Deck 11: Translation and Consolidation of Foreign Operations

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

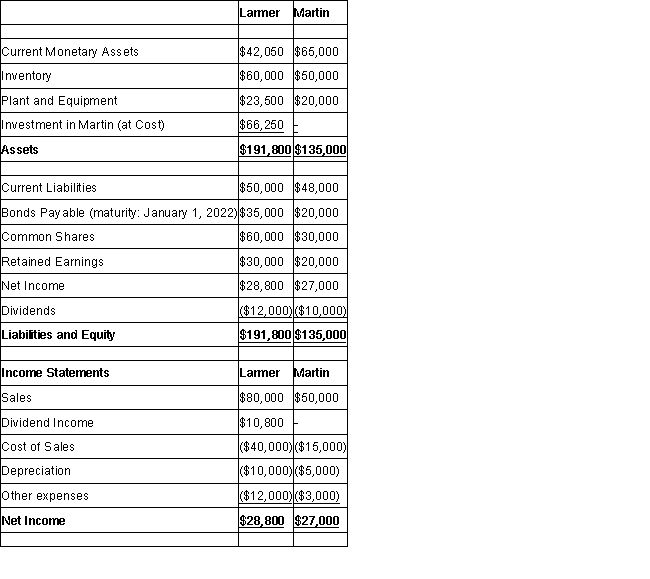

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Compute Martin's exchange gain or loss for 2017 if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Compute Martin's exchange gain or loss for 2017 if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Question

Question

Question

Question

Question

Question

Question

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Translate Martin's 2017 Income Statement into Canadian dollars if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Translate Martin's 2017 Income Statement into Canadian dollars if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Calculate Larmer's Consolidated Net Income for 2017 if Martin is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Calculate Larmer's Consolidated Net Income for 2017 if Martin is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent).

Question

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Compute Martin's exchange gain or loss for 2017 if Martin is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Compute Martin's exchange gain or loss for 2017 if Martin is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent).

Question

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Prepare Larmer's December 31, 2017 Consolidated Balance Sheet if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Prepare Larmer's December 31, 2017 Consolidated Balance Sheet if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Question

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Translate Martin's 2017 Income Statement into Canadian dollars if Martin is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Translate Martin's 2017 Income Statement into Canadian dollars if Martin is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent).

Question

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Translate Martin's December 31, 2017 Balance Sheet into Canadian dollars if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Translate Martin's December 31, 2017 Balance Sheet into Canadian dollars if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/65

Play

Full screen (f)

Deck 11: Translation and Consolidation of Foreign Operations

1

Under the presentation currency translation (PCT) method, which of the following statements is correct?

A) All balance sheet items excluding shareholders equity are translated using the closing rate in effect at the balance sheet date.

B) All balance sheet items are translated using the closing rate in effect at the balance sheet date.

C) All balance sheet items are translated using the average rate in effect throughout the year.

D)Only non-current balance sheet items are translated using the closing rate in effect at the balance sheet date.

A) All balance sheet items excluding shareholders equity are translated using the closing rate in effect at the balance sheet date.

B) All balance sheet items are translated using the closing rate in effect at the balance sheet date.

C) All balance sheet items are translated using the average rate in effect throughout the year.

D)Only non-current balance sheet items are translated using the closing rate in effect at the balance sheet date.

A

2

Which of the following statements is correct?

A) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), dividends must be translated using closing rates.

B) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), dividends must be translated using average rates.

C) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), dividends must be translated using historical rates.

D)If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), dividends must be translated using average rates.

A) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), dividends must be translated using closing rates.

B) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), dividends must be translated using average rates.

C) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), dividends must be translated using historical rates.

D)If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), dividends must be translated using average rates.

C

3

Which of the following statements is correct?

A) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), monetary items must be translated using closing rates.

B) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), monetary items must be translated using average rates.

C) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), shareholders' equity must be translated using closing rates.

D)If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), non-monetary items recorded at cost must be translated using average rates.

A) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), monetary items must be translated using closing rates.

B) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), monetary items must be translated using average rates.

C) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), shareholders' equity must be translated using closing rates.

D)If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), non-monetary items recorded at cost must be translated using average rates.

A

4

Which of the following statements is correct with respect to the translation of cost of sales in an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent)?

A) Opening inventory is translated using an average rate.

B) Opening inventory is translated using closing rates.

C) Ending inventory is translated using an average rate.

D)Ending inventory is translated using the rate in effect when the inventory was acquired.

A) Opening inventory is translated using an average rate.

B) Opening inventory is translated using closing rates.

C) Ending inventory is translated using an average rate.

D)Ending inventory is translated using the rate in effect when the inventory was acquired.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following statements is correct?

A) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), depreciation and amortization must be translated using closing rates.

B) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), depreciation and amortization must be translated using average rates.

C) If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent), depreciation and amortization must be translated using historical rates.

D)If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), depreciation and amortization must be translated using closing rates.

A) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), depreciation and amortization must be translated using closing rates.

B) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), depreciation and amortization must be translated using average rates.

C) If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent), depreciation and amortization must be translated using historical rates.

D)If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), depreciation and amortization must be translated using closing rates.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

6

Under the presentation currency translation (PCT) method, which of the following statements is correct?

A) Transaction exposure is greatest.

B) The relationship of balance sheet items is best preserved.

C) Income statement items are translated using a mix of rates.

D)Income statement items are translated using average rates.

A) Transaction exposure is greatest.

B) The relationship of balance sheet items is best preserved.

C) Income statement items are translated using a mix of rates.

D)Income statement items are translated using average rates.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following statements is correct?

A) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), non-monetary items recorded at cost must be translated using historical rates.

B) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), non-monetary items recorded at cost must be translated using average rates.

C) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), non-monetary items recorded at cost must be translated using closing rates.

D)If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), non-monetary items recorded at cost must be translated using closing rates.

A) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), non-monetary items recorded at cost must be translated using historical rates.

B) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), non-monetary items recorded at cost must be translated using average rates.

C) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), non-monetary items recorded at cost must be translated using closing rates.

D)If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), non-monetary items recorded at cost must be translated using closing rates.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following rates would be used to translate the company's income statement items?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

9

The risk exposure resulting from the translation of foreign-currency-denominated financial risks is referred to as:

A) translation (accounting) exposure.

B) transaction exposure.

C) economic exposure.

D)business risk.

A) translation (accounting) exposure.

B) transaction exposure.

C) economic exposure.

D)business risk.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

10

For a self-sustaining foreign operation (i.e., the functional currency of the foreign operation is different than the parent), exchange gains and losses are to be included in or along with:

A) other comprehensive income.

B) an exchange account.

C) non-controlling interest.

D)the acquisition differential amortization.

A) other comprehensive income.

B) an exchange account.

C) non-controlling interest.

D)the acquisition differential amortization.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following rates would be used to translate the company's Assets and Liabilities?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following rates would be used to translate the company's Retained Earnings at the start of the year?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

13

The risk exposure that occurs between the time of entering into a transaction and the time of settling it is referred to as:

A) translation (accounting) exposure.

B) transaction exposure.

C) economic exposure.

D)business risk.

A) translation (accounting) exposure.

B) transaction exposure.

C) economic exposure.

D)business risk.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following statements is correct?

A) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), contributed capital must be translated using closing rates.

B) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), contributed capital must be translated using average rates.

C) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), contributed capital must be translated using historical rates.

D)If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), contributed capital must be translated using average rates.

A) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), contributed capital must be translated using closing rates.

B) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), contributed capital must be translated using average rates.

C) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), contributed capital must be translated using historical rates.

D)If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), contributed capital must be translated using average rates.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

15

If the functional currency of the foreign entity is the same as the parent's functional currency, which of the following statements is correct?

A) The foreign entity is classified as integrated.

B) The foreign entity is classified as self-sustaining.

C) The foreign entity is classified as a foreign affiliate.

D)The investment in the foreign entity is classified as a non-monetary asset.

A) The foreign entity is classified as integrated.

B) The foreign entity is classified as self-sustaining.

C) The foreign entity is classified as a foreign affiliate.

D)The investment in the foreign entity is classified as a non-monetary asset.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following rates would be used to translate the company's Dividends paid during the year?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8125

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8125

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following rates would be used to translate the company's Common Shares?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

18

Under the functional currency translation (FCT) method, which of the following statements is correct?

A) The relationship of balance sheet items is best preserved.

B) A single historic rate is used to translate all income statement items.

C) A net asset exposure is most likely.

D)Historic rates are used to translate most non-monetary items.

A) The relationship of balance sheet items is best preserved.

B) A single historic rate is used to translate all income statement items.

C) A net asset exposure is most likely.

D)Historic rates are used to translate most non-monetary items.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following statements is correct?

A) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), non-monetary items recorded at closing values must be translated using closing rates.

B) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), non-monetary items recorded at closing values must be translated using average rates.

C) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), non-monetary items recorded at closing values must be translated using historical rates.

D)If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), non-monetary items recorded at closing values must be translated using average rates.

A) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), non-monetary items recorded at closing values must be translated using closing rates.

B) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), non-monetary items recorded at closing values must be translated using average rates.

C) If an organization is self-sustaining (i.e., the functional currency of the foreign operation is different than the parent), non-monetary items recorded at closing values must be translated using historical rates.

D)If an organization is considered an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), non-monetary items recorded at closing values must be translated using average rates.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

20

The risk exposure resulting from the possible reduction in terms of the domestic reporting foreign currency, of the discounted future cash flows generated from foreign investments or operations due to real changes in exchange rates is referred to as:

A) translation (accounting) exposure.

B) transaction exposure.

C) economic exposure.

D)business risk.

A) translation (accounting) exposure.

B) transaction exposure.

C) economic exposure.

D)business risk.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

21

If the bonds were outstanding throughout the year, which of the following rates would be used to translate the company's bond interest expense for the year?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following rates would be used to translate the company's other expenses?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following rates would be used to translate the company's bonds payable?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following statements is FALSE?

A) If a subsidiary is self-sustaining, the method of valuation of assets and liabilities is of no consequence in the translation because all of the assets are translated at the closing rate.

B) If a subsidiary is an integrated foreign subsidiary, the method of valuation of assets and liabilities is of no consequence in the translation because all of the assets are translated at the closing rate.

C) If a subsidiary is an integrated foreign subsidiary, a write-down to market may be required in the translated financial statements.

D)If a subsidiary is an integrated foreign subsidiary, no write-down is required in the foreign currency financial statements.

A) If a subsidiary is self-sustaining, the method of valuation of assets and liabilities is of no consequence in the translation because all of the assets are translated at the closing rate.

B) If a subsidiary is an integrated foreign subsidiary, the method of valuation of assets and liabilities is of no consequence in the translation because all of the assets are translated at the closing rate.

C) If a subsidiary is an integrated foreign subsidiary, a write-down to market may be required in the translated financial statements.

D)If a subsidiary is an integrated foreign subsidiary, no write-down is required in the foreign currency financial statements.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

25

According to IAS 29 Financial Reporting in Hyperinflationary Economies, the term "hyper-inflationary" means:

A) an annual inflation rate of 50%.

B) an annual inflation rate of 100%.

C) a cumulative inflation rate of 100% over a 3-5 year period.

D)it does not establish an absolute rate which is deemed to be hyper-inflation.

A) an annual inflation rate of 50%.

B) an annual inflation rate of 100%.

C) a cumulative inflation rate of 100% over a 3-5 year period.

D)it does not establish an absolute rate which is deemed to be hyper-inflation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

26

For the sake of simplicity, assume once again that US1's cost of sales was calculated to be CDN$3,000,000. What is the amount (in Canadian dollars) of US1's net income?

A) $300,000.

B) $301,500.

C) $302,500.

D)$412,500.

A) $300,000.

B) $301,500.

C) $302,500.

D)$412,500.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following rates would be used to translate the company's dividends?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8125

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8125

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following rates would be used to translate the company's cash?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following rates would be used to translate the company's sales?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = $0.83 CDN

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = $0.83 CDN

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

30

For the sake of simplicity, assume once again that US1's cost of sales was calculated to be CDN$3,000,000. What is the amount (in Canadian dollars) of US1's retained earnings at December 31, 2017?

A) $545,000.

B) $546,250.

C) $547,250.

D)$660,000.

A) $545,000.

B) $546,250.

C) $547,250.

D)$660,000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

31

If the company had no capital asset additions or disposals in 2017, which of the following rates would be used to translate the company's depreciation expense for the year?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following rates would be used to translate the company's current liabilities?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following rates would be used to translate the company's beginning retained earnings?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

34

What is the amount of the gain or loss arising from translation?

A) A CDN$5,000 loss.

B) A CDN$750 loss.

C) A CDN$307 loss.

D)A CDN$3,750 gain.

A) A CDN$5,000 loss.

B) A CDN$750 loss.

C) A CDN$307 loss.

D)A CDN$3,750 gain.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following is an indication that the functional currency of a foreign subsidiary is not the Canadian dollar?

A) Only goods imported from the parent are sold by the subsidiary.

B) The parent dictates the subsidiary's operating procedures.

C) Cash to pay obligations is generated by local operations or borrowed from local lenders.

D)Intercompany transactions account for a high proportion of the subsidiary's overall activities.

A) Only goods imported from the parent are sold by the subsidiary.

B) The parent dictates the subsidiary's operating procedures.

C) Cash to pay obligations is generated by local operations or borrowed from local lenders.

D)Intercompany transactions account for a high proportion of the subsidiary's overall activities.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

36

Which of the following rates would be used to translate the company's accounts receivable?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

37

If there were no additions or disposals of plant and equipment in 2017, which of the following rates would be used to translate the company's plant and equipment?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following statements is correct?

A) If a foreign currency weakens with respect to the Canadian dollar, both self-sustaining and integrated foreign subsidiaries will show a foreign exchange gain.

B) If a foreign currency weakens with respect to the Canadian dollar, both self-sustaining and integrated foreign subsidiaries will show a foreign exchange loss.

C) If a foreign currency weakens with respect to the Canadian dollar, a self-sustaining subsidiary will show a foreign exchange gain while an integrated foreign subsidiary will show a foreign exchange loss.

D)If a foreign currency weakens with respect to the Canadian dollar, a self-sustaining subsidiary will show a foreign exchange loss while an integrated foreign subsidiary will show a foreign exchange gain.

A) If a foreign currency weakens with respect to the Canadian dollar, both self-sustaining and integrated foreign subsidiaries will show a foreign exchange gain.

B) If a foreign currency weakens with respect to the Canadian dollar, both self-sustaining and integrated foreign subsidiaries will show a foreign exchange loss.

C) If a foreign currency weakens with respect to the Canadian dollar, a self-sustaining subsidiary will show a foreign exchange gain while an integrated foreign subsidiary will show a foreign exchange loss.

D)If a foreign currency weakens with respect to the Canadian dollar, a self-sustaining subsidiary will show a foreign exchange loss while an integrated foreign subsidiary will show a foreign exchange gain.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following rates would be used to translate the company's common shares?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following rates would be used to translate the company's inventory?

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

A) US$1 = CDN$0.815

B) US$1 = CDN$0.8175

C) US$1 = CDN$0.825

D)US$1 = CDN$0.83

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

41

Translate Wilsen's December 31, 2017 Statement of Retained Earnings if Wilsen was considered to be a self-sustaining foreign operation (i.e., the functional currency of the foreign operation is different than the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

42

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Compute Martin's exchange gain or loss for 2017 if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Compute Martin's exchange gain or loss for 2017 if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

43

If Maker is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), what amount will be shown for capital assets (net) on its translated Canadian dollar financial statements as at December 31, 2016?

A) $168,000.

B) $169,600.

C) $170,000.

D)$170,400.

A) $168,000.

B) $169,600.

C) $170,000.

D)$170,400.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

44

If Maker is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent), what amount will be shown for capital assets (net) on its translated Canadian dollar financial statements as at December 31, 2017?

A) $212,500.

B) $224,430.

C) $225,830.

D)$228,438.

A) $212,500.

B) $224,430.

C) $225,830.

D)$228,438.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

45

If Maker is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), what amount will be shown for amortization expense on Holdings consolidated income statements for the year ended on December 31, 2017?

A) $27,500.

B) $29,010.

C) $29,210.

D)$29,425.

A) $27,500.

B) $29,010.

C) $29,210.

D)$29,425.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

46

If Maker is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent), what amount will be shown for amortization expense on its translated Canadian dollar financial statements as at December 31, 2016?

A) $20,000.

B) $21,000.

C) $21,200.

D)$21,250.

A) $20,000.

B) $21,000.

C) $21,200.

D)$21,250.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

47

Calculate the exchange gain or loss that would result from the translation of Wilsen's Financial Statements if Wilsen was considered to be a self-sustaining foreign operation (i.e., the functional currency of the foreign operation is different than the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

48

Translate Wilsen's 2017 Income Statement if Wilsen was considered to be a self-sustaining foreign operation (i.e., the functional currency of the foreign operation is different than the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

49

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Translate Martin's 2017 Income Statement into Canadian dollars if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Translate Martin's 2017 Income Statement into Canadian dollars if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

50

Translate Wilsen's December 31, 2017 Balance Sheet if Wilsen is considered to be an integrated foreign operation (i.e., the functional currency of the foreign operation is the same as the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

51

If Maker is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent), what amount will be shown for amortization expense on its translated Canadian dollar financial statements as at December 31, 2017?

A) $32,500.

B) $34,510.

C) $34,775.

D)$34,938.

A) $32,500.

B) $34,510.

C) $34,775.

D)$34,938.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

52

Compute Wilsen's exchange gain or loss for 2017 if Wilson is considered to be an integrated subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

53

Translate Wilsen's December 31, 2017 Balance Sheet if Wilsen was considered to be a self-sustaining foreign operation (i.e., the functional currency of the foreign operation is different than the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

54

Translate Wilsen's 2014 Income Statement if Wilsen is considered to be an integrated subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

55

If Maker is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), what amount will be shown for capital assets (net) on its translated Canadian dollar financial statements as at December 31, 2017?

A) $212,500.

B) $224,430.

C) $225,830.

D)$228,438.

A) $212,500.

B) $224,430.

C) $225,830.

D)$228,438.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

56

If Maker is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent), what amount will be shown for amortization expense on its translated Canadian dollar financial statements as at December 31, 2016?

A) $20,000.

B) $21,000.

C) $21,200.

D)$21,250.

A) $20,000.

B) $21,000.

C) $21,200.

D)$21,250.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

57

If Maker is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent), what amount will be shown for amortization expense on its translated Canadian dollar financial statements as at December 31, 2017?

A) $27,500.

B) $29,010.

C) $29,210.

D)$29,425.

A) $27,500.

B) $29,010.

C) $29,210.

D)$29,425.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

58

Translate Wilsen's December 31, 2017 Statement of Retained Earnings if Wilsen is considered to be an integrated subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

59

If Maker is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent), what amount will be shown for capital assets (net) on its translated Canadian dollar financial statements as at December 31, 2016?

A) $168,000.

B) $169,600.

C) $170,000.

D)$170,400.

A) $168,000.

B) $169,600.

C) $170,000.

D)$170,400.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

60

A foreign subsidiary is considered to be an integrated foreign operation (i.e., the functional currency of the foreign operation is the same as the parent), and its income is earned evenly over the year. It paid its income taxes for the year in two instalments, half on June 30 and half on December 31. What rate(s) should be used to translate the company's income tax expense into Canadian dollars when preparing translated financial statements for the year?

A) Half at the rate at June 30 and half at the rate at December 31.

B) All at the average rate for the year.

C) All at the closing rate for the year.

D)All at the opening rate for the year.

A) Half at the rate at June 30 and half at the rate at December 31.

B) All at the average rate for the year.

C) All at the closing rate for the year.

D)All at the opening rate for the year.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

61

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Calculate Larmer's Consolidated Net Income for 2017 if Martin is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Calculate Larmer's Consolidated Net Income for 2017 if Martin is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

62

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Compute Martin's exchange gain or loss for 2017 if Martin is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Compute Martin's exchange gain or loss for 2017 if Martin is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

63

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Prepare Larmer's December 31, 2017 Consolidated Balance Sheet if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Prepare Larmer's December 31, 2017 Consolidated Balance Sheet if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

64

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Translate Martin's 2017 Income Statement into Canadian dollars if Martin is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Translate Martin's 2017 Income Statement into Canadian dollars if Martin is considered to be a self-sustaining foreign subsidiary (i.e., the functional currency of the foreign operation is different than the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

65

On January 1, 2017, Larmer Corp. (a Canadian company) purchased 80% of Martin Inc, an American company, for US$50,000.

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Translate Martin's December 31, 2017 Balance Sheet into Canadian dollars if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Martin's book values approximated its fair values on that date except for plant and equipment, which had a fair value of US$30,000 with a remaining life expectancy of 5 years. A goodwill impairment loss of US$1,000 occurred during 2017. Martin's January 1, 2017 Balance Sheet is shown below (in U.S. dollars): The following exchange rates were in effect during 2017:

Dividends declared and paid December 31, 2017.

The financial statements of Larmer (in Canadian dollars) and Martin (in U.S. dollars) are shown below:

Balance Sheets

-Translate Martin's December 31, 2017 Balance Sheet into Canadian dollars if Martin is considered to be an integrated foreign subsidiary (i.e., the functional currency of the foreign operation is the same as the parent).

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 65 flashcards in this deck.