Deck 12: Accounting for Not-For-Profit and Public Sector Organizations

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

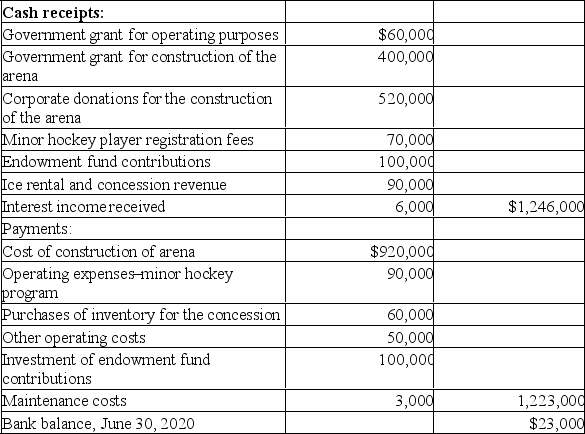

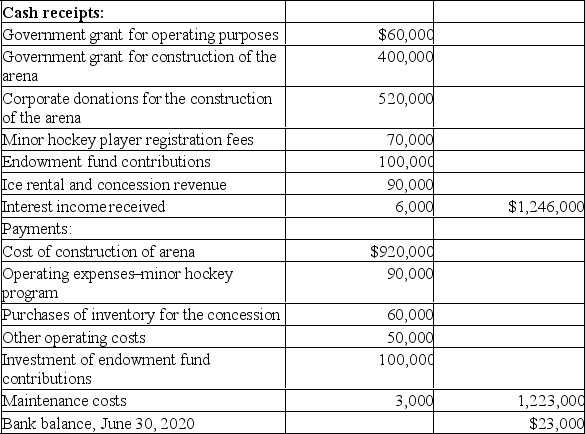

The Rift Valley Minor Hockey Association was established in the village of Rift Valley in early 2019. It was established to promote hockey in the village and surrounding territory. With the support of the provincial government, local business people and many individuals, the association raised sufficient funds to build an indoor hockey arena and also established an endowment fund to cover maintenance costs. The association is required by the provincial government to prepare financial statements in accordance with generally accepted accounting principles.

The board has decided that its year end will be June 30 and that capital assets will be capitalized and amortized over their expected useful lives. They have decided not to use the restricted fund method of accounting but will account for restricted donations using the deferral method of accounting for contributions. The first set of financial statements will cover the eighteen month period from the establishment of the association to June 30, 2020.

From the bank statements, you determine the following:

Additional information:

Additional information:

1. The new arena was completed and officially opened on Canada Day (July 1) of 2019. It has an estimated forty year life with no residual value.

2. A long-term resident of Rift Valley donated the land upon which the arena was constructed. The land was valued at $120,000 and the association issued a receipt in that amount. Another resident donated ice-making and ice-cleaning equipment to the association. The equipment has an estimated useful life of six years and no residual value and was estimated to have a value of $66,000 when donated.

3. The endowment contribution was received at the opening celebration and was invested for one year at 5% interest. The terms of the endowment were that the income earned from its investment could be used only for maintenance costs for the arena. $3,000 of such costs were incurred and paid for in May 2020. (The other $1,000 in interest income was earned on the balances in the bank account.)

4. The government had agreed to provide funding of $10,000 per month for the eight months of the minor hockey season (September 1 to April 30 each year). The amount was payable at $7,500 per month during the season and the final $20,000 upon submission of the annual financial statements to the government.

5. Registration fees for minor hockey players cover the season from September to April. $10,000 of the fees received were payments in advance for the 2020-2021 season.

6. An inventory count was taken at the concession stand at the end of June 2020 and the inventory on hand was valued at $6,000 (lower of cost or realizable value). The concession stand sold snacks and drinks during minor hockey games and other events.

7. At June 30, 2020, unpaid invoices were $3,000 for concession purchases, $2,000 for hockey clinics held and $1,000 for miscellaneous other costs.

Prepare a statement of financial position for the Rift Valley Minor Hockey Association as at June 30, 2020.

The board has decided that its year end will be June 30 and that capital assets will be capitalized and amortized over their expected useful lives. They have decided not to use the restricted fund method of accounting but will account for restricted donations using the deferral method of accounting for contributions. The first set of financial statements will cover the eighteen month period from the establishment of the association to June 30, 2020.

From the bank statements, you determine the following:

Additional information:1. The new arena was completed and officially opened on Canada Day (July 1) of 2019. It has an estimated forty year life with no residual value.

2. A long-term resident of Rift Valley donated the land upon which the arena was constructed. The land was valued at $120,000 and the association issued a receipt in that amount. Another resident donated ice-making and ice-cleaning equipment to the association. The equipment has an estimated useful life of six years and no residual value and was estimated to have a value of $66,000 when donated.

3. The endowment contribution was received at the opening celebration and was invested for one year at 5% interest. The terms of the endowment were that the income earned from its investment could be used only for maintenance costs for the arena. $3,000 of such costs were incurred and paid for in May 2020. (The other $1,000 in interest income was earned on the balances in the bank account.)

4. The government had agreed to provide funding of $10,000 per month for the eight months of the minor hockey season (September 1 to April 30 each year). The amount was payable at $7,500 per month during the season and the final $20,000 upon submission of the annual financial statements to the government.

5. Registration fees for minor hockey players cover the season from September to April. $10,000 of the fees received were payments in advance for the 2020-2021 season.

6. An inventory count was taken at the concession stand at the end of June 2020 and the inventory on hand was valued at $6,000 (lower of cost or realizable value). The concession stand sold snacks and drinks during minor hockey games and other events.

7. At June 30, 2020, unpaid invoices were $3,000 for concession purchases, $2,000 for hockey clinics held and $1,000 for miscellaneous other costs.

Prepare a statement of financial position for the Rift Valley Minor Hockey Association as at June 30, 2020.

Question

Question

Question

Question

Question

Question

Question

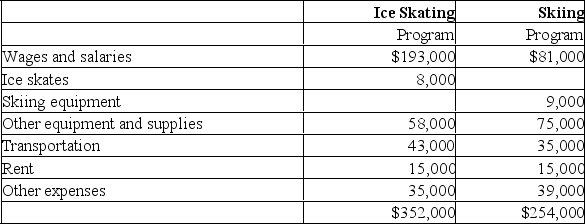

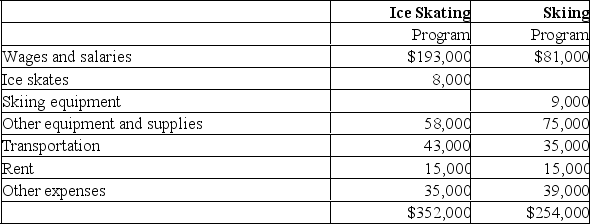

On January 1, 2020, some residents of the community of Kiterup,B.C., formed the Kiterup Winter Sports Association (KWSA) which was organized as a not-for-profit organization which has as its purposes encouraging participation in outdoor winter sports. In its first year, the board decided to restrict its activities to ice skating and skiing.

Initial funding was provided by a wealthy individual who made an endowment contribution of $200,000 which was invested in bonds and generated income during the year of $8,000. The donor placed no restrictions on the use of the income produced by the investment of the endowment contribution which were to be divided evenly between all programs undertaken by the Association.

During the year donations of $750,000 were received and a further $150,000 of pledges was outstanding of which the board estimated $130,000 would be collected. It was agreed that such donations, all of which were unrestricted, would be divided evenly between the skating and skiing programs. As a practical matter, donations not yet received at year-end were considered to be restricted for use in the following year. A special fund drive was undertaken to raise money to provide skates to needy youngsters and skiing equipment to needy senior citizens. During the year $25,000 was received in contributions for skates and $15,000 for contributions towards purchasing skis.

During the year ended December 31, 2020, the organization incurred the following costs.

At December 31, 2020, the only outstanding payables were for $30,000 relating to the skiing program (the costs are included in the table above). The ice skates and skiing equipment were paid for out of the funds raised by the special fund drive and were expensed as acquired.

At December 31, 2020, the only outstanding payables were for $30,000 relating to the skiing program (the costs are included in the table above). The ice skates and skiing equipment were paid for out of the funds raised by the special fund drive and were expensed as acquired.

KWSA does not use fund accounting but uses the deferral method to account for restricted donations and uses programmatic reporting to report the results of its activities.

Prepare a statement of financial position of the Kiterup Winter Sports Association as at December 31, 2020. Statements for the individual programs are not required.

Initial funding was provided by a wealthy individual who made an endowment contribution of $200,000 which was invested in bonds and generated income during the year of $8,000. The donor placed no restrictions on the use of the income produced by the investment of the endowment contribution which were to be divided evenly between all programs undertaken by the Association.

During the year donations of $750,000 were received and a further $150,000 of pledges was outstanding of which the board estimated $130,000 would be collected. It was agreed that such donations, all of which were unrestricted, would be divided evenly between the skating and skiing programs. As a practical matter, donations not yet received at year-end were considered to be restricted for use in the following year. A special fund drive was undertaken to raise money to provide skates to needy youngsters and skiing equipment to needy senior citizens. During the year $25,000 was received in contributions for skates and $15,000 for contributions towards purchasing skis.

During the year ended December 31, 2020, the organization incurred the following costs.

At December 31, 2020, the only outstanding payables were for $30,000 relating to the skiing program (the costs are included in the table above). The ice skates and skiing equipment were paid for out of the funds raised by the special fund drive and were expensed as acquired.KWSA does not use fund accounting but uses the deferral method to account for restricted donations and uses programmatic reporting to report the results of its activities.

Prepare a statement of financial position of the Kiterup Winter Sports Association as at December 31, 2020. Statements for the individual programs are not required.

Question

Question

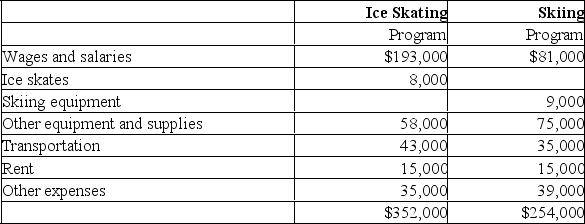

On January 1, 2020, some residents of the community of Kiterup,B.C., formed the Kiterup Winter Sports Association (KWSA) which was organized as a not-for-profit organization which has as its purposes encouraging participation in outdoor winter sports. In its first year, the board decided to restrict its activities to ice skating and skiing.

Initial funding was provided by a wealthy individual who made an endowment contribution of $200,000 which was invested in bonds and generated income during the year of $8,000. The donor placed no restrictions on the use of the income produced by the investment of the endowment contribution which were to be divided evenly between all programs undertaken by the Association.

During the year donations of $750,000 were received and a further $150,000 of pledges was outstanding of which the board estimated $130,000 would be collected. It was agreed that such donations, all of which were unrestricted, would be divided evenly between the skating and skiing programs. As a practical matter, donations not yet received at year-end were considered to be restricted for use in the following year. A special fund drive was undertaken to raise money to provide skates to needy youngsters and skiing equipment to needy senior citizens. During the year $25,000 was received in contributions for skates and $15,000 for contributions towards purchasing skis.

During the year ended December 31, 2020, the organization incurred the following costs.

At December 31, 2020, the only outstanding payables were for $30,000 relating to the skiing program (the costs are included in the table above). The ice skates and skiing equipment were paid for out of the funds raised by the special fund drive and were expensed as acquired.

At December 31, 2020, the only outstanding payables were for $30,000 relating to the skiing program (the costs are included in the table above). The ice skates and skiing equipment were paid for out of the funds raised by the special fund drive and were expensed as acquired.

KWSA does not use fund accounting but uses the deferral method to account for restricted donations and uses programmatic reporting to report the results of its activities.

Prepare journal entries to record the transactions of the Kiterup Winter Sports Association for the year ended December 31, 2020. Closing entries are not required.

Initial funding was provided by a wealthy individual who made an endowment contribution of $200,000 which was invested in bonds and generated income during the year of $8,000. The donor placed no restrictions on the use of the income produced by the investment of the endowment contribution which were to be divided evenly between all programs undertaken by the Association.

During the year donations of $750,000 were received and a further $150,000 of pledges was outstanding of which the board estimated $130,000 would be collected. It was agreed that such donations, all of which were unrestricted, would be divided evenly between the skating and skiing programs. As a practical matter, donations not yet received at year-end were considered to be restricted for use in the following year. A special fund drive was undertaken to raise money to provide skates to needy youngsters and skiing equipment to needy senior citizens. During the year $25,000 was received in contributions for skates and $15,000 for contributions towards purchasing skis.

During the year ended December 31, 2020, the organization incurred the following costs.

At December 31, 2020, the only outstanding payables were for $30,000 relating to the skiing program (the costs are included in the table above). The ice skates and skiing equipment were paid for out of the funds raised by the special fund drive and were expensed as acquired.KWSA does not use fund accounting but uses the deferral method to account for restricted donations and uses programmatic reporting to report the results of its activities.

Prepare journal entries to record the transactions of the Kiterup Winter Sports Association for the year ended December 31, 2020. Closing entries are not required.

Question

Question

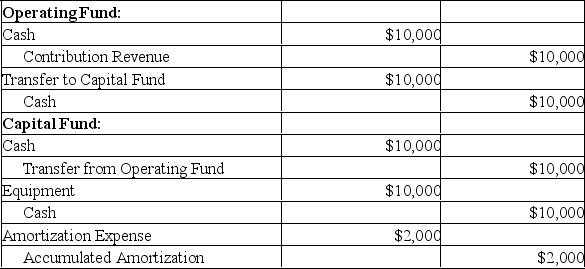

The following are selected transactions for HELP-ON-US (HOU), an NFPO for 2020. HOU uses the restricted fund method of accounting for contributions. HOU has an operating fund, a capital fund and an endowment fund.

On January 1, the organization purchased fixed assets at a cost of $10,000. The assets were estimated to have a useful life of 5 years with no residual value. Straight-line amortization is used.

Assuming that the assets were purchased from unrestricted contribution that was made on January 1, 2020, prepare the required journal entries for 2020, indicating the fund or funds to be used.

On January 1, the organization purchased fixed assets at a cost of $10,000. The assets were estimated to have a useful life of 5 years with no residual value. Straight-line amortization is used.

Assuming that the assets were purchased from unrestricted contribution that was made on January 1, 2020, prepare the required journal entries for 2020, indicating the fund or funds to be used.

Question

Question

Question

The Rift Valley Minor Hockey Association was established in the village of Rift Valley in early 2019. It was established to promote hockey in the village and surrounding territory. With the support of the provincial government, local business people and many individuals, the association raised sufficient funds to build an indoor hockey arena and also established an endowment fund to cover maintenance costs. The association is required by the provincial government to prepare financial statements in accordance with generally accepted accounting principles.

The board has decided that its year end will be June 30 and that capital assets will be capitalized and amortized over their expected useful lives. They have decided not to use the restricted fund method of accounting but will account for restricted donations using the deferral method of accounting for contributions. The first set of financial statements will cover the eighteen month period from the establishment of the association to June 30, 2020.

From the bank statements, you determine the following:

Additional information:

Additional information:

1. The new arena was completed and officially opened on Canada Day (July 1) of 2019. It has an estimated forty year life with no residual value.

2. A long-term resident of Rift Valley donated the land upon which the arena was constructed. The land was valued at $120,000 and the association issued a receipt in that amount. Another resident donated ice-making and ice-cleaning equipment to the association. The equipment has an estimated useful life of six years and no residual value and was estimated to have a value of $66,000 when donated.

3. The endowment contribution was received at the opening celebration and was invested for one year at 5% interest. The terms of the endowment were that the income earned from its investment could be used only for maintenance costs for the arena. $3,000 of such costs were incurred and paid for in May 2020. (The other $1,000 in interest income was earned on the balances in the bank account.)

4. The government had agreed to provide funding of $10,000 per month for the eight months of the minor hockey season (September 1 to April 30 each year). The amount was payable at $7,500 per month during the season and the final $20,000 upon submission of the annual financial statements to the government.

5. Registration fees for minor hockey players cover the season from September to April. $10,000 of the fees received were payments in advance for the 2020-2021 season.

6. An inventory count was taken at the concession stand at the end of June 2020 and the inventory on hand was valued at $6,000 (lower of cost or realizable value). The concession stand sold snacks and drinks during minor hockey games and other events.

7. At June 30, 2020, unpaid invoices were $3,000 for concession purchases, $2,000 for hockey clinics held and $1,000 for miscellaneous other costs.

Prepare a statement of operations for the Rift Valley Minor Hockey Association for the eighteen month period ended June 30, 2020.

The board has decided that its year end will be June 30 and that capital assets will be capitalized and amortized over their expected useful lives. They have decided not to use the restricted fund method of accounting but will account for restricted donations using the deferral method of accounting for contributions. The first set of financial statements will cover the eighteen month period from the establishment of the association to June 30, 2020.

From the bank statements, you determine the following:

Additional information:1. The new arena was completed and officially opened on Canada Day (July 1) of 2019. It has an estimated forty year life with no residual value.

2. A long-term resident of Rift Valley donated the land upon which the arena was constructed. The land was valued at $120,000 and the association issued a receipt in that amount. Another resident donated ice-making and ice-cleaning equipment to the association. The equipment has an estimated useful life of six years and no residual value and was estimated to have a value of $66,000 when donated.

3. The endowment contribution was received at the opening celebration and was invested for one year at 5% interest. The terms of the endowment were that the income earned from its investment could be used only for maintenance costs for the arena. $3,000 of such costs were incurred and paid for in May 2020. (The other $1,000 in interest income was earned on the balances in the bank account.)

4. The government had agreed to provide funding of $10,000 per month for the eight months of the minor hockey season (September 1 to April 30 each year). The amount was payable at $7,500 per month during the season and the final $20,000 upon submission of the annual financial statements to the government.

5. Registration fees for minor hockey players cover the season from September to April. $10,000 of the fees received were payments in advance for the 2020-2021 season.

6. An inventory count was taken at the concession stand at the end of June 2020 and the inventory on hand was valued at $6,000 (lower of cost or realizable value). The concession stand sold snacks and drinks during minor hockey games and other events.

7. At June 30, 2020, unpaid invoices were $3,000 for concession purchases, $2,000 for hockey clinics held and $1,000 for miscellaneous other costs.

Prepare a statement of operations for the Rift Valley Minor Hockey Association for the eighteen month period ended June 30, 2020.

Question

Question

On January 1, 2020, some residents of the community of Kiterup,B.C., formed the Kiterup Winter Sports Association (KWSA) which was organized as a not-for-profit organization which has as its purposes encouraging participation in outdoor winter sports. In its first year, the board decided to restrict its activities to ice skating and skiing.

Initial funding was provided by a wealthy individual who made an endowment contribution of $200,000 which was invested in bonds and generated income during the year of $8,000. The donor placed no restrictions on the use of the income produced by the investment of the endowment contribution which were to be divided evenly between all programs undertaken by the Association.

During the year donations of $750,000 were received and a further $150,000 of pledges was outstanding of which the board estimated $130,000 would be collected. It was agreed that such donations, all of which were unrestricted, would be divided evenly between the skating and skiing programs. As a practical matter, donations not yet received at year-end were considered to be restricted for use in the following year. A special fund drive was undertaken to raise money to provide skates to needy youngsters and skiing equipment to needy senior citizens. During the year $25,000 was received in contributions for skates and $15,000 for contributions towards purchasing skis.

During the year ended December 31, 2020, the organization incurred the following costs.

At December 31, 2020, the only outstanding payables were for $30,000 relating to the skiing program (the costs are included in the table above). The ice skates and skiing equipment were paid for out of the funds raised by the special fund drive and were expensed as acquired.

At December 31, 2020, the only outstanding payables were for $30,000 relating to the skiing program (the costs are included in the table above). The ice skates and skiing equipment were paid for out of the funds raised by the special fund drive and were expensed as acquired.

KWSA does not use fund accounting but uses the deferral method to account for restricted donations and uses programmatic reporting to report the results of its activities.

Prepare a statement of operations for the Kiterup Winter Sports Association for the year ended December 31, 2020.

Initial funding was provided by a wealthy individual who made an endowment contribution of $200,000 which was invested in bonds and generated income during the year of $8,000. The donor placed no restrictions on the use of the income produced by the investment of the endowment contribution which were to be divided evenly between all programs undertaken by the Association.

During the year donations of $750,000 were received and a further $150,000 of pledges was outstanding of which the board estimated $130,000 would be collected. It was agreed that such donations, all of which were unrestricted, would be divided evenly between the skating and skiing programs. As a practical matter, donations not yet received at year-end were considered to be restricted for use in the following year. A special fund drive was undertaken to raise money to provide skates to needy youngsters and skiing equipment to needy senior citizens. During the year $25,000 was received in contributions for skates and $15,000 for contributions towards purchasing skis.

During the year ended December 31, 2020, the organization incurred the following costs.

At December 31, 2020, the only outstanding payables were for $30,000 relating to the skiing program (the costs are included in the table above). The ice skates and skiing equipment were paid for out of the funds raised by the special fund drive and were expensed as acquired.KWSA does not use fund accounting but uses the deferral method to account for restricted donations and uses programmatic reporting to report the results of its activities.

Prepare a statement of operations for the Kiterup Winter Sports Association for the year ended December 31, 2020.

Question

XYZ is a local charity that commenced operations on January 1, 2020. XYZ uses the restricted fund method of accounting for contributions. XYZ has a general fund, a capital fund and an endowment fund.

For the following partial data provided, prepare the journal entry to record that transaction. Specify which fund or funds must be used to record the entry.

a) Revenue deferred earlier in the year in the amount of $5,000 was recognized.

b) Pledges receivable in the amount of $10,000 were collected in full.

c) Accounts payable and wages payable amounting to $10,000 and $5,000 were paid.

d) Government grants amounted to $50,000, half of which was received. The balance is expected by late 2021. The grants may be applied to any of the organization's programs.

e) Total Wage costs amounted to $60,000 which breaks down as follows:

25% of these expenses are still payable at the end of 2020.

25% of these expenses are still payable at the end of 2020.

f) A wealthy local businessman donated $100,000 to be held in endowment, with the interest earned to be unrestricted.

g) The investments in an endowment fund earned interest in the amount $3,000.

h) Amortization expense for the year amounted to $10,000.

For the following partial data provided, prepare the journal entry to record that transaction. Specify which fund or funds must be used to record the entry.

a) Revenue deferred earlier in the year in the amount of $5,000 was recognized.

b) Pledges receivable in the amount of $10,000 were collected in full.

c) Accounts payable and wages payable amounting to $10,000 and $5,000 were paid.

d) Government grants amounted to $50,000, half of which was received. The balance is expected by late 2021. The grants may be applied to any of the organization's programs.

e) Total Wage costs amounted to $60,000 which breaks down as follows:

25% of these expenses are still payable at the end of 2020.f) A wealthy local businessman donated $100,000 to be held in endowment, with the interest earned to be unrestricted.

g) The investments in an endowment fund earned interest in the amount $3,000.

h) Amortization expense for the year amounted to $10,000.

Question

A not-for-profit organization received unrestricted pledges of $200,000, and believes based on past experience that 95% of them will be paid. What entry should be made to record the pledges?

A.

B.

C.

D.

A.

B.

C.

D.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/60

Play

Full screen (f)

Deck 12: Accounting for Not-For-Profit and Public Sector Organizations

1

Section 4433 contains a compromise provision applicable to small NFPOs. Which of the following statements pertaining to a small NFPO is false?

A) A small NFPOs average of annual revenues recognized in the statement of operations for the current and preceding period is less than $500,000.

B) The small NFPO is exempt from having to record donated capital assets at fair value.

C) A small NFPO is exempt from having to capitalize and amortize tangible capital assets.

D) A small NFPO can choose to expense a capital asset when it is acquired.

A) A small NFPOs average of annual revenues recognized in the statement of operations for the current and preceding period is less than $500,000.

B) The small NFPO is exempt from having to record donated capital assets at fair value.

C) A small NFPO is exempt from having to capitalize and amortize tangible capital assets.

D) A small NFPO can choose to expense a capital asset when it is acquired.

B

2

Do-Good Inc. is a not-for-profit organization that was formed on January 1, 2020. Do-Good has a December 31 year end. It has an accounting policy of capitalizing and amortizing its capital assets. On April 1, 2020, Do-Good purchased equipment costing $8,000. The equipment is estimated to have a useful life of 4 years, with no residual value at that time. This transaction was the only transaction that took place to date. The equipment was purchased from an unrestricted contribution of $8,000.

What would be the balance in the General Fund on December 31, 2020?

A) $0

B) $6,000

C) $6,400

D) $8,000

What would be the balance in the General Fund on December 31, 2020?

A) $0

B) $6,000

C) $6,400

D) $8,000

A

3

Which of the following statements is correct?

A) Unrestricted resources can be used for any purposes by a not-for-profit organization.

B) Unrestricted resources can be used for any purposes that are consistent with the goals and objectives of the not-for-profit organization.

C) Restricted resources can only be used in the case of a serious financial deficit situation.

D) Both restricted and unrestricted funds must be used in accordance with the wishes of the contributor.

A) Unrestricted resources can be used for any purposes by a not-for-profit organization.

B) Unrestricted resources can be used for any purposes that are consistent with the goals and objectives of the not-for-profit organization.

C) Restricted resources can only be used in the case of a serious financial deficit situation.

D) Both restricted and unrestricted funds must be used in accordance with the wishes of the contributor.

B

4

Collections are works of art that have been excluded from the definition of capital assets. Which of the following statements is NOT a criterion which must be met before works of art qualify as collections under Canadian accounting standards?

A) It must be possible to establish a useful life for the works and an appropriate amortization period.

B) They are held for public exhibition, education, or research.

C) They are protected, cared for, and preserved.

D) They are subject to organizational policies that require any proceeds from their sale to be used to acquire other items for the collection, or for the direct care of the existing collection.

A) It must be possible to establish a useful life for the works and an appropriate amortization period.

B) They are held for public exhibition, education, or research.

C) They are protected, cared for, and preserved.

D) They are subject to organizational policies that require any proceeds from their sale to be used to acquire other items for the collection, or for the direct care of the existing collection.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

5

Section 4433 of the CPA Canada Handbook contains an exemption from capitalizing and amortizing all fixed assets for an NFPO that has revenues below $500,000. If the NFPO's revenues subsequently increase to over $500,000 over a two year period, which of the following statements is TRUE?

A) The NFPO ceases to be a small NFPO but it is only required to capitalize and amortize if the increase in revenue is sustained for a period of two years.

B) The NFPO ceases to be a small NFPO and it must capitalize and amortize on a retroactive basis to allow for comparative financial statements.

C) The NFPO ceases to be a small NFPO but it does not need to adopt the policy of capitalizing and amortizing if that policy does not meet the needs of the financial statement users.

D) The NFPO ceases to be a small NFPO and must capitalize and amortize on a prospective basis.

A) The NFPO ceases to be a small NFPO but it is only required to capitalize and amortize if the increase in revenue is sustained for a period of two years.

B) The NFPO ceases to be a small NFPO and it must capitalize and amortize on a retroactive basis to allow for comparative financial statements.

C) The NFPO ceases to be a small NFPO but it does not need to adopt the policy of capitalizing and amortizing if that policy does not meet the needs of the financial statement users.

D) The NFPO ceases to be a small NFPO and must capitalize and amortize on a prospective basis.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

6

Do-Good Inc. is a not-for-profit organization that was formed on January 1, 2020. Do-Good has a December 31 year end. It has an accounting policy of capitalizing and amortizing its capital assets. On April 1, 2020, Do-Good purchased equipment costing $8,000. The equipment is estimated to have a useful life of 4 years, with no residual value at that time. This transaction was the only transaction that took place to date. The equipment was purchased from a restricted fund contribution of $8,400.

What would be the balance in the Capital Fund on December 31, 2020?

A) ($1,600)

B) $400

C) $4,400

D) $6,900

What would be the balance in the Capital Fund on December 31, 2020?

A) ($1,600)

B) $400

C) $4,400

D) $6,900

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following financial statements are NOT required by not-for-profit organizations for external reporting purposes?

A) A Statement of Financial Position.

B) A Statement of Changes in Members' Equity.

C) A Statement of Cash Flows.

D) A Statement of Operations.

A) A Statement of Financial Position.

B) A Statement of Changes in Members' Equity.

C) A Statement of Cash Flows.

D) A Statement of Operations.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

8

The maximum amortization period specified by Section 4433 with respect to capital assets is:

A) 5 years.

B) 10 years.

C) 20 years.

D) No maximum amortization period is specified.

A) 5 years.

B) 10 years.

C) 20 years.

D) No maximum amortization period is specified.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following is NOT an acceptable way of reporting for a not-for-profit entity over which an organization has control?

A) By consolidating the controlled organization in its financial statements.

B) By providing the disclosure set out in paragraph 4450.22 of the Handbook.

C) If the controlled organization is one of a large number of individually immaterial organizations, by adhering to the disclosure requirements set out in paragraph 4450.26 of the CPA Canada Handbook.

D) By using the equity method.

A) By consolidating the controlled organization in its financial statements.

B) By providing the disclosure set out in paragraph 4450.22 of the Handbook.

C) If the controlled organization is one of a large number of individually immaterial organizations, by adhering to the disclosure requirements set out in paragraph 4450.26 of the CPA Canada Handbook.

D) By using the equity method.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

10

Do-Good Inc. is a not-for-profit organization that was formed on January 1, 2020. Do-Good has a December 31 year end. It has an accounting policy of capitalizing and amortizing its capital assets. On April 1, 2020, Do-Good purchased equipment costing $8,000. The equipment is estimated to have a useful life of 4 years, with no residual value at that time. This transaction was the only transaction that took place to date. The equipment was purchased from an unrestricted contribution of $8,000.

What would be the balance in the Capital Fund on December 31, 2020?

A) $8,000

B) $6,000

C) $6,500

D) $8,400

What would be the balance in the Capital Fund on December 31, 2020?

A) $8,000

B) $6,000

C) $6,500

D) $8,400

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

11

Do-Good Inc. is a not-for-profit organization that was formed on January 1, 2020. Do-Good has a December 31 year end. It has an accounting policy of capitalizing and amortizing its capital assets. On April 1, 2020, Do-Good purchased equipment costing $8,000. The equipment is estimated to have a useful life of 4 years, with no residual value at that time. This transaction was the only transaction that took place to date. The equipment was purchased from an unrestricted contribution of $8,000.

In which fund would the purchase of the asset be recorded?

A) The general fund

B) The operating fund

C) The capital fund

D) The endowment fund

In which fund would the purchase of the asset be recorded?

A) The general fund

B) The operating fund

C) The capital fund

D) The endowment fund

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

12

When is the earliest a bequest can be recorded?

A) When the person making the bequests dies.

B) When the person making the bequest includes the amount of the donation in his or her will.

C) When the beneficiaries of the estate decide to pay out the bequest.

D) When the will has been probated and the time for appeal has passed.

A) When the person making the bequests dies.

B) When the person making the bequest includes the amount of the donation in his or her will.

C) When the beneficiaries of the estate decide to pay out the bequest.

D) When the will has been probated and the time for appeal has passed.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following statements is correct?

A) Endowments are donations that are received with the provision that it will be invested and only the investment income may be spent by the organization.

B) Endowments are unrestricted donations which can be used for any purposes that are consistent with the goals and objectives of the not-for-profit organization.

C) Endowments are provided as donations which only allow a not-for-profit organization to invest in other not-for-profit organizations only.

D) Endowments may be restricted and unrestricted funds which must be used in accordance with the wishes of the contributor and only available during the life of the donor.

A) Endowments are donations that are received with the provision that it will be invested and only the investment income may be spent by the organization.

B) Endowments are unrestricted donations which can be used for any purposes that are consistent with the goals and objectives of the not-for-profit organization.

C) Endowments are provided as donations which only allow a not-for-profit organization to invest in other not-for-profit organizations only.

D) Endowments may be restricted and unrestricted funds which must be used in accordance with the wishes of the contributor and only available during the life of the donor.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following statements is NOT correct?

A) A contribution receivable should be recognized as an asset when the amount can be reasonably estimated and the ultimate collection is reasonably assured.

B) A contribution receivable should be recognized as an asset when the amount can be reasonably estimated or the ultimate collection is reasonably assured.

C) Contribution revenue is a type of revenue where the contributor receives nothing directly in return for his or her contribution.

D) Government grants typically qualify as a contribution.

A) A contribution receivable should be recognized as an asset when the amount can be reasonably estimated and the ultimate collection is reasonably assured.

B) A contribution receivable should be recognized as an asset when the amount can be reasonably estimated or the ultimate collection is reasonably assured.

C) Contribution revenue is a type of revenue where the contributor receives nothing directly in return for his or her contribution.

D) Government grants typically qualify as a contribution.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

15

How would the not-for-profit organization report each controlled profit-oriented enterprise?

A) It is not required to report its interest in profit-oriented subsidiaries.

B) By disclosure in the notes to the financial statements of the not-for-profit organization.

C) By consolidating the controlled enterprise into its own financial statements or by using the equity method and disclosing additional financial information.

D) By using the cost method together with appropriate note disclosure.

A) It is not required to report its interest in profit-oriented subsidiaries.

B) By disclosure in the notes to the financial statements of the not-for-profit organization.

C) By consolidating the controlled enterprise into its own financial statements or by using the equity method and disclosing additional financial information.

D) By using the cost method together with appropriate note disclosure.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

16

How may a not-for-profit organization account for a portfolio (i.e. non-strategic) investment it has made in a profit-oriented entity?

A) By using fair value or the cost method

B) By using the equity method

C) By using proportionate consolidation

D) By consolidating the results of the profit-seeking entity with its own

A) By using fair value or the cost method

B) By using the equity method

C) By using proportionate consolidation

D) By consolidating the results of the profit-seeking entity with its own

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

17

Do-Good Inc. is a not-for-profit organization that was formed on January 1, 2020. Do-Good has a December 31 year end. It has an accounting policy of capitalizing and amortizing its capital assets. On April 1, 2020, Do-Good purchased equipment costing $8,000. The equipment is estimated to have a useful life of 4 years, with no residual value at that time. This transaction was the only transaction that took place to date. The equipment was purchased from a restricted fund contribution of $8,400.

What would be the carrying value of the equipment on December 31, 2020?

A) $6,500

B) $6,000

C) $8,000

D) $8,400

What would be the carrying value of the equipment on December 31, 2020?

A) $6,500

B) $6,000

C) $8,000

D) $8,400

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

18

Do-Good Inc. is a not-for-profit organization that was formed on January 1, 2020. Do-Good has a December 31 year end. It has an accounting policy of capitalizing and amortizing its capital assets. On April 1, 2020, Do-Good purchased equipment costing $8,000. The equipment is estimated to have a useful life of 4 years, with no residual value at that time. This transaction was the only transaction that took place to date. The equipment was purchased from a restricted fund contribution of $8,400. In which fund would the purchase and amortization of the asset be recorded?

A) The General Fund

B) The Operating Fund

C) The Capital Fund

D) The Endowment Fund

A) The General Fund

B) The Operating Fund

C) The Capital Fund

D) The Endowment Fund

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

19

Do-Good Inc. is a not-for-profit organization that was formed on January 1, 2020. Do-Good has a December 31 year end. It has an accounting policy of capitalizing and amortizing its capital assets. On April 1, 2020, Do-Good purchased equipment costing $8,000. The equipment is estimated to have a useful life of 4 years, with no residual value at that time. This transaction was the only transaction that took place to date. The equipment was purchased from an unrestricted contribution of $8,000.

In which fund would the receipt of the unrestricted contribution be recorded?

A) The general fund

B) The endowment fund

C) The capital fund

D) The encumbrance fund

In which fund would the receipt of the unrestricted contribution be recorded?

A) The general fund

B) The endowment fund

C) The capital fund

D) The encumbrance fund

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

20

For a small NFPO to qualify for the exemption provided for in Section 4433, these organizations must disclose all of the following EXCEPT:

A) Accounting policy for capital assets.

B) Information about capital assets not shown in the balance sheet.

C) The amount expensed in the current period if their policy is to expense capital assets when acquired.

D) An appraised listing of the organization's capital assets, showing book values and appraised market values.

A) Accounting policy for capital assets.

B) Information about capital assets not shown in the balance sheet.

C) The amount expensed in the current period if their policy is to expense capital assets when acquired.

D) An appraised listing of the organization's capital assets, showing book values and appraised market values.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following is NOT a requirement for a not-for-profit organization to record donated materials and services?

A) The fair value of the donation can be determined.

B) The organization uses the deferral method of accounting for contributions.

C) The materials or services would normally have been used in the organization's operations.

D) The not-for-profit organization would have purchased the goods or services if they had not been donated.

A) The fair value of the donation can be determined.

B) The organization uses the deferral method of accounting for contributions.

C) The materials or services would normally have been used in the organization's operations.

D) The not-for-profit organization would have purchased the goods or services if they had not been donated.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

22

NFPOs receive different types of contributions. Which of the following is a contribution with a restriction that the contribution cannot be spent, but must be maintained permanently?

A) Unrestricted contribution

B) Endowment contribution

C) Restricted contribution

D) Operating contribution

A) Unrestricted contribution

B) Endowment contribution

C) Restricted contribution

D) Operating contribution

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

23

A not-for-profit organization receives a restricted contribution of $20,000 to be used for a specific project. During the current year, $14,000 is spent toward the project with the balance to be spent next year. How much donation revenue should the not-for-profit organization recognize in the current year, if the organization uses the restricted fund method for reporting and had a fund for this project?

A) $20,000

B) $6,000

C) $14,000

D) Nil

A) $20,000

B) $6,000

C) $14,000

D) Nil

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following is NOT among the choices available to a not-for-profit organization with two-year average annual revenues of less than $500,000?

A) Capitalize and amortize capital assets.

B) Capitalize and not amortize capital assets.

C) Expense capital assets when acquired.

D) Make no entries when capital assets are acquired.

A) Capitalize and amortize capital assets.

B) Capitalize and not amortize capital assets.

C) Expense capital assets when acquired.

D) Make no entries when capital assets are acquired.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

25

If a not-for-profit organization uses the restricted fund method of reporting and has a capital fund, how should a donation of cash restricted to the purchase of land be reported?

A) As revenue in the general fund.

B) As revenue in the capital fund.

C) As a direct increase in net assets in the general fund.

D) As a direct increase in net assets in the capital fund.

A) As revenue in the general fund.

B) As revenue in the capital fund.

C) As a direct increase in net assets in the general fund.

D) As a direct increase in net assets in the capital fund.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

26

If a not-for-profit organization uses the restricted fund method of reporting and has an endowment fund, how should an endowment contribution be reported?

A) As revenue in the general fund.

B) As revenue in the endowment fund.

C) As a direct increase in net assets in the general fund.

D) As a direct increase in net assets in the endowment fund.

A) As revenue in the general fund.

B) As revenue in the endowment fund.

C) As a direct increase in net assets in the general fund.

D) As a direct increase in net assets in the endowment fund.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

27

If a not-for-profit organization has revenues in excess of $500,000, how must it report its capital assets?

A) All asset purchases must be immediately and entirely expensed.

B) All capital assets must be capitalized and amortized.

C) All capital assets must be capitalized but not amortized.

D) All capital assets must be disclosed in a note to the financial statements.

A) All asset purchases must be immediately and entirely expensed.

B) All capital assets must be capitalized and amortized.

C) All capital assets must be capitalized but not amortized.

D) All capital assets must be disclosed in a note to the financial statements.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

28

A not-for-profit organization receives a restricted contribution of $20,000 to be used for a specific project. During the current year, $14,000 is spent toward the project with the balance to be spent next year. What should be the balance in the deferred contribution account at the end of the year, if the organization uses the deferred contribution method of reporting?

A) $20,000

B) $6,000

C) $14,000

D) Nil

A) $20,000

B) $6,000

C) $14,000

D) Nil

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

29

A not-for-profit organization receives a restricted contribution of $20,000 to be used for a specific project. During the current year, $14,000 is spent toward the project with the balance to be spent next year. What will the net asset balance in the restricted fund be at the end of the year if the organization uses the restricted fund method for reporting and had a fund for this project?

A) $20,000

B) $6,000

C) $14,000

D) Nil

A) $20,000

B) $6,000

C) $14,000

D) Nil

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

30

Net assets could be broken down into any of the following categories EXCEPT:

A) internally restricted and other externally restricted net assets.

B) net assets maintained permanently in endowments.

C) unrestricted net assets.

D) net assets invested in operations.

A) internally restricted and other externally restricted net assets.

B) net assets maintained permanently in endowments.

C) unrestricted net assets.

D) net assets invested in operations.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following is NOT a type of contribution as identified by the Handbook?

A) Restricted.

B) Endowment.

C) Unrestricted.

D) Donated.

A) Restricted.

B) Endowment.

C) Unrestricted.

D) Donated.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

32

How should that portion of investment income earned from the investment of endowment contributions that is required to be used to maintain the purchasing power of the endowment be accounted for if the not-for-profit organization uses the restricted fund method of reporting and has an endowment fund?

A) As investment income in the general fund.

B) As investment income in the endowment fund.

C) As a direct increase in net assets in the general fund.

D) As a direct increase in net assets in the endowment fund.

A) As investment income in the general fund.

B) As investment income in the endowment fund.

C) As a direct increase in net assets in the general fund.

D) As a direct increase in net assets in the endowment fund.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

33

Where should be endowment contributions presented in the financial statements of a not-for-profit organization under the deferral method?

A) They are reflected in the notes to the financial statements.

B) They are used to effect a reduction to a related expense account.

C) They are reflected in the statement of changes in net assets.

D) They are shown in the statement of operations.

A) They are reflected in the notes to the financial statements.

B) They are used to effect a reduction to a related expense account.

C) They are reflected in the statement of changes in net assets.

D) They are shown in the statement of operations.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

34

A not-for-profit organization is required to record the donation of capital assets at:

A) replacement cost.

B) fair value.

C) net realizable value.

D) the original cost to the donor of the capital asset.

A) replacement cost.

B) fair value.

C) net realizable value.

D) the original cost to the donor of the capital asset.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

35

Assuming a not-for-profit organization used the restricted fund method and had separate funds for the purpose for which donations were intended, how should investment income earned on donation revenue be accounted for if the donation revenue was a restricted contribution but there was no restriction placed on the use of the investment income?

A) As investment income in the general fund.

B) As investment income in the restricted fund.

C) As donation revenue in the restricted fund.

D) As a direct increase in net assets in the restricted fund.

A) As investment income in the general fund.

B) As investment income in the restricted fund.

C) As donation revenue in the restricted fund.

D) As a direct increase in net assets in the restricted fund.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

36

How should investment income earned from the investment of endowment contributions be accounted for if the not-for-profit organization uses the restricted fund method of accounting and the use of the investment income is restricted to a specific purpose for which the not-for-profit organization has a restricted fund?

A) As investment income in the endowment fund

B) As a deferred contribution

C) As investment income in the general fund

D) As investment income in the specific restricted fund

A) As investment income in the endowment fund

B) As a deferred contribution

C) As investment income in the general fund

D) As investment income in the specific restricted fund

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

37

How should investment income earned from the investment of endowment contributions be accounted for if the not-for-profit organization uses the deferral method of accounting for contributions and the use of the investment income is restricted to a specific purpose?

A) As investment income.

B) As a deferred contribution.

C) As a direct increase in net assets.

D) As donation revenue.

A) As investment income.

B) As a deferred contribution.

C) As a direct increase in net assets.

D) As donation revenue.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

38

How should that portion of investment income earned from the investment of endowment contributions that is required to be used to maintain the purchasing power of the endowment be accounted for, if the not-for-profit organization uses the deferred contribution method of accounting?

A) As investment income.

B) As a deferred contribution.

C) As a direct increase in net assets.

D) As donation revenue.

A) As investment income.

B) As a deferred contribution.

C) As a direct increase in net assets.

D) As donation revenue.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

39

A not-for-profit organization receives a restricted contribution of $20,000 to be used for a specific project. During the current year, $14,000 is spent toward the project with the balance to be spent next year. How much donation revenue should the not-for-profit organization recognize in the current year, if the organization uses the deferral method of reporting?

A) $6,000

B) $14,000

C) $20,000

D) $34,000

A) $6,000

B) $14,000

C) $20,000

D) $34,000

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

40

An NFPO may exercise significant influence over the strategic operating, investing, and financing activities of another NFPO. Which of the following is NOT a factor in determining significant influence?

A) Ability to place members on the board of directors

B) Substantial transactions between the organizations

C) Percentage of share ownership

D) Sharing of senior personnel

A) Ability to place members on the board of directors

B) Substantial transactions between the organizations

C) Percentage of share ownership

D) Sharing of senior personnel

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

41

What reporting choices are given to Canadian private not-for-profit organizations?

A) They may report under the Accounting Standards for Private Enterprises (ASPE) found in Part II of the CPA Canada Handbook without modification.

B) They may report using the standards found in Part III of the CPA Canada Handbook and apply Part II (ASPE) to the extent that the Part II standards address topics not addressed in Part III.

C) They may report under the International Financial Reporting Standards (IFRS) modified by the standards found in Part III of the CPA Canada Handbook.

D) If the NFPO was formed prior to 2010, they may continue to report in accordance with the Canadian standards for not-for-profit enterprises that existed prior to 2011-2012.

A) They may report under the Accounting Standards for Private Enterprises (ASPE) found in Part II of the CPA Canada Handbook without modification.

B) They may report using the standards found in Part III of the CPA Canada Handbook and apply Part II (ASPE) to the extent that the Part II standards address topics not addressed in Part III.

C) They may report under the International Financial Reporting Standards (IFRS) modified by the standards found in Part III of the CPA Canada Handbook.

D) If the NFPO was formed prior to 2010, they may continue to report in accordance with the Canadian standards for not-for-profit enterprises that existed prior to 2011-2012.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

42

The Rift Valley Minor Hockey Association was established in the village of Rift Valley in early 2019. It was established to promote hockey in the village and surrounding territory. With the support of the provincial government, local business people and many individuals, the association raised sufficient funds to build an indoor hockey arena and also established an endowment fund to cover maintenance costs. The association is required by the provincial government to prepare financial statements in accordance with generally accepted accounting principles.

The board has decided that its year end will be June 30 and that capital assets will be capitalized and amortized over their expected useful lives. They have decided not to use the restricted fund method of accounting but will account for restricted donations using the deferral method of accounting for contributions. The first set of financial statements will cover the eighteen month period from the establishment of the association to June 30, 2020.

From the bank statements, you determine the following:

Additional information:

1. The new arena was completed and officially opened on Canada Day (July 1) of 2019. It has an estimated forty year life with no residual value.

2. A long-term resident of Rift Valley donated the land upon which the arena was constructed. The land was valued at $120,000 and the association issued a receipt in that amount. Another resident donated ice-making and ice-cleaning equipment to the association. The equipment has an estimated useful life of six years and no residual value and was estimated to have a value of $66,000 when donated.

3. The endowment contribution was received at the opening celebration and was invested for one year at 5% interest. The terms of the endowment were that the income earned from its investment could be used only for maintenance costs for the arena. $3,000 of such costs were incurred and paid for in May 2020. (The other $1,000 in interest income was earned on the balances in the bank account.)

4. The government had agreed to provide funding of $10,000 per month for the eight months of the minor hockey season (September 1 to April 30 each year). The amount was payable at $7,500 per month during the season and the final $20,000 upon submission of the annual financial statements to the government.

5. Registration fees for minor hockey players cover the season from September to April. $10,000 of the fees received were payments in advance for the 2020-2021 season.

6. An inventory count was taken at the concession stand at the end of June 2020 and the inventory on hand was valued at $6,000 (lower of cost or realizable value). The concession stand sold snacks and drinks during minor hockey games and other events.

7. At June 30, 2020, unpaid invoices were $3,000 for concession purchases, $2,000 for hockey clinics held and $1,000 for miscellaneous other costs.

Prepare a statement of financial position for the Rift Valley Minor Hockey Association as at June 30, 2020.

The board has decided that its year end will be June 30 and that capital assets will be capitalized and amortized over their expected useful lives. They have decided not to use the restricted fund method of accounting but will account for restricted donations using the deferral method of accounting for contributions. The first set of financial statements will cover the eighteen month period from the establishment of the association to June 30, 2020.

From the bank statements, you determine the following:

Additional information:1. The new arena was completed and officially opened on Canada Day (July 1) of 2019. It has an estimated forty year life with no residual value.

2. A long-term resident of Rift Valley donated the land upon which the arena was constructed. The land was valued at $120,000 and the association issued a receipt in that amount. Another resident donated ice-making and ice-cleaning equipment to the association. The equipment has an estimated useful life of six years and no residual value and was estimated to have a value of $66,000 when donated.

3. The endowment contribution was received at the opening celebration and was invested for one year at 5% interest. The terms of the endowment were that the income earned from its investment could be used only for maintenance costs for the arena. $3,000 of such costs were incurred and paid for in May 2020. (The other $1,000 in interest income was earned on the balances in the bank account.)

4. The government had agreed to provide funding of $10,000 per month for the eight months of the minor hockey season (September 1 to April 30 each year). The amount was payable at $7,500 per month during the season and the final $20,000 upon submission of the annual financial statements to the government.

5. Registration fees for minor hockey players cover the season from September to April. $10,000 of the fees received were payments in advance for the 2020-2021 season.

6. An inventory count was taken at the concession stand at the end of June 2020 and the inventory on hand was valued at $6,000 (lower of cost or realizable value). The concession stand sold snacks and drinks during minor hockey games and other events.

7. At June 30, 2020, unpaid invoices were $3,000 for concession purchases, $2,000 for hockey clinics held and $1,000 for miscellaneous other costs.

Prepare a statement of financial position for the Rift Valley Minor Hockey Association as at June 30, 2020.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

43

A capital asset (equipment) with a fair value of $1,500,000 and land with a fair value of $2,000,000 is donated to a not-for-profit organization on January 1, 2020. The equipment has a ten year useful life. The organization will use the equipment in its operations. The NFPO has a December 31 year end.

Prepare the journal entries (including amortization) if the organization uses the:

a) the deferral method for contributions.

b) the restricted fund method with a capital fund.

Prepare the journal entries (including amortization) if the organization uses the:

a) the deferral method for contributions.

b) the restricted fund method with a capital fund.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

44

Buana Fide is a local charity which received the following donations during 2020:

A local radio station donated air time valued at $20,000. If the air time had not been donated, Buana Fide would have purchased it and used it for advertising a fundraising event and silent auction.

An anonymous donor donated land with a fair value of $50,000 as well as machinery valued at $4,000.

During a recent fund-raising campaign, volunteers spent roughly 1,000 hours soliciting donations from the public. The minimum hourly wage rate in Buana Fide's main area of operation is $8.00 per hour.

Prepare the necessary journal entries to record these transactions assuming that the deferral method of accounting for contributions is used. Note: if a journal entry is not needed, state your reason.

A local radio station donated air time valued at $20,000. If the air time had not been donated, Buana Fide would have purchased it and used it for advertising a fundraising event and silent auction.

An anonymous donor donated land with a fair value of $50,000 as well as machinery valued at $4,000.

During a recent fund-raising campaign, volunteers spent roughly 1,000 hours soliciting donations from the public. The minimum hourly wage rate in Buana Fide's main area of operation is $8.00 per hour.

Prepare the necessary journal entries to record these transactions assuming that the deferral method of accounting for contributions is used. Note: if a journal entry is not needed, state your reason.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

45

Buana Fide is a local charity which received the following donations during 2020:

A local radio station donated air time valued at $20,000. If the air time had not been donated, Buana Fide would have purchased it and used it for advertising a fundraising event and silent auction.

An anonymous donor donated land with a fair value of $50,000 as well as machinery valued at $4,000.

During a recent fund-raising campaign, volunteers spent roughly 1,000 hours soliciting donations from the public. The minimum hourly wage rate in Buana Fide's main area of operation is $8.00 per hour.

Prepare the necessary journal entries to record these transactions assuming that the restricted fund method of accounting for contributions is used and the organization has a general fund, a capital fund and an endowment fund. Note: if a journal entry is not needed, state your reason.

A local radio station donated air time valued at $20,000. If the air time had not been donated, Buana Fide would have purchased it and used it for advertising a fundraising event and silent auction.

An anonymous donor donated land with a fair value of $50,000 as well as machinery valued at $4,000.

During a recent fund-raising campaign, volunteers spent roughly 1,000 hours soliciting donations from the public. The minimum hourly wage rate in Buana Fide's main area of operation is $8.00 per hour.

Prepare the necessary journal entries to record these transactions assuming that the restricted fund method of accounting for contributions is used and the organization has a general fund, a capital fund and an endowment fund. Note: if a journal entry is not needed, state your reason.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

46

Describe what fund accounting is and why is it used for not-for-profit organizations.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

47

A not-for-profit organization receives a restricted contribution of $20,000 to be used for a specific project. During the current year, $14,000 is spent toward the project with the balance to be spent next year. How much donation revenue should the not-for-profit organization recognize in the current year, if the organization uses the restricted fund method of reporting and did not have a fund for this project?

A) $6,000

B) $14,000

C) $20,000

D) $34,000

A) $6,000

B) $14,000

C) $20,000

D) $34,000

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

48

A statement of changes in net assets in the financial statements of a not-for-profit organization corresponds most closely to which of the following in the financial statements of a profit-oriented business which reports under IFRS?

A) The statement of financial position.

B) The statement of cash flows.

C) The income statement.

D) The statement of changes in shareholders' equity.

A) The statement of financial position.

B) The statement of cash flows.

C) The income statement.

D) The statement of changes in shareholders' equity.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

49

On January 1, 2020, some residents of the community of Kiterup,B.C., formed the Kiterup Winter Sports Association (KWSA) which was organized as a not-for-profit organization which has as its purposes encouraging participation in outdoor winter sports. In its first year, the board decided to restrict its activities to ice skating and skiing.

Initial funding was provided by a wealthy individual who made an endowment contribution of $200,000 which was invested in bonds and generated income during the year of $8,000. The donor placed no restrictions on the use of the income produced by the investment of the endowment contribution which were to be divided evenly between all programs undertaken by the Association.

During the year donations of $750,000 were received and a further $150,000 of pledges was outstanding of which the board estimated $130,000 would be collected. It was agreed that such donations, all of which were unrestricted, would be divided evenly between the skating and skiing programs. As a practical matter, donations not yet received at year-end were considered to be restricted for use in the following year. A special fund drive was undertaken to raise money to provide skates to needy youngsters and skiing equipment to needy senior citizens. During the year $25,000 was received in contributions for skates and $15,000 for contributions towards purchasing skis.

During the year ended December 31, 2020, the organization incurred the following costs.

At December 31, 2020, the only outstanding payables were for $30,000 relating to the skiing program (the costs are included in the table above). The ice skates and skiing equipment were paid for out of the funds raised by the special fund drive and were expensed as acquired.

KWSA does not use fund accounting but uses the deferral method to account for restricted donations and uses programmatic reporting to report the results of its activities.

Prepare a statement of financial position of the Kiterup Winter Sports Association as at December 31, 2020. Statements for the individual programs are not required.

Initial funding was provided by a wealthy individual who made an endowment contribution of $200,000 which was invested in bonds and generated income during the year of $8,000. The donor placed no restrictions on the use of the income produced by the investment of the endowment contribution which were to be divided evenly between all programs undertaken by the Association.

During the year donations of $750,000 were received and a further $150,000 of pledges was outstanding of which the board estimated $130,000 would be collected. It was agreed that such donations, all of which were unrestricted, would be divided evenly between the skating and skiing programs. As a practical matter, donations not yet received at year-end were considered to be restricted for use in the following year. A special fund drive was undertaken to raise money to provide skates to needy youngsters and skiing equipment to needy senior citizens. During the year $25,000 was received in contributions for skates and $15,000 for contributions towards purchasing skis.

During the year ended December 31, 2020, the organization incurred the following costs.

At December 31, 2020, the only outstanding payables were for $30,000 relating to the skiing program (the costs are included in the table above). The ice skates and skiing equipment were paid for out of the funds raised by the special fund drive and were expensed as acquired.KWSA does not use fund accounting but uses the deferral method to account for restricted donations and uses programmatic reporting to report the results of its activities.

Prepare a statement of financial position of the Kiterup Winter Sports Association as at December 31, 2020. Statements for the individual programs are not required.

Unlock Deck

Unlock for access to all 60 flashcards in this deck.

Unlock Deck

k this deck

50

When a not-for-profit organization uses the deferral method of revenue recognition and receives a donation restricted to the purchase of land, when should the donation be recognized as revenue?

A) When the cash is received.

B) When the land is purchased.

C) When the land is put into service by the organization.

D) It should not be recognized as revenue at all.

A) When the cash is received.

B) When the land is purchased.

C) When the land is put into service by the organization.