Deck 6: Accounting Quality

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

On September 1,2012,Ramos Inc.approved a plan to dispose of a segment of its business.Ramos expected that the sale would occur on March 31,2013,at an estimated gain of $375,500.The segment had actual and estimated operating profits (losses as follows):

Assume a marginal tax rate of 35%

Assume a marginal tax rate of 35%

Required:

A)In its 2012 income statement,what should Ramos report as profit or loss from discontinued operations (net of tax effects)?

B)Calculate the amount of income that should be shown on the 2013 income statement as a result of the operating profit and the gain on disposal (net of tax)

Assume a marginal tax rate of 35%Required:

A)In its 2012 income statement,what should Ramos report as profit or loss from discontinued operations (net of tax effects)?

B)Calculate the amount of income that should be shown on the 2013 income statement as a result of the operating profit and the gain on disposal (net of tax)

Question

Question

Question

Question

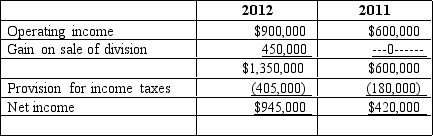

Motor Corporation's income statements for the years ended December 31,2012 and 2011 included the following information before adjustments:

On January 1,2012,Motor Corporation agreed to sell the assets and product line of one of its operating divisions for $1,600,000.The sale was consummated on December 31,2012,and it resulted in a gain on disposition of $450,000.This division's pre-tax net losses were $320,000 in 2012 and $250,000 in 2011.The income tax rate for both years was 30%.

On January 1,2012,Motor Corporation agreed to sell the assets and product line of one of its operating divisions for $1,600,000.The sale was consummated on December 31,2012,and it resulted in a gain on disposition of $450,000.This division's pre-tax net losses were $320,000 in 2012 and $250,000 in 2011.The income tax rate for both years was 30%.

Required:

Starting with operating income (before tax),prepare revised comparative income statements for 2012 and 2011 showing appropriate details for gain (loss)from discontinued operations.

On January 1,2012,Motor Corporation agreed to sell the assets and product line of one of its operating divisions for $1,600,000.The sale was consummated on December 31,2012,and it resulted in a gain on disposition of $450,000.This division's pre-tax net losses were $320,000 in 2012 and $250,000 in 2011.The income tax rate for both years was 30%.Required:

Starting with operating income (before tax),prepare revised comparative income statements for 2012 and 2011 showing appropriate details for gain (loss)from discontinued operations.

Question

Question

Question

Question

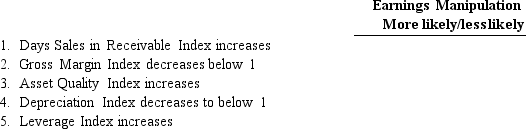

For each of the following factors,determine if the given change or level of that factor would lead an analyst to believe that managers of a firm are more or less likely to engage in earnings manipulation:

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/70

Play

Full screen (f)

Deck 6: Accounting Quality

1

Which of the following items is consistent with earnings being informative about current performance and informing the analyst that level of current earnings are not sustainable?

A) The firm recognizes an unexpected gain

B) The firm recognizes a fair value gain on a financial asset as a result of a favorable move in interest rates.

C) The firm recognizes additional expenses this period due to pre-opening costs associated with new stores.

D) The firm experiences a large jump in sales and earnings as a result of successful research and development of new products.

A) The firm recognizes an unexpected gain

B) The firm recognizes a fair value gain on a financial asset as a result of a favorable move in interest rates.

C) The firm recognizes additional expenses this period due to pre-opening costs associated with new stores.

D) The firm experiences a large jump in sales and earnings as a result of successful research and development of new products.

A

2

On the income statement,income from discontinued operations is shown:

A) as an accounting principle change.

B) without any income tax effect.

C) as a separate section of income from continuing operations.

D) net of taxes after income from continuing operations.

A) as an accounting principle change.

B) without any income tax effect.

C) as a separate section of income from continuing operations.

D) net of taxes after income from continuing operations.

D

3

Which of the following items is consistent with earnings not being informative about current performance but are informative about future earnings?

A) The firm recognizes an unexpected gain

B) The firm recognizes a fair value gain on a financial asset as a result of a favorable move in interest rates.

C) The firm recognizes additional expenses this period due to pre-opening costs associated with new stores.

D) The firm experiences a large jump in sales and earnings as a result of successful research and development of new products.

A) The firm recognizes an unexpected gain

B) The firm recognizes a fair value gain on a financial asset as a result of a favorable move in interest rates.

C) The firm recognizes additional expenses this period due to pre-opening costs associated with new stores.

D) The firm experiences a large jump in sales and earnings as a result of successful research and development of new products.

C

4

The assessment of earnings quality is best accomplished through the use of which one of the following?

A) Balance sheet and cash flow statement.

B) Single-step financial statements.

C) Single-step income statement,balance sheet,and cash flow statement.

D) Multi-step income statement,balance sheet,and cash flow statement.

A) Balance sheet and cash flow statement.

B) Single-step financial statements.

C) Single-step income statement,balance sheet,and cash flow statement.

D) Multi-step income statement,balance sheet,and cash flow statement.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

5

In a restructuring it is possible that managers may use the opportunity to write down assets that do not even relate directly to the restructuring action.Why might a manager decide to write down an asset that is not included in the restructuring action?

A) The manager is practicing conservatism.

B) The write down relieves future periods of depreciation expense,which increases cash flows.

C) Normally the stock market reacts positively to restructuring and the greater the amount the better.

D) The write down relieves future periods of depreciation expense,which increases earnings.

A) The manager is practicing conservatism.

B) The write down relieves future periods of depreciation expense,which increases cash flows.

C) Normally the stock market reacts positively to restructuring and the greater the amount the better.

D) The write down relieves future periods of depreciation expense,which increases earnings.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

6

During July 2012,Ralston Company decides to dispose of one of its subsidiaries,which qualifies for accounting as a discontinued operation.At the July 2012 measurement date,Ralston Company estimates that it will report net losses of $1,500,000 dollars from the measurement date until the disposal date,which is expected to be in April 2013.In addition,Ralston estimates that it will lose $300,000 on the sale of the segment.How much gain or loss on discontinued operations will Ralston report in its 2012 income statement (net of income taxes)?

A) $1,500,000 loss

B) $0

C) $1,800,000 loss

D) $300,000 loss

A) $1,500,000 loss

B) $0

C) $1,800,000 loss

D) $300,000 loss

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

7

Firms' choices and estimates within U.S.GAAP or IFRS should be determined by all of the following except:

A) firms' underlying economic circumstances.

B) conditions in the company's industry.

C) the company's competitive strategy.

D) accelerated management efforts to meet earnings projections.

A) firms' underlying economic circumstances.

B) conditions in the company's industry.

C) the company's competitive strategy.

D) accelerated management efforts to meet earnings projections.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

8

Examples of poor earnings quality that hinder the forecasting of expected future earnings include all of the following except:

A) Earnings dominated by a substantial one-time gain from the sale of real estate tangential to the firm's operations.

B) Reporting a large expense from a warehouse fire that was not covered by insurance.

C) A local government corrects a processing error and a firm receives an unexpected rebate on property taxes previously paid.

D) The company adds equipment that reduces carbon emissions in response to EPA requirements and increases production efficiency.

A) Earnings dominated by a substantial one-time gain from the sale of real estate tangential to the firm's operations.

B) Reporting a large expense from a warehouse fire that was not covered by insurance.

C) A local government corrects a processing error and a firm receives an unexpected rebate on property taxes previously paid.

D) The company adds equipment that reduces carbon emissions in response to EPA requirements and increases production efficiency.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

9

The best measure of a firm's sustainable income is:

A) net income.

B) income from continuing operations.

C) income before extraordinary items.

D) income before extraordinary item and change in accounting principle.

A) net income.

B) income from continuing operations.

C) income before extraordinary items.

D) income before extraordinary item and change in accounting principle.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following items is consistent with earnings being informative about current performance and informing the analyst that level of current earnings is sustainable?

A) The firm recognizes an unexpected gain

B) The firm recognizes a fair value gain on a financial asset as a result of a favorable move in interest rates.

C) The firm recognizes additional expenses this period due to pre-opening costs associated with new stores.

D) The firm experiences a large jump in sales and earnings as a result of successful research and development of new products.

A) The firm recognizes an unexpected gain

B) The firm recognizes a fair value gain on a financial asset as a result of a favorable move in interest rates.

C) The firm recognizes additional expenses this period due to pre-opening costs associated with new stores.

D) The firm experiences a large jump in sales and earnings as a result of successful research and development of new products.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

11

Users of financial statements should consider which of the following when evaluating the quality of accounting information?

A) Economic faithfulness of accounting measurements and classifications.

B) Reliability of the measurements.

C) Reasonableness of the estimates made in applying GAAP or IFRS.

D) All of these should be considered.

A) Economic faithfulness of accounting measurements and classifications.

B) Reliability of the measurements.

C) Reasonableness of the estimates made in applying GAAP or IFRS.

D) All of these should be considered.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

12

All of the following are true regarding a high quality balance sheet except:

A) It should portray the economic resources that can be reasonably expected to generate future economic benefits.

B) It should provide a complete and fair portrayal of all of the firm's obligations at a point in time,including the present value of long-term liabilities for future payments.

C) It should minimize measurement error and bias.

D) It should be optimistic in terms of accounting numbers.

A) It should portray the economic resources that can be reasonably expected to generate future economic benefits.

B) It should provide a complete and fair portrayal of all of the firm's obligations at a point in time,including the present value of long-term liabilities for future payments.

C) It should minimize measurement error and bias.

D) It should be optimistic in terms of accounting numbers.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

13

During July 2013,Ralston Company decides to dispose of one of its subsidiaries,which qualifies for accounting as a discontinued operation.At the July 2013 measurement date,Ralston Company estimates that it will report net income of $300,0000 dollars from the measurement date until the disposal date,which is expected to be in April 2014.In addition,Ralston estimates that it will lose 100,000 on the sale of the segment.How much gain or loss on discontinued operations will Ralston report in its 2012 income statement (net of income taxes)?

A) $200,000 gain

B) $0

C) $100,000 loss

D) $300,000 loss

A) $200,000 gain

B) $0

C) $100,000 loss

D) $300,000 loss

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

14

Which one of the following is an example of sustainable earnings?

A) A gain from corporate restructuring.

B) A loss from debt retirement.

C) A settlement paid by the company for a class action suit.

D) Earnings from repeat customers.

A) A gain from corporate restructuring.

B) A loss from debt retirement.

C) A settlement paid by the company for a class action suit.

D) Earnings from repeat customers.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following items is consistent with earnings being informative about current performance but not informative about future earnings?

A) The firm recognizes an unexpected gain

B) The firm recognizes a fair value gain on a financial asset as a result of a favorable move in interest rates.

C) The firm recognizes additional expenses this period due to pre-opening costs associated with new stores.

D) The firm experiences a large jump in sales and earnings as a result of successful research and development of new products.

A) The firm recognizes an unexpected gain

B) The firm recognizes a fair value gain on a financial asset as a result of a favorable move in interest rates.

C) The firm recognizes additional expenses this period due to pre-opening costs associated with new stores.

D) The firm experiences a large jump in sales and earnings as a result of successful research and development of new products.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

16

Under new accounting standards passed in 2006 firms must report changes in accounting principle in the current and prior years as if the new accounting principle had been applied all along.The rationale for this change was:

A) using the same accounting principle in current and prior periods enhances the information content of reported earnings in forecasting future earnings.

B) conservatism.

C) comparability.

D) materiality.

A) using the same accounting principle in current and prior periods enhances the information content of reported earnings in forecasting future earnings.

B) conservatism.

C) comparability.

D) materiality.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

17

Income or loss from discontinued operations would best be regarded by an analyst as:

A) sustainable earnings.

B) impairments.

C) transitory earnings.

D) permanent earnings.

A) sustainable earnings.

B) impairments.

C) transitory earnings.

D) permanent earnings.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

18

When a company makes a change in an estimate that it has used in its financial statements,it should account for the change by:

A) retroactively restating all prior financial statements

B) treat the change as a cumulative effect change in accounting estimate

C) spread the effect of the change over the current and future periods

D) companies are not allowed to make changes to estimates

A) retroactively restating all prior financial statements

B) treat the change as a cumulative effect change in accounting estimate

C) spread the effect of the change over the current and future periods

D) companies are not allowed to make changes to estimates

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following does not describe an extraordinary gain or loss?

A) infrequent in occurrence

B) peripheral to the company's core business

C) unusual in nature

D) material in amount

A) infrequent in occurrence

B) peripheral to the company's core business

C) unusual in nature

D) material in amount

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

20

As transitory components become a more important part of a firm's reported earnings,the reported earnings:

A) are more quality enhanced.

B) become a more reliable indicator of sustainable cash flows.

C) are a less reliable indicator of sustainable cash flows.

D) are a more reliable indicator of fundamental value.

A) are more quality enhanced.

B) become a more reliable indicator of sustainable cash flows.

C) are a less reliable indicator of sustainable cash flows.

D) are a more reliable indicator of fundamental value.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

21

The Orbus Company has a 30,000 unrealized gain and a 10,000 unrealized loss.Where would Orbus Company report these transactions?

A) Only in non-current assets and liabilities

B) In stockholders' equity

C) Other comprehensive income

D) On the balance sheet as a current asset

A) Only in non-current assets and liabilities

B) In stockholders' equity

C) Other comprehensive income

D) On the balance sheet as a current asset

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

22

Accounting information should be a fair and complete representation of the firm's economic ____________________,____________________,and ____________________.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

23

Accounting information should provide a fair and complete representation about a number of a firm's characteristics.Which of the following is not one of those characteristics?

A) risk

B) position

C) performance

D) conservatism

A) risk

B) position

C) performance

D) conservatism

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

24

One definition of earnings management is that it occurs when managers use:

A) judgment in financial reporting to alter financial reports to mislead stakeholder.

B) an accounting method that is inconsistent with other industry members.

C) more conservative accounting estimates than other companies.

D) pro forma accounting results as opposed to GAAP results.

A) judgment in financial reporting to alter financial reports to mislead stakeholder.

B) an accounting method that is inconsistent with other industry members.

C) more conservative accounting estimates than other companies.

D) pro forma accounting results as opposed to GAAP results.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

25

Firm's choices and estimates within U.S.GAAP should be determined by:

A) how the industry operates.

B) the firm's underlying economic circumstances.

C) SEC interpretations regarding specific choices.

D) the firm's auditor.

A) how the industry operates.

B) the firm's underlying economic circumstances.

C) SEC interpretations regarding specific choices.

D) the firm's auditor.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

26

Many times a financial analyst may decide to make adjustments to the financial statements in order to make the statements more useful.Which of the following would not require an adjustment to the financial statement?

A) A company signs a new contract with a customer.

B) A delivery company incurs a loss from disposition of used delivery trucks.

C) A company changes the useful life of its equipment from 5 years to 8 years.

D) A company incurs a charge related restructuring its operations.

A) A company signs a new contract with a customer.

B) A delivery company incurs a loss from disposition of used delivery trucks.

C) A company changes the useful life of its equipment from 5 years to 8 years.

D) A company incurs a charge related restructuring its operations.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

27

Earnings that are high quality would:

A) be informative about current performance and provide information about the long-run sustainability of profits.

B) be informative about past performance and provide information about the long-run sustainability of profits.

C) be informative about current performance and provide information about the long-run sustainability of assets.

D) be informative about past performance and provide information about the long-run sustainability of assets and liabilities.

A) be informative about current performance and provide information about the long-run sustainability of profits.

B) be informative about past performance and provide information about the long-run sustainability of profits.

C) be informative about current performance and provide information about the long-run sustainability of assets.

D) be informative about past performance and provide information about the long-run sustainability of assets and liabilities.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

28

All of the following are criteria that financial reporting requires before recognizing an obligation as a liability except:

A) The transaction or event that gave rise to the obligation has already occurred.

B) The firm has a present obligation and little or no discretion to avoid the transfer.

C) The firm must know the precise amount of the obligation before recording it.

D) The obligation involves a probable future sacrifice of economic benefits-a future transfer of cash,goods,or services;the forgoing of a future cash receipt;or the transfer of equity shares-at a specified or determinable date.The firm can measure with reasonable precision the cash-equivalent value of the resources needed to satisfy the obligation.

A) The transaction or event that gave rise to the obligation has already occurred.

B) The firm has a present obligation and little or no discretion to avoid the transfer.

C) The firm must know the precise amount of the obligation before recording it.

D) The obligation involves a probable future sacrifice of economic benefits-a future transfer of cash,goods,or services;the forgoing of a future cash receipt;or the transfer of equity shares-at a specified or determinable date.The firm can measure with reasonable precision the cash-equivalent value of the resources needed to satisfy the obligation.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

29

All of the following are typically recognized as accounting liabilities except:

A) Obligations with Fixed Payment Dates and Amounts

B) Obligations under Mutually Unexecuted Contracts

C) Obligations Arising from Advances from Customers on Unexecuted Contracts and Agreements

D) Obligations with Fixed Payment Amounts but Estimated Payment Dates

A) Obligations with Fixed Payment Dates and Amounts

B) Obligations under Mutually Unexecuted Contracts

C) Obligations Arising from Advances from Customers on Unexecuted Contracts and Agreements

D) Obligations with Fixed Payment Amounts but Estimated Payment Dates

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

30

All of the following are the general principles underlying the valuation of liabilities except:

A) Liabilities requiring future cash payments appear at the present value of the required future cash flows discounted at an interest rate that reflects the uncertainty that the firm will be able to make the cash payments.

B) The fair value of a liability cannot differ from the amount appearing on the balance sheet,particularly for long-term debt.

C) Liabilities representing cash advances from customers appear at the amount of the cash advance.

D) Liabilities requiring the future delivery of goods or services appear at the estimated cost of those goods and services.

A) Liabilities requiring future cash payments appear at the present value of the required future cash flows discounted at an interest rate that reflects the uncertainty that the firm will be able to make the cash payments.

B) The fair value of a liability cannot differ from the amount appearing on the balance sheet,particularly for long-term debt.

C) Liabilities representing cash advances from customers appear at the amount of the cash advance.

D) Liabilities requiring the future delivery of goods or services appear at the estimated cost of those goods and services.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

31

Quality accounting information seeks to maximize relevance and economic faithfulness,subject to the constraints of the ____________________ of the measurements.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

32

The _________________________ is the date on which a firm commits itself to a formal plan to dispose of a business segment.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following is not considered a motive to manage earnings?

A) To create optimal manager compensation payments

B) To create optimal job security for senior management

C) To create optimal measures of assets and liabilities for balance sheet purposes

D) To manage reported earnings in order to reduce industry-specific actions

A) To create optimal manager compensation payments

B) To create optimal job security for senior management

C) To create optimal measures of assets and liabilities for balance sheet purposes

D) To manage reported earnings in order to reduce industry-specific actions

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

34

Accounting information should provide relevant information to forecast the firm's expected future earnings and _________________________.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

35

How is a disposal of a segment of the business reported?

A) separately stated item on the income statement

B) balance sheet

C) statement of cash flows

D) statement of retained earnings

A) separately stated item on the income statement

B) balance sheet

C) statement of cash flows

D) statement of retained earnings

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

36

All of the following are typically recognized as accounting liabilities except:

A) Bonds Payable

B) Rental Fees Received in Advance

C) Loan Guarantees

D) Taxes Payable

A) Bonds Payable

B) Rental Fees Received in Advance

C) Loan Guarantees

D) Taxes Payable

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

37

When evaluating the quality of accounting information,an analyst should consider all of the following except:

A) reliability of the measurements made

B) adequacy of disclosures

C) comparability of estimates

D) economic faithfulness of the measurements made

A) reliability of the measurements made

B) adequacy of disclosures

C) comparability of estimates

D) economic faithfulness of the measurements made

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

38

Quality accounting information should be informative as to both the __________________________________________________ of the current period's earnings and the long-run sustainability of profits.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following are characteristics of an extraordinary item?

A) Unusual in nature

B) Infrequent in occurrence

C) Material in amount

D) All of the above

A) Unusual in nature

B) Infrequent in occurrence

C) Material in amount

D) All of the above

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

40

Warranties payable and Notes payable are considered which of the following?

A) Accounting Liabilities

B) Assets

C) Stockholders' Equity

D) Other Financial Assets

A) Accounting Liabilities

B) Assets

C) Stockholders' Equity

D) Other Financial Assets

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

41

U.S.GAAP requires that changes in estimates be accounted for by recognizing the effect ________________________________________ period(s).

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

42

When evaluating the quality of accounting information the user should consider the _____________________________________________ of the measurements made.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

43

Earnings are informative if they signal the portion of current period's due to a new product and the additional earnings in the future as a result of the ____________________ of this new earnings stream.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

44

In bankruptcy prediction analysis,a type ____________________ error is classifying a firm as nonbankrupt when it ultimately goes bankrupt.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

45

When evaluating the quality of accounting information the user should consider the reasonableness of the ____________________ made in applying GAAP.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

46

One of the conditions that must be met to recognize an estimated loss from a contingency is that the amount of loss can be estimated with ________________________________________.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

47

Under current GAAP unrealized gains and losses from four balance sheet items are reported in ___________________________________________________________________________.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

48

An extraordinary gain or loss is unusual in nature,_____________________________________________,and material in amount.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

49

Banks Corp.reported net income of $595,000 in 2012.During 2012 Banks reported a loss of $87,435 from a peripheral activity.The loss was included as part of income from continuing operations.Assuming that the loss is a one-time event and that Banks has an effective tax rate of 35%,calculate Banks' adjusted net income.Show all of your calculations for credit.

In addition,discuss why analysts might make an adjustment of this type.

In addition,discuss why analysts might make an adjustment of this type.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

50

When evaluating the quality of accounting information the user should consider the ____________________ of the firm's disclosures.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

51

A change in the useful life of an asset is treated as a(n)_____________

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

52

Some firms attempt to maximize the amount of restructuring charge in a particular year;analysts refer to this as the _________________________ approach.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

53

On the income statement the disposal of a segment of a business should be shown _________ .

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

54

____________________ represents the concept of being able to compare financial statement data across years for any particular firm.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

55

A(n)____________________ of operations differs from a discontinuation of operations because the firm continues to operate in the business segment.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

56

Creighton Corp. ,a textile manufacturer,reported net income of $258,000 in 2012.During 2012 Creighton reported a gain of $29,800 from the sale of three used delivery trucks.The gain was included as part of income from continuing operations.Assuming that the gain is a one-time event and that Creighton has an effective tax rate of 35% calculate Creighton's adjusted net income.Show all of your calculations for credit.

In addition,discuss why analysts might make an adjustment of this type.

In addition,discuss why analysts might make an adjustment of this type.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

57

When evaluating the quality of accounting information the user should consider the ____________________ of the measurements made.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

58

Many times an analyst will have to make judgments as to whether to include unrealized gains and losses when assessing earnings persistence and predicting future profitability.Discuss the case for and the case against including unrealized gains and losses as part of sustainable earnings when examining earnings persistence and future profitability.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

59

In bankruptcy prediction analysis,a type ____________________ error is classifying a firm as bankrupt and it ultimately survives.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

60

Gains and losses differ from revenues and expenses in that they are produced by ____________________ activities.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

61

A company may try to paint a favorable picture of itself by accelerating the timing of revenues or estimating the collectible amounts too aggressively.In these cases the quality of accounting information declines because it does not represent the company's true economic condition and may not be sustainable.List four conditions which might suggest that a company is recognizing revenues too early?

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

62

On September 1,2012,Ramos Inc.approved a plan to dispose of a segment of its business.Ramos expected that the sale would occur on March 31,2013,at an estimated gain of $375,500.The segment had actual and estimated operating profits (losses as follows):

Assume a marginal tax rate of 35%

Required:

A)In its 2012 income statement,what should Ramos report as profit or loss from discontinued operations (net of tax effects)?

B)Calculate the amount of income that should be shown on the 2013 income statement as a result of the operating profit and the gain on disposal (net of tax)

Assume a marginal tax rate of 35%Required:

A)In its 2012 income statement,what should Ramos report as profit or loss from discontinued operations (net of tax effects)?

B)Calculate the amount of income that should be shown on the 2013 income statement as a result of the operating profit and the gain on disposal (net of tax)

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

63

Healy and Wahlen state that one type of earnings management occurs when managers use judgement in financial reporting to alter financial reports in order to mislead some stakeholder about the economic performance of the company.Earnings management is a consequence of a judgement by management which results in lower economic information content of the financial reports.

Discuss four reasons that discourage managers from practicing earnings management.

Discuss four reasons that discourage managers from practicing earnings management.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

64

Achieving comparability in financial reporting is important to the analysis of multinational firms.However,the data from the reconciliation of foreign firm's financial statement to U.S.GAAP must be carefully interpreted.What types of things complicate the analysis of multinational firms?

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

65

On July 15,2009 Time Services decided to sell its agricultural business and focus on its landscape equipment business.The sale of the agricultural business qualifies for discontinued operations accounting treatment.On November 11,2009 Time Services signs a firm contract to sell the agricultural business to Acme Inc.on March 10,2010.For each of the situations listed discuss how Time Services would report the discontinued operations in its December 31,2009 income statement.(You may disregard tax issues with respect to the sale. )

Situation 1: For the period January 1,2009 to July 15,2009 Time Services reports that the agricultural business lost $3.2M.From July 16,2009 to November 11,2009 Time Services reports that the agricultural business loses an addition $1.4 million dollars.At the end of the 2009 Time estimates that it will lose an additional $800,000 on the sale of the agricultural business when it is finally completed in 2010.

Situation 2: For the period January 1,2009 to July 15,2009 Time Services reports that the agricultural business had a profit of $1.5M.From July 16,2009 to November 11th,2009 Time Services reports that the net income from the agricultural business was $600,000 dollars.At the end of the 2009 Time estimates that the sale of the agricultural business will result in a gain of $1.7 million dollars when it is finally completed in 2010.

Situation 3: For the period January 1,2009 to July 15,2009 Time Services reports that the agricultural business lost $3.2M.From July 16,2009 to November 11th,2009 Time Services reports that the agricultural business loses an addition $1 million dollars.However,at the end of the 2009 Time estimates that the sale of the agricultural business will result in a gain of $1.3 million dollars when it is finally completed in 2010.

Situation 1: For the period January 1,2009 to July 15,2009 Time Services reports that the agricultural business lost $3.2M.From July 16,2009 to November 11,2009 Time Services reports that the agricultural business loses an addition $1.4 million dollars.At the end of the 2009 Time estimates that it will lose an additional $800,000 on the sale of the agricultural business when it is finally completed in 2010.

Situation 2: For the period January 1,2009 to July 15,2009 Time Services reports that the agricultural business had a profit of $1.5M.From July 16,2009 to November 11th,2009 Time Services reports that the net income from the agricultural business was $600,000 dollars.At the end of the 2009 Time estimates that the sale of the agricultural business will result in a gain of $1.7 million dollars when it is finally completed in 2010.

Situation 3: For the period January 1,2009 to July 15,2009 Time Services reports that the agricultural business lost $3.2M.From July 16,2009 to November 11th,2009 Time Services reports that the agricultural business loses an addition $1 million dollars.However,at the end of the 2009 Time estimates that the sale of the agricultural business will result in a gain of $1.3 million dollars when it is finally completed in 2010.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

66

Motor Corporation's income statements for the years ended December 31,2012 and 2011 included the following information before adjustments:

On January 1,2012,Motor Corporation agreed to sell the assets and product line of one of its operating divisions for $1,600,000.The sale was consummated on December 31,2012,and it resulted in a gain on disposition of $450,000.This division's pre-tax net losses were $320,000 in 2012 and $250,000 in 2011.The income tax rate for both years was 30%.

Required:

Starting with operating income (before tax),prepare revised comparative income statements for 2012 and 2011 showing appropriate details for gain (loss)from discontinued operations.

On January 1,2012,Motor Corporation agreed to sell the assets and product line of one of its operating divisions for $1,600,000.The sale was consummated on December 31,2012,and it resulted in a gain on disposition of $450,000.This division's pre-tax net losses were $320,000 in 2012 and $250,000 in 2011.The income tax rate for both years was 30%.Required:

Starting with operating income (before tax),prepare revised comparative income statements for 2012 and 2011 showing appropriate details for gain (loss)from discontinued operations.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

67

Healy and Wahlen state that one type of earnings management occurs when managers use judgement in financial reporting to alter financial reports in order to mislead some stakeholder about the economic performance of the company.Earnings management is a consequence of a judgement by management which results in lower economic information content of the financial reports.

Discuss five motives that encourage managers to practice earnings management.

Discuss five motives that encourage managers to practice earnings management.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

68

On November 15,2012,Jacobs Co.sold a segment of its business for $2,750,000.The net book value of the segment at the time of its disposal was $3,000,000.Jacobs had pretax operating income of $1,750,000 for 2012 which included $380,000 earned by the discontinued segment prior to its disposal.Assume Jacobs' tax rate is 30%.

Required:

Prepare a partial income statement for Jacobs Co.beginning with pretax income from continuing operations.

Required:

Prepare a partial income statement for Jacobs Co.beginning with pretax income from continuing operations.

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

69

Many users of financial statements believe that the quality of accounting information for intangible assets is low because firms seldom report intangible asset resources on the balance sheet.However,from the perspective of accounting quality what are arguments in favor of expensing most intangibles and not recording them on the balance sheet?

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

70

For each of the following factors,determine if the given change or level of that factor would lead an analyst to believe that managers of a firm are more or less likely to engage in earnings manipulation:

Unlock Deck

Unlock for access to all 70 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 70 flashcards in this deck.