Deck 15: Leases

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

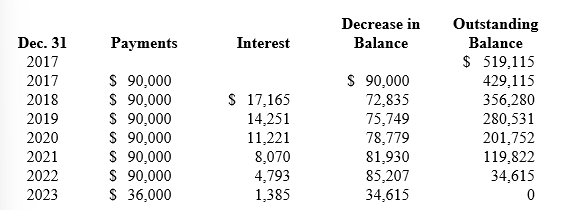

Use the information below to answer the following questions.

On December 31, 2017, Reagan Inc. signed a lease with Silver Leasing Co. for some equipment having a seven-year useful life. The lease payments are made by Reagan annually, beginning at signing date. Title does not transfer to the lessee, so the equipment will be returned to the lessor on December 31, 2023. There is no purchase option, and Reagan guarantees a residual value to the lessor on termination of the lease.

Reagan's lease amortization schedule appears below:

-What is the amount of residual value guaranteed by Reagan to the lessor?

A) $1,385.

B) $34,615.

C) $36,000.

D) Cannot be determined from the given information.

On December 31, 2017, Reagan Inc. signed a lease with Silver Leasing Co. for some equipment having a seven-year useful life. The lease payments are made by Reagan annually, beginning at signing date. Title does not transfer to the lessee, so the equipment will be returned to the lessor on December 31, 2023. There is no purchase option, and Reagan guarantees a residual value to the lessor on termination of the lease.

Reagan's lease amortization schedule appears below:

-What is the amount of residual value guaranteed by Reagan to the lessor?

A) $1,385.

B) $34,615.

C) $36,000.

D) Cannot be determined from the given information.

Question

Use the information below to answer the following questions.

On December 31, 2017, Reagan Inc. signed a lease with Silver Leasing Co. for some equipment having a seven-year useful life. The lease payments are made by Reagan annually, beginning at signing date. Title does not transfer to the lessee, so the equipment will be returned to the lessor on December 31, 2023. There is no purchase option, and Reagan guarantees a residual value to the lessor on termination of the lease.

Reagan's lease amortization schedule appears below:

-In this situation, Reagan:

A) is the lessee in a sales-type lease.

B) is the lessee in a finance lease.

C) is the lessor in a finance lease.

D) is the lessor in a sales-type lease.

On December 31, 2017, Reagan Inc. signed a lease with Silver Leasing Co. for some equipment having a seven-year useful life. The lease payments are made by Reagan annually, beginning at signing date. Title does not transfer to the lessee, so the equipment will be returned to the lessor on December 31, 2023. There is no purchase option, and Reagan guarantees a residual value to the lessor on termination of the lease.

Reagan's lease amortization schedule appears below:

-In this situation, Reagan:

A) is the lessee in a sales-type lease.

B) is the lessee in a finance lease.

C) is the lessor in a finance lease.

D) is the lessor in a sales-type lease.

Question

Use the information below to answer the following questions.

On December 31, 2017, Reagan Inc. signed a lease with Silver Leasing Co. for some equipment having a seven-year useful life. The lease payments are made by Reagan annually, beginning at signing date. Title does not transfer to the lessee, so the equipment will be returned to the lessor on December 31, 2023. There is no purchase option, and Reagan guarantees a residual value to the lessor on termination of the lease.

Reagan's lease amortization schedule appears below:

-What is the effective annual interest rate charged to Reagan on this lease?

A) 4%.

B) 6%.

C) 8%.

D) 17%.

On December 31, 2017, Reagan Inc. signed a lease with Silver Leasing Co. for some equipment having a seven-year useful life. The lease payments are made by Reagan annually, beginning at signing date. Title does not transfer to the lessee, so the equipment will be returned to the lessor on December 31, 2023. There is no purchase option, and Reagan guarantees a residual value to the lessor on termination of the lease.

Reagan's lease amortization schedule appears below:

-What is the effective annual interest rate charged to Reagan on this lease?

A) 4%.

B) 6%.

C) 8%.

D) 17%.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

On January 1, 2018, Wellburn Corporation leased an asset from Tabitha Company. The asset originally cost Tabitha $300,000. The lease agreement is an operating lease that calls for four annual payments beginning on January 1, 2018, in the amount of $36,000. The other three remaining payments will be made on January 1 of each subsequent year. Which of the following journal entries should Tabitha record on January 1, 2018?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

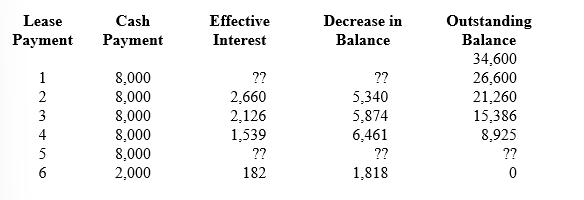

Refer to the following lease amortization schedule. The five payments are made annually starting with the beginning of the lease. A $2,000 purchase option is reasonably certain to be exercised at the end of the five-year lease. The asset has an expected economic life of eight years.

-What amount would the lessee record as annual amortization on the asset using the straight-line method, assuming no residual value?

A) $3,325.

B) $6,920.

C) $4,325.

D) $5,320.

-What amount would the lessee record as annual amortization on the asset using the straight-line method, assuming no residual value?

A) $3,325.

B) $6,920.

C) $4,325.

D) $5,320.

Question

Question

Question

Refer to the following lease amortization schedule. The five payments are made annually starting with the beginning of the lease. A $2,000 purchase option is reasonably certain to be exercised at the end of the five-year lease. The asset has an expected economic life of eight years.

-What is the effective annual interest rate?

A) 9%.

B) 10%.

C) 11%.

D) 20%.

-What is the effective annual interest rate?

A) 9%.

B) 10%.

C) 11%.

D) 20%.

Question

Question

Question

Question

Refer to the following lease amortization schedule. The five payments are made annually starting with the beginning of the lease. A $2,000 purchase option is reasonably certain to be exercised at the end of the five-year lease. The asset has an expected economic life of eight years.

-What is the outstanding balance after payment 5?

A) $1,818.

B) $2,000.

C) $2,182.

D) $3,818.

-What is the outstanding balance after payment 5?

A) $1,818.

B) $2,000.

C) $2,182.

D) $3,818.

Question

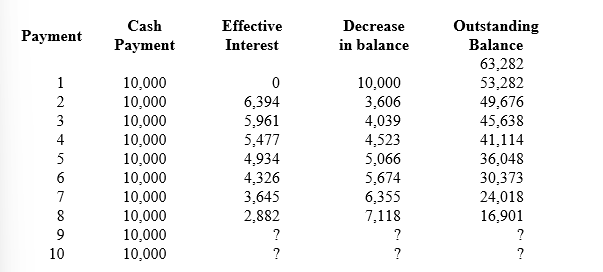

Refer to the following lease amortization schedule. The 10 payments are made annually starting with the beginning of the lease. Title does not transfer to the lessee and there is no purchase option or guaranteed residual value. The asset has an expected economic life of 12 years. The lease is noncancelable.

-What is the outstanding balance after payment 9?

A) $8,929.

B) $13,463.

C) $5,000.

D) $5,537.

-What is the outstanding balance after payment 9?

A) $8,929.

B) $13,463.

C) $5,000.

D) $5,537.

Question

Question

Refer to the following lease amortization schedule. The 10 payments are made annually starting with the beginning of the lease. Title does not transfer to the lessee and there is no purchase option or guaranteed residual value. The asset has an expected economic life of 12 years. The lease is noncancelable.

-What is the effective annual interest rate?

A) 9%.

B) 10%.

C) 11%.

D) 12%.

-What is the effective annual interest rate?

A) 9%.

B) 10%.

C) 11%.

D) 12%.

Question

Refer to the following lease amortization schedule. The 10 payments are made annually starting with the beginning of the lease. Title does not transfer to the lessee and there is no purchase option or guaranteed residual value. The asset has an expected economic life of 12 years. The lease is noncancelable.

-What amount would the lessee record as annual amortization on the right-of-use asset using the straight-line method?

A) $5,328.

B) $6,328.

C) $6,392.

D) $10,000.

-What amount would the lessee record as annual amortization on the right-of-use asset using the straight-line method?

A) $5,328.

B) $6,328.

C) $6,392.

D) $10,000.

Question

Refer to the following lease amortization schedule. The five payments are made annually starting with the beginning of the lease. A $2,000 purchase option is reasonably certain to be exercised at the end of the five-year lease. The asset has an expected economic life of eight years.

-What would be the amount of interest expense recorded with payment 5?

A) $2,000.

B) $893.

C) $7,107.

D) $1,107.

-What would be the amount of interest expense recorded with payment 5?

A) $2,000.

B) $893.

C) $7,107.

D) $1,107.

Question

Refer to the following lease amortization schedule. The 10 payments are made annually starting with the beginning of the lease. Title does not transfer to the lessee and there is no purchase option or guaranteed residual value. The asset has an expected economic life of 12 years. The lease is noncancelable.

-What would be the outstanding balance after payment 10?

A) $0.

B) $2,028.

C) $8,929.

D) $10,000.

-What would be the outstanding balance after payment 10?

A) $0.

B) $2,028.

C) $8,929.

D) $10,000.

Question

Question

Refer to the following lease amortization schedule. The 10 payments are made annually starting with the beginning of the lease. Title does not transfer to the lessee and there is no purchase option or guaranteed residual value. The asset has an expected economic life of 12 years. The lease is noncancelable.

-What is the total effective interest paid over the term of the lease?

A) $100,000.

B) $36,718.

C) $53,282.

D) $63,282.

-What is the total effective interest paid over the term of the lease?

A) $100,000.

B) $36,718.

C) $53,282.

D) $63,282.

Question

Question

Refer to the following lease amortization schedule. The five payments are made annually starting with the beginning of the lease. A $2,000 purchase option is reasonably certain to be exercised at the end of the five-year lease. The asset has an expected economic life of eight years.

-What is the total interest paid over the term of the lease?

A) $42,000.

B) $8,200.

C) $7,400.

D) $3,460.

-What is the total interest paid over the term of the lease?

A) $42,000.

B) $8,200.

C) $7,400.

D) $3,460.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

On January 1, 2018, Calloway Company leased a machine to Zone Corporation. The lease qualifies as a sales-type lease. Calloway paid $240,000 for the machine and is leasing it to Zone for $34,000 per year, an amount that will return 10% to Calloway. The present value of the lease payments is $240,000. The lease payments are due each January 1, beginning in 2018. What is the appropriate interest entry on December 31, 2018?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/262

Play

Full screen (f)

Deck 15: Leases

1

When the total expenses over the life of an operating lease are compared to the total expenses over the life of a finance lease, one will find that:

A) The expenses of a finance lease are greater than the expenses of the operating lease.

B) The expenses of the finance lease and operating lease are equal.

C) The expenses of an operating lease are greater than the expenses of a finance lease.

D) No meaningful comparison can be made.

A) The expenses of a finance lease are greater than the expenses of the operating lease.

B) The expenses of the finance lease and operating lease are equal.

C) The expenses of an operating lease are greater than the expenses of a finance lease.

D) No meaningful comparison can be made.

B

2

For the lessee to account for a lease as a finance lease, the lease must meet:

A) All five of the criteria specified by GAAP regarding accounting for leases.

B) Any one of the six criteria specified by GAAP regarding accounting for leases.

C) Any two of the criteria specified by GAAP regarding accounting for leases.

D) Any one of the five criteria specified by GAAP regarding accounting for leases.

A) All five of the criteria specified by GAAP regarding accounting for leases.

B) Any one of the six criteria specified by GAAP regarding accounting for leases.

C) Any two of the criteria specified by GAAP regarding accounting for leases.

D) Any one of the five criteria specified by GAAP regarding accounting for leases.

D

3

From the perspective of the lessee, leases may be classified as either:

A) Sales-type without selling profit or sales-type with selling profit.

B) Finance or sales-type without selling profit.

C) Finance or operating.

D) Sales-type or operating.

A) Sales-type without selling profit or sales-type with selling profit.

B) Finance or sales-type without selling profit.

C) Finance or operating.

D) Sales-type or operating.

C

4

One of the five criteria for a finance lease specifies that the lease term be equal to or greater than:

A) the major part of the remaining economic life of the leased property.

B) the entire amount of the remaining economic life of the leased property.

C) a meaningful part of the remaining economic life of the leased property.

D) a non-insignificant part of the remaining economic life of the leased property.

A) the major part of the remaining economic life of the leased property.

B) the entire amount of the remaining economic life of the leased property.

C) a meaningful part of the remaining economic life of the leased property.

D) a non-insignificant part of the remaining economic life of the leased property.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

5

If the lease begins "at or near the end" of an asset's economic life, the criterion of the lease term being for the major part of the economic life does not apply when classifying the type of lease. This is consistent with the basic premise of this criterion that most of the risks and rewards of ownership occur prior to that time.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

6

On a transaction that qualifies for sale-leaseback accounting, any gain on the "sale" portion of the transaction is recognized immediately.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

7

If the underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term, then it must be considered to be an operating lease.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

8

For the lessor to account for a lease as a sales-type lease, the lease must meet:

A) Any one of first five classification criteria and both of the last two additional conditions specified by GAAP regarding accounting for leases.

B) More than one of the five criteria specified by GAAP regarding accounting for leases.

C) All five of the criteria specified by GAAP regarding accounting for leases.

D) Any one of the five criteria specified by GAAP regarding accounting for leases.

A) Any one of first five classification criteria and both of the last two additional conditions specified by GAAP regarding accounting for leases.

B) More than one of the five criteria specified by GAAP regarding accounting for leases.

C) All five of the criteria specified by GAAP regarding accounting for leases.

D) Any one of the five criteria specified by GAAP regarding accounting for leases.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

9

When the lessee guarantees an estimated residual value of $75,000, the amount the lessee records as a right-of-use asset and as a lease liability is increased by $75,000.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

10

At the beginning of a lease agreement, a lessee's debt to equity ratio and rate of return on assets are both affected regardless of whether the lease is classified as a finance lease or as an operating lease.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

11

A bargain purchase option is defined as the option of purchasing leased property at a price that is equal to the expected fair value of a leased asset.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

12

The five criteria provided in GAAP for distinguishing a finance lease from an operating lease do not include:

A) The agreement specifies that ownership transfers at the end of the lease term.

B) The collectibility of the lease payments must be reasonably predictable.

C) The agreement grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise.

D) The noncancelable lease term is for the major part of the remaining economic life of the leased asset.

A) The agreement specifies that ownership transfers at the end of the lease term.

B) The collectibility of the lease payments must be reasonably predictable.

C) The agreement grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise.

D) The noncancelable lease term is for the major part of the remaining economic life of the leased asset.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

13

From the perspective of the lessor, two possible lease classifications are:

A) Financing or sales-type.

B) Operating or financing.

C) Sales-type or indirect financing.

D) Operating or sales-type.

A) Financing or sales-type.

B) Operating or financing.

C) Sales-type or indirect financing.

D) Operating or sales-type.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

14

Distinguishing between operating and finance leases is due in large part to the accounting concept of:

A) Conservatism.

B) Materiality.

C) Substance over form.

D) Historical cost.

A) Conservatism.

B) Materiality.

C) Substance over form.

D) Historical cost.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

15

If the lessee is expected to take ownership of a leased asset at the end of the lease term, the lessor must use an estimated residual value when calculating the lease payments necessary to achieve a desired rate of return.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

16

Finance leases are agreements that are formulated outwardly as leases, but are installment purchases in substance.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

17

One of the five criteria for a finance lease specifies that the present value of the lease payments be equal to or greater than:

A) substantially all of the cost of the asset.

B) the major part of the fair value of the asset.

C) substantially all of the fair value of the asset.

D) the major part of the cost of the asset.

A) substantially all of the cost of the asset.

B) the major part of the fair value of the asset.

C) substantially all of the fair value of the asset.

D) the major part of the cost of the asset.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

18

GAAP requires that some lease agreements be accounted for as purchases of assets. The theoretical justification for this treatment is that a lease of this type:

A) Complies with the concept of form over substance.

B) Reflects the relationship of cause and effect.

C) Satisfies the concept of historical cost.

D) Conveys most of the benefits of property ownership.

A) Complies with the concept of form over substance.

B) Reflects the relationship of cause and effect.

C) Satisfies the concept of historical cost.

D) Conveys most of the benefits of property ownership.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

19

In accounting for operating leases, the lessee will recognize amortization on the leased asset.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following is not among the criteria for classifying a lease as a finance lease?

A) The agreement specifies that ownership of the asset transfers to the lessee.

B) The agreement contains an option to purchase the underlying asset that the lessee is reasonably certain to exercise.

C) The lease term is for substantially all of the remaining economic life of the underlying asset.

D) The present value of the sum of the lease payments and any residual value guaranteed by the lessee that isn't already reflected in the lease payments equals or exceeds substantially all of the fair value of the underlying asset.

A) The agreement specifies that ownership of the asset transfers to the lessee.

B) The agreement contains an option to purchase the underlying asset that the lessee is reasonably certain to exercise.

C) The lease term is for substantially all of the remaining economic life of the underlying asset.

D) The present value of the sum of the lease payments and any residual value guaranteed by the lessee that isn't already reflected in the lease payments equals or exceeds substantially all of the fair value of the underlying asset.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

21

Crystal Corporation makes $2,000 payments every month for leasing office equipment. Crystal recorded a lease payment as follows: Crystal must have a(n):

A) Operating lease.

B) Leveraged lease.

C) Finance lease.

D) Sales-type lease without selling profit.

A) Operating lease.

B) Leveraged lease.

C) Finance lease.

D) Sales-type lease without selling profit.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

22

Technoid Inc. sells computer systems. Technoid leases computers to Lone Star Company on January 1, 2018. The manufacturing cost of the computers was $12 million.

This noncancelable lease had the following terms:

• Lease payments: $2,466,754 semiannually; first payment at January 1, 2018;

remaining payments at June 30 and December 31 each year through June 30, 2022.

• Lease term: five years (10 semiannual payments).

• No residual value; no purchase option.

• Economic life of equipment: five years.

• Implicit interest rate and lessee's incremental borrowing rate: 5% semiannually.

• Fair value of the computers at January 1, 2018: $20 million.

-What is the outstanding balance of the lease liability in Lone Star's June 30, 2018, balance sheet? (Round your answer to the nearest dollar.)

A) $15,943,154.

B) $17,533,246.

C) $21,000,000.

D) None of these answer choices is correct.

This noncancelable lease had the following terms:

• Lease payments: $2,466,754 semiannually; first payment at January 1, 2018;

remaining payments at June 30 and December 31 each year through June 30, 2022.

• Lease term: five years (10 semiannual payments).

• No residual value; no purchase option.

• Economic life of equipment: five years.

• Implicit interest rate and lessee's incremental borrowing rate: 5% semiannually.

• Fair value of the computers at January 1, 2018: $20 million.

-What is the outstanding balance of the lease liability in Lone Star's June 30, 2018, balance sheet? (Round your answer to the nearest dollar.)

A) $15,943,154.

B) $17,533,246.

C) $21,000,000.

D) None of these answer choices is correct.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

23

On January 1, 2018, Gibson Corporation entered into a four-year operating lease. The payments were as follows: $20,000 for 2018, $18,000 for 2019, $16,000 for 2020, and $14,000 for 2021. What is the correct amount of total lease expense for 2019?

A) $20,500.

B) $19,000.

C) $17,000.

D) $18,000.

A) $20,500.

B) $19,000.

C) $17,000.

D) $18,000.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

24

The lessee normally measures the lease liability to be recorded as the:

A) Future value of the lease payments.

B) Sum of the cash payments over the term of the lease.

C) Present value of the lease payments.

D) Book value of the leased asset.

A) Future value of the lease payments.

B) Sum of the cash payments over the term of the lease.

C) Present value of the lease payments.

D) Book value of the leased asset.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

25

Technoid Inc. sells computer systems. Technoid leases computers to Lone Star Company on January 1, 2018. The manufacturing cost of the computers was $12 million.

This noncancelable lease had the following terms:

• Lease payments: $2,466,754 semiannually; first payment at January 1, 2018;

remaining payments at June 30 and December 31 each year through June 30, 2022.

• Lease term: five years (10 semiannual payments).

• No residual value; no purchase option.

• Economic life of equipment: five years.

• Implicit interest rate and lessee's incremental borrowing rate: 5% semiannually.

• Fair value of the computers at January 1, 2018: $20 million.

-What is the interest revenue that Technoid would report for this lease in its 2018 income statement?

A) $0.

B) $1,673,820.

C) $876,662.

D) None of these answer choices is correct.

This noncancelable lease had the following terms:

• Lease payments: $2,466,754 semiannually; first payment at January 1, 2018;

remaining payments at June 30 and December 31 each year through June 30, 2022.

• Lease term: five years (10 semiannual payments).

• No residual value; no purchase option.

• Economic life of equipment: five years.

• Implicit interest rate and lessee's incremental borrowing rate: 5% semiannually.

• Fair value of the computers at January 1, 2018: $20 million.

-What is the interest revenue that Technoid would report for this lease in its 2018 income statement?

A) $0.

B) $1,673,820.

C) $876,662.

D) None of these answer choices is correct.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

26

On September 1, 2018, Custom Shirts Inc. entered into a lease agreement appropriately classified as an operating lease. The lease term is three years. The annual payments by Custom Shirts are (a) $20,000 for year 1, (b) $24,000 for year 2, and (c) $28,000 for year 3. How much total lease expense will Custom Shirts recognize for 2018?

A) $6,667.

B) $24,000.

C) $20,000.

D) $ 8,000.

A) $6,667.

B) $24,000.

C) $20,000.

D) $ 8,000.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

27

Use the information below to answer the following questions.

On December 31, 2017, Reagan Inc. signed a lease with Silver Leasing Co. for some equipment having a seven-year useful life. The lease payments are made by Reagan annually, beginning at signing date. Title does not transfer to the lessee, so the equipment will be returned to the lessor on December 31, 2023. There is no purchase option, and Reagan guarantees a residual value to the lessor on termination of the lease.

Reagan's lease amortization schedule appears below:

-What is the amount of residual value guaranteed by Reagan to the lessor?

A) $1,385.

B) $34,615.

C) $36,000.

D) Cannot be determined from the given information.

On December 31, 2017, Reagan Inc. signed a lease with Silver Leasing Co. for some equipment having a seven-year useful life. The lease payments are made by Reagan annually, beginning at signing date. Title does not transfer to the lessee, so the equipment will be returned to the lessor on December 31, 2023. There is no purchase option, and Reagan guarantees a residual value to the lessor on termination of the lease.

Reagan's lease amortization schedule appears below:

-What is the amount of residual value guaranteed by Reagan to the lessor?

A) $1,385.

B) $34,615.

C) $36,000.

D) Cannot be determined from the given information.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

28

Use the information below to answer the following questions.

On December 31, 2017, Reagan Inc. signed a lease with Silver Leasing Co. for some equipment having a seven-year useful life. The lease payments are made by Reagan annually, beginning at signing date. Title does not transfer to the lessee, so the equipment will be returned to the lessor on December 31, 2023. There is no purchase option, and Reagan guarantees a residual value to the lessor on termination of the lease.

Reagan's lease amortization schedule appears below:

-In this situation, Reagan:

A) is the lessee in a sales-type lease.

B) is the lessee in a finance lease.

C) is the lessor in a finance lease.

D) is the lessor in a sales-type lease.

On December 31, 2017, Reagan Inc. signed a lease with Silver Leasing Co. for some equipment having a seven-year useful life. The lease payments are made by Reagan annually, beginning at signing date. Title does not transfer to the lessee, so the equipment will be returned to the lessor on December 31, 2023. There is no purchase option, and Reagan guarantees a residual value to the lessor on termination of the lease.

Reagan's lease amortization schedule appears below:

-In this situation, Reagan:

A) is the lessee in a sales-type lease.

B) is the lessee in a finance lease.

C) is the lessor in a finance lease.

D) is the lessor in a sales-type lease.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

29

Use the information below to answer the following questions.

On December 31, 2017, Reagan Inc. signed a lease with Silver Leasing Co. for some equipment having a seven-year useful life. The lease payments are made by Reagan annually, beginning at signing date. Title does not transfer to the lessee, so the equipment will be returned to the lessor on December 31, 2023. There is no purchase option, and Reagan guarantees a residual value to the lessor on termination of the lease.

Reagan's lease amortization schedule appears below:

-What is the effective annual interest rate charged to Reagan on this lease?

A) 4%.

B) 6%.

C) 8%.

D) 17%.

On December 31, 2017, Reagan Inc. signed a lease with Silver Leasing Co. for some equipment having a seven-year useful life. The lease payments are made by Reagan annually, beginning at signing date. Title does not transfer to the lessee, so the equipment will be returned to the lessor on December 31, 2023. There is no purchase option, and Reagan guarantees a residual value to the lessor on termination of the lease.

Reagan's lease amortization schedule appears below:

-What is the effective annual interest rate charged to Reagan on this lease?

A) 4%.

B) 6%.

C) 8%.

D) 17%.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

30

At what amount would Reagan record the right-of-use asset at the beginning of the agreement?

A) $519,115.

B) $429,115.

C) $540,000.

D) $576,000.

A) $519,115.

B) $429,115.

C) $540,000.

D) $576,000.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

31

If the lessor records deferred rent revenue at the beginning of a lease term, the lease must:

A) Be a financing lease.

B) Be a sales-type lease.

C) Contain a bargain renewal option.

D) Be an operating lease.

A) Be a financing lease.

B) Be a sales-type lease.

C) Contain a bargain renewal option.

D) Be an operating lease.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

32

Technoid would account for this as:

A) A finance lease.

B) A sales-type lease without selling profit.

C) A sales-type lease with selling profit.

D) An operating lease.

A) A finance lease.

B) A sales-type lease without selling profit.

C) A sales-type lease with selling profit.

D) An operating lease.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

33

What is the balance of the lease liability on Reagan's December 31, 2019, balance sheet (after the third lease payment is made)?

A) $280,531.

B) $190,530.

C) $266,280.

D) $356,280.

A) $280,531.

B) $190,530.

C) $266,280.

D) $356,280.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

34

The appropriate asset value reported in the balance sheet by the lessee for an operating lease is:

A) Present value of the lease payments.

B) Sum of the lease payments.

C) The lessor's book value of the asset at the beginning of the lease.

D) Zero, unless a prepayment or accrual is involved.

A) Present value of the lease payments.

B) Sum of the lease payments.

C) The lessor's book value of the asset at the beginning of the lease.

D) Zero, unless a prepayment or accrual is involved.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

35

Lone Star Company would account for this as:

A) A finance lease.

B) A sales type lease without selling profit.

C) A sales type lease with selling profit.

D) An operating lease.

A) A finance lease.

B) A sales type lease without selling profit.

C) A sales type lease with selling profit.

D) An operating lease.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

36

Advance payments made by the lessee on an operating lease are considered to be:

A) Lease expense.

B) Amortization of the right-of-use asset.

C) Deferred revenue to the lessor.

D) A prepayment of interest expense.

A) Lease expense.

B) Amortization of the right-of-use asset.

C) Deferred revenue to the lessor.

D) A prepayment of interest expense.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following statements characterizes an operating lease?

A) The lessee reports cash outflows as financing activities.

B) The lessor records depreciation and lease revenue.

C) The lessor transfers title at the end of the lease term.

D) The lessee has an option to purchase the leased assets and is reasonably sure to exercise the option.

A) The lessee reports cash outflows as financing activities.

B) The lessor records depreciation and lease revenue.

C) The lessor transfers title at the end of the lease term.

D) The lessee has an option to purchase the leased assets and is reasonably sure to exercise the option.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

38

Of the five criteria for a finance lease, which one is not applied if the lease begins "at or near the end" of the economic life of the underlying asset?

A) A purchase option is reasonably certain to be exercised.

B) The economic life test.

C) The present value of lease payments greater or equal to substantially all of fair value test.

D) The passage of title criteria.

A) A purchase option is reasonably certain to be exercised.

B) The economic life test.

C) The present value of lease payments greater or equal to substantially all of fair value test.

D) The passage of title criteria.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

39

A short-term lease:

A) Must be accounted for by the short-cut method if using U.S. GAAP.

B) Is defined as having a value of $10,000 or less.

C) Is defined as having a lease term of fifteen months or less.

D) Not required to be accounted for by the short-cut method if using IFRS.

A) Must be accounted for by the short-cut method if using U.S. GAAP.

B) Is defined as having a value of $10,000 or less.

C) Is defined as having a lease term of fifteen months or less.

D) Not required to be accounted for by the short-cut method if using IFRS.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

40

On January 1, 2018, Wellburn Corporation leased an asset from Tabitha Company. The asset originally cost Tabitha $300,000. The lease agreement is an operating lease that calls for four annual payments beginning on January 1, 2018, in the amount of $36,000. The other three remaining payments will be made on January 1 of each subsequent year. Which of the following journal entries should Tabitha record on January 1, 2018?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

41

A sales-type lease is reported in the lessor's balance sheet as:

A) An asset.

B) A liability.

C) Interest revenue.

D) A contra account to lease liability.

A) An asset.

B) A liability.

C) Interest revenue.

D) A contra account to lease liability.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

42

Since the lease payments under a lease agreement are normally paid at the beginning of each period, the appropriate compound interest table to be used to determine the amount at which the right-of-use asset should be recorded is the:

A) Ordinary annuity table.

B) Present value of $1 table.

C) Present value of an annuity due table.

D) Future value of an annuity due table.

A) Ordinary annuity table.

B) Present value of $1 table.

C) Present value of an annuity due table.

D) Future value of an annuity due table.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

43

Refer to the following lease amortization schedule. The five payments are made annually starting with the beginning of the lease. A $2,000 purchase option is reasonably certain to be exercised at the end of the five-year lease. The asset has an expected economic life of eight years.

-What amount would the lessee record as annual amortization on the asset using the straight-line method, assuming no residual value?

A) $3,325.

B) $6,920.

C) $4,325.

D) $5,320.

-What amount would the lessee record as annual amortization on the asset using the straight-line method, assuming no residual value?

A) $3,325.

B) $6,920.

C) $4,325.

D) $5,320.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

44

For a finance lease, an amount equal to the present value of the lease payments should be recorded by the lessee as a(n):

A) Asset and a liability.

B) Asset and a different amount should be recorded as a liability.

C) Liability and a different amount should be recorded as an asset.

D) Expense.

A) Asset and a liability.

B) Asset and a different amount should be recorded as a liability.

C) Liability and a different amount should be recorded as an asset.

D) Expense.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

45

Like other assets, the cost of a leasehold improvement is allocated as depreciation expense over its useful life to the lessee, which will be:

A) The shorter of the physical life of the asset or the lease term.

B) The physical life of the asset.

C) The lease term.

D) A time period determined by management.

A) The shorter of the physical life of the asset or the lease term.

B) The physical life of the asset.

C) The lease term.

D) A time period determined by management.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

46

Refer to the following lease amortization schedule. The five payments are made annually starting with the beginning of the lease. A $2,000 purchase option is reasonably certain to be exercised at the end of the five-year lease. The asset has an expected economic life of eight years.

-What is the effective annual interest rate?

A) 9%.

B) 10%.

C) 11%.

D) 20%.

-What is the effective annual interest rate?

A) 9%.

B) 10%.

C) 11%.

D) 20%.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

47

For a right-of-use asset under a lease that qualifies as a finance lease because the lease contains a purchase option and the option is reasonably certain to be exercised, the amortization period used by the lessee must be:

A) The same period that was used by the lessor.

B) The economic life of the asset at the time the lease agreement took effect.

C) The term of the lease.

D) The term of the lease or the economic life of the asset, whichever is shorter.

A) The same period that was used by the lessor.

B) The economic life of the asset at the time the lease agreement took effect.

C) The term of the lease.

D) The term of the lease or the economic life of the asset, whichever is shorter.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

48

Titanic Corporation leased executive limos under terms of a $20,000 first payment upon signing the lease and four equal annual payments of $30,000 on the anniversary date of the lease. The interest rate implicit in the lease is 11%. The first year's interest expense would be: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1)

A) $13,200.

B) $10,238.

C) $33,200.

D) $15,543.

A) $13,200.

B) $10,238.

C) $33,200.

D) $15,543.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

49

When a lease qualifies as a finance lease, what amount is recorded as the cost of the right-of-use asset?

A) The present value of the lease payments, exclusive of nonlease components.

B) The present value of the lease payments plus nonlease components.

C) The sum of the gross lease payments.

D) The present value of the lease payments plus the present value of nonlease components.

A) The present value of the lease payments, exclusive of nonlease components.

B) The present value of the lease payments plus nonlease components.

C) The sum of the gross lease payments.

D) The present value of the lease payments plus the present value of nonlease components.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

50

Refer to the following lease amortization schedule. The five payments are made annually starting with the beginning of the lease. A $2,000 purchase option is reasonably certain to be exercised at the end of the five-year lease. The asset has an expected economic life of eight years.

-What is the outstanding balance after payment 5?

A) $1,818.

B) $2,000.

C) $2,182.

D) $3,818.

-What is the outstanding balance after payment 5?

A) $1,818.

B) $2,000.

C) $2,182.

D) $3,818.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

51

Refer to the following lease amortization schedule. The 10 payments are made annually starting with the beginning of the lease. Title does not transfer to the lessee and there is no purchase option or guaranteed residual value. The asset has an expected economic life of 12 years. The lease is noncancelable.

-What is the outstanding balance after payment 9?

A) $8,929.

B) $13,463.

C) $5,000.

D) $5,537.

-What is the outstanding balance after payment 9?

A) $8,929.

B) $13,463.

C) $5,000.

D) $5,537.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

52

Leasehold improvements usually are classified in a balance sheet as:

A) Property, plant, and equipment.

B) Other long-term assets.

C) Investments.

D) Expenses.

A) Property, plant, and equipment.

B) Other long-term assets.

C) Investments.

D) Expenses.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

53

Refer to the following lease amortization schedule. The 10 payments are made annually starting with the beginning of the lease. Title does not transfer to the lessee and there is no purchase option or guaranteed residual value. The asset has an expected economic life of 12 years. The lease is noncancelable.

-What is the effective annual interest rate?

A) 9%.

B) 10%.

C) 11%.

D) 12%.

-What is the effective annual interest rate?

A) 9%.

B) 10%.

C) 11%.

D) 12%.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

54

Refer to the following lease amortization schedule. The 10 payments are made annually starting with the beginning of the lease. Title does not transfer to the lessee and there is no purchase option or guaranteed residual value. The asset has an expected economic life of 12 years. The lease is noncancelable.

-What amount would the lessee record as annual amortization on the right-of-use asset using the straight-line method?

A) $5,328.

B) $6,328.

C) $6,392.

D) $10,000.

-What amount would the lessee record as annual amortization on the right-of-use asset using the straight-line method?

A) $5,328.

B) $6,328.

C) $6,392.

D) $10,000.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

55

Refer to the following lease amortization schedule. The five payments are made annually starting with the beginning of the lease. A $2,000 purchase option is reasonably certain to be exercised at the end of the five-year lease. The asset has an expected economic life of eight years.

-What would be the amount of interest expense recorded with payment 5?

A) $2,000.

B) $893.

C) $7,107.

D) $1,107.

-What would be the amount of interest expense recorded with payment 5?

A) $2,000.

B) $893.

C) $7,107.

D) $1,107.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

56

Refer to the following lease amortization schedule. The 10 payments are made annually starting with the beginning of the lease. Title does not transfer to the lessee and there is no purchase option or guaranteed residual value. The asset has an expected economic life of 12 years. The lease is noncancelable.

-What would be the outstanding balance after payment 10?

A) $0.

B) $2,028.

C) $8,929.

D) $10,000.

-What would be the outstanding balance after payment 10?

A) $0.

B) $2,028.

C) $8,929.

D) $10,000.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

57

On October 1, 2018, Sonoma Company leased equipment from Napa Inc. in lease payable in five equal annual payments of $500,000, beginning Oct 1, 2019. Similar transactions have carried an 11% interest rate. The right-of-use asset would be recorded at: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1)

A) $0.

B) $1,847,950.

C) $2,115,270.

D) $2,500,000.

A) $0.

B) $1,847,950.

C) $2,115,270.

D) $2,500,000.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

58

Refer to the following lease amortization schedule. The 10 payments are made annually starting with the beginning of the lease. Title does not transfer to the lessee and there is no purchase option or guaranteed residual value. The asset has an expected economic life of 12 years. The lease is noncancelable.

-What is the total effective interest paid over the term of the lease?

A) $100,000.

B) $36,718.

C) $53,282.

D) $63,282.

-What is the total effective interest paid over the term of the lease?

A) $100,000.

B) $36,718.

C) $53,282.

D) $63,282.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

59

If the lessor retains title to leased property under the terms of the lease:

A) The amount to be recovered through periodic lease payments is reduced by the present value of any residual amount.

B) The amount to be recovered through periodic lease payments is increased by the present value of the residual amount.

C) The amount to be recovered will be the same as if there were no residual value.

D) The lessor will record a greater amount of depreciation due to the residual value.

A) The amount to be recovered through periodic lease payments is reduced by the present value of any residual amount.

B) The amount to be recovered through periodic lease payments is increased by the present value of the residual amount.

C) The amount to be recovered will be the same as if there were no residual value.

D) The lessor will record a greater amount of depreciation due to the residual value.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

60

Refer to the following lease amortization schedule. The five payments are made annually starting with the beginning of the lease. A $2,000 purchase option is reasonably certain to be exercised at the end of the five-year lease. The asset has an expected economic life of eight years.

-What is the total interest paid over the term of the lease?

A) $42,000.

B) $8,200.

C) $7,400.

D) $3,460.

-What is the total interest paid over the term of the lease?

A) $42,000.

B) $8,200.

C) $7,400.

D) $3,460.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

61

When a finance lease is first recorded at the beginning of the lease, the lessee typically debits:

A) Right-of-use asset.

B) Rent expense.

C) Lease expense.

D) Lease receivable.

A) Right-of-use asset.

B) Rent expense.

C) Lease expense.

D) Lease receivable.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

62

On January 1, 2018, Princess Corporation leased equipment to King Company. The lease term is eight years. The first payment of $675,000 was made on January 1, 2018. The equipment cost Princess Corporation $3,600,000. The present value of the lease payments is $3,960,000. The lease is appropriately classified as a sales-type lease. Assuming the interest rate for this lease is 10%, how much interest revenue will Princess record in 2019 on this lease?

A) $261,000.

B) $328,500.

C) $325,350.

D) $293,850.

A) $261,000.

B) $328,500.

C) $325,350.

D) $293,850.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

63

XYZ Company leased equipment to West Corporation under a lease agreement that qualifies as a finance lease to West but not as a result of a bargain purchase option or a title transfer. The present value of the lease payments is $600,000. The expected economic life of the asset is seven years. The lease term is five years. Using the straight-line method, what would West record as annual amortization?

A) $120,000.

B) $61,000.

C) $60,000.

D) $0.

A) $120,000.

B) $61,000.

C) $60,000.

D) $0.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

64

N Corp. entered into a nine-year finance lease on a warehouse on December 31, 2018. Lease payments of $26,000, which includes maintenance services of $1,000, are due annually, beginning on December 31, 2019, and every December 31 thereafter. N does not know the interest rate implicit in the lease; N's incremental borrowing rate is 9%. The rounded present value of an ordinary annuity for nine years at 9% is 6.0. What amount should N report as recorded lease liability at December 31, 2018?

A) $150,000.

B) $156,000.

C) $225,000.

D) $234,000.

A) $150,000.

B) $156,000.

C) $225,000.

D) $234,000.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

65

If the lessee expects to obtain title to leased property due to a purchase option that is reasonably certain to be exercised or the passage of title at the end of the lease term:

A) The lessee ignores any residual value for the leased property.

B) The lessor ignores any residual value for the leased property.

C) The lessee adds the present value of the residual value to the amount recorded for the lease.

D) The lessor will always charge a higher annual lease rate.

A) The lessee ignores any residual value for the leased property.

B) The lessor ignores any residual value for the leased property.

C) The lessee adds the present value of the residual value to the amount recorded for the lease.

D) The lessor will always charge a higher annual lease rate.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

66

By the lessee, a lessee-guaranteed residual value at the beginning of a finance lease should be:

A) Excluded from lease payments.

B) Included as part of lease payments at present value.

C) Included as part of lease payments at future value.

D) Included as part of lease payments only to the extent that guaranteed residual value is expected to exceed estimated residual value.

A) Excluded from lease payments.

B) Included as part of lease payments at present value.

C) Included as part of lease payments at future value.

D) Included as part of lease payments only to the extent that guaranteed residual value is expected to exceed estimated residual value.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

67

Recording a sales-type lease with a selling profit is similar to recording:

A) A purchase on account.

B) An exchange of assets.

C) A sale of a fixed asset.

D) A sale of merchandise on account.

A) A purchase on account.

B) An exchange of assets.

C) A sale of a fixed asset.

D) A sale of merchandise on account.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

68

On January 1, 2018, Packard Corporation leased equipment to Hewlitt Company. The lease term is eight years. The first payment of $450,000 was made on January 1, 2018. Remaining payments are made on December 31 each year, beginning with December 31, 2018. The equipment cost Packard Corporation $2,400,000. The present value of the lease payments is $2,640,000. The lease is appropriately classified as a sales-type lease. Assuming the interest rate for this lease is 10%, what will be the balance reported as a liability by Hewlitt in the December 31, 2019, balance sheet?

A) $1,950,000.

B) $1,509,000.

C) $1,959,000.

D) $1,704,900.

A) $1,950,000.

B) $1,509,000.

C) $1,959,000.

D) $1,704,900.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

69

The costs that (a) are associated directly with consummating a lease, (b) are essential to acquire the lease, and (c) would not have been incurred had the lease agreement not occurred, are referred to as initial direct costs. Initial direct costs incurred by the lessor are deferred and expensed over the lease term:

A) Only in an operating lease.

B) Only in a sales-type lease with selling profit.

C) Only in a sales-type lease with no selling profit.

D) In both an operating lease and a sales-type lease with no selling profit.

A) Only in an operating lease.

B) Only in a sales-type lease with selling profit.

C) Only in a sales-type lease with no selling profit.

D) In both an operating lease and a sales-type lease with no selling profit.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

70

The costs that (a) are associated directly with consummating a lease, (b) are essential to acquire the lease, and (c) would not have been incurred had the lease agreement not occurred, are referred to as initial direct costs. Initial direct costs are expensed at the beginning of the lease in:

A) An operating lease.

B) A sales-type lease with selling profit.

C) A sales-type lease with no selling profit.

D) Both an operating lease and a sales-type lease with no selling profit.

A) An operating lease.

B) A sales-type lease with selling profit.

C) A sales-type lease with no selling profit.

D) Both an operating lease and a sales-type lease with no selling profit.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

71

A noncancelable lease contains an option to purchase a leased asset at a price that is sufficiently lower than the asset's expected fair value so that the exercise of the option appears reasonably certain. The fair value of the asset exceeds the lessor's cost of the asset. Therefore, the lease will be accounted for by the lessor as a(n):

A) Sales-type lease.

B) Financing lease.

C) Operating lease.

D) Guaranteed lease.

A) Sales-type lease.

B) Financing lease.

C) Operating lease.

D) Guaranteed lease.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

72

If the residual value of a leased asset turns out to be more than the amount guaranteed by the lessee, the:

A) Lessor must compensate the lessee for the excess.

B) Lessee must pay the lessor the amount of the excess.

C) Lessee will reduce the last year's depreciation.

D) Lessor is not obligated to compensate the lessee for the excess.

A) Lessor must compensate the lessee for the excess.

B) Lessee must pay the lessor the amount of the excess.

C) Lessee will reduce the last year's depreciation.

D) Lessor is not obligated to compensate the lessee for the excess.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

73

ABC Company leased equipment to Best Corporation under a lease agreement that qualifies as a finance lease. The cost of the asset is $120,000. The lease contains a bargain purchase option that is effective at the end of the fifth year. The expected economic life of the asset is 10 years. The lease term is five years. The asset is expected to have a residual value of $2,000 at the end of 10 years. Using the straight-line method, what would Best record as annual amortization?

A) $23,600.

B) $12,200.

C) $12,000.

D) $11,800.

A) $23,600.

B) $12,200.

C) $12,000.

D) $11,800.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

74

On January 1, 2018, Calloway Company leased a machine to Zone Corporation. The lease qualifies as a sales-type lease. Calloway paid $240,000 for the machine and is leasing it to Zone for $34,000 per year, an amount that will return 10% to Calloway. The present value of the lease payments is $240,000. The lease payments are due each January 1, beginning in 2018. What is the appropriate interest entry on December 31, 2018?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

75

Which of the following statements regarding lessee-guaranteed residual values is true for the lessee?

A) The asset and liability at the beginning of the lease should be increased by the amount of the residual value to the extent that guaranteed residual value is expected to exceed estimated residual value.

B) The asset and liability at the beginning of the lease should be decreased by the amount of the residual value to the extent that guaranteed residual value is expected to exceed estimated residual value.

C) The asset and liability at the beginning of the lease should be increased by the present value of the residual value to the extent that guaranteed residual value is expected to exceed estimated residual value.

D) The asset and liability at the beginning of the lease should be decreased by the present value of the residual value to the extent that guaranteed residual value is expected to exceed estimated residual value.

A) The asset and liability at the beginning of the lease should be increased by the amount of the residual value to the extent that guaranteed residual value is expected to exceed estimated residual value.

B) The asset and liability at the beginning of the lease should be decreased by the amount of the residual value to the extent that guaranteed residual value is expected to exceed estimated residual value.

C) The asset and liability at the beginning of the lease should be increased by the present value of the residual value to the extent that guaranteed residual value is expected to exceed estimated residual value.

D) The asset and liability at the beginning of the lease should be decreased by the present value of the residual value to the extent that guaranteed residual value is expected to exceed estimated residual value.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

76

What are the three types of expenses that a lessee experiences with a finance lease?

A) Lease expense, payments for nonlease components, interest expense.

B) Amortization expense, lease expense, interest expense.

C) Payments for nonlease components, lease expense, amortization expense.

D) Amortization expense, interest expense, payments for nonlease components.

A) Lease expense, payments for nonlease components, interest expense.

B) Amortization expense, lease expense, interest expense.

C) Payments for nonlease components, lease expense, amortization expense.

D) Amortization expense, interest expense, payments for nonlease components.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

77

Francisco leased equipment from Julio on December 31, 2018. The lease is a 10-year lease with annual payments of $150,000 due on December 31 of each year beginning December 31, 2018. The present value of the lease payments is $1,020,000. Francisco's incremental borrowing rate is 12% for this type of lease. The implicit rate of 10% is known by the lessee. What should be the balance in Francisco lease liability at December 31, 2019?

A) $824,400.

B) $807,000.

C) $806,400.

D) $792,000.

A) $824,400.

B) $807,000.

C) $806,400.

D) $792,000.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

78

The lessee's option to purchase a leased asset at a price that is sufficiently lower than the asset's expected fair value so that the exercise of the option appears reasonably certain sometimes is called a:

A) Bargain purchase option.

B) Lessee buy-out option.

C) Lessor sell-out option.

D) Guaranteed purchase option.

A) Bargain purchase option.

B) Lessee buy-out option.

C) Lessor sell-out option.

D) Guaranteed purchase option.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

79

Durney Co. recorded a right-of-use asset of $800,000 in a ten-year finance lease. The interest rate charged by the lessor was 10%. The balance in the right-of-use asset after two years will be:

A) $648,000

B) $640,000

C) $880,000

D) $968,000

A) $648,000

B) $640,000

C) $880,000

D) $968,000

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

80

The costs that (a) are associated directly with consummating a lease, (b) are essential to acquire the lease, and (c) would not have been incurred had the lease agreement not occurred, are referred to as initial direct costs. Initial direct costs incurred by the lessee are:

A) added to the right-of-use asset and expensed over an amortization period.

B) recorded as an expense at the beginning of the lease.

C) deferred in an operating lease until the asset is returned to the lessor.

D) a reduction to the lease liability at the beginning of the lease.

A) added to the right-of-use asset and expensed over an amortization period.

B) recorded as an expense at the beginning of the lease.

C) deferred in an operating lease until the asset is returned to the lessor.

D) a reduction to the lease liability at the beginning of the lease.

Unlock Deck

Unlock for access to all 262 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 262 flashcards in this deck.