared by adding the carrying amounts of both the parent and its subsidiary.

B) The consolidated balance sheet is prepared by adding the carrying amounts of both the parent and its subsidiary as well as the parent's share of any acquisition differentials.

C) The consolidated balance sheet is prepared by adding the fair market values of both the Parent and its subsidiary as well as the parent's share of any acquisition differentials.

D) The consolidated balance sheet is prepared by adding together the fair market values of both the parent and its subsidiary.

A) The consolidated balance sheet is prepared by adding the carrying amounts of both the parent and its subsidiary.

B) The consolidated balance sheet is prepared by adding the carrying amounts of both the parent and its subsidiary as well as the parent's share of any acquisition differentials.

C) The consolidated balance sheet is prepared by adding the fair market values of both the Parent and its subsidiary as well as the parent's share of any acquisition differentials.

D) The consolidated balance sheet is prepared by adding together the fair market values of both the parent and its subsidiary.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

5

Any negative goodwill arising on the date of acquisition:

A) is prorated among the parent company's identifiable net assets.

B) is recognized as a gain on the date of acquisition.

C) should be amortized over a predetermined period.

D) is recognized as a gain on date of acquisition by both the parent and the non-controlling interest.

A) is prorated among the parent company's identifiable net assets.

B) is recognized as a gain on the date of acquisition.

C) should be amortized over a predetermined period.

D) is recognized as a gain on date of acquisition by both the parent and the non-controlling interest.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

6

Contingent consideration should be valued at:

A) the fair value of the consideration on the date of acquisition.

B) the book value of the consideration at the date of acquisition.

C) the acquirer's pro-rata share of the subsidiary's net assets at book value at the date of acquisition.

D) the acquirer's pro-rata share of the subsidiary's net assets at fair value at the date of acquisition.

A) the fair value of the consideration on the date of acquisition.

B) the book value of the consideration at the date of acquisition.

C) the acquirer's pro-rata share of the subsidiary's net assets at book value at the date of acquisition.

D) the acquirer's pro-rata share of the subsidiary's net assets at fair value at the date of acquisition.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

7

Which consolidation method should be used in preparing consolidated financial statements in accordance with IFRS?

A) Proportionate consolidation method.

B) Parent company method.

C) New entity method.

D) Either identifiable net assets or fair value enterprise method.

A) Proportionate consolidation method.

B) Parent company method.

C) New entity method.

D) Either identifiable net assets or fair value enterprise method.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following is a TRUE statement pertaining to a bargain purchase?

A) A bargain purchase occurs when the total consideration is less than the net book value of the subsidiary's identifiable net assets.

B) A bargain purchase occurs when the total consideration is less than the fair market value of the subsidiary's identifiable net assets.

C) A bargain purchase occurs when the total consideration is greater than the fair market value of the subsidiary's identifiable net assets.

D) A bargain purchase occurs when the total consideration is greater than the net book value of the subsidiary's identifiable net assets.

A) A bargain purchase occurs when the total consideration is less than the net book value of the subsidiary's identifiable net assets.

B) A bargain purchase occurs when the total consideration is less than the fair market value of the subsidiary's identifiable net assets.

C) A bargain purchase occurs when the total consideration is greater than the fair market value of the subsidiary's identifiable net assets.

D) A bargain purchase occurs when the total consideration is greater than the net book value of the subsidiary's identifiable net assets.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

9

Parent Inc. and Sub Inc. had the following balance sheets on July 31, 2019: Assuming that Parent Inc acquires 80% of Sub Inc on August 1, 2019 for cash of $180,000, what would be the amount of goodwill appearing on the Consolidated Balance Sheet on the date of acquisition if the proportionate consolidation method were used?

A) $72,000

B) $88,000

C) $70,400

D) Nil

A) $72,000

B) $88,000

C) $70,400

D) Nil

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

10

Parent Inc. and Sub Inc. had the following balance sheets on July 31, 2019: Assuming that Parent Inc acquires 80% of Sub Inc on August 1, 2019 for cash of $180,000, the assets section of Parent's consolidated balance sheet on the date of acquisition would total what amount if the proportionate consolidation method were used?

A) $669,600

B) $599,200

C) $651,000

D) $520,000

A) $669,600

B) $599,200

C) $651,000

D) $520,000

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

11

Parent Inc. and Sub Inc. had the following balance sheets on July 31, 2019: Assuming that Parent Inc acquires 80% of Sub Inc on August 1, 2019 for cash of $180,000, what amount would appear in the Non-Controlling Interest (NCI) Account on the Consolidated Balance Sheet on the date of acquisition if the identifiable net assets (INA) method were used?

A) $45,000

B) $27,400

C) $26,000

D) Nil

A) $45,000

B) $27,400

C) $26,000

D) Nil

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

12

Under the proportionate consolidation method the non-controlling interest (NCI) is:

A) presented as a liability in the consolidated balance sheet.

B) presented as a separate component of shareholders' equity on the consolidated balance sheet.

C) not acknowledged at all.

D) presented as a component of retained earnings on the consolidated balance sheet.

A) presented as a liability in the consolidated balance sheet.

B) presented as a separate component of shareholders' equity on the consolidated balance sheet.

C) not acknowledged at all.

D) presented as a component of retained earnings on the consolidated balance sheet.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

13

Parent Inc. and Sub Inc. had the following balance sheets on July 31, 2019: Assuming that Parent Inc acquires 80% of Sub Inc on August 1, 2019 for cash of $180,000, what amount would appear in the Non-Controlling Interest (NCI) Account on the Consolidated Balance Sheet on the date of acquisition if the proportionate consolidation method were used?

A) Nil

B) $45,000

C) $36,000

D) $180,000

A) Nil

B) $45,000

C) $36,000

D) $180,000

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

14

On the date of acquisition, consolidated retained earnings and consolidated ordinary shares in shareholders' equity is equal to:

A) the sum of the parent and subsidiary's shareholders' equity.

B) the sum of the parent's shareholders' equity plus its pro rata share of the subsidiary's shareholders' equity.

C) the parent's shareholders' equity.

D) the subsidiary's shareholders' equity.

A) the sum of the parent and subsidiary's shareholders' equity.

B) the sum of the parent's shareholders' equity plus its pro rata share of the subsidiary's shareholders' equity.

C) the parent's shareholders' equity.

D) the subsidiary's shareholders' equity.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

15

When the parent forms a new subsidiary:

A) there should be no acquisition differential.

B) gain or loss will usually arise.

C) push down accounting rules must be followed.

D) it should not be included in the company's consolidated financial statements as this would effectively be double-counting.

A) there should be no acquisition differential.

B) gain or loss will usually arise.

C) push down accounting rules must be followed.

D) it should not be included in the company's consolidated financial statements as this would effectively be double-counting.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

16

A negative acquisition differential:

A) is always equal to negative goodwill.

B) occurs when the fair value of the subsidiary's net assets are less than their carrying amounts.

C) implies that the parent company may have overpaid for its acquisition.

D) cannot occur under the acquisition method.

A) is always equal to negative goodwill.

B) occurs when the fair value of the subsidiary's net assets are less than their carrying amounts.

C) implies that the parent company may have overpaid for its acquisition.

D) cannot occur under the acquisition method.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following statements pertaining to the non-controlling interest (NCI) when using the identifiable net assets (INA) method is TRUE?

A) The NCI value is based on the full fair value of the subsidiary including goodwill.

B) The NCI value is based on the book value of the net identifiable assets of the subsidiary excluding any value pertaining to goodwill.

C) The NCI value is based on the book value of the net identifiable assets of the subsidiary including goodwill.

D) The NCI value is based on the fair value of the net identifiable assets of the subsidiary but excludes any value pertaining to goodwill.

A) The NCI value is based on the full fair value of the subsidiary including goodwill.

B) The NCI value is based on the book value of the net identifiable assets of the subsidiary excluding any value pertaining to goodwill.

C) The NCI value is based on the book value of the net identifiable assets of the subsidiary including goodwill.

D) The NCI value is based on the fair value of the net identifiable assets of the subsidiary but excludes any value pertaining to goodwill.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

18

A Co. has acquired an 80% controlling interest in B Co. If using the proportionate consolidation method, the consolidated balance sheet on the date of acquisition, will contain:

A) the parent's pro rata share of the assets and liabilities of the subsidiary at book value.

B) 100% of the assets and liabilities of the subsidiary at fair market value.

C) 100% of the assets and liabilities of the subsidiary at book value.

D) the parent's pro rata share of the assets and liabilities of the subsidiary at fair market value.

A) the parent's pro rata share of the assets and liabilities of the subsidiary at book value.

B) 100% of the assets and liabilities of the subsidiary at fair market value.

C) 100% of the assets and liabilities of the subsidiary at book value.

D) the parent's pro rata share of the assets and liabilities of the subsidiary at fair market value.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

19

HRN Enterprises Inc. (HRN) purchases 80% of the outstanding voting shares of NHR Inc. on January 1, 2018. HRN is using the fair value enterprise (FVE) consolidation method. On that date, which of the following statements pertaining to the non-controlling interest (NCI) is TRUE?

A) HRN's non-controlling interest (NCI) account will include 20% of the book value of NHR's net assets, 20% of the fair value excess and 20% of the goodwill.

B) HRN's non-controlling interest (NCI) account will include 20% of the book value of NHR's net assets.

C) HRN's non-controlling interest (NCI) account will include 20% of the acquisition differential on the date of acquisition.

D) HRN's non-controlling interest (NCI) account will include 20% of the book value of NHR's net assets and 20% of the fair value excess.

A) HRN's non-controlling interest (NCI) account will include 20% of the book value of NHR's net assets, 20% of the fair value excess and 20% of the goodwill.

B) HRN's non-controlling interest (NCI) account will include 20% of the book value of NHR's net assets.

C) HRN's non-controlling interest (NCI) account will include 20% of the acquisition differential on the date of acquisition.

D) HRN's non-controlling interest (NCI) account will include 20% of the book value of NHR's net assets and 20% of the fair value excess.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following is the best approach to determine the fair value of the non-controlling interest under the fair value enterprise method?

A) If a control premium is unlikely, use an implied value based on the consideration paid by the parent

B) Use the market value of the outstanding subsidiary shares (not owned by the parent).

C) Use a valuation model based on the subsidiary's discounted cash flows.

D) Use the share price paid by the parent.

A) If a control premium is unlikely, use an implied value based on the consideration paid by the parent

B) Use the market value of the outstanding subsidiary shares (not owned by the parent).

C) Use a valuation model based on the subsidiary's discounted cash flows.

D) Use the share price paid by the parent.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

21

Parent Inc. and Sub Inc. had the following balance sheets on July 31, 2019: Assuming that Parent Inc acquires 80% of Sub Inc on August 1, 2019 for cash of $180,000, what amount would appear in the Non-Controlling Interest (NCI) Account on the Consolidated Balance Sheet if the fair value enterprise (FVE) method were used?

A) $45,000

B) $27,400

C) $26,000

D) Nil

A) $45,000

B) $27,400

C) $26,000

D) Nil

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

22

Parent Inc. and Sub Inc. had the following balance sheets on July 31, 2019: Assuming that Parent Inc acquires 80% of Sub Inc on August 1, 2019 for cash of $180,000, the assets section of Parent's consolidated balance sheet on the date of acquisition would total to what amount under the fair value enterprise method?

A) $552,000

B) $639,200

C) $651,000

D) $659,000

A) $552,000

B) $639,200

C) $651,000

D) $659,000

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

23

In the event of a negative acquisition differential, under what circumstances is it still possible to have positive goodwill?

A) It is not possible; once there is a negative acquisition differential, the result is negative goodwill.

B) If the fair values of the subsidiary's net assets are less than their carrying amounts and if the total consideration is greater than the fair value of the subsidiary's identifiable nets assets, there will be positive goodwill.

C) If the total consideration exceeds the carrying value of the subsidiary's identifiable nets assets, there will be positive goodwill.

D) If the carrying values of the subsidiary's net assets are less than their fair values and if the total consideration is greater than the carrying amount of the subsidiary's identifiable nets assets, there will be positive goodwill.

A) It is not possible; once there is a negative acquisition differential, the result is negative goodwill.

B) If the fair values of the subsidiary's net assets are less than their carrying amounts and if the total consideration is greater than the fair value of the subsidiary's identifiable nets assets, there will be positive goodwill.

C) If the total consideration exceeds the carrying value of the subsidiary's identifiable nets assets, there will be positive goodwill.

D) If the carrying values of the subsidiary's net assets are less than their fair values and if the total consideration is greater than the carrying amount of the subsidiary's identifiable nets assets, there will be positive goodwill.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

24

If the non-controlling interest at acquisition is based on the fair value of the subsidiary's identifiable net assets, which consolidation method is being applied?

A) Proportionate consolidation method

B) Parent company method

C) Fair value enterprise method

D) Identifiable net assets method.

A) Proportionate consolidation method

B) Parent company method

C) Fair value enterprise method

D) Identifiable net assets method.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

25

When a contingent consideration arising from a business combination is classified as a liability, how is any difference between the original estimate of the amount to be paid and the actual amount paid accounted for if the difference arises due to a change in circumstances?

A) As an adjustment to the consideration paid for the subsidiary.

B) As an adjustment to an estimate included in the determination of net income.

C) As a direct adjustment to consolidated retained earnings.

D) As an adjustment to consolidated contributed surplus.

A) As an adjustment to the consideration paid for the subsidiary.

B) As an adjustment to an estimate included in the determination of net income.

C) As a direct adjustment to consolidated retained earnings.

D) As an adjustment to consolidated contributed surplus.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

26

Parent Inc. and Sub Inc. had the following balance sheets on July 31, 2019: Assuming that Parent Inc acquires 80% of Sub Inc on August 1, 2019 for cash of $180,000, what would be the amount of goodwill appearing on the Consolidated Balance Sheet on the date of acquisition if the identifiable net assets (INA) method were used?

A) $72,000

B) $88,000

C) $70,400

D) Nil

A) $72,000

B) $88,000

C) $70,400

D) Nil

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

27

Parent Inc. and Sub Inc. had the following balance sheets on July 31, 2019: Assuming that Parent Inc acquires 80% of Sub Inc on August 1, 2019 for cash of $180,000, the Shareholders' Equity section of Parent's consolidated balance sheet on the date of acquisition would total to what amount under the fair value enterprise method?

A) $140,000

B) $185,000

C) $244,000

D) $270,000

A) $140,000

B) $185,000

C) $244,000

D) $270,000

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

28

Parent Inc. and Sub Inc. had the following balance sheets on July 31, 2019: Assuming that Parent Inc acquires 80% of Sub Inc on August 1, 2019 for cash of $180,000, the liabilities section of Parent's consolidated balance sheet on the date of acquisition (August 1, 2019) would total to what amount under the fair value enterprise method?

A) $470,000

B) $474,000

C) $500,000

D) $519,000

A) $470,000

B) $474,000

C) $500,000

D) $519,000

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

29

Any goodwill on the subsidiary company's books on the date of acquisition:

A) must be revalued.

B) must be eliminated in preparing consolidated financial statements.

C) must be recorded as a loss on acquisition.

D) must be subject to an impairment test.

A) must be revalued.

B) must be eliminated in preparing consolidated financial statements.

C) must be recorded as a loss on acquisition.

D) must be subject to an impairment test.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

30

Which statement about the differences between consolidation methods permitted under ASPE and IFRS is true?

A) IFRS and ASPE both require the use of the fair value enterprise method or the identifiable net assets method.

B) IFRS and ASPE both require the use of the identifiable net assets method.

C) IFRS permits either the fair value enterprise method or identifiable net assets method; ASPE requires the fair value enterprise method.

D) IFRS permits either the fair value enterprise method or the identifiable net assets method; ASPE requires the identifiable net assets method.

A) IFRS and ASPE both require the use of the fair value enterprise method or the identifiable net assets method.

B) IFRS and ASPE both require the use of the identifiable net assets method.

C) IFRS permits either the fair value enterprise method or identifiable net assets method; ASPE requires the fair value enterprise method.

D) IFRS permits either the fair value enterprise method or the identifiable net assets method; ASPE requires the identifiable net assets method.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

31

When a contingent consideration arising from a business combination is classified as equity, how is any change in its fair value accounted for if the difference arises due to a change in circumstances?

A) As an adjustment to the consideration paid for the subsidiary.

B) As an adjustment to an estimate included in the determination of net income.

C) As a memorandum entry indicating that additional shares had been issued.

D) As an adjustment to consolidated contributed surplus.

A) As an adjustment to the consideration paid for the subsidiary.

B) As an adjustment to an estimate included in the determination of net income.

C) As a memorandum entry indicating that additional shares had been issued.

D) As an adjustment to consolidated contributed surplus.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

32

Which accounts differ on the consolidated balance sheet when using the fair value enterprise method compared to the identifiable net assets method?

A) The investment in subsidiary balance and the consolidated retained earnings balance.

B) The goodwill balance and the consolidated retained earnings balance.

C) The goodwill balance and the non-controlling interest balance.

D) The investment in subsidiary balance and the non-controlling interest balance.

A) The investment in subsidiary balance and the consolidated retained earnings balance.

B) The goodwill balance and the consolidated retained earnings balance.

C) The goodwill balance and the non-controlling interest balance.

D) The investment in subsidiary balance and the non-controlling interest balance.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

33

Non-controlling interest (NCI) is presented under the liabilities section of the consolidated balance sheet under the:

A) the fair value enterprise method.

B) the proportionate consolidation method.

C) the parent company method.

D) both the parent company method and the proportionate consolidation method.

A) the fair value enterprise method.

B) the proportionate consolidation method.

C) the parent company method.

D) both the parent company method and the proportionate consolidation method.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

34

IFRS permits several methods to be used to determine the fair value of the non-controlling interest in a subsidiary at the acquisition date. Which of the following is NOT an appropriate method to determine the fair value of the non-controlling interest (NCI)?

A) The NCI may be valued at the market value of the subsidiary's shares.

B) The NCI may be valued by determining the fair value of the business by means of an independent business valuation and then deducting the fair value of the controlling interest.

C) The NCI may be valued proportionately to the price paid by the parent for its controlling interest.

D) The NCI can't be valued objectively, so a nominal value of one dollar is assigned to the NCI.

A) The NCI may be valued at the market value of the subsidiary's shares.

B) The NCI may be valued by determining the fair value of the business by means of an independent business valuation and then deducting the fair value of the controlling interest.

C) The NCI may be valued proportionately to the price paid by the parent for its controlling interest.

D) The NCI can't be valued objectively, so a nominal value of one dollar is assigned to the NCI.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

35

The focus of the consolidated financial statements on the shareholders of the parent company is characteristic of:

A) the fair value enterprise method.

B) The proportionate consolidation method.

C) the parent company method.

D) both the parent Company method and the proportionate consolidation method.

A) the fair value enterprise method.

B) The proportionate consolidation method.

C) the parent company method.

D) both the parent Company method and the proportionate consolidation method.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

36

When a contingent consideration arising from a business combination is classified as a liability, how is any change in its fair value as a result of new information about the facts and circumstances that existed at the acquisition date accounted for if identified and measured within one year subsequent to the acquisition date?

A) As an adjustment to the consideration paid for the subsidiary.

B) As an adjustment to an estimate included in the determination of net income.

C) As a direct adjustment to consolidated retained earnings.

D) As an adjustment to consolidated contributed surplus.

A) As an adjustment to the consideration paid for the subsidiary.

B) As an adjustment to an estimate included in the determination of net income.

C) As a direct adjustment to consolidated retained earnings.

D) As an adjustment to consolidated contributed surplus.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

37

Parent Inc. and Sub Inc. had the following balance sheets on July 31, 2019: Assuming that Parent Inc acquires 80% of Sub Inc on August 1, 2019 for cash of $180,000, what would be the amount of goodwill appearing on the Consolidated Balance Sheet on the date of acquisition if the fair value enterprise (FVE) method were used?

A) $72,000

B) $88,000

C) $70,400

D) Nil

A) $72,000

B) $88,000

C) $70,400

D) Nil

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

38

Which method presents the non-controlling interest (NCI) in in the Shareholders' Equity section of the balance sheet?

A) The fair value enterprise method.

B) The proportionate consolidation.

C) The parent company method.

D) The acquisition methoD.The NCI is not presented under the proportionate consolidation method. The NCI is presented as a liability under the parent company method. The NCI is presented as a component of shareholders' equity under the fair value enterprise method. Note: the identifiable net assets method also presents the NCI in the shareholders' equity section.

A) The fair value enterprise method.

B) The proportionate consolidation.

C) The parent company method.

D) The acquisition methoD.The NCI is not presented under the proportionate consolidation method. The NCI is presented as a liability under the parent company method. The NCI is presented as a component of shareholders' equity under the fair value enterprise method. Note: the identifiable net assets method also presents the NCI in the shareholders' equity section.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

39

Parent Inc. and Sub Inc. had the following balance sheets on July 31, 2019: Assuming that Parent Inc acquires 80% of Sub Inc on August 1, 2019 for cash of $180,000, the Shareholders' Equity section of Parent's consolidated balance sheet on the date of acquisition would total to what amount if the identifiable net assets (INA) method were used?

A) $140,000

B) $185,000

C) $270,000

D) $167,400

A) $140,000

B) $185,000

C) $270,000

D) $167,400

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

40

When the non-controlling interest's share of the subsidiary's goodwill cannot be reliably determined, the method used to prepare consolidated financial statements is:

A) the fair value enterprise method.

B) The proportionate consolidation method.

C) the parent company method.

D) the identifiable net assets method.

A) the fair value enterprise method.

B) The proportionate consolidation method.

C) the parent company method.

D) the identifiable net assets method.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

41

A business combination involves a contingent consideration. As a result, two years after the acquisition date, the acquirer was required to issue an additional 40,000 common shares at a time when the fair value of the common shares was $4 per share. What effect would this transaction have on the balance in the common shares account in the consolidated financial statements on the date of acquisition?

A) It would increase by $160,000.

B) It would not change.

C) It would decrease by $160,000.

D) It is not possible to determine the effect from the information provided.

A) It would increase by $160,000.

B) It would not change.

C) It would decrease by $160,000.

D) It is not possible to determine the effect from the information provided.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

42

What value should be recorded as the fair value of a contingent consideration arising from a business acquisition when it is classified as a liability?

A) The undiscounted maximum amount that could be paid.

B) The discounted present value of the maximum amount that could be paid.

C) The undiscounted probabilistic estimate of the amount to be paid.

D) The discounted probabilistic estimate of the amount to be paid.

A) The undiscounted maximum amount that could be paid.

B) The discounted present value of the maximum amount that could be paid.

C) The undiscounted probabilistic estimate of the amount to be paid.

D) The discounted probabilistic estimate of the amount to be paid.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

43

Company A Inc. owns a controlling interest in Company

B. Assuming that Company A is based in Canada, is this allowed? Explain.

B. which is located overseas. Company A and B are in entirely different lines of business. Company A wishes to file a request allowing it to not consolidate its financial statements with those of Company

B. Assuming that Company A is based in Canada, is this allowed? Explain.

B. which is located overseas. Company A and B are in entirely different lines of business. Company A wishes to file a request allowing it to not consolidate its financial statements with those of Company

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

44

A business combination involves a contingent consideration. It is considered 70% probable that a payment of $500,000 will become payable three years after the acquisition date. Using a 7% discount rate, what liability should be recorded for the contingent consideration on the acquisition date?

A) $285,704

B) $350,000

C) $408,149

D) $500,000

A) $285,704

B) $350,000

C) $408,149

D) $500,000

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

45

After the introduction of the Fair Value Enterprise (FVE) method in Canada, many companies opted to value the non-controlling interest in subsidiaries based on the fair value of the subsidiary's identifiable net assets at the acquisition date instead of valuing the non-controlling interest at its fair value. That is, they opted to use the Identifiable Net Assets (INA) method rather than the FVE method when preparing consolidated financial statements. What motivation might preparers of consolidated financial statements have that would cause them to have this preference?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

46

Keen Inc. and Lax Inc. had the following balance sheets on October 31, 2019:

Assuming that Keen Inc. purchases 80% of Lax Inc. for cash of $240,000 on November 1, 2019, prepare the consolidated balance sheet on the date of acquisition under the Fair Value Enterprise Method.

Assuming that Keen Inc. purchases 80% of Lax Inc. for cash of $240,000 on November 1, 2019, prepare the consolidated balance sheet on the date of acquisition under the Fair Value Enterprise Method. Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

47

Keen Inc and Lax Inc had the following balance sheets on October 31, 2019:

Assuming that Keen Purchases 100% of Lax for a consideration of $100,000 on September 1, 2019, and accounts for its investment using the cost method, prepare (under the Fair Value Enterprise Method):

a) the journal entry that Keen Inc. would make to record the acquisition;

b) the elimination entry necessary to produce consolidated balance sheet on the acquisition date.

Assuming that Keen Purchases 100% of Lax for a consideration of $100,000 on September 1, 2019, and accounts for its investment using the cost method, prepare (under the Fair Value Enterprise Method):a) the journal entry that Keen Inc. would make to record the acquisition;

b) the elimination entry necessary to produce consolidated balance sheet on the acquisition date.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

48

X Company Purchases a (100%) controlling interest in Y Company by issuing $2,000,000 worth of common shares. An agreement was drawn whereby X Company would pay 10% of any earnings in excess of $750,000 to Y's shareholders in the first year following the acquisition. On that date, X's shares had a market value of $80 per share.

Required:

a) Assuming that Y's net income was $950,000, prepare any journal entries (for company X) that you feel may be necessary to reflect Y's results under IFRS 3 Business Combinations. Assume that on the acquisition date no provision was made for the contingent consideration.

b) Assuming that the agreement called for Y's shareholders to be compensated with 1,250 shares for any decline in X's share price, what journal entries would be required under IFRS 3, if the market value of X's shares dropped to $64 within the year?

Required:

a) Assuming that Y's net income was $950,000, prepare any journal entries (for company X) that you feel may be necessary to reflect Y's results under IFRS 3 Business Combinations. Assume that on the acquisition date no provision was made for the contingent consideration.

b) Assuming that the agreement called for Y's shareholders to be compensated with 1,250 shares for any decline in X's share price, what journal entries would be required under IFRS 3, if the market value of X's shares dropped to $64 within the year?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

49

Keen Inc and Lax Inc had the following balance sheets on October 31, 2019:

Assuming that Keen Purchases 80% of Lax for a cash consideration of $240,000 on November 1, 2019, prepare (under the Fair Value Enterprise Method):

a) the journal entry that Keen Inc. would make to record the acquisition;

b) the elimination entry necessary to produce consolidated balance sheet on the acquisition date.

Assuming that Keen Purchases 80% of Lax for a cash consideration of $240,000 on November 1, 2019, prepare (under the Fair Value Enterprise Method):a) the journal entry that Keen Inc. would make to record the acquisition;

b) the elimination entry necessary to produce consolidated balance sheet on the acquisition date.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

50

Keen Inc. and Lax Inc. had the following balance sheets on October 31, 2019:

On November 1, 2019, Keen acquired 80% of Lax Inc. for cash consideration of $240,000. Assume that the following draft balance sheet was prepared by a co-worker on the date of acquisition. Assuming this balance sheet is devoid of technical errors, what can be concluded about the balance sheet below?

On November 1, 2019, Keen acquired 80% of Lax Inc. for cash consideration of $240,000. Assume that the following draft balance sheet was prepared by a co-worker on the date of acquisition. Assuming this balance sheet is devoid of technical errors, what can be concluded about the balance sheet below? Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

51

Discuss the disclosure requirements for long term investments including accounting policies and non-controlling interest (NCI).

Companies should disclose their policies with regard to long-term investments. The general presumptions regarding the factors that establish a control investment and noted that these presumptions could be overcome in certain situations.

IFRS 3 Business Combinations requires that a reporting entity describe the basis for its assessment and any significant assumptions or judgments when the reporting entity has concluded that:

Companies should disclose their policies with regard to long-term investments. The general presumptions regarding the factors that establish a control investment and noted that these presumptions could be overcome in certain situations.

IFRS 3 Business Combinations requires that a reporting entity describe the basis for its assessment and any significant assumptions or judgments when the reporting entity has concluded that:

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

52

If a business combination occurs and the consideration paid exceeds the fair value of the identifiable net assets of the subsidiary on the acquisition date and the parent acquires less than 100% of the outstanding common shares of the subsidiary, which consolidation method will result in the highest value for non-controlling interest on the acquisition date?

A) Proportionate consolidation method

B) Parent company method

C) Fair value enterprise method

D) Identifiable net assets method

A) Proportionate consolidation method

B) Parent company method

C) Fair value enterprise method

D) Identifiable net assets method

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

53

Jean and John Inc had the following balance sheets on August 31, 2019:

On August 31, 2019, Jean's date of acquisition, Jean Inc. purchased 90% of John Inc. for cash consideration of $400,000.

Assuming the above balance sheets were prepared immediately before the acquisition, prepare Jean Inc's consolidated balance sheet on the date of acquisition using the Fair Value Enterprise Method.

On August 31, 2019, Jean's date of acquisition, Jean Inc. purchased 90% of John Inc. for cash consideration of $400,000.Assuming the above balance sheets were prepared immediately before the acquisition, prepare Jean Inc's consolidated balance sheet on the date of acquisition using the Fair Value Enterprise Method.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

54

Major Corporation issues 1,000,000 common shares for all of the outstanding common shares of Minor Corporation on August 1, Year 1. The shares issued have a fair market value of $40.

In addition, the merger agreement provides that if the market price of Major's shares is below $60 two years from the date of the merger, Major will issue additional shares to the former shareholders of Minor Corporation in an amount that will compensate them for their loss of value.

Major predicts that there is a 25% probability that Major's shares will be trading at $59 per share and a 75% probability that they will be trading at greater than $60 per share two years from the date of the merger. Assume a discount rate of 7%.

Required:

Prepare the journal entry to record the issuance of the shares.

In addition, the merger agreement provides that if the market price of Major's shares is below $60 two years from the date of the merger, Major will issue additional shares to the former shareholders of Minor Corporation in an amount that will compensate them for their loss of value.

Major predicts that there is a 25% probability that Major's shares will be trading at $59 per share and a 75% probability that they will be trading at greater than $60 per share two years from the date of the merger. Assume a discount rate of 7%.

Required:

Prepare the journal entry to record the issuance of the shares.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

55

In an inflationary economy, under which consolidation method would total assets in the consolidated balance sheet at the acquisition date be greatest?

A) Proportionate consolidation method

B) Parent company method

C) Fair value enterprise method

D) Identifiable net assets method

A) Proportionate consolidation method

B) Parent company method

C) Fair value enterprise method

D) Identifiable net assets method

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

56

Keen Inc. and Lax Inc. had the following balance sheets on October 31, 2019:

Assuming that Keen Inc. purchases 100% of Lax Inc. for cash of $200,000 on November 1, 2019, prepare the consolidated balance sheet on the date of acquisition under the Fair Value Enterprise Method.

Assuming that Keen Inc. purchases 100% of Lax Inc. for cash of $200,000 on November 1, 2019, prepare the consolidated balance sheet on the date of acquisition under the Fair Value Enterprise Method. Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

57

Various methods have been proposed as solutions to preparing consolidated financial statements for non-wholly owned subsidiaries. Provide the methods and include your reasoning to support the method(s) that is/are being adopted under IFRS.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

58

A business combination involves a contingent consideration. It is considered 70% probable that a payment of $500,000 will become payable three years after the acquisition date. Using a 7% discount rate, how much interest expense should be recorded on the liability for the first year after acquisition?

A) $19,999

B) $24,500

C) $28,570

D) $35,000

A) $19,999

B) $24,500

C) $28,570

D) $35,000

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

59

Jean Inc and John Inc had the following balance sheets on August 31, 2019:

On August 31, 2019, Jean's date of acquisition, Jean Inc. purchased 90% of John Inc. for cash consideration of $400,000.

Assuming the above balance sheets were prepared immediately before the acquisition, prepare Jean Inc's consolidated balance sheet on the date of acquisition using the Proportionate Consolidation Method.

On August 31, 2019, Jean's date of acquisition, Jean Inc. purchased 90% of John Inc. for cash consideration of $400,000.Assuming the above balance sheets were prepared immediately before the acquisition, prepare Jean Inc's consolidated balance sheet on the date of acquisition using the Proportionate Consolidation Method.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

60

Why might the fair value of the non-controlling interest in a subsidiary on the date that it is acquired in a business combination not be proportionate to the price per share paid by the parent company to acquire control? How do the IFRS recognize this?

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 60 flashcards in this deck.