Deck 5: Activity-Based Costing and Management

Full screen (f)

Question

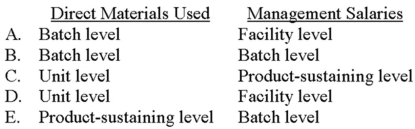

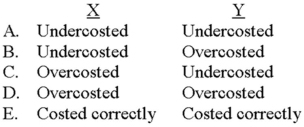

Which of the following choices correctly depicts the proper classification of direct materials used and management salaries?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

Question

Question

Question

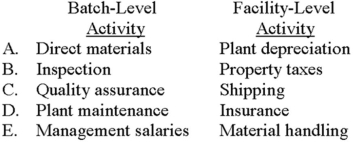

Which of the following choices correctly depicts a cost that arises from a batch-level activity and one that arises from a facility-level activity?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Riverside Florists uses an activity-based costing system to compute the cost of making floral bouquets and delivering the bouquets to its commercial customers. Company personnel who earn $180,000 typically perform both tasks; other firm-wide overhead is expected to total $70,000. These costs are allocated as follows:  Riverside anticipates making 20,000 bouquets and 4,000 deliveries in the upcoming year.

Riverside anticipates making 20,000 bouquets and 4,000 deliveries in the upcoming year.

The cost of wages and salaries and other overhead that would be charged to each bouquet made is:

A) $7.15.

B) $8.75.

C) $12.50.

D) $13.75.

E) None of the other answers is correct.

Riverside anticipates making 20,000 bouquets and 4,000 deliveries in the upcoming year.The cost of wages and salaries and other overhead that would be charged to each bouquet made is:

A) $7.15.

B) $8.75.

C) $12.50.

D) $13.75.

E) None of the other answers is correct.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Koski manufactures products J and K, applying overhead on the basis of labor hours. J, a low-volume product, requires a variety of complex manufacturing procedures. K, on the other hand, is both a high-volume product and relatively simplistic in nature. What would an activity-based costing system likely disclose about products J and K as a result of Koski's current accounting procedures?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

Question

Question

Question

Question

Question

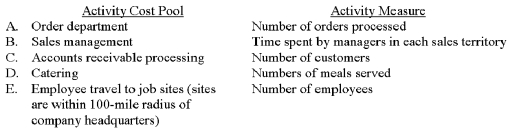

Which of the following activity cost pools and activity measures likely has the lowest degree of correlation?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

Question

Jackson manufactures products X and Y, applying overhead on the basis of labor hours. X, a low-volume product, requires a variety of complex manufacturing procedures. Y, on the other hand, is both a high-volume product and relatively simplistic in nature. What would an activity-based costing system likely disclose about products X and Y as a result of Jackson's current accounting procedures?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

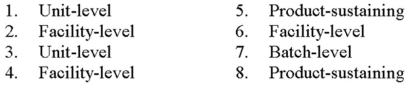

Consider the following costs that relate to a bank and a manufacturer of software:

Bank

1. Review costs of commercial loan applications

2. Operating costs of human resources department

3. Immediate processing costs of a specific customer's cash deposit

4. Bank membership costs of joining local Chamber of Commerce

Software manufacturer

5. Label and packaging charges from a commercial printer for a new software release

6. Air conditioning/heating costs of the firm's production plant

7. Transport costs of moving the finished products from production run no. 1 to the company's warehouse

8. Design and development costs of new spreadsheet software

Required:

A.

A. Classify the eight costs listed as arising from either a unit-level, batch-level, product-sustaining, or facility-level activity.

B. The number of loan applications would be more appropriate because it has a higher correlation with the amount of review costs incurred. Applications create review costs; customers, on the other hand, may not.

B. Would number of loan applications or number of customers be a more appropriate cost-driver base for #1 above? Briefly explain.

Bank

1. Review costs of commercial loan applications

2. Operating costs of human resources department

3. Immediate processing costs of a specific customer's cash deposit

4. Bank membership costs of joining local Chamber of Commerce

Software manufacturer

5. Label and packaging charges from a commercial printer for a new software release

6. Air conditioning/heating costs of the firm's production plant

7. Transport costs of moving the finished products from production run no. 1 to the company's warehouse

8. Design and development costs of new spreadsheet software

Required:

A.

A. Classify the eight costs listed as arising from either a unit-level, batch-level, product-sustaining, or facility-level activity.

B. The number of loan applications would be more appropriate because it has a higher correlation with the amount of review costs incurred. Applications create review costs; customers, on the other hand, may not.

B. Would number of loan applications or number of customers be a more appropriate cost-driver base for #1 above? Briefly explain.

Question

Question

Question

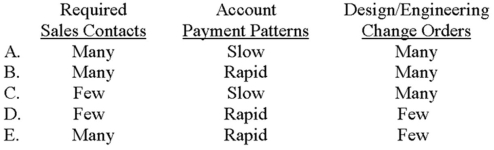

Hilton Corporation's customers differ greatly with respect to number of required sales contacts (e.g., phone calls and sales visits), account payment patterns, and design/engineering change orders. Which of the following choices likely denotes an ideal customer from Hilton's perspective?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/85

Play

Full screen (f)

Deck 5: Activity-Based Costing and Management

1

Which of the following choices correctly depicts the proper classification of direct materials used and management salaries?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

D

2

Generally speaking, companies prefer doing business with customers who order small quantities rather than large quantities.

False

3

Which of the following tasks is not normally associated with an activity-based costing system?

A) Calculation of pool rates.

B) Identification of cost pools.

C) Preparation of allocation matrices.

D) Identification of cost drivers.

E) Assignment of cost to products.

A) Calculation of pool rates.

B) Identification of cost pools.

C) Preparation of allocation matrices.

D) Identification of cost drivers.

E) Assignment of cost to products.

C

4

Feinstein, Inc., an appliance manufacturer, is developing a new line of ovens that uses controlled-laser technology. The research and testing costs associated with the new ovens is said to arise from a:

A) unit-level activity.

B) batch-level activity.

C) product-sustaining activity.

D) facility-level activity.

E) competitive-level activity.

A) unit-level activity.

B) batch-level activity.

C) product-sustaining activity.

D) facility-level activity.

E) competitive-level activity.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following choices correctly depicts a cost that arises from a batch-level activity and one that arises from a facility-level activity?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

6

The following tasks are associated with an activity-based costing system:

1- Assignment of cost to products

2- Calculation of pool rates

3- Identification of cost drivers

4- Identification of cost pools

Which of the following choices correctly expresses the proper order of the preceding tasks?

A) 1, 2, 3, 4.

B) 2, 4, 1, 3.

C) 3, 4, 2, 1.

D) 4, 2, 1, 3.

E) 4, 3, 2, 1.

1- Assignment of cost to products

2- Calculation of pool rates

3- Identification of cost drivers

4- Identification of cost pools

Which of the following choices correctly expresses the proper order of the preceding tasks?

A) 1, 2, 3, 4.

B) 2, 4, 1, 3.

C) 3, 4, 2, 1.

D) 4, 2, 1, 3.

E) 4, 3, 2, 1.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

7

An example of a customer-value-added activity is final painting and polishing of the product.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

8

Consider the following statements regarding product-sustaining activities:

I) They must be performed for each batch of product that is made.

II) They must be performed for each unit of product that is made.

III) They are needed to support an entire product line.

Which of the above statements is (are) true?

A) I only.

B) II only.

C) III only.

D) I and II.

E) II and III.

I) They must be performed for each batch of product that is made.

II) They must be performed for each unit of product that is made.

III) They are needed to support an entire product line.

Which of the above statements is (are) true?

A) I only.

B) II only.

C) III only.

D) I and II.

E) II and III.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following is not a broad, cost classification category typically used in activity-based costing?

A) Unit-level.

B) Batch-level.

C) Product-sustaining level.

D) Facility-level.

E) Management-level.

A) Unit-level.

B) Batch-level.

C) Product-sustaining level.

D) Facility-level.

E) Management-level.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following is the proper sequence of events in an activity-based costing system?

A) Identification of cost drivers, identification of cost pools, calculation of pool rates, assignment of cost to products.

B) Identification of cost pools, identification of cost drivers, calculation of pool rates, assignment of cost to products.

C) Assignment of cost to products, identification of cost pools, identification of cost drivers, calculation of pool rates.

D) Calculation of pool rates, identification of cost drivers, identification of cost pools, assignment of cost to products.

E) None of the other answers is correct.

A) Identification of cost drivers, identification of cost pools, calculation of pool rates, assignment of cost to products.

B) Identification of cost pools, identification of cost drivers, calculation of pool rates, assignment of cost to products.

C) Assignment of cost to products, identification of cost pools, identification of cost drivers, calculation of pool rates.

D) Calculation of pool rates, identification of cost drivers, identification of cost pools, assignment of cost to products.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following is least likely to be classified as a batch-level activity in an activity-based costing system?

A) Shipping.

B) Receiving and inspection.

C) Production setup.

D) Property taxes.

E) Quality assurance.

A) Shipping.

B) Receiving and inspection.

C) Production setup.

D) Property taxes.

E) Quality assurance.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

12

Many traditional costing systems:

A) trace manufacturing overhead to individual activities and require the development of numerous activity-costing rates.

B) write off manufacturing overhead as an expense of the current period.

C) combine widely varying elements of overhead into a single cost pool.

D) use a host of different cost drivers (e.g., number of production setups, inspection hours, orders processed) to improve the accuracy of product costing.

E) produce results far superior to those achieved with activity-based costing.

A) trace manufacturing overhead to individual activities and require the development of numerous activity-costing rates.

B) write off manufacturing overhead as an expense of the current period.

C) combine widely varying elements of overhead into a single cost pool.

D) use a host of different cost drivers (e.g., number of production setups, inspection hours, orders processed) to improve the accuracy of product costing.

E) produce results far superior to those achieved with activity-based costing.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

13

In an activity-based costing system, direct materials used would typically be classified as a unit-level cost.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

14

Activity-based costing systems have a tendency to distort product costs.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

15

The salaries of a manufacturing plant's management are said to arise from:

A) unit-level activities.

B) batch-level activities.

C) product-sustaining activities.

D) facility-level activities.

E) direct-cost activities.

A) unit-level activities.

B) batch-level activities.

C) product-sustaining activities.

D) facility-level activities.

E) direct-cost activities.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

16

Consider the following statements regarding traditional costing systems:

I) Overhead costs are applied to products on the basis of volume-related measures.

II) All manufacturing costs are easily traceable to the goods produced.

III) Traditional costing systems tend to distort unit manufacturing costs when numerous goods are made that have widely varying production requirements.

Which of the above statements is (are) true?

A) I only.

B) II only.

C) III only.

D) I and III.

E) II and III.

I) Overhead costs are applied to products on the basis of volume-related measures.

II) All manufacturing costs are easily traceable to the goods produced.

III) Traditional costing systems tend to distort unit manufacturing costs when numerous goods are made that have widely varying production requirements.

Which of the above statements is (are) true?

A) I only.

B) II only.

C) III only.

D) I and III.

E) II and III.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

17

In an activity-based costing system, direct materials used would typically be classified as a:

A) unit-level cost.

B) batch-level cost.

C) product-sustaining cost.

D) facility-level cost.

E) matrix-level cost.

A) unit-level cost.

B) batch-level cost.

C) product-sustaining cost.

D) facility-level cost.

E) matrix-level cost.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

18

In an activity-based costing system, materials receiving would typically be classified as a:

A) unit-level activity.

B) batch-level activity.

C) product-sustaining activity.

D) facility-level activity.

E) period-level activity.

A) unit-level activity.

B) batch-level activity.

C) product-sustaining activity.

D) facility-level activity.

E) period-level activity.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is least likely to be classified as a facility-level activity in an activity-based costing system?

A) Plant maintenance.

B) Property taxes.

C) Machine processing cost.

D) Plant depreciation.

E) Plant management salaries.

A) Plant maintenance.

B) Property taxes.

C) Machine processing cost.

D) Plant depreciation.

E) Plant management salaries.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

20

Consumption ratios are useful in determining the existence of product-line diversity.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

21

Under an activity-based costing system, what is the per-unit overhead cost of Standard?

A) $164.

B) $228.

C) $272.

D) $282.

E) None of the other answers is correct.

A) $164.

B) $228.

C) $272.

D) $282.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

22

St. James, Inc., currently uses traditional costing procedures, applying $800,000 of overhead to products Beta and Zeta on the basis of direct labor hours. The company is considering a shift to activity-based costing and the creation of individual cost pools that will use direct labor hours (DLH), production setups (SU), and number of parts components (PC) as cost drivers. Data on the cost pools and respective driver volumes follow. The overhead cost allocated to Zeta by using traditional costing procedures would be:

A) $240,000.

B) $356,000.

C) $444,000.

D) $560,000.

E) None of the other answers is correct.

A) $240,000.

B) $356,000.

C) $444,000.

D) $560,000.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

23

Assume that HiTech is using a volume-based costing system, and the preceding overhead costs are applied to all products on the basis of direct labor hours. The overhead cost that would be assigned to the Standard product line is closest to:

A) $456,471.

B) $646,471.

C) $961,176.

D) $1,141,176.

E) None of the other answers is correct.

A) $456,471.

B) $646,471.

C) $961,176.

D) $1,141,176.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

24

Alaina's customer service department follows up on customer complaints by telephone inquiry. During a recent period, the department initiated 10,000 calls and incurred costs of $312,000. Of these calls, 3,800 were for the company's wholesale operation; the remainder was for the retail division. Costs allocated to the wholesale operation are:

A) $0.

B) $31,200.

C) $118,560.

D) $193,440.

E) $203,000.

A) $0.

B) $31,200.

C) $118,560.

D) $193,440.

E) $203,000.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

25

Assume that HiTech is using a volume-based costing system, and the preceding overhead costs are applied to all products on the basis of direct labor hours. The overhead cost that would be assigned to the Deluxe product line is closest to:

A) $456,471.

B) $646,471.

C) $961,176.

D) $1,141,176.

E) None of the other answers is correct.

A) $456,471.

B) $646,471.

C) $961,176.

D) $1,141,176.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

26

Riverside Florists uses an activity-based costing system to compute the cost of making floral bouquets and delivering the bouquets to its commercial customers. Company personnel who earn $180,000 typically perform both tasks; other firm-wide overhead is expected to total $70,000. These costs are allocated as follows: Riverside anticipates making 20,000 bouquets and 4,000 deliveries in the upcoming year.

The cost of wages and salaries and other overhead that would be charged to each delivery is closest to:

A) $19.63.

B) $20.31.

C) $26.75.

D) $40.63.

E) None of the other answers is correct.

The cost of wages and salaries and other overhead that would be charged to each delivery is closest to:

A) $19.63.

B) $20.31.

C) $26.75.

D) $40.63.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

27

Aladdin's customer service department follows up on customer complaints by telephone inquiry. During a recent period, the department initiated 7,000 calls and incurred costs of $203,000. If 2,940 of these calls were for the company's wholesale operation (the remainder were for the retail division), costs allocated to the wholesale operation should amount to:

A) $0.

B) $29.

C) $85,260.

D) $117,740.

E) $203,000.

A) $0.

B) $29.

C) $85,260.

D) $117,740.

E) $203,000.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

28

HiTech Products manufactures three types of remote-control devices: Economy, Standard, and Deluxe. The company, which uses activity-based costing, has identified five activities (and related cost drivers). Each activity, its budgeted cost, and related cost driver is identified below. The following information pertains to the three product lines for next year:

What is HiTech's pool rate for the finishing activity?

A) $5.00 per labor hour.

B) $5.00 per machine hour.

C) $5.00 per unit.

D) $7.50 per unit.

E) None of the other answers is correct.

What is HiTech's pool rate for the finishing activity?

A) $5.00 per labor hour.

B) $5.00 per machine hour.

C) $5.00 per unit.

D) $7.50 per unit.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

29

St. James, Inc., currently uses traditional costing procedures, applying $800,000 of overhead to products Beta and Zeta on the basis of direct labor hours. The company is considering a shift to activity-based costing and the creation of individual cost pools that will use direct labor hours (DLH), production setups (SU), and number of parts components (PC) as cost drivers. Data on the cost pools and respective driver volumes follow. The overhead cost allocated to Beta by using activity-based costing procedures would be:

A) $240,000.

B) $356,000.

C) $444,000.

D) $560,000.

E) None of the other answers is correct.

A) $240,000.

B) $356,000.

C) $444,000.

D) $560,000.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

30

Under an activity-based costing system, what is the per-unit overhead cost of Deluxe?

A) $272.

B) $282.

C) $320.

D) $440.

E) None of the other answers is correct.

A) $272.

B) $282.

C) $320.

D) $440.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

31

St. James, Inc., currently uses traditional costing procedures, applying $800,000 of overhead to products Beta and Zeta on the basis of direct labor hours. The company is considering a shift to activity-based costing and the creation of individual cost pools that will use direct labor hours (DLH), production setups (SU), and number of parts components (PC) as cost drivers. Data on the cost pools and respective driver volumes follow. The overhead cost allocated to Zeta by using activity-based costing procedures would be:

A) $240,000.

B) $356,000.

C) $444,000.

D) $560,000.

E) None of the other answers is correct.

A) $240,000.

B) $356,000.

C) $444,000.

D) $560,000.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

32

Riverside Florists uses an activity-based costing system to compute the cost of making floral bouquets and delivering the bouquets to its commercial customers. Company personnel who earn $180,000 typically perform both tasks; other firm-wide overhead is expected to total $70,000. These costs are allocated as follows: Riverside anticipates making 20,000 bouquets and 4,000 deliveries in the upcoming year.

The cost of wages and salaries and other overhead that would be charged to each bouquet made is:

A) $7.15.

B) $8.75.

C) $12.50.

D) $13.75.

E) None of the other answers is correct.

Riverside anticipates making 20,000 bouquets and 4,000 deliveries in the upcoming year.The cost of wages and salaries and other overhead that would be charged to each bouquet made is:

A) $7.15.

B) $8.75.

C) $12.50.

D) $13.75.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

33

HiTech Products manufactures three types of remote-control devices: Economy, Standard, and Deluxe. The company, which uses activity-based costing, has identified five activities (and related cost drivers). Each activity, its budgeted cost, and related cost driver is identified below. The following information pertains to the three product lines for next year:

What is HiTech's pool rate for the material-handling activity?

A) $1.00 per part.

B) $2.25 per part.

C) $6.62 per labor hour.

D) $13.23 per part.

E) None of the other answers is correct.

What is HiTech's pool rate for the material-handling activity?

A) $1.00 per part.

B) $2.25 per part.

C) $6.62 per labor hour.

D) $13.23 per part.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

34

Alamo's customer service department follows up on customer complaints by telephone inquiry. During a recent period, the department initiated 7,000 calls and incurred costs of $203,000. If 2,940 of these calls were for the company's wholesale operation (the remainder were for the retail division), costs allocated to the retail division should amount to:

A) $0.

B) $29.

C) $85,260.

D) $117,740.

E) $203,000.

A) $0.

B) $29.

C) $85,260.

D) $117,740.

E) $203,000.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

35

The division of activities into unit-level, batch-level, product-sustaining level, and facility-level categories is commonly known as a cost:

A) object.

B) application method.

C) hierarchy.

D) estimation method.

E) classification scheme that is useful in traditional, volume-based systems.

A) object.

B) application method.

C) hierarchy.

D) estimation method.

E) classification scheme that is useful in traditional, volume-based systems.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

36

HiTech Products manufactures three types of remote-control devices: Economy, Standard, and Deluxe. The company, which uses activity-based costing, has identified five activities (and related cost drivers). Each activity, its budgeted cost, and related cost driver is identified below. The following information pertains to the three product lines for next year:

What is HiTech's pool rate for the automated machinery activity?

A) $24.00 per machine hour.

B) $24.50 per labor hour.

C) $49.42 per unit.

D) $50.00 per machine hour.

E) None of the other answers is correct.

What is HiTech's pool rate for the automated machinery activity?

A) $24.00 per machine hour.

B) $24.50 per labor hour.

C) $49.42 per unit.

D) $50.00 per machine hour.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

37

Under an activity-based costing system, what is the per-unit overhead cost of Economy?

A) $141.

B) $164.

C) $225.

D) $228.

E) None of the other answers is correct.

A) $141.

B) $164.

C) $225.

D) $228.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

38

Astro's customer service department follows up on customer complaints by telephone inquiry. During a recent period, the department initiated 10,000 calls and incurred costs of $312,000. Of these calls, 3,800 were for the company's wholesale operation; the remainder was for the retail division. Costs allocated to the retail division are:

A) $0.

B) $31,200.

C) $118,560.

D) $193,440.

E) $203,000.

A) $0.

B) $31,200.

C) $118,560.

D) $193,440.

E) $203,000.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

39

St. James, Inc., currently uses traditional costing procedures, applying $800,000 of overhead to products Beta and Zeta on the basis of direct labor hours. The company is considering a shift to activity-based costing and the creation of individual cost pools that will use direct labor hours (DLH), production setups (SU), and number of parts components (PC) as cost drivers. Data on the cost pools and respective driver volumes follow. The overhead cost allocated to Beta by using traditional costing procedures would be:

A) $240,000.

B) $356,000.

C) $444,000.

D) $560,000.

E) None of the other answers is correct.

A) $240,000.

B) $356,000.

C) $444,000.

D) $560,000.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

40

HiTech Products manufactures three types of remote-control devices: Economy, Standard, and Deluxe. The company, which uses activity-based costing, has identified five activities (and related cost drivers). Each activity, its budgeted cost, and related cost driver is identified below. The following information pertains to the three product lines for next year:

What is HiTech's pool rate for the packaging activity?

A) $4.86 per machine hour.

B) $5.00 per labor hour.

C) $10.00 per unit.

D) $100.00 per order shipped.

E) None of the other answers is correct.

What is HiTech's pool rate for the packaging activity?

A) $4.86 per machine hour.

B) $5.00 per labor hour.

C) $10.00 per unit.

D) $100.00 per order shipped.

E) None of the other answers is correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

41

Koski manufactures products J and K, applying overhead on the basis of labor hours. J, a low-volume product, requires a variety of complex manufacturing procedures. K, on the other hand, is both a high-volume product and relatively simplistic in nature. What would an activity-based costing system likely disclose about products J and K as a result of Koski's current accounting procedures?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

42

Vanguilder combines all manufacturing overhead into a single cost pool and allocates this overhead to products by using machine hours. Activity-based costing would likely show that with Vanguard's current procedures that:

A) all of the company's products are undercosted.

B) the company's high-volume products are undercosted.

C) all of the company's products are overcosted.

D) the company's high-volume products are overcosted.

E) the company's low-volume products are overcosted.

A) all of the company's products are undercosted.

B) the company's high-volume products are undercosted.

C) all of the company's products are overcosted.

D) the company's high-volume products are overcosted.

E) the company's low-volume products are overcosted.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

43

During a recent accounting period, Marty's shipping department processed 26 orders. Each order typically takes four hours to complete. However, the average time increased to five hours because of various departmental inefficiencies. If shipping labor is paid $14 per hour, the company's non-value-added cost would be:

A) $0.

B) $56.

C) $364.

D) $1,456.

E) $1,820.

A) $0.

B) $56.

C) $364.

D) $1,456.

E) $1,820.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

44

Kelly and Logan, an accounting firm, provides consulting and tax planning services. For many years, the firm's total administrative cost (currently $250,000) has been allocated to services on the basis of billable hours to clients. A recent analysis found that 65% of the firm's billable hours to clients resulted from tax planning services, while 35% resulted from consulting services.

The firm, contemplating a change to activity-based costing, has identified three components of administrative cost, as follows:

A recent analysis of staff support found a strong correlation between the number of staff personnel and the number of clients served (consulting, 20; tax planning, 60). In contrast, in-house computing and miscellaneous office cost varied directly with the number of computer hours logged and number of client transactions, respectively. Consulting consumed 30% of the firm's computer hours and had 20% of the total client transactions.

Assuming the use of activity-based costing, the proper percentage to use in allocating staff support costs to tax planning services is:

A) 20%.

B) 60%.

C) 65%.

D) 75%.

E) 80%.

The firm, contemplating a change to activity-based costing, has identified three components of administrative cost, as follows:

A recent analysis of staff support found a strong correlation between the number of staff personnel and the number of clients served (consulting, 20; tax planning, 60). In contrast, in-house computing and miscellaneous office cost varied directly with the number of computer hours logged and number of client transactions, respectively. Consulting consumed 30% of the firm's computer hours and had 20% of the total client transactions.

Assuming the use of activity-based costing, the proper percentage to use in allocating staff support costs to tax planning services is:

A) 20%.

B) 60%.

C) 65%.

D) 75%.

E) 80%.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

45

Consider the following factors:

I) The degree of correlation between consumption of an activity and consumption of a particular cost driver.

II) The likelihood that a particular cost driver will induce a desired behavioral effect.

III) The likelihood that a particular cost driver will cause an increase in the cost of measurement.

Which of these factors should be considered in the selection of a cost driver?

A) I only.

B) I and II.

C) I and III.

D) II and III.

E) I, II, and III.

I) The degree of correlation between consumption of an activity and consumption of a particular cost driver.

II) The likelihood that a particular cost driver will induce a desired behavioral effect.

III) The likelihood that a particular cost driver will cause an increase in the cost of measurement.

Which of these factors should be considered in the selection of a cost driver?

A) I only.

B) I and II.

C) I and III.

D) II and III.

E) I, II, and III.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

46

Johnson manufactures products X and Y, applying overhead on the basis of labor hours. X is a high-volume product and relatively simplistic in nature. Y is both a low-volume product and requires a variety of complex manufacturing procedures. What would an activity-based costing system likely disclose about products X and Y as a result of Johnson's current accounting procedures?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following activity cost pools and activity measures likely has the lowest degree of correlation?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

48

Activity-based costing systems:

A) use a single, volume-based cost driver.

B) assign overhead to products based on the products' relative usage of direct labor.

C) often reveal products that were under- or over-costed by traditional costing systems.

D) typically use fewer cost drivers than more traditional costing systems.

E) have a tendency to distort product costs.

A) use a single, volume-based cost driver.

B) assign overhead to products based on the products' relative usage of direct labor.

C) often reveal products that were under- or over-costed by traditional costing systems.

D) typically use fewer cost drivers than more traditional costing systems.

E) have a tendency to distort product costs.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

49

Jackson manufactures products X and Y, applying overhead on the basis of labor hours. X, a low-volume product, requires a variety of complex manufacturing procedures. Y, on the other hand, is both a high-volume product and relatively simplistic in nature. What would an activity-based costing system likely disclose about products X and Y as a result of Jackson's current accounting procedures?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

50

Successful adoptions of activity-based costing typically occur when companies rely heavily on:

A) finance personnel.

B) accounting personnel.

C) manufacturing personnel.

D) office personnel.

E) multidisciplinary project teams.

A) finance personnel.

B) accounting personnel.

C) manufacturing personnel.

D) office personnel.

E) multidisciplinary project teams.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

51

Widely varying consumption ratios:

A) are reflective of product-line diversity.

B) indicate an out-of-control production environment.

C) dictate a need for traditional costing systems.

D) work against the implementation of activity-based costing.

E) create an unsolvable product-costing problem.

A) are reflective of product-line diversity.

B) indicate an out-of-control production environment.

C) dictate a need for traditional costing systems.

D) work against the implementation of activity-based costing.

E) create an unsolvable product-costing problem.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

52

Consider the following statements:

I) Product diversity creates costing problems because diverse products tend to utilize manufacturing activities in different ways.

II) Overhead costs that are not incurred at the unit level create costing problems because such costs do not vary with traditional application bases such as direct labor hours or machine hours.

III) Product diversity typically exists when a single product (e.g., a ballpoint pen) is made in different colors.

Which of the above statements is (are) true?

A) I only.

B) II only.

C) I and II.

D) I and III.

E) II and III.

I) Product diversity creates costing problems because diverse products tend to utilize manufacturing activities in different ways.

II) Overhead costs that are not incurred at the unit level create costing problems because such costs do not vary with traditional application bases such as direct labor hours or machine hours.

III) Product diversity typically exists when a single product (e.g., a ballpoint pen) is made in different colors.

Which of the above statements is (are) true?

A) I only.

B) II only.

C) I and II.

D) I and III.

E) II and III.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

53

Drake Manufacturing sells a number of goods whose selling price is heavily influenced by cost. A recent study of product no. 520 revealed a traditionally-derived total cost of $1,623 and a selling price of $1,850 based on that figure. A newly computed activity-based total cost is $1,215. Which of the following statements is true?

A) All other things being equal, Drake should consider increasing its sales price.

B) Drake should increase the product's selling price to maintain the same markup percentage.

C) Product no. 520 could be labeled as being overcosted by Drake's traditional costing procedures.

D) If product no. 520 is undercosted by traditional accounting procedures, then all of Drake's other products must be undercosted as well.

E) Generally speaking, the activity-based cost figure is "less accurate" than the traditionally-derived cost figure.

A) All other things being equal, Drake should consider increasing its sales price.

B) Drake should increase the product's selling price to maintain the same markup percentage.

C) Product no. 520 could be labeled as being overcosted by Drake's traditional costing procedures.

D) If product no. 520 is undercosted by traditional accounting procedures, then all of Drake's other products must be undercosted as well.

E) Generally speaking, the activity-based cost figure is "less accurate" than the traditionally-derived cost figure.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

54

Dreyson Manufacturing sells a number of goods whose selling price is heavily influenced by cost. A recent study of product no. 519 revealed a traditionally-derived total cost of $1,019, a selling price of $1,850 based on that figure, and a newly computed activity-based total cost of $1,215. Which of the following statements is true?

A) All other things being equal, the company should consider a drop in its sales price.

B) The company may have been extremely competitive in the marketplace from a price perspective.

C) Product no. 519 could be labeled as being overcosted by the firm's traditional costing procedures.

D) If product no. 519 is undercosted by traditional accounting procedures, then all of the company's other products must be undercosted as well.

E) Generally speaking, the activity-based cost figure is "less accurate" than the traditionally-derived cost figure.

A) All other things being equal, the company should consider a drop in its sales price.

B) The company may have been extremely competitive in the marketplace from a price perspective.

C) Product no. 519 could be labeled as being overcosted by the firm's traditional costing procedures.

D) If product no. 519 is undercosted by traditional accounting procedures, then all of the company's other products must be undercosted as well.

E) Generally speaking, the activity-based cost figure is "less accurate" than the traditionally-derived cost figure.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

55

Grist Enterprises is converting to an activity-based costing system It wishes to depict the various activities in its manufacturing process along with the activities' relationships. Which of the following is a tool that the company can use to accomplish this task?

A) Storyboards.

B) Activity relationship charts (ARCs).

C) Decision trees.

D) Simulation games.

E) Process organizers.

A) Storyboards.

B) Activity relationship charts (ARCs).

C) Decision trees.

D) Simulation games.

E) Process organizers.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

56

In comparison with a system that uses a single, volume-based cost driver, an activity-based costing system is preferred when a company has:

A) a large proportion of nonunit-level activities.

B) product-line diversity.

C) minimal product-line diversity and a small proportion of nonunit-level activities.

D) existing variances from budgeted amounts.

E) product-line diversity and a large proportion of nonunit-level activities.

A) a large proportion of nonunit-level activities.

B) product-line diversity.

C) minimal product-line diversity and a small proportion of nonunit-level activities.

D) existing variances from budgeted amounts.

E) product-line diversity and a large proportion of nonunit-level activities.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

57

Consumption ratios are useful in determining:

A) the existence of product-line diversity.

B) overhead that is incurred at the unit level.

C) if overhead-producing activities are being utilized effectively.

D) if overhead costs are being applied to products.

E) if overhead-producing activities are being utilized efficiently.

A) the existence of product-line diversity.

B) overhead that is incurred at the unit level.

C) if overhead-producing activities are being utilized effectively.

D) if overhead costs are being applied to products.

E) if overhead-producing activities are being utilized efficiently.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following statements is (are) true about non-value-added activities?

I) Non-value-added activities are often unnecessary and dispensable.

II) Non-value-added activities may be necessary but are being performed in an inefficient and improvable manner.

III) Non-value-added activities can be eliminated without deterioration of product quality, performance, or perceived value.

A) I only

B) II only

C) III only

D) I and II

E) I, II, and III

I) Non-value-added activities are often unnecessary and dispensable.

II) Non-value-added activities may be necessary but are being performed in an inefficient and improvable manner.

III) Non-value-added activities can be eliminated without deterioration of product quality, performance, or perceived value.

A) I only

B) II only

C) III only

D) I and II

E) I, II, and III

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

59

Martin and Beasley, an accounting firm, provides consulting and tax planning services. For many years, the firm's total administrative cost (currently $270,000) has been allocated to services on this basis of billable hours to clients. A recent analysis found that 55% of the firm's billable hours to clients resulted from tax planning services, while 45% resulted from consulting services.

The firm, contemplating a change to activity-based costing, has identified three components of administrative cost, as follows:

A recent analysis of staff support found a strong correlation with the number of clients served. In contrast, in-house computing and miscellaneous office cost varied directly with the number of computer hours logged and number of client transactions, respectively. Consulting clients served totaled 35% of the total client base, consumed 30% of the firm's computer hours, and accounted for 20% of the total client transactions.

If Martin and Beasley switched from its current accounting method to an activity-based costing system, the amount of administrative cost chargeable to consulting services would:

A) decrease by $32,500.

B) increase by $32,500.

C) decrease by $59,500.

D) change by an amount other than those listed.

E) change, but the amount cannot be determined based on the information presented.

The firm, contemplating a change to activity-based costing, has identified three components of administrative cost, as follows:

A recent analysis of staff support found a strong correlation with the number of clients served. In contrast, in-house computing and miscellaneous office cost varied directly with the number of computer hours logged and number of client transactions, respectively. Consulting clients served totaled 35% of the total client base, consumed 30% of the firm's computer hours, and accounted for 20% of the total client transactions.

If Martin and Beasley switched from its current accounting method to an activity-based costing system, the amount of administrative cost chargeable to consulting services would:

A) decrease by $32,500.

B) increase by $32,500.

C) decrease by $59,500.

D) change by an amount other than those listed.

E) change, but the amount cannot be determined based on the information presented.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

60

Kelly and Logan, an accounting firm, provides consulting and tax planning services. For many years, the firm's total administrative cost (currently $250,000) has been allocated to services on the basis of billable hours to clients. A recent analysis found that 65% of the firm's billable hours to clients resulted from tax planning services, while 35% resulted from consulting services.

The firm, contemplating a change to activity-based costing, has identified three components of administrative cost, as follows:

A recent analysis of staff support found a strong correlation between the number of staff personnel and the number of clients served (consulting, 20; tax planning, 60). In contrast, in-house computing and miscellaneous office cost varied directly with the number of computer hours logged and number of client transactions, respectively. Consulting consumed 30% of the firm's computer hours and had 20% of the total client transactions.

If Kelly and Logan switched from its current accounting method to an activity-based costing system, the amount of administrative cost chargeable to consulting services would:

A) decrease by $23,500.

B) increase by $23,500.

C) decrease by $32,500.

D) change by an amount other than those listed.

E) change, but the amount cannot be determined based on the information presented.

The firm, contemplating a change to activity-based costing, has identified three components of administrative cost, as follows:

A recent analysis of staff support found a strong correlation between the number of staff personnel and the number of clients served (consulting, 20; tax planning, 60). In contrast, in-house computing and miscellaneous office cost varied directly with the number of computer hours logged and number of client transactions, respectively. Consulting consumed 30% of the firm's computer hours and had 20% of the total client transactions.

If Kelly and Logan switched from its current accounting method to an activity-based costing system, the amount of administrative cost chargeable to consulting services would:

A) decrease by $23,500.

B) increase by $23,500.

C) decrease by $32,500.

D) change by an amount other than those listed.

E) change, but the amount cannot be determined based on the information presented.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

61

The adoption of a 24/7 employee hotline for workplace complaints is an example of a:

A) business-value-added activity.

B) customer-value-added activity.

C) nonvalue-added activity.

D) batch-related activity.

E) product-sustaining activity.

A) business-value-added activity.

B) customer-value-added activity.

C) nonvalue-added activity.

D) batch-related activity.

E) product-sustaining activity.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

62

Generally speaking, companies prefer doing business with customers who:

A) order small quantities rather than large quantities.

B) often change their orders.

C) require special packaging or handling.

D) request normal delivery times.

E) need specialized engineering design changes.

A) order small quantities rather than large quantities.

B) often change their orders.

C) require special packaging or handling.

D) request normal delivery times.

E) need specialized engineering design changes.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

63

An example of a customer-value-added activity is:

A) final painting and polishing of the product.

B) installation of a computerized human resource management module.

C) shortening the customers' billing cycle.

D) addition of an employee hotline for workplace complaints.

E) maintenance of an adequate safety stock.

A) final painting and polishing of the product.

B) installation of a computerized human resource management module.

C) shortening the customers' billing cycle.

D) addition of an employee hotline for workplace complaints.

E) maintenance of an adequate safety stock.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

64

Of the following organizations, activity-based costing (ABC) cannot be used by:

A) manufacturers.

B) financial-services firms.

C) book publishers.

D) hotels.

E) None of these are correct, as all these organizations can use ABC.

A) manufacturers.

B) financial-services firms.

C) book publishers.

D) hotels.

E) None of these are correct, as all these organizations can use ABC.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

65

Storch Corporation takes eight hours to complete the setup process for a certain electrical component, with the setup cost averaging $150 per hour. If the company's competitor can accomplish the same process in six hours, Stanley's non-value-added cost would be:

A) $0.

B) $150.

C) $300.

D) $900.

E) $1,200.

A) $0.

B) $150.

C) $300.

D) $900.

E) $1,200.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

66

Factory Oak produces various wooden bookcases, tables, storage units, and chairs. Which of the following would be included in a listing of the company's non-value-added activities?

A) Assembly of tables.

B) Staining of storage units.

C) Transfer of chairs from the assembly line to the staining facility.

D) Storage of completed bookcases in inventory.

E) Transfer of chairs from the assembly line to the staining facility and storage of completed bookcases in inventory.

A) Assembly of tables.

B) Staining of storage units.

C) Transfer of chairs from the assembly line to the staining facility.

D) Storage of completed bookcases in inventory.

E) Transfer of chairs from the assembly line to the staining facility and storage of completed bookcases in inventory.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following is not an example of a business-value-added activity?

A) Adopting bar-code technology in the receiving department.

B) Installation of a computerized human resource management module.

C) Shortening the customers' billing cycle.

D) Addition of an employee hotline for workplace complaints.

E) Final painting and polishing of the product.

A) Adopting bar-code technology in the receiving department.

B) Installation of a computerized human resource management module.

C) Shortening the customers' billing cycle.

D) Addition of an employee hotline for workplace complaints.

E) Final painting and polishing of the product.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

68

Alexander Corporation produces flat-screen computer monitors. Consider the following selected costs that arose during the current year:

1. Direct materials used: $3,640,000

2. Plant rent, utilities, and taxes: $1,229,000

3. New technology design engineering: $2,040,000

4. Materials receiving: $318,000

5. Manufacturing-run/set-up charges: $115,000

6. Equipment depreciation: $92,000

7. General management salaries: $1,564,000

Required:

A. A batch-level activity is performed for each batch of products rather than for each unit. In contrast, a facility-level activity is required for an entire process to occur. Examples of the latter, which support the organization as a whole, include plant maintenance and property taxes.

A. Briefly distinguish between batch-level and facility-level activities.

B. Determine the cost of the firm's unit-level, batch-level, product-sustaining, and facility-level activities.

B. Unit-level: $3,640,000 (1)

Batch-level: $318,000 (4) + $115,000 (5) = $433,000

Product-sustaining: $2,040,000 (3)

Facility-level: $1,229,000 (2) + $92,000 (6) + $1,564,000 (7) = $2,885,000

1. Direct materials used: $3,640,000

2. Plant rent, utilities, and taxes: $1,229,000

3. New technology design engineering: $2,040,000

4. Materials receiving: $318,000

5. Manufacturing-run/set-up charges: $115,000

6. Equipment depreciation: $92,000

7. General management salaries: $1,564,000

Required:

A. A batch-level activity is performed for each batch of products rather than for each unit. In contrast, a facility-level activity is required for an entire process to occur. Examples of the latter, which support the organization as a whole, include plant maintenance and property taxes.

A. Briefly distinguish between batch-level and facility-level activities.

B. Determine the cost of the firm's unit-level, batch-level, product-sustaining, and facility-level activities.

B. Unit-level: $3,640,000 (1)

Batch-level: $318,000 (4) + $115,000 (5) = $433,000

Product-sustaining: $2,040,000 (3)

Facility-level: $1,229,000 (2) + $92,000 (6) + $1,564,000 (7) = $2,885,000

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

69

Consider the following costs that relate to a bank and a manufacturer of software:

Bank

1. Review costs of commercial loan applications

2. Operating costs of human resources department

3. Immediate processing costs of a specific customer's cash deposit

4. Bank membership costs of joining local Chamber of Commerce

Software manufacturer

5. Label and packaging charges from a commercial printer for a new software release

6. Air conditioning/heating costs of the firm's production plant

7. Transport costs of moving the finished products from production run no. 1 to the company's warehouse

8. Design and development costs of new spreadsheet software

Required:

A.

A. Classify the eight costs listed as arising from either a unit-level, batch-level, product-sustaining, or facility-level activity.

B. The number of loan applications would be more appropriate because it has a higher correlation with the amount of review costs incurred. Applications create review costs; customers, on the other hand, may not.

B. Would number of loan applications or number of customers be a more appropriate cost-driver base for #1 above? Briefly explain.

Bank

1. Review costs of commercial loan applications

2. Operating costs of human resources department

3. Immediate processing costs of a specific customer's cash deposit

4. Bank membership costs of joining local Chamber of Commerce

Software manufacturer

5. Label and packaging charges from a commercial printer for a new software release

6. Air conditioning/heating costs of the firm's production plant

7. Transport costs of moving the finished products from production run no. 1 to the company's warehouse

8. Design and development costs of new spreadsheet software

Required:

A.

A. Classify the eight costs listed as arising from either a unit-level, batch-level, product-sustaining, or facility-level activity.

B. The number of loan applications would be more appropriate because it has a higher correlation with the amount of review costs incurred. Applications create review costs; customers, on the other hand, may not.

B. Would number of loan applications or number of customers be a more appropriate cost-driver base for #1 above? Briefly explain.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

70

Consider the nine activities that follow.

1. Microsoft: Developing computer coding for a new spreadsheet package.

2. General Mills: Painting the office of a maintenance supervisor at a plant that produces cereal.

3. Mayo Clinic: Examining a new patient.

4. American Airlines: The 90 minutes that a Boeing 757 sits idle on the ground between flights.

5. Office Depot: Moving cases of paper from one location to another in the same warehouse.

6. Rolex: Attaching a watch band to the watch's face.

7. United States Postal Service: Reprocessing mail that had been sorted incorrectly on a malfunctioning sorting machine.

8. Fidelity Investments: Correcting errors made by company personnel in customer accounts.

9. Marriott: Upgrading the quality of bedding used at hotels in very competitive marketplaces.

Required:

Categorize each of the activities as either value-added or non-value-added for the companies noted.

1. Microsoft: Developing computer coding for a new spreadsheet package.

2. General Mills: Painting the office of a maintenance supervisor at a plant that produces cereal.

3. Mayo Clinic: Examining a new patient.

4. American Airlines: The 90 minutes that a Boeing 757 sits idle on the ground between flights.

5. Office Depot: Moving cases of paper from one location to another in the same warehouse.

6. Rolex: Attaching a watch band to the watch's face.

7. United States Postal Service: Reprocessing mail that had been sorted incorrectly on a malfunctioning sorting machine.

8. Fidelity Investments: Correcting errors made by company personnel in customer accounts.

9. Marriott: Upgrading the quality of bedding used at hotels in very competitive marketplaces.

Required:

Categorize each of the activities as either value-added or non-value-added for the companies noted.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

71

Which of the following can have a negative impact on a particular sale's profitability?

A) Number of required sales contacts (phone calls, visits, etc.).

B) Special shipping instructions.

C) Accounts receivable collection time.

D) Purchase-order changes.

E) All of the answers are correct.

A) Number of required sales contacts (phone calls, visits, etc.).

B) Special shipping instructions.

C) Accounts receivable collection time.

D) Purchase-order changes.

E) All of the answers are correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

72

Hilton Corporation's customers differ greatly with respect to number of required sales contacts (e.g., phone calls and sales visits), account payment patterns, and design/engineering change orders. Which of the following choices likely denotes an ideal customer from Hilton's perspective?

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

A) Choice A

B) Choice B

C) Choice C

D) Choice D

E) Choice E

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

73

The adoption of a 24/7 customer service help line is an example of a:

A) business-value-added activity.

B) customer-value-added activity.

C) nonvalue-added activity.

D) batch-related activity.

E) product-sustaining activity.

A) business-value-added activity.

B) customer-value-added activity.

C) nonvalue-added activity.

D) batch-related activity.

E) product-sustaining activity.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

74

St. Helena Cellars produces wine in northern California. Consider the following selected costs that arose during the current year:

1. Safety costs at winery

2. Truckload shipping costs

3. Building maintenance costs

4. Bottle and cork cost

5. Development cost of new, after-dinner wine

6. Tasting and testing costs

Required:

A. A unit-level activity is performed for each unit of production. In contrast, a product-sustaining activity is needed to support an entire product line. The latter is not necessarily performed each time a new unit or batch of products is manufactured.

A. Briefly distinguish between unit-level and product-sustaining activities.

B. 1. Facility-level

2. Batch-level

3. Facility-level

4. Unit-level

5. Product-sustaining

6. Batch-level

B. Classify the six costs listed as arising from a unit-level, batch-level, product-sustaining, or facility-level activity.

1. Safety costs at winery

2. Truckload shipping costs

3. Building maintenance costs

4. Bottle and cork cost

5. Development cost of new, after-dinner wine

6. Tasting and testing costs

Required:

A. A unit-level activity is performed for each unit of production. In contrast, a product-sustaining activity is needed to support an entire product line. The latter is not necessarily performed each time a new unit or batch of products is manufactured.

A. Briefly distinguish between unit-level and product-sustaining activities.

B. 1. Facility-level

2. Batch-level

3. Facility-level

4. Unit-level

5. Product-sustaining

6. Batch-level

B. Classify the six costs listed as arising from a unit-level, batch-level, product-sustaining, or facility-level activity.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

75

Customer profitability analysis is tied closely to:

A) just-in-time systems.

B) activity-based costing.

C) job costing.

D) process costing.

E) operation costing.

A) just-in-time systems.

B) activity-based costing.

C) job costing.

D) process costing.

E) operation costing.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

76

Bravo Manufacturing is a relatively new customer of Haxton Enterprises. In the short period that the two companies have done business with each other, Haxton has found Bravo to be, in management's words, "an expensive proposition." Numerous sales visits are typically required to "close a deal," with selling prices and discounts offered being among the most attractive in the industry. Complicating matters, Bravo is slow to settle its account, orders in small quantities, and often has numerous specialized shipping and handling needs.

A recent customer profitability analysis has painted a very negative picture of Bravo Manufacturing, and Haxton's managers are questioning whether an on-going relationship with the firm is warranted.

Required:

A. Briefly explain why the customer profitability analysis painted a negative picture of Bravo Manufacturing.

A. Profit is a function of two basic factors-revenues and expenses-and Haxton is being squeezed on both elements. Prices are low, discounts are high, and order sizes are small. Furthermore, the costs of working with Bravo are high, courtesy of numerous sales calls being required to produce a sale, a slow-paying customer, and specialized handling and shipping needs.

B. Haxton should attempt to work with Bravo in a cost-cutting drive, explaining that favorable terms can only be extended for a short period of time. Acceleration of amounts due, increases in order size, and reductions in sales visits and specialized handling and shipping needs are possible topics for discussion/improvement. If Haxton is unsuccessful in its efforts, price hikes and/or elimination of discounts may be in order.

B. What actions are available to Haxton Enterprises to improve Bravo profitability?

A recent customer profitability analysis has painted a very negative picture of Bravo Manufacturing, and Haxton's managers are questioning whether an on-going relationship with the firm is warranted.

Required:

A. Briefly explain why the customer profitability analysis painted a negative picture of Bravo Manufacturing.

A. Profit is a function of two basic factors-revenues and expenses-and Haxton is being squeezed on both elements. Prices are low, discounts are high, and order sizes are small. Furthermore, the costs of working with Bravo are high, courtesy of numerous sales calls being required to produce a sale, a slow-paying customer, and specialized handling and shipping needs.

B. Haxton should attempt to work with Bravo in a cost-cutting drive, explaining that favorable terms can only be extended for a short period of time. Acceleration of amounts due, increases in order size, and reductions in sales visits and specialized handling and shipping needs are possible topics for discussion/improvement. If Haxton is unsuccessful in its efforts, price hikes and/or elimination of discounts may be in order.

B. What actions are available to Haxton Enterprises to improve Bravo profitability?

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

77

Airstream builds recreational motor homes. All of the following activities add value to the finished product except:

A) installation of carpet.

B) assembly of the frame to the chassis.

C) storage of the vehicle in the sales area.

D) addition of exterior lights.

E) final painting and polishing.

A) installation of carpet.

B) assembly of the frame to the chassis.

C) storage of the vehicle in the sales area.

D) addition of exterior lights.

E) final painting and polishing.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

78

When determining customer profitability, activity-based costing can be used to analyze:

A) orders processed.

B) sales visits.

C) special packaging and handling.

D) billing and collections.

E) All of the answers are correct.

A) orders processed.

B) sales visits.

C) special packaging and handling.

D) billing and collections.

E) All of the answers are correct.

Unlock Deck

Unlock for access to all 85 flashcards in this deck.

Unlock Deck

k this deck

79

Homestead Corporation sells a line of power tools to home improvement chains, generating a cost of goods sold equal to 70% of net sales. The selected data that follow relate to the period just ended for the company's three largest customers: Weekend Project, Tool Mart, and Fix-It City.

A. 1. Customer-related costs as a percentage of gross margin:

Weekend Project: $245,100 ÷ [($2,000,000 - $100,000) × 30%] = 43%

Tool Mart: $918,000 ÷ [($4,900,000 - $400,000) × 30%] = 68%

Fix-It City: $457,800 ÷ [($4,600,000 - $240,000) × 30%] = 35%

2. Average order size:

Weekend Project: $2,000,000 ÷ 50 orders = $40,000

Tool Mart: $4,900,000 ÷ 175 orders = $28,000

Fix-It City: $4,600,000 ÷ 125 orders = $36,800

3. Ratio of regular orders to rush orders:

Weekend Project: 40:10 = 4:1

Tool Mart: 135:40 = 3.375:1

Fix-It City: 110:15 = 7.33:1

4. Number of sales returns as a percentage of total orders:

Weekend Project: 3 ÷ 50 = 6%

Tool Mart: 20 ÷ 175 = 11.4%

Fix-It City: 8 ÷ 125 = 6.4%

A. For each of the three chains, compute:

1. Total customer-related costs as a percentage of gross margin.

2. The average order size (ignoring sales returns).

3. The ratio of regular orders to rush orders.

4. The number of sales returns as a percentage of the number of total orders.

B. Customer-related costs are driven by events (and costs) directly traceable to clients. In this case, Tool Mart's costs as a percentage of gross margin are much higher (68%) than those of Weekend Project and Fix-It City. This result is not surprising given that the firm creates a large number of small orders ($28,000 vs. $36,800 and $40,000) for Homestead to process. In addition, relative to the other two firms, Tool Mart depends more heavily on rush orders, which likely creates additional cost. Finally, a number of Tool Mart's orders (11.4%) eventually result in sales returns, again creating additional processing expense for Homestead. In summary, Tool Mart seems to be an outlier in relation to Weekend Project and Fix-It City, and management should approach Tool Mart to see if the company can change its ways of doing business.