Deck 12: Investments

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

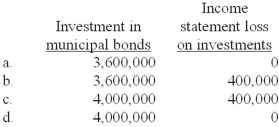

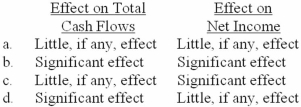

In 2011, Osgood Corporation purchased $4 million in 10-year municipal bonds at face value. On December 31, 2013, the bonds had a market value of $3,600,000 and Osgood reclassified the bonds from held to maturity to trading securities. Osgood's December 31, 2013, balance sheet and the 2013 income statement would show the following:

A)Option a

B)Option b

C)Option c

D)Option d

A)Option a

B)Option b

C)Option c

D)Option d

Question

Question

Question

Question

Question

Question

Question

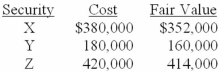

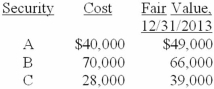

Hobson Company bought the securities listed below during 2012. These securities were classified as trading securities. In its December 31, 2012, income statement Hobson reported a net unrealized loss of $13,000 on these securities. Pertinent data at the end of December 2013 is as follows:  What amount of loss on these securities should Hobson include in its income statement for the year ended December 31, 2013?

What amount of loss on these securities should Hobson include in its income statement for the year ended December 31, 2013?

A)$41,000.

B)$54,000.

C)$13,000.

D)$0.

What amount of loss on these securities should Hobson include in its income statement for the year ended December 31, 2013?A)$41,000.

B)$54,000.

C)$13,000.

D)$0.

Question

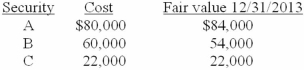

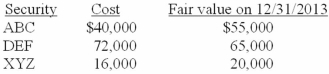

Anthers Inc. bought the following portfolio of trading securities near the end of 2013.  What amount will be reported in the balance sheet for this portfolio at December 31, 2013, and how will it be classified?

What amount will be reported in the balance sheet for this portfolio at December 31, 2013, and how will it be classified?

A)Option a

B)Option b

C)Option c

D)Option d

What amount will be reported in the balance sheet for this portfolio at December 31, 2013, and how will it be classified? A)Option a

B)Option b

C)Option c

D)Option d

Question

Question

Question

Question

What is the effect on a company's cash flows and reported profit from accounting for an investment as a trading security as compared to accounting for it as an available-for-sale security?

A)Option a

B)Option b

C)Option c

D)Option d

A)Option a

B)Option b

C)Option c

D)Option d

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

On January 1, 2013, Everglade Company purchased the following securities and properly accounted for them as securities available for sale:  All declines in value are considered temporary. What amount should the Everglade Company report relative to these securities in its 2013 statement of other comprehensive income?

All declines in value are considered temporary. What amount should the Everglade Company report relative to these securities in its 2013 statement of other comprehensive income?

A)$0.

B)$19,000 unrealized gain.

C)$12,000 net unrealized gain.

D)$7,000 unrealized loss.

All declines in value are considered temporary. What amount should the Everglade Company report relative to these securities in its 2013 statement of other comprehensive income?A)$0.

B)$19,000 unrealized gain.

C)$12,000 net unrealized gain.

D)$7,000 unrealized loss.

Question

Question

Question

Question

Question

Question

Question

Question

Question

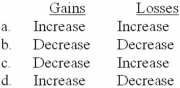

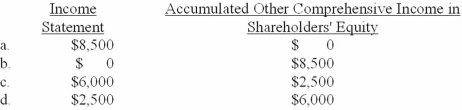

Unrealized holding gains and losses on securities available for sale would have the following effects on accumulated other comprehensive income:

A)Option a

B)Option b

C)Option c

D)Option d

A)Option a

B)Option b

C)Option c

D)Option d

Question

Question

Question

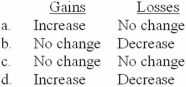

Unrealized holding gains and losses on securities available for sale would have the following effects on retained earnings:

A)Option a

B)Option b

C)Option c

D)Option d

A)Option a

B)Option b

C)Option c

D)Option d

Question

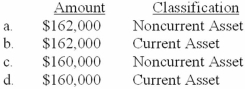

Boulter, Inc. began business on January 1, 2013. At the end of December 2013, Boulter had the following investments in equity securities:  All declines in value are deemed to be temporary in nature. How should the corresponding losses be reflected in the financial statements at December 31, 2013?

All declines in value are deemed to be temporary in nature. How should the corresponding losses be reflected in the financial statements at December 31, 2013?

A)Option a

B)Option b

C)Option c

D)Option d

All declines in value are deemed to be temporary in nature. How should the corresponding losses be reflected in the financial statements at December 31, 2013? A)Option a

B)Option b

C)Option c

D)Option d

Question

Question

Jeremiah Corporation purchased securities during 2013 and classified them as securities available for sale:  All declines are considered to be temporary. How much gain will be reported by Jeremiah Corporation in the December 31, 2013, income statement relative to the portfolio?

All declines are considered to be temporary. How much gain will be reported by Jeremiah Corporation in the December 31, 2013, income statement relative to the portfolio?

A)$0.

B)$16,000.

C)$20,000.

D)None of the above is correct.

All declines are considered to be temporary. How much gain will be reported by Jeremiah Corporation in the December 31, 2013, income statement relative to the portfolio?A)$0.

B)$16,000.

C)$20,000.

D)None of the above is correct.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/186

Play

Full screen (f)

Deck 12: Investments

1

Under IFRS No. 9, investments for which the investor lacks significant influence use basically the same reporting classifications as those used under U.S. GAAP.

False

2

All securities considered available for sale should be reported as current assets in a classified balance sheet.

False

3

Net unrealized holding gains (losses) are reported in the income statement for trading securities.

True

4

When available-for-sale securities are sold, the amount of gain or loss realized from the date of purchase is included in before-tax net income.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

5

If an investment is accounted for under the equity method, the investor reduces investment income and the investment account for amortization of goodwill acquired in the investment.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

6

Selecting the fair value option for an available-for-sale investment is equivalent to reclassifying that investment as a trading security.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

7

Both trading securities and securities available for sale are reported at their fair values.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

8

Both debt and equity securities can be categorized as trading securities.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

9

Companies must always use the equity method when they hold between 25% and 50% of the common stock of an investee.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

10

All investments in debt securities whose fair values are not readily determinable are carried at historical cost.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

11

Routine transfers of debt and equity investments among the trading, available for sale, and held to maturity portfolios need not be disclosed in the financial statements.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

12

Purchases and sales of securities are always reported as investing activities in a statement of cash flows.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

13

Under IAS No. 39, investments for which the investor lacks significant influence use basically the same reporting classifications as those used under U.S. GAAP.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

14

Securities classified as held to maturity could be reported as either current or long-term in a classified balance sheet, depending upon their maturity dates.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

15

The equity method is in many ways a partial consolidation.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

16

Unrealized gains and losses are included in other comprehensive income for securities that are classified as available for sale.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

17

Under the equity method of accounting for a stock investment, cash dividends received are considered a reduction of the investee's net assets.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

18

When an equity method investment is sold, a gain or loss is recognized for the difference between its selling price and its cost.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

19

The fair value option cannot be elected for significant-influence investments because those must be accounted for under the equity method.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

20

Under IFRS No. 9, debt investments are classified as either "available for sale" or "fair value through profit and loss (FVTPL)."

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following investment securities held by Zoogle Inc. may be classified as held-to-maturity securities in its balance sheet?

A)Long-term debenture bonds.

B)Common stock.

C)Callable preferred stock.

D)All of the above are correct.

A)Long-term debenture bonds.

B)Common stock.

C)Callable preferred stock.

D)All of the above are correct.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

22

The income statement reports changes in fair value for which type of securities?

A)Securities reported under the equity method.

B)Trading securities.

C)Held-to-maturity securities.

D)Securities available for sale.

A)Securities reported under the equity method.

B)Trading securities.

C)Held-to-maturity securities.

D)Securities available for sale.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

23

If Ziggy Company concluded that an investment originally classified as held to maturity would now more appropriately be classified as available for sale, Ziggy would:

A)Not reclassify the investment, as original classifications are irrevocable.

B)Reclassify the investment as available for sale and immediately recognize in net income any unrealized gain or loss on the reclassification date.

C)Reclassify the investment as available for sale and immediately recognize in accumulated other comprehensive income any unrealized gain or loss on the reclassification date.

D)Need to restate earnings, as the original classification was in error.

A)Not reclassify the investment, as original classifications are irrevocable.

B)Reclassify the investment as available for sale and immediately recognize in net income any unrealized gain or loss on the reclassification date.

C)Reclassify the investment as available for sale and immediately recognize in accumulated other comprehensive income any unrealized gain or loss on the reclassification date.

D)Need to restate earnings, as the original classification was in error.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

24

If Dinsburry Company concluded that an investment originally classified as a trading security would now more appropriately be classified as held to maturity, Dinsburry would:

A)Not reclassify the investment, as original classifications are irrevocable.

B)Reclassify the investment as held to maturity and immediately recognize in net income all unrealized gains and losses that have not already been recognized as of the reclassification date.

C)Reclassify the investment as held to maturity and treat the fair value as of the date of reclassification as the investment's amortized cost basis for future amortization.

D)Reclassify the investment as held to maturity, but there would be no income effect.

A)Not reclassify the investment, as original classifications are irrevocable.

B)Reclassify the investment as held to maturity and immediately recognize in net income all unrealized gains and losses that have not already been recognized as of the reclassification date.

C)Reclassify the investment as held to maturity and treat the fair value as of the date of reclassification as the investment's amortized cost basis for future amortization.

D)Reclassify the investment as held to maturity, but there would be no income effect.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

25

What would be the balance in Beresford's accumulated other comprehensive income with respect to these investments in its 12/31/2013 balance sheet (ignore taxes)?

A)$55,100.

B)$26,500.

C)$10,400.

D)None of the above is correct.

A)$55,100.

B)$26,500.

C)$10,400.

D)None of the above is correct.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

26

Under IFRS No. 9, equity investments are classified as either "fair value through other comprehensive income (FVTOCI)" or "fair value through profit and loss (FVTPL)."

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

27

If Dizbert Company concluded that an investment originally classified as available for sale would now more appropriately be classified as held to maturity, Dizbert would:

A)Not reclassify the investment, as original classifications are irrevocable.

B)Reclassify the investment as held to maturity and immediately recognize in net income any unrealized gain or loss on the reclassification date.

C)Reclassify the investment as held to maturity and treat the fair value as of the date of reclassification as the investment's amortized cost basis for future amortization.

D)Need to restate earnings, as the original classification was in error.

A)Not reclassify the investment, as original classifications are irrevocable.

B)Reclassify the investment as held to maturity and immediately recognize in net income any unrealized gain or loss on the reclassification date.

C)Reclassify the investment as held to maturity and treat the fair value as of the date of reclassification as the investment's amortized cost basis for future amortization.

D)Need to restate earnings, as the original classification was in error.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

28

Both fair values and subsequent growth of the investee are not as relevant for investments in which of the following categories?

A)Securities reported under the equity method.

B)Trading securities.

C)Held-to-maturity securities.

D)Securities available for sale.

A)Securities reported under the equity method.

B)Trading securities.

C)Held-to-maturity securities.

D)Securities available for sale.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

29

Securities that are purchased with the intent of selling them in the near future to take advantage of short-term price changes are classified as:

A)Securities available for sale.

B)Consolidating securities.

C)Held-to-maturity securities.

D)Trading securities.

A)Securities available for sale.

B)Consolidating securities.

C)Held-to-maturity securities.

D)Trading securities.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

30

What total unrealized holding gain would Beresford report in its 2013 income statement relative to its investment securities?

A)$55,900.

B)$36,000.

C)$80,900.

D)$48,200.

A)$55,900.

B)$36,000.

C)$80,900.

D)$48,200.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

31

Trading securities are most commonly found on the books of:

A)Oil companies.

B)Manufacturing companies.

C)Banks.

D)Foreign subsidiaries.

A)Oil companies.

B)Manufacturing companies.

C)Banks.

D)Foreign subsidiaries.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

32

Under IFRS No. 9, cost can be used as an estimate of fair value in some circumstances.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

33

On January 1, 2013, Rupar Retailers purchased $100,000 of Anand Company bonds at a discount of $5,000. The Anand bonds pay 6% interest but were purchased when the market interest rate was 7% for bonds of similar risk and maturity. The bonds pay interest semiannually on January 1 and July 1 of each year. Rupar accounts for the bonds as a held-to-maturity investment, and uses the effective interest method. In Rupar's December 31, 2013, journal entry to record the second period of interest, Rupar would record a credit to interest revenue of:

A)$3,336.

B)$3,325.

C)$3,000.

D)$3,500.

A)$3,336.

B)$3,325.

C)$3,000.

D)$3,500.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

34

What balance sheet amount would Beresford report for its total investment securities at 12/31/2012?

A)$637,000.

B)$644,500.

C)$645,400.

D)None of the above is correct.

A)$637,000.

B)$644,500.

C)$645,400.

D)None of the above is correct.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

35

The investment category for which the investor's "positive intent and ability to hold" is important is:

A)Securities reported under the equity method.

B)Trading securities.

C)Securities classified as held to maturity.

D)Securities available for sale.

A)Securities reported under the equity method.

B)Trading securities.

C)Securities classified as held to maturity.

D)Securities available for sale.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

36

In 2011, Osgood Corporation purchased $4 million in 10-year municipal bonds at face value. On December 31, 2013, the bonds had a market value of $3,600,000 and Osgood reclassified the bonds from held to maturity to trading securities. Osgood's December 31, 2013, balance sheet and the 2013 income statement would show the following:

A)Option a

B)Option b

C)Option c

D)Option d

A)Option a

B)Option b

C)Option c

D)Option d

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

37

Under IFRS No. 9, debt investments are classified as either "amortized cost" or "fair value through profit and loss (FVTPL)."

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

38

Which category completely excludes equity securities?

A)Securities available for sale.

B)Consolidating securities.

C)Held-to-maturity securities.

D)Trading securities.

A)Securities available for sale.

B)Consolidating securities.

C)Held-to-maturity securities.

D)Trading securities.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following investment securities held by Zoogle Inc. are not reported at fair value in its balance sheet?

A)Common stock held as available for sale securities.

B)Debt securities held to maturity.

C)Preferred stock held as trading securities.

D)All of the above are reported at fair value.

A)Common stock held as available for sale securities.

B)Debt securities held to maturity.

C)Preferred stock held as trading securities.

D)All of the above are reported at fair value.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

40

Under IAS No. 39, transfers of debt investments out of the FVTPL category into AFS or HTM are permitted under "rare circumstances."

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

41

Investments in securities to be held for an unspecified period of time are reported at:

A)Historical cost.

B)Present value.

C)Lower of cost or market.

D)Fair value.

A)Historical cost.

B)Present value.

C)Lower of cost or market.

D)Fair value.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

42

Holding gains and losses on trading securities are included in earnings because:

A)They measure the success or failure of taking advantage of short-term price changes.

B)The IRS mandates the inclusion.

C)The SEC mandates the inclusion.

D)They measure the book value of the securities in the balance sheet date.

A)They measure the success or failure of taking advantage of short-term price changes.

B)The IRS mandates the inclusion.

C)The SEC mandates the inclusion.

D)They measure the book value of the securities in the balance sheet date.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

43

Hobson Company bought the securities listed below during 2012. These securities were classified as trading securities. In its December 31, 2012, income statement Hobson reported a net unrealized loss of $13,000 on these securities. Pertinent data at the end of December 2013 is as follows: What amount of loss on these securities should Hobson include in its income statement for the year ended December 31, 2013?

A)$41,000.

B)$54,000.

C)$13,000.

D)$0.

What amount of loss on these securities should Hobson include in its income statement for the year ended December 31, 2013?A)$41,000.

B)$54,000.

C)$13,000.

D)$0.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

44

Anthers Inc. bought the following portfolio of trading securities near the end of 2013. What amount will be reported in the balance sheet for this portfolio at December 31, 2013, and how will it be classified?

A)Option a

B)Option b

C)Option c

D)Option d

What amount will be reported in the balance sheet for this portfolio at December 31, 2013, and how will it be classified? A)Option a

B)Option b

C)Option c

D)Option d

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

45

All investment securities are initially recorded at:

A)Cost.

B)Present value.

C)Equity value.

D)None of the above is correct.

A)Cost.

B)Present value.

C)Equity value.

D)None of the above is correct.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

46

When an equity security is appropriately carried and reported as securities available for sale, a gain should be reported in the income statement:

A)When the fair value of the security increases.

B)When the present value of the security increases.

C)Only when the Dow Jones Industrial Average increases at least 100 points.

D)Only when the security is sold.

A)When the fair value of the security increases.

B)When the present value of the security increases.

C)Only when the Dow Jones Industrial Average increases at least 100 points.

D)Only when the security is sold.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

47

Nichols Enterprises has an investment in 25,000 shares of Elliott Electronics that Nichols accounts for as a security available for sale. Elliott shares are publicly traded on the New York Stock Exchange, and The Wall Street Journal quotes a price for those shares of $10 a share, but Nichols believes the market has not appreciated the full value of the Elliott shares and that a more accurate price is $12 a share. Nichols should carry the Elliott investment on its balance sheet at:

A)$300,000.

B)$250,000.

C)Either $250,000 or $300,000, as either are defensible valuations.

D)$275,000, the midpoint of Nichols' range of reasonably likely valuations of Elliott.

A)$300,000.

B)$250,000.

C)Either $250,000 or $300,000, as either are defensible valuations.

D)$275,000, the midpoint of Nichols' range of reasonably likely valuations of Elliott.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

48

What is the effect on a company's cash flows and reported profit from accounting for an investment as a trading security as compared to accounting for it as an available-for-sale security?

A)Option a

B)Option b

C)Option c

D)Option d

A)Option a

B)Option b

C)Option c

D)Option d

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

49

On January 1, 2013, Nana Company paid $100,000 for 8,000 shares of Papa Company common stock. These securities were classified as trading securities. The ownership in Papa Company is 10%. Papa reported net income of $52,000 for the year ended December 31, 2013. The fair value of the Papa stock on that date was $45 per share. What amount will be reported in the balance sheet of Nana Company for the investment in Papa at December 31, 2013?

A)$284,400.

B)$300,000.

C)$315,600.

D)$360,000.

A)$284,400.

B)$300,000.

C)$315,600.

D)$360,000.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

50

All investments in debt and equity securities that don't fit the definitions of the other reporting categories are classified as:

A)Trading securities.

B)Securities available for sale.

C)Held-to-maturity securities.

D)Consolidated securities.

A)Trading securities.

B)Securities available for sale.

C)Held-to-maturity securities.

D)Consolidated securities.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

51

When an investor classifies an investment in common stock as securities available for sale, cash dividends are classified by the investor as:

A)A return of capital.

B)A loss.

C)A deduction from the investment account.

D)Dividend income.

A)A return of capital.

B)A loss.

C)A deduction from the investment account.

D)Dividend income.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

52

Trading securities, by definition, are properly classified in the balance sheet as:

A)Shareholders' equity.

B)Intangibles.

C)Current assets.

D)Other assets.

A)Shareholders' equity.

B)Intangibles.

C)Current assets.

D)Other assets.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

53

In the statement of cash flows, inflows and outflows of cash from buying and selling trading securities typically are considered:

A)Investing activities.

B)Operating activities.

C)Financing activities.

D)Noncash financing activities.

A)Investing activities.

B)Operating activities.

C)Financing activities.

D)Noncash financing activities.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

54

For trading securities, unrealized holding gains and losses are included in earnings:

A)Only at the end of the fiscal year.

B)On each reporting date.

C)Only when they exceed 10% of the underlying investment.

D)Based on a vote of the board of directors.

A)Only at the end of the fiscal year.

B)On each reporting date.

C)Only when they exceed 10% of the underlying investment.

D)Based on a vote of the board of directors.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

55

Dyckman Dealers has an investment in Thomas Corporation that Dyckman accounts for as a trading security. Thomas Corporation shares are publicly traded on the New York Stock Exchange, and the prevailing price on that exchange indicates that Dyckman's investment is worth $20,000. However, Dyckman management believes that the stock market is generally overvalued, and their analysis of the Thomas investment suggests to them that it is worth $18,000. Dyckman should carry the Thomas investment on its balance sheet at:

A)$20,000.

B)$18,000.

C)Either $18,000 or $20,000, as either are defensible valuations.

D)$19,000, the midpoint of Dyckman's range of reasonably likely valuations of Thomas.

A)$20,000.

B)$18,000.

C)Either $18,000 or $20,000, as either are defensible valuations.

D)$19,000, the midpoint of Dyckman's range of reasonably likely valuations of Thomas.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

56

The fair value of debt securities not regularly traded can be most reasonably approximated by:

A)Calculating the discounted present value of the principal and interest payments.

B)Determining the value using similar securities in the NASDAQ market.

C)Using the relative fair value method.

D)Calling a licensed and registered stockbroker.

A)Calculating the discounted present value of the principal and interest payments.

B)Determining the value using similar securities in the NASDAQ market.

C)Using the relative fair value method.

D)Calling a licensed and registered stockbroker.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

57

Goofy Inc. bought 15,000 shares of Crazy Co.'s stock for $150,000 on May 5, 2012, and classified the stock as available for sale. The market value of the stock declined to $118,000 by December 31, 2012. Goofy reclassified this investment as trading securities in December of 2013 when the market value had risen to $125,000. What effect on 2013 income should be reported by Goofy for the Crazy Co. shares?

A)$0.

B)$25,000 net loss.

C)$7,000 net gain.

D)$32,000 net loss.

A)$0.

B)$25,000 net loss.

C)$7,000 net gain.

D)$32,000 net loss.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

58

GAAP regarding accounting for unrealized gains and losses on investments in equity securities will apply to an investment when the percentage of ownership of another company is:

A)Less than 20%.

B)20% to 50%.

C)Over 50%.

D)Exactly 100%.

A)Less than 20%.

B)20% to 50%.

C)Over 50%.

D)Exactly 100%.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

59

Investments in securities available for sale are reported at:

A)Discounted present value.

B)Lower of cost or market.

C)Historical cost.

D)Fair value on the reporting date.

A)Discounted present value.

B)Lower of cost or market.

C)Historical cost.

D)Fair value on the reporting date.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

60

Accumulated Other Comprehensive Income in the shareholders' equity section of the balance sheet reflects changes in the fair value of securities for which type of securities?

A)Securities available for sale.

B)Trading securities.

C)Consolidated securities.

D)Held-to-maturity securities.

A)Securities available for sale.

B)Trading securities.

C)Consolidated securities.

D)Held-to-maturity securities.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

61

Dim Corporation purchased 1,000 shares of Witt Corporation stock in 2010 for $800 per share and classified the investment as securities available for sale. Witt's market value was $400 per share on December 31, 2011, and $300 on December 31, 2012. During 2013, Dim sold all of its Witt stock at $350 per share. In its 2013 income statement, Dim would report:

A)A realized gain of $50,000.

B)A recognition of unrealized losses of $400,000.

C)A loss on the sale of investments of $450,000.

D)A trading gain of $50,000 and an unrealized loss of $500,000.

A)A realized gain of $50,000.

B)A recognition of unrealized losses of $400,000.

C)A loss on the sale of investments of $450,000.

D)A trading gain of $50,000 and an unrealized loss of $500,000.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

62

A weakness of __________ is that firms can increase or decrease net income by choosing to sell particular investments with net unrealized gains or unrealized losses.

A)the available-for-sale approach

B)the trading-securities approach

C)both the available-for-sale and trading-securities approaches

D)neither the available-for-sale and trading-securities approaches

A)the available-for-sale approach

B)the trading-securities approach

C)both the available-for-sale and trading-securities approaches

D)neither the available-for-sale and trading-securities approaches

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

63

On January 1, 2013, Everglade Company purchased the following securities and properly accounted for them as securities available for sale: All declines in value are considered temporary. What amount should the Everglade Company report relative to these securities in its 2013 statement of other comprehensive income?

A)$0.

B)$19,000 unrealized gain.

C)$12,000 net unrealized gain.

D)$7,000 unrealized loss.

All declines in value are considered temporary. What amount should the Everglade Company report relative to these securities in its 2013 statement of other comprehensive income?A)$0.

B)$19,000 unrealized gain.

C)$12,000 net unrealized gain.

D)$7,000 unrealized loss.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

64

Zwick Company bought 28,000 shares of the voting common stock of Handy Corporation in January 2013. In December, Hart announced $200,000 net income for 2013 and declared and paid a cash dividend of $2 per share on the 200,000 shares of outstanding common stock. Zwick Company's dividend revenue from Handy Corporation in December 2013 would be:

A)$0.

B)$28,000.

C)$56,000.

D)None of the above is correct.

A)$0.

B)$28,000.

C)$56,000.

D)None of the above is correct.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

65

Seybert Systems accounts for its investment in Wang Engineering as available for sale. Seybert's balance in accumulated other comprehensive income with respect to the Wang investment is a credit balance of $20,000, and Seybert reports the investment at $100,000 on its balance sheet. Seybert purchased the Wang investment for (ignore taxes):

A)$100,000.

B)$120,000.

C)$80,000.

D)Cannot be determined from this information.

A)$100,000.

B)$120,000.

C)$80,000.

D)Cannot be determined from this information.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

66

In the statement of cash flows, inflows and outflows of cash from buying and selling available for sale securities are considered:

A)Operating activities.

B)Financing activities.

C)Investing activities.

D)Noncash financing activities.

A)Operating activities.

B)Financing activities.

C)Investing activities.

D)Noncash financing activities.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

67

If an available-for-sale investment is sold for which there are unrealized gains in accumulated other comprehensive income (AOCI), a reclassification adjustment affects other comprehensive income (OCI) in the period of sale by:

A)Reducing OCI for the amount of unrealized gains in AOCI.

B)Increasing OCI for the amount of unrealized gains in AOCI.

C)No effect on OCI, as OCI only includes the effects of unrealized gains and losses.

D)No effect on OCI, as the realized gain is included in AOCI.

A)Reducing OCI for the amount of unrealized gains in AOCI.

B)Increasing OCI for the amount of unrealized gains in AOCI.

C)No effect on OCI, as OCI only includes the effects of unrealized gains and losses.

D)No effect on OCI, as the realized gain is included in AOCI.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

68

If an available-for-sale investment is sold for which there are unrealized losses in accumulated other comprehensive income (AOCI), the total effect on total comprehensive income is:

A)An increase.

B)A decrease.

C)No effect.

D)Cannot be determined given this information.

A)An increase.

B)A decrease.

C)No effect.

D)Cannot be determined given this information.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

69

The equity method of accounting for investments in voting common stock is appropriate when:

A)The investor can significantly influence the investee.

B)The investor has voting control over the investee.

C)The investor intends to hold the common stock indefinitely.

D)The investor is assured of a continued supply of a valuable raw material.

A)The investor can significantly influence the investee.

B)The investor has voting control over the investee.

C)The investor intends to hold the common stock indefinitely.

D)The investor is assured of a continued supply of a valuable raw material.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

70

Sloan Company has owned an investment during 2013 that has increased in fair value. After all closing entries for 2013 are completed, the effect of the increase in fair value on total shareholders' equity would be:

A)Higher under the available-for-sale approach than under the trading-securities approach.

B)Lower under the available-for-sale approach than under the trading-securities approach.

C)The same amount under the available-for-sale and trading-securities approaches.

D)Not possible to identify whether the available-for-sale or trading-securities approaches yield higher shareholders' equity given this information.

A)Higher under the available-for-sale approach than under the trading-securities approach.

B)Lower under the available-for-sale approach than under the trading-securities approach.

C)The same amount under the available-for-sale and trading-securities approaches.

D)Not possible to identify whether the available-for-sale or trading-securities approaches yield higher shareholders' equity given this information.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

71

When investments are treated as available-for-sale, other comprehensive income (OCI) also includes the tax effects associated with unrealized holding gains and losses. As a result:

A)Accumulated other comprehensive income would be increased by the tax benefits typically associated with unrealized holding gains.

B)Other comprehensive income typically would be reduced by the tax expense associated with unrealized holding gains.

C)Accumulated other comprehensive income would not be affected by taxes.

D)None of the above is correct.

A)Accumulated other comprehensive income would be increased by the tax benefits typically associated with unrealized holding gains.

B)Other comprehensive income typically would be reduced by the tax expense associated with unrealized holding gains.

C)Accumulated other comprehensive income would not be affected by taxes.

D)None of the above is correct.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

72

Unrealized holding gains and losses on securities available for sale would have the following effects on accumulated other comprehensive income:

A)Option a

B)Option b

C)Option c

D)Option d

A)Option a

B)Option b

C)Option c

D)Option d

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

73

On January 2, 2012, Howdy Doody Corporation purchased 12% of Ranger Corporation's common stock for $50,000 and classified the investment as available for sale. Ranger's net income for the years ended December 31, 2012 and 2013, were $10,000 and $50,000, respectively. During 2013, Ranger declared and paid a dividend of $60,000. There were no dividends in 2012. On December 31, 2012, the fair value of the Ranger stock owned by Howdy Doody had increased to $70,000. How much should Howdy Doody show in the 2013 income statement as income from this investment?

A)$26,000.

B)$7,200.

C)$20,000.

D)$27,200.

A)$26,000.

B)$7,200.

C)$20,000.

D)$27,200.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

74

If Pop Company owns 15% of the common stock of Son Company, then Pop Company typically:

A)Would record 15% of the net income of Son Company as investment income each year.

B)Would record dividends received from Son Company as investment revenue.

C)Would increase its investment account by 15% of Son Company income each year.

D)All of the above are correct.

A)Would record 15% of the net income of Son Company as investment income each year.

B)Would record dividends received from Son Company as investment revenue.

C)Would increase its investment account by 15% of Son Company income each year.

D)All of the above are correct.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

75

Unrealized holding gains and losses on securities available for sale would have the following effects on retained earnings:

A)Option a

B)Option b

C)Option c

D)Option d

A)Option a

B)Option b

C)Option c

D)Option d

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

76

Boulter, Inc. began business on January 1, 2013. At the end of December 2013, Boulter had the following investments in equity securities: All declines in value are deemed to be temporary in nature. How should the corresponding losses be reflected in the financial statements at December 31, 2013?

A)Option a

B)Option b

C)Option c

D)Option d

All declines in value are deemed to be temporary in nature. How should the corresponding losses be reflected in the financial statements at December 31, 2013? A)Option a

B)Option b

C)Option c

D)Option d

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

77

The Guitar World (TGW) holds an investment that increased in fair value over 2013, and accounts for that investment as available for sale. When considering taxes, TGW would:

A)Recognize tax expense on the income statement, and probably increase taxes payable.

B)Recognize tax expense on the income statement, and probably increase its deferred tax liability.

C)Reduce accumulated other comprehensive income (AOCI) for tax expense, and probably increase taxes payable.

D)Reduce accumulated other comprehensive income (AOCI) for tax expense, and probably increase its deferred tax liability.

A)Recognize tax expense on the income statement, and probably increase taxes payable.

B)Recognize tax expense on the income statement, and probably increase its deferred tax liability.

C)Reduce accumulated other comprehensive income (AOCI) for tax expense, and probably increase taxes payable.

D)Reduce accumulated other comprehensive income (AOCI) for tax expense, and probably increase its deferred tax liability.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

78

Jeremiah Corporation purchased securities during 2013 and classified them as securities available for sale: All declines are considered to be temporary. How much gain will be reported by Jeremiah Corporation in the December 31, 2013, income statement relative to the portfolio?

A)$0.

B)$16,000.

C)$20,000.

D)None of the above is correct.

All declines are considered to be temporary. How much gain will be reported by Jeremiah Corporation in the December 31, 2013, income statement relative to the portfolio?A)$0.

B)$16,000.

C)$20,000.

D)None of the above is correct.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

79

Consolidated financial statements are prepared when one company has:

A)Accounted for the investment using the equity method.

B)Accounted for the investment as securities available for sale.

C)Control over another company.

D)None of the above is correct.

A)Accounted for the investment using the equity method.

B)Accounted for the investment as securities available for sale.

C)Control over another company.

D)None of the above is correct.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

80

Hawk Corporation purchased 10,000 shares of Diamond Corporation stock in 2010 for $50 per share and classified the investment as securities available for sale. Diamond's market value was $60 per share on December 31, 2011, and $65 on December 31, 2012. During 2013, Hawk sold all of its Diamond stock at $70 per share. In its 2013 income statement, Hawk would report:

A)A gain of $50,000.

B)A gain of $150,000.

C)A gain of $200,000

D)A gain of $300,000.

A)A gain of $50,000.

B)A gain of $150,000.

C)A gain of $200,000

D)A gain of $300,000.

Unlock Deck

Unlock for access to all 186 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 186 flashcards in this deck.