Deck 9: Business Valuation and Corporate Restructuring

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

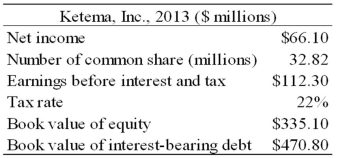

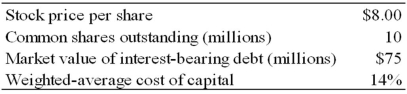

Ketema,Inc.is a manufacturer of electronic instruments.Use the following information on Ketema and five other similar companies to value Ketema,Inc.on December 31,2013.

The median and mean values for Ketema's peers are presented below:

The following estimates require subjective reasoning.In coming to these estimates,Ketema,Inc.is judged as exhibiting representative earnings per share growth,but considerably higher financial leverage,and a below-average five-year growth rate in sales.The company's higher-than-average leverage suggests that its firm value ratios will be particularly key,as equity value ratios can be distorted by Ketema's higher leverage.Since the firm value ratios abstract from differences in financing,values for these ratios are selected that are closer to the sample averages.Turning to equity value ratios,Ketema's modest growth and higher financial leverage suggest a 10 to 20 percent discount from the group average for its price/earnings and price/sales indicators.

The median and mean values for Ketema's peers are presented below:

The following estimates require subjective reasoning.In coming to these estimates,Ketema,Inc.is judged as exhibiting representative earnings per share growth,but considerably higher financial leverage,and a below-average five-year growth rate in sales.The company's higher-than-average leverage suggests that its firm value ratios will be particularly key,as equity value ratios can be distorted by Ketema's higher leverage.Since the firm value ratios abstract from differences in financing,values for these ratios are selected that are closer to the sample averages.Turning to equity value ratios,Ketema's modest growth and higher financial leverage suggest a 10 to 20 percent discount from the group average for its price/earnings and price/sales indicators.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The following information is available about Chiantivino Corp.(CC):

An activist investor is confident that by terminating CC's money-losing fortified wine division,she can increase free cash flow by $4 million annually for the next decade.In addition,she estimates that an immediate,special dividend of $10 million can be financed by the sale of the division.a.Assuming these actions do not affect CC's cost of capital,what is the maximum price per share the investor would be justified in bidding for control of CC? What percentage premium does this represent?

b.Show your answer if you conduct a sensitivity analysis by assuming the cost of capital is 15 percent and the increased cash flow is only $3.5 million per year.

An activist investor is confident that by terminating CC's money-losing fortified wine division,she can increase free cash flow by $4 million annually for the next decade.In addition,she estimates that an immediate,special dividend of $10 million can be financed by the sale of the division.a.Assuming these actions do not affect CC's cost of capital,what is the maximum price per share the investor would be justified in bidding for control of CC? What percentage premium does this represent?

b.Show your answer if you conduct a sensitivity analysis by assuming the cost of capital is 15 percent and the increased cash flow is only $3.5 million per year.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/36

Play

Full screen (f)

Deck 9: Business Valuation and Corporate Restructuring

1

In venture capital valuation,the post-money valuation is equal to the pre-money valuation plus the amount of the venture capitalist's investment.

True

2

Which of the following statements are correct?

I.Liquidation value of a firm is equal to the present worth of expected future cash flows from operating activities.

II.When an acquiring firm purchases a target firm's equity,the acquirer must assume the target's liabilities.

III.The market value of a public company reflects the worth of the business to minority investors.

IV.The fair market value of a business is usually the lower of its liquidation value and its going-concern value.

A) I and III only

B) II and IV only

C) II and III only

D) I,II,and III only

E) II,III,and IV only

I.Liquidation value of a firm is equal to the present worth of expected future cash flows from operating activities.

II.When an acquiring firm purchases a target firm's equity,the acquirer must assume the target's liabilities.

III.The market value of a public company reflects the worth of the business to minority investors.

IV.The fair market value of a business is usually the lower of its liquidation value and its going-concern value.

A) I and III only

B) II and IV only

C) II and III only

D) I,II,and III only

E) II,III,and IV only

II and III only

3

An acquirer should be willing to pay a higher control premium for a poorly managed company than for a well-managed company.

True

4

An acquirer should never consider a target that would reduce the acquirer's earnings per share.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

5

Use BSL's actual financial data for 2010 and its projections for 2011 to 2015 as shown above.Estimate the present value of BSL's free cash flow (in $ millions)for the years 2011 to 2015.The WACC of the acquiring firm (Macklemore)is 8.0 percent,BSL's WACC is 11.5 percent,and the average of the two companies' WACCs,weighted by sales,is 8.2 percent.

A) -$1.29

B) $628.79

C) $720.58

D) $726.68

E) $743.94

A) -$1.29

B) $628.79

C) $720.58

D) $726.68

E) $743.94

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

6

Use BSL's actual financial data for 2010 and its projections for 2011 to 2015 as shown above.Estimate BSL's value (in $ millions)at the end of 2010 assuming it is worth the book value of its assets at the end of 2015.The WACC of the acquiring firm (Macklemore)is 8.0 percent,BSL's WACC is 11.5 percent,and the average of the two companies' WACCs,weighted by sales,is 8.2 percent.

A) $628.24

B) $3,669.01

C) $4,297.80

D) $4,412.94

E) $4,984.28

A) $628.24

B) $3,669.01

C) $4,297.80

D) $4,412.94

E) $4,984.28

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

7

Use BSL's actual financial data for 2010 and its projections for 2011 as shown above.What is BSL's projected free cash flow (in $ millions)for 2011?

A) -$938

B) -$792

C) -$7

D) $122

E) $1,091

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

8

The following table presents forecasted financial and other information for Havasham Industries:

What is an appropriate estimate of Havasham's terminal value as of the end of 2014,using a warranted price-to-earnings multiple as your estimate?

A) $225 million

B) $3,833.0 million

C) $4,207.5 million

D) $4,365.0 million

E) $6,788.1 million

What is an appropriate estimate of Havasham's terminal value as of the end of 2014,using a warranted price-to-earnings multiple as your estimate?

A) $225 million

B) $3,833.0 million

C) $4,207.5 million

D) $4,365.0 million

E) $6,788.1 million

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

9

Ginormous Oil entered into an agreement to purchase all of the outstanding shares of Slick Company for $60 per share.The number of outstanding shares at the time of the announcement was 82 million.The book value of liabilities on the balance sheet of Slick Co.was $1.46 billion.Immediately prior to the Ginormous Oil bid,the shares of Slick Co.traded at $33 per share.What value did Ginormous Oil place on the control of Slick Co.?

A) $2.21 billion

B) $2.71 billion

C) $4.17 billion

D) $6.38 billion

E) None of the abovE.

A) $2.21 billion

B) $2.71 billion

C) $4.17 billion

D) $6.38 billion

E) None of the abovE.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

10

Use BSL's actual financial data for 2010 and its projections for 2011 to 2015 as shown above.Estimate BSL's value (in $ millions)at the end of 2010 assuming that in the years after 2015 the company's free cash flow grows 4 percent per year in perpetuity.The WACC of the acquiring firm (Macklemore)is 8.0 percent,BSL's WACC is 11.5 percent,and the average of the two companies' WACCs,weighted by sales,is 8.2 percent.

A) $4,297.25

B) $4,571.49

C) $4,686.78

D) $6,181.49

E) $5,351.19

A) $4,297.25

B) $4,571.49

C) $4,686.78

D) $6,181.49

E) $5,351.19

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

11

In business valuation,a typical discount for lack of marketability is about 10 percent.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following statements are correct?

i.Going-concern value of a firm is equal to the present value of expected future cash flows to owners and creditors.II.When an acquiring firm purchases a target firm's equity,the acquirer need not assume the target's liabilities.III.The market value of a public company reflects the worth of the business to minority investors.IV.The fair market value of a business is usually the lower of its liquidation value and its going-concern value.

A) I and III only

B) II and IV only

C) II and III only

D) I,II,and III only

E) II,III,and IV only

i.Going-concern value of a firm is equal to the present value of expected future cash flows to owners and creditors.II.When an acquiring firm purchases a target firm's equity,the acquirer need not assume the target's liabilities.III.The market value of a public company reflects the worth of the business to minority investors.IV.The fair market value of a business is usually the lower of its liquidation value and its going-concern value.

A) I and III only

B) II and IV only

C) II and III only

D) I,II,and III only

E) II,III,and IV only

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following statements is/are correct?

i.Going-concern value of a firm is equal to the present value of expected net income.II.When a buyer values a target firm,the appropriate discount rate is the buyer's weighted-average cost of capital.III.The liquidation value estimate of terminal value usually vastly understates a healthy company's terminal value.IV.The value of a firm's equity equals the discounted cash flow value of the firm minus all liabilities.

A) II only

B) III only

C) I and II only

D) II and III only

E) II,III,and IV only

i.Going-concern value of a firm is equal to the present value of expected net income.II.When a buyer values a target firm,the appropriate discount rate is the buyer's weighted-average cost of capital.III.The liquidation value estimate of terminal value usually vastly understates a healthy company's terminal value.IV.The value of a firm's equity equals the discounted cash flow value of the firm minus all liabilities.

A) II only

B) III only

C) I and II only

D) II and III only

E) II,III,and IV only

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

14

Atmosphere,Inc.has offered $860 million cash for all of the common stock in ACE Corporation.Based on recent market information,ACE is worth $710 million as an independent operation.For the merger to make economic sense for Atmosphere,what would the minimum estimated present value of the enhancements from the merger have to be?

A) $0

B) $75 million

C) $150 million

D) $710 million

E) $860 million

A) $0

B) $75 million

C) $150 million

D) $710 million

E) $860 million

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

15

The following table presents forecasted financial and other information for Havasham Industries:

What is an appropriate estimate of Havasham's terminal value as of the end of 2014,using a warranted multiple of free cash flow as your estimate?

A) $155 million

B) $2,898.5 million

C) $3,007.0 million

D) $4,365.0 million

E) $7,042.2 million

What is an appropriate estimate of Havasham's terminal value as of the end of 2014,using a warranted multiple of free cash flow as your estimate?

A) $155 million

B) $2,898.5 million

C) $3,007.0 million

D) $4,365.0 million

E) $7,042.2 million

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

16

Acquisitions create shareholder value,on average.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

17

Use BSL's actual financial data for 2010 and its projections for 2011 to 2015 as shown above.Assume BSL is worth the book value of its assets at the end of 2015.The WACC of the acquiring firm (Macklemore)is 8.0 percent,BSL's WACC is 11.5 percent,and the average of the two companies' WACCs,weighted by sales,is 8.2 percent.What is the maximum acquisition price (in $ millions)Macklemore should pay to acquire BSL's equity?

A) $1,702.80

B) $2,227.80

C) $2,342.94

D) $2,383.94

E) $2,603.80

A) $1,702.80

B) $2,227.80

C) $2,342.94

D) $2,383.94

E) $2,603.80

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

18

Consider the following premerger information about a bidding firm (Buyitall Inc. )and a target firm (Tarjay Corp. ).Assume that neither firm has any debt outstanding.Buyitall has estimated that the present value of any enhancements that Buyitall expects from acquiring Tarjay is $2,600.What is the NPV of the merger assuming that Tarjay is willing to be acquired for $28 per share in cash?

A) $400

B) $600

C) $1,800

D) $2,200

E) $2,600

A) $400

B) $600

C) $1,800

D) $2,200

E) $2,600

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

19

All else equal,a terminal value based on a no-growth perpetuity would be higher than a terminal value based on a perpetuity with 2 percent growth.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

20

Ginormous Oil entered into an agreement to purchase all of the outstanding shares of Slick Company for $60 per share.The number of outstanding shares at the time of the announcement was 82 million.The book value of liabilities on the balance sheet of Slick Co.was $1.46 billion.What was the cost of this acquisition to the shareholders of Ginormous Oil?

A) $1.46 billion

B) $3.46 billion

C) $4.92 billion

D) $6.38 billion

E) $8.38 billion

A) $1.46 billion

B) $3.46 billion

C) $4.92 billion

D) $6.38 billion

E) $8.38 billion

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

21

STU Corporation has $3 million in earnings on $20 million in sales and has 1 million shares outstanding.Earnings per share of comparable firm 1 is $5,and earnings per share of comparable firm 2 is $2.Comparable firm 1's stock is trading for $50,and comparable firm 2's stock is trading for $28.What is the estimated stock price of STU using the method of comparables? (Use average multiples of the comparable firms when doing the calculations. )

A) $33.43

B) $36.00

C) $39.00

D) $40.00

Comp.1 P/E = 10,Comp.2 P/E = 14,Avg.P/E = 12

STU = 12 × $3.00 (EPS)= $36.00

A) $33.43

B) $36.00

C) $39.00

D) $40.00

Comp.1 P/E = 10,Comp.2 P/E = 14,Avg.P/E = 12

STU = 12 × $3.00 (EPS)= $36.00

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

22

Given the forecast below,estimate the fair market value of Kenmore Air's equity per share at the end of 2012 under the following assumptions:

• EBIT in year 2016 will be $210 million.• At year-end 2016,Kenmore Air has reached maturity,and analysts expect its equity will sell for 15 times year 2016 net income.• At year-end 2016,Kenmore Air has $300 million book value of interest-bearing liabilities outstanding at an average interest rate of 10 percent.• Kenmore Air's weighted-average cost of capital is 11 percent and its tax rate is 40 percent.• Kenmore Air has 50 million shares outstanding and the market value of its interest-bearing liabilities on the valuation date equals $300 million.

• EBIT in year 2016 will be $210 million.• At year-end 2016,Kenmore Air has reached maturity,and analysts expect its equity will sell for 15 times year 2016 net income.• At year-end 2016,Kenmore Air has $300 million book value of interest-bearing liabilities outstanding at an average interest rate of 10 percent.• Kenmore Air's weighted-average cost of capital is 11 percent and its tax rate is 40 percent.• Kenmore Air has 50 million shares outstanding and the market value of its interest-bearing liabilities on the valuation date equals $300 million.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

23

Given the forecast below,estimate the fair market value per share of Kenmore Air's equity at the end of 2012 if the company has 50 million shares outstanding and the market value of its interest-bearing liabilities on the valuation date equals $300 million.Assume that after 2016,earnings before interest and tax will remain constant at $220 million,depreciation will equal capital expenditures in each year,and working capital will not change.Kenmore Air's weighted-average cost of capital is 11 percent and its tax rate is 40 percent.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

24

Ketema,Inc.is a manufacturer of electronic instruments.Use the following information on Ketema and five other similar companies to value Ketema,Inc.on December 31,2013.

The median and mean values for Ketema's peers are presented below:

The following estimates require subjective reasoning.In coming to these estimates,Ketema,Inc.is judged as exhibiting representative earnings per share growth,but considerably higher financial leverage,and a below-average five-year growth rate in sales.The company's higher-than-average leverage suggests that its firm value ratios will be particularly key,as equity value ratios can be distorted by Ketema's higher leverage.Since the firm value ratios abstract from differences in financing,values for these ratios are selected that are closer to the sample averages.Turning to equity value ratios,Ketema's modest growth and higher financial leverage suggest a 10 to 20 percent discount from the group average for its price/earnings and price/sales indicators.

The median and mean values for Ketema's peers are presented below:

The following estimates require subjective reasoning.In coming to these estimates,Ketema,Inc.is judged as exhibiting representative earnings per share growth,but considerably higher financial leverage,and a below-average five-year growth rate in sales.The company's higher-than-average leverage suggests that its firm value ratios will be particularly key,as equity value ratios can be distorted by Ketema's higher leverage.Since the firm value ratios abstract from differences in financing,values for these ratios are selected that are closer to the sample averages.Turning to equity value ratios,Ketema's modest growth and higher financial leverage suggest a 10 to 20 percent discount from the group average for its price/earnings and price/sales indicators.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

25

Use BSL's actual financial data for 2010 and its projections for 2011 to 2015 as shown above.Assume that in the years after 2015 the company's free cash flow grows 4 percent per year in perpetuity.The WACC of the acquiring firm (Macklemore)is 8.0 percent,BSL's WACC is 11.5 percent,and the average of the two companies' WACCs,weighted by sales,is 8.2 percent.What is the maximum acquisition price (in $ millions)Macklemore should pay to acquire BSL's equity at the end of 2010?

A) $1,976.49

B) $2,501.49

C) $2,877.49

D) $4,195.49

E) $4,571.49

A) $1,976.49

B) $2,501.49

C) $2,877.49

D) $4,195.49

E) $4,571.49

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

26

Given the forecast below,estimate the fair market value of Kenmore Air's equity per share at the end of 2012 under the following assumptions:

• EBIT in year 2016 is $210 million,and then grows at 4 percent per year forever.• To support the perpetual growth in EBIT,capital expenditures in year 2017 exceed depreciation by $25 million,and this difference grows 4 percent per year forever.• Similarly,working capital investments are $10 million in 2017,and this amount grows 4 percent per year forever.• Kenmore Air's weighted-average cost of capital is 11 percent and its tax rate is 40 percent.• Kenmore Air has 50 million shares outstanding and the market value of its interest-bearing liabilities on the valuation date equals $300 million.

• EBIT in year 2016 is $210 million,and then grows at 4 percent per year forever.• To support the perpetual growth in EBIT,capital expenditures in year 2017 exceed depreciation by $25 million,and this difference grows 4 percent per year forever.• Similarly,working capital investments are $10 million in 2017,and this amount grows 4 percent per year forever.• Kenmore Air's weighted-average cost of capital is 11 percent and its tax rate is 40 percent.• Kenmore Air has 50 million shares outstanding and the market value of its interest-bearing liabilities on the valuation date equals $300 million.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

27

Tutter Corporation is being valued using discounted cash flow methodology with terminal value calculated as a growing perpetuity.Not including the terminal value,the present value of projected free cash flows for years 1 through 5 is $200 million (total).In year 5,projections show free cash flow of $60 million.What is the estimated fair market value of Tutter Corporation? Assume a WACC of 10% and a growth rate of 2%.

A) $666 million

B) $675 million

C) $950 million

D) $965 million

FMV = PV{FCF,1-5} + PV{Terminal value}.

Terminal value = FCF(1 + g)/(KW - g)= $61.2/0.08 = $765 million.

PV of Terminal value = $765 million/1.115 = $475 million.

FMV = 200 million + 475 million = $675 million.

A) $666 million

B) $675 million

C) $950 million

D) $965 million

FMV = PV{FCF,1-5} + PV{Terminal value}.

Terminal value = FCF(1 + g)/(KW - g)= $61.2/0.08 = $765 million.

PV of Terminal value = $765 million/1.115 = $475 million.

FMV = 200 million + 475 million = $675 million.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

28

Rainy City Coffee's (RCC)free cash flow next year will be $100 million and it is expected to grow at a 4 percent annual rate indefinitely.The company's weighted average cost of capital is 10 percent,the market value of its liabilities is $1 billion,and it has 20 million shares outstanding.a.Estimate the price per share of RCC's common stock.b.A hedge fund believes that by selling the company's private jet and instituting other cost savings,it can increase RCC's free cash flow next year to $110 million and can add a full percentage point to RCC's growth rate without affecting its cost of capital.What is the maximum price per share the hedge fund can justify bidding for control of RCC?

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

29

Below is a recent income statement for Gatlin Camera:

Calculate Gatlin's free cash flow in this year assuming it spent $510 on new capital equipment and increased current assets net of noninterest-bearing current liabilities $340.Free cash flow = EBIT(1 - Tax rate)+ Depreciation - Fixed investment - Working capital investment.

Calculate Gatlin's free cash flow in this year assuming it spent $510 on new capital equipment and increased current assets net of noninterest-bearing current liabilities $340.Free cash flow = EBIT(1 - Tax rate)+ Depreciation - Fixed investment - Working capital investment.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

30

Use BSL's actual financial data for 2010 and its projections for 2011 to 2015 as shown above.Estimate BSL's value (in $ millions)at the end of 2010 assuming that at year-end 2015 the company's equity is worth 15 times earnings after tax and its debt is worth book value.The WACC of the acquiring firm (Macklemore)is 8.0 percent,BSL's WACC is 11.5 percent,and the average of the two companies' WACCs,weighted by sales,is 8.2 percent.

A) $628.24

B) $3,669.01

C) $7,429.74

D) $6,343.81

E) $6,755.83

A) $628.24

B) $3,669.01

C) $7,429.74

D) $6,343.81

E) $6,755.83

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

31

Use BSL's actual financial data for 2010 and its projections for 2011 to 2015 as shown above.Assume that at year-end 2015 the company's equity is worth 15 times earnings after tax and its debt is worth book value.The WACC of the acquiring firm (Macklemore)is 8.0 percent,BSL's WACC is 11.5 percent,and the average of the two companies' WACCs,weighted by sales,is 8.2 percent.What is the maximum acquisition price (in $ millions)Macklemore should pay to acquire BSL's equity at the end of 2010?

A) $3,484.68

B) $4,723.81

C) $4,938.06

D) $5,554.68

E) $6,343.81

A) $3,484.68

B) $4,723.81

C) $4,938.06

D) $5,554.68

E) $6,343.81

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

32

Estimate a current stock price for Montana Corporation using the following information.Projected free cash flows for the next three years are shown in the table below.Assume the growth rate in years 1 through 3 continues into the future.Calculate terminal value as a growing perpetuity.Montana's WACC is 18%,the market value of its debt is $5 million,and it has 1.2 million shares of stock outstanding.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

33

Given the forecast below,estimate the fair market value of Kenmore Air at the end of 2012.Assume that after 2016,earnings before interest and tax will remain constant at $220 million,depreciation will equal capital expenditures in each year,and working capital will not change.Kenmore Air's weighted-average cost of capital is 11 percent and its tax rate is 40 percent.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

34

The following information is available about Chiantivino Corp.(CC):

An activist investor is confident that by terminating CC's money-losing fortified wine division,she can increase free cash flow by $4 million annually for the next decade.In addition,she estimates that an immediate,special dividend of $10 million can be financed by the sale of the division.a.Assuming these actions do not affect CC's cost of capital,what is the maximum price per share the investor would be justified in bidding for control of CC? What percentage premium does this represent?

b.Show your answer if you conduct a sensitivity analysis by assuming the cost of capital is 15 percent and the increased cash flow is only $3.5 million per year.

An activist investor is confident that by terminating CC's money-losing fortified wine division,she can increase free cash flow by $4 million annually for the next decade.In addition,she estimates that an immediate,special dividend of $10 million can be financed by the sale of the division.a.Assuming these actions do not affect CC's cost of capital,what is the maximum price per share the investor would be justified in bidding for control of CC? What percentage premium does this represent?

b.Show your answer if you conduct a sensitivity analysis by assuming the cost of capital is 15 percent and the increased cash flow is only $3.5 million per year.

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

35

A venture capital firm wants to invest $5 million in Artichoke Corp. ,a startup biotech firm.Artichoke is expected to go public in 4 years.Earnings will be negligible until year 4,but are projected to be $4 million in year 4.Comparable biotech firms are trading at P/E ratios of 18 on average.Artichoke has 3 million shares of stock outstanding.The VC firm will apply a discount rate of 40% to the investment.How many shares of stock should the VC firm be given for its $5 million investment?

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

36

Empirical evidence indicates that the returns to shareholders of the target firm vary significantly from the returns to the shareholders of the acquiring firm.Identify the shareholders that tend to realize the smaller return.Does your answer depend on the way the acquisition is financed?

Unlock Deck

Unlock for access to all 36 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 36 flashcards in this deck.