Deck 18: Integrated Audits of Public Companies

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

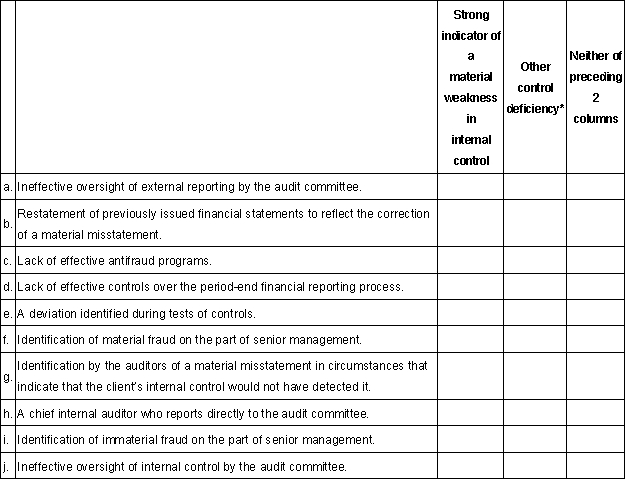

The PCAOB has outlined a number of circumstances that are indicators of a material weakness. In addition, other control deficiencies may or may not be a material weakness depending upon details of the circumstances involved. Categorize the following:  *May be material weakness, significant deficiency, or lesser deficiency, but is not ordinarily considered a strong indicator of a material weakness in internal control.

*May be material weakness, significant deficiency, or lesser deficiency, but is not ordinarily considered a strong indicator of a material weakness in internal control.

*May be material weakness, significant deficiency, or lesser deficiency, but is not ordinarily considered a strong indicator of a material weakness in internal control. Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/43

Play

Full screen (f)

Deck 18: Integrated Audits of Public Companies

1

An auditor's report on internal control ordinarily includes negative assurance on the effectiveness of internal control.

False

2

Assume that an auditor is focusing on two weaknesses in internal control. Although neither is by itself a material weakness, the two significant deficiencies in combination represent a material weakness. The client effectively remediates one of them prior to year-end but does not have time to remediate the other prior to year-end. What type of audit report on internal control is appropriate?

A) Adverse.

B) Qualified.

C) Unqualified.

D) Unqualified with explanatory language.

A) Adverse.

B) Qualified.

C) Unqualified.

D) Unqualified with explanatory language.

C

3

Which of the following is most likely to be considered a material weakness in internal control?

A) An ineffective control environment.

B) Restatement of previously issued financial statements due to a change in accounting principles.

C) Inadequate controls over non-systematic transactions.

D) Weaknesses in risk assessment.

A) An ineffective control environment.

B) Restatement of previously issued financial statements due to a change in accounting principles.

C) Inadequate controls over non-systematic transactions.

D) Weaknesses in risk assessment.

A

4

The lack of effective antifraud programs is always considered a material weakness.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

5

The Sarbanes-Oxley Act changed auditor association with a client's internal control from the review to the audit form of association.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

6

Which must management communicate to the audit committee?

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following is a weakness in internal control that allows a reasonable possibility that a significant (but less than material) misstatement may occur and not be detected?

A) Control deficiency.

B) Material weakness.

C) Reportable material item.

D) Significant deficiency.

A) Control deficiency.

B) Material weakness.

C) Reportable material item.

D) Significant deficiency.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

8

The amount involved with a significant deficiency is at least a material amount.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

9

A material weakness that exists at year-end will result in what type of audit report on internal control?

A) Adverse.

B) Qualified.

C) Unqualified.

D) Unqualified with explanatory language.

A) Adverse.

B) Qualified.

C) Unqualified.

D) Unqualified with explanatory language.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

10

A client imposed scope limitation relating to the audit of internal control ordinarily results in a qualified report.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

11

According to PCAOB standards, determining the allowance for doubtful accounts is referred to as a(n):

A) Substantive transaction.

B) Routine transaction.

C) Nonroutine transaction.

D) Accounting estimate transaction.

A) Substantive transaction.

B) Routine transaction.

C) Nonroutine transaction.

D) Accounting estimate transaction.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

12

Tests of operating effectiveness ordinarily include reperformance of the application of controls.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

13

Walk-throughs provide evidence that helps the auditor to:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

14

The framework most likely to be used by the client in its internal control assessment is the:

A) COSO internal control framework.

B) COSO enterprise risk management framework.

C) FASB 37 internal control definitional framework.

D) AICPA internal control analysis manager.

A) COSO internal control framework.

B) COSO enterprise risk management framework.

C) FASB 37 internal control definitional framework.

D) AICPA internal control analysis manager.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

15

The "as of date" for internal control reporting is ordinarily the last day of the fiscal year.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

16

Walk-throughs provide the auditors with evidence to:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

17

Which must the auditor communicate to management?

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

18

If management's report on internal control discloses a material weakness, the auditors (who agree that it is a material weakness) will issue a report that includes an adverse opinion.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

19

PCAOB standards suggest that auditors emphasize nonroutine transactions as contrasted to routine transactions in their consideration of internal control.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

20

Section 404 of the Sarbanes-Oxley Act of 2002 includes internal control reporting requirements for both management and auditors.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following must be included in management's report internal control under section 404 of the Sarbanes-Oxley Act of 2002?

A) It is management's responsibility to eliminate or publicly report on significant deficiencies in internal control.

B) A detailed description of the COSO criteria.

C) Management's assessment of the operating effectiveness for the period from the beginning to the end of the fiscal year under audit.

D) Identification of the framework used for evaluating internal control.

A) It is management's responsibility to eliminate or publicly report on significant deficiencies in internal control.

B) A detailed description of the COSO criteria.

C) Management's assessment of the operating effectiveness for the period from the beginning to the end of the fiscal year under audit.

D) Identification of the framework used for evaluating internal control.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following would most likely be included in a SEC 10K filing in which a material weakness in internal control exists?

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

23

A control deficiency that is less than a significant deficiency is most likely to result in what form of audit opinion on internal control?

A) Adverse.

B) Qualified.

C) Unqualified.

D) Unqualified with explanatory language.

A) Adverse.

B) Qualified.

C) Unqualified.

D) Unqualified with explanatory language.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

24

A material weakness involves a reasonable possibility that what size misstatement will not be prevented or detected?

A) Immaterial.

B) Material.

C) More than inconsequential.

D) Substantial.

A) Immaterial.

B) Material.

C) More than inconsequential.

D) Substantial.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

25

An auditor identified a material weakness in internal control in December. The client was informed and the client corrected the material weakness shortly after year-end (December 31); the auditor agrees that the correction eliminated the material weakness as of January 31. The appropriate audit report on internal control under PCAOB standards on reporting on internal control is:

A) Adverse.

B) Unqualified.

C) Unqualified with explanatory language relating to the material weakness.

D) Qualified.

A) Adverse.

B) Unqualified.

C) Unqualified with explanatory language relating to the material weakness.

D) Qualified.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

26

The minimum likelihood of loss involved in the consideration of a possible material weakness is:

A) Remote.

B) Reasonably possible.

C) Probable.

D) Not considered.

A) Remote.

B) Reasonably possible.

C) Probable.

D) Not considered.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

27

Which is least likely to be a question asked of employee personnel during a walk-through?

A) Have you ever been asked to override the process?

B) Have you assessed the operating effectiveness of the system?

C) What do you do when you find an error?

D) What are you looking for to determine if there is an error?

A) Have you ever been asked to override the process?

B) Have you assessed the operating effectiveness of the system?

C) What do you do when you find an error?

D) What are you looking for to determine if there is an error?

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following fits most directly under the control activities components of the COSO IC framework?

A) Company-level controls dealing with tone at the top.

B) Overall methods for assigning authority and responsibility.

C) The control environment.

D) Accounting for shipping documents to ensure that all sales are recorded.

A) Company-level controls dealing with tone at the top.

B) Overall methods for assigning authority and responsibility.

C) The control environment.

D) Accounting for shipping documents to ensure that all sales are recorded.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

29

According to PCAOB standards for reporting on internal control, calculating depreciation expense or adjusting for foreign currencies is referred to as:

A) Substantive transactions.

B) Routine transactions.

C) Nonroutine transactions.

D) Accounting Estimate transactions.

A) Substantive transactions.

B) Routine transactions.

C) Nonroutine transactions.

D) Accounting Estimate transactions.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

30

An auditor identified a significant deficiency in internal control in December. The client was informed and the client corrected the significant deficiency shortly before year-end (December 31); the auditor agrees that the correction eliminated the significant deficiency as of December 31. The appropriate audit report on internal control under a PCAOB Standard No. 5 audit of internal control is:

A) Adverse.

B) Unqualified.

C) Unqualified with explanatory language relating to the significant deficiency.

D) Qualified.

A) Adverse.

B) Unqualified.

C) Unqualified with explanatory language relating to the significant deficiency.

D) Qualified.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

31

Consider a company whose sales are initiated by customers either through the Internet or in a retail store. Which of the following is correct?

A) These types of sales represent two major classes of transactions within the sales process.

B) These types of sales represent two sales processes within a major evaluation processing cycle.

C) These sales represent a sales assertion on completeness.

D) These events represent nonroutine transactions that must be investigated in detail.

A) These types of sales represent two major classes of transactions within the sales process.

B) These types of sales represent two sales processes within a major evaluation processing cycle.

C) These sales represent a sales assertion on completeness.

D) These events represent nonroutine transactions that must be investigated in detail.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

32

The minimum likelihood of loss involved in the consideration of a control deficiency that is less than a significant deficiency is:

A) Remote.

B) More than remote.

C) Probable.

D) Not considered.

A) Remote.

B) More than remote.

C) Probable.

D) Not considered.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

33

An auditor identified a material weakness in internal control in August. The client was informed and the client corrected the material weakness prior to year-end (December 31); the auditor agrees that the correction eliminated the material weakness prior to year-end. The appropriate audit report on internal control under PCAOB standards on reporting on internal control is:

A) Adverse.

B) Unqualified.

C) Disclaimer.

D) Qualified.

A) Adverse.

B) Unqualified.

C) Disclaimer.

D) Qualified.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

34

A material weakness because the oversight of the external financial reporting function by the audit committee is ineffective will ordinarily result in communication to:

A) Option A

B) Option B

C) Option C

D) Option D

A) Option A

B) Option B

C) Option C

D) Option D

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

35

Deficiencies in internal control identified by the auditor that are lesser than significant deficiencies:

A) Must be communicated to the board of directors, the audit committee, and management.

B) Must be reported to the audit committee and management.

C) Must be communicated to management, with the audit committee only informed of the communication to management.

D) Need not be disclosed unless they in aggregate equal (at least) a significant deficiency.

A) Must be communicated to the board of directors, the audit committee, and management.

B) Must be reported to the audit committee and management.

C) Must be communicated to management, with the audit committee only informed of the communication to management.

D) Need not be disclosed unless they in aggregate equal (at least) a significant deficiency.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

36

Based on PCAOB standards for an internal control audit, which of the following is least likely to indicate a significant deficiency relating to a client's antifraud programs?

A) No program for anonymous submissions of alleged fraud.

B) Audit committee active engagement in discussions on the topic of fraud.

C) Senior management delegates to lower levels responsibility for oversight of antifraud programs.

D) Lack of audit committee interaction with the internal audit department.

A) No program for anonymous submissions of alleged fraud.

B) Audit committee active engagement in discussions on the topic of fraud.

C) Senior management delegates to lower levels responsibility for oversight of antifraud programs.

D) Lack of audit committee interaction with the internal audit department.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

37

The minimum likelihood of loss involved in the consideration of a possible significant deficiency is:

A) Remote.

B) Reasonably possible.

C) Probable.

D) Not considered.

A) Remote.

B) Reasonably possible.

C) Probable.

D) Not considered.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

38

Under PCAOB internal control reporting standards, what are the auditor's communication requirements to the audit committee with respect to material weaknesses?

A) All must be communicated in written form.

B) All must be communicated in written form or orally.

C) Only those that violate the Foreign Corrupt Practices Act need to be communicated, but in written form.

D) Only those that violate the Foreign Corrupt Practices Act need to be communicated, in written form or orally.

A) All must be communicated in written form.

B) All must be communicated in written form or orally.

C) Only those that violate the Foreign Corrupt Practices Act need to be communicated, but in written form.

D) Only those that violate the Foreign Corrupt Practices Act need to be communicated, in written form or orally.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following is a strong indicator that a material weakness in internal control exists?

A) Restatement of previously issued financial statements to reflect a correction.

B) Inadequate controls over non-routine transactions.

C) Inadequate controls over the period-end financial reporting process.

D) Weaknesses in a control activity.

A) Restatement of previously issued financial statements to reflect a correction.

B) Inadequate controls over non-routine transactions.

C) Inadequate controls over the period-end financial reporting process.

D) Weaknesses in a control activity.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

40

A circumstance caused scope limitation in a Sarbanes-Oxley 404 internal control audit is most likely to result in a(n):

A) Withdrawal from the engagement.

B) Disclaimer of opinion.

C) Unqualified opinion with explanatory language.

D) All of these are equally likely.

A) Withdrawal from the engagement.

B) Disclaimer of opinion.

C) Unqualified opinion with explanatory language.

D) All of these are equally likely.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

41

The existence of a material weakness led to an adverse opinion in the internal control audit report of a publicly traded company. Which of the following statements is correct if management believes that it has remediated the weakness?

A) Management may engage the auditors to report on whether the material weakness continues to exist prior to its next annual audit.

B) Management is required to engage the auditors to report on whether the material weakness continues to exist prior to its next annual audit.

C) Management may not engage the auditors to report on whether the material weakness continues to exist prior to its next annual audit.

D) Management may engage the auditors to modify the prior adverse audit report be modified to an unqualified report.

A) Management may engage the auditors to report on whether the material weakness continues to exist prior to its next annual audit.

B) Management is required to engage the auditors to report on whether the material weakness continues to exist prior to its next annual audit.

C) Management may not engage the auditors to report on whether the material weakness continues to exist prior to its next annual audit.

D) Management may engage the auditors to modify the prior adverse audit report be modified to an unqualified report.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

42

The PCAOB has outlined a number of circumstances that are indicators of a material weakness. In addition, other control deficiencies may or may not be a material weakness depending upon details of the circumstances involved. Categorize the following: *May be material weakness, significant deficiency, or lesser deficiency, but is not ordinarily considered a strong indicator of a material weakness in internal control.

*May be material weakness, significant deficiency, or lesser deficiency, but is not ordinarily considered a strong indicator of a material weakness in internal control. Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

43

An audit firm has been engaged to report on whether a material weakness that previously resulted in an adverse opinion on internal control has been remediated. Which of the following statements is correct?

A) A significant scope limitation on the auditor's procedures results in a qualified opinion or an adverse opinion.

B) If there has been an auditor change, the successor auditor may issue such a report.

C) If while performing the engagement another material weakness is identified, it will result in an adverse opinion relating to the current engagement to report upon the other material weakness.

D) The engagement may only take place at year-end during the next year's audit of internal control.

A) A significant scope limitation on the auditor's procedures results in a qualified opinion or an adverse opinion.

B) If there has been an auditor change, the successor auditor may issue such a report.

C) If while performing the engagement another material weakness is identified, it will result in an adverse opinion relating to the current engagement to report upon the other material weakness.

D) The engagement may only take place at year-end during the next year's audit of internal control.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 43 flashcards in this deck.