Deck 17: Other Public Accounting Services and Reportsreviews and Compilations

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

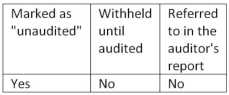

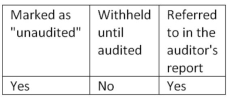

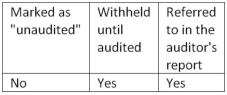

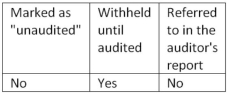

When unaudited financial statements are presented in comparative form with audited financial statements, such statements should be ________.

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/51

Play

Full screen (f)

Deck 17: Other Public Accounting Services and Reportsreviews and Compilations

1

Substantive and compliance testing are applicable to ________.

A) audits only

B) reviews and audits

C) compilations and audits

D) reviews and compilations

A) audits only

B) reviews and audits

C) compilations and audits

D) reviews and compilations

A

2

With a compilation service, the procedures performed by a professional accountant can be described as ________.

A) extensive

B) few, if any

C) comparable to a review service

D) comparable to an audit

A) extensive

B) few, if any

C) comparable to a review service

D) comparable to an audit

B

3

Ordinarily, which of the following procedures should be applied when an independent accountant conducts a review of interim financial information of a publicly held company?

A) Verify changes in key account balances.

B) Read the minutes of the board of directors' meetings.

C) Inspect the open purchase order file.

D) Perform cutoff tests for cash receipts and disbursements.

A) Verify changes in key account balances.

B) Read the minutes of the board of directors' meetings.

C) Inspect the open purchase order file.

D) Perform cutoff tests for cash receipts and disbursements.

B

4

Which of the following procedures should an accountant perform during an engagement to review the financial statements of a private company?

A) Communicate internal control system weaknesses that were discovered during the assessment of control risk.

B) Obtain a letter of representation signed by top-level management.

C) Send bank confirmations to the company's financial institutions.

D) Examine cash disbursements in the subsequent period for evidence of unrecorded liabilities.

A) Communicate internal control system weaknesses that were discovered during the assessment of control risk.

B) Obtain a letter of representation signed by top-level management.

C) Send bank confirmations to the company's financial institutions.

D) Examine cash disbursements in the subsequent period for evidence of unrecorded liabilities.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

5

Reviews of interim financial information consist primarily of ________.

A) substantive procedures

B) recalculation

C) external confirmations

D) enquiry and analytical procedures

A) substantive procedures

B) recalculation

C) external confirmations

D) enquiry and analytical procedures

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

6

The review of interim financial information should ideally take place ________.

A) at or near year-end

B) just after the cutoff date

C) at or near the date of the interim information

D) six months into the fiscal year

A) at or near year-end

B) just after the cutoff date

C) at or near the date of the interim information

D) six months into the fiscal year

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

7

With compilation engagements, the minimum standard is that financial statements ________.

A) not be false or misleading

B) be accurate

C) be fairly presented

D) be prepared in accordance with GAAP

A) not be false or misleading

B) be accurate

C) be fairly presented

D) be prepared in accordance with GAAP

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following procedures would not be performed in a review of the financial statements of a private company?

A) Enquire about the accounting system and bookkeeping procedures.

B) Perform analytical procedures to identify relationships and individual items that appear to be unusual.

C) Obtain a lawyer's letter about claims and possible claims.

D) Study the financial statements for indications that they conform to generally accepted accounting principles.

A) Enquire about the accounting system and bookkeeping procedures.

B) Perform analytical procedures to identify relationships and individual items that appear to be unusual.

C) Obtain a lawyer's letter about claims and possible claims.

D) Study the financial statements for indications that they conform to generally accepted accounting principles.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

9

The primary purpose for the development of standards by the Criteria of Control Committee was to ________.

A) provide guidance for companies developing best practice control systems

B) provide a basis similar to GAAP for reporting on controls

C) provide detailed tests of controls for audits of financial statements

D) provide clarity on who is responsible for controls

A) provide guidance for companies developing best practice control systems

B) provide a basis similar to GAAP for reporting on controls

C) provide detailed tests of controls for audits of financial statements

D) provide clarity on who is responsible for controls

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

10

XYZ Ltd. has prepared financial statements that are not in accordance with GAAP. The review report should ________.

A) ensure that the nature of the departure is described in the notes

B) contain a reservation describing the nature of the departure from GAAP

C) be a standard review report, since a review is not an audit

D) indicate the dollar effect of restatement for each account affected

A) ensure that the nature of the departure is described in the notes

B) contain a reservation describing the nature of the departure from GAAP

C) be a standard review report, since a review is not an audit

D) indicate the dollar effect of restatement for each account affected

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

11

The level of assurance provided by a review engagement can best be described as ________.

A) comparable to that of an audit

B) moderate

C) high

D) nonexistent

A) comparable to that of an audit

B) moderate

C) high

D) nonexistent

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

12

When compiling the financial statements of a private company, an accountant should ________.

A) review agreements with financial institutions for restrictions on cash balances

B) study and understand the client's business

C) enquire of key personnel concerning related parties and subsequent events

D) perform ratio analyses of the financial data of comparable prior periods

A) review agreements with financial institutions for restrictions on cash balances

B) study and understand the client's business

C) enquire of key personnel concerning related parties and subsequent events

D) perform ratio analyses of the financial data of comparable prior periods

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

13

An accountant's review engagement report would NOT include a statement that ________.

A) the engagement was performed in accordance with generally accepted auditing standards (GAAS)

B) an accountant reviews information supplied by the company

C) a review does not constitute an audit and an audit opinion is not expressed on the financial statements

D) the accountant is not aware of any material departure from generally accepted accounting standards (GAAP)

A) the engagement was performed in accordance with generally accepted auditing standards (GAAS)

B) an accountant reviews information supplied by the company

C) a review does not constitute an audit and an audit opinion is not expressed on the financial statements

D) the accountant is not aware of any material departure from generally accepted accounting standards (GAAP)

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

14

If an accountant is engaged to compile the financial statements of a private entity and the statements omit substantially all disclosures required by GAAP, which of the following alternatives is correct?

A) If the accountant concludes that the omissions result in misleading financial statements and the matter cannot be resolved, the accountant should withdraw from the engagement.

B) The report should be amended to state that the financial statements have been prepared in accordance with a comprehensive basis of accounting other than GAAP.

C) The report should be amended to state that the financial statements have not been compiled in accordance with standards for compilation and review engagements.

D) The report should indicate that the statements are special-purpose financial statements that are not comparable to those of prior periods.

A) If the accountant concludes that the omissions result in misleading financial statements and the matter cannot be resolved, the accountant should withdraw from the engagement.

B) The report should be amended to state that the financial statements have been prepared in accordance with a comprehensive basis of accounting other than GAAP.

C) The report should be amended to state that the financial statements have not been compiled in accordance with standards for compilation and review engagements.

D) The report should indicate that the statements are special-purpose financial statements that are not comparable to those of prior periods.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

15

An auditor is most concerned that interim financial statements are not misleading relative to ________.

A) the prior year's interim financial statements

B) the annual report

C) pro forma financial statements

D) the prior year's annual financial statements

A) the prior year's interim financial statements

B) the annual report

C) pro forma financial statements

D) the prior year's annual financial statements

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following statements about a compilation engagement is NOT true?

A) The accountant must have adequate technical training and proficiency in accounting.

B) The accountant does not have to have an objective state of mind.

C) The statements must comply with generally accepted accounting principles.

D) The accountant should adequately plan and properly execute the work.

A) The accountant must have adequate technical training and proficiency in accounting.

B) The accountant does not have to have an objective state of mind.

C) The statements must comply with generally accepted accounting principles.

D) The accountant should adequately plan and properly execute the work.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

17

The scope of a review engagement is ________.

A) similar to that of an audit

B) less than that of a compilation

C) less than that of an audit

D) more than that of an audit

A) similar to that of an audit

B) less than that of a compilation

C) less than that of an audit

D) more than that of an audit

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

18

An accountant's communication on the financial statements in a compilation engagement would NOT include a statement that ________.

A) the statements may not be appropriate for the purposes of users

B) the financial statement information has been compiled

C) a compilation engagement consists primarily of inquiries of company personnel and analytical procedures applied to financial data

D) financial statements have not been audited or reviewed and the accountant did not attempt to verify accuracy or completeness.

A) the statements may not be appropriate for the purposes of users

B) the financial statement information has been compiled

C) a compilation engagement consists primarily of inquiries of company personnel and analytical procedures applied to financial data

D) financial statements have not been audited or reviewed and the accountant did not attempt to verify accuracy or completeness.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

19

When unaudited financial statements are presented in comparative form with audited financial statements, such statements should be ________.

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

20

CPA is a minority shareholder in ABC Co., and has just completed a compilation engagement for the company. The Notice to Reader should ________.

A) disclaim an opinion

B) provide negative assurance

C) include a statement that CPA is not objective

D) not be issued, since CPA is not objective

A) disclaim an opinion

B) provide negative assurance

C) include a statement that CPA is not objective

D) not be issued, since CPA is not objective

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

21

The scope of a review engagement is similar to that of an audit.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

22

A review engagement consists primarily of enquiry, analytical procedures, and discussion.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

23

According to the Guidance on Criteria of Control (CoCo), control is effected by ________.

A) senior management

B) the board of directors

C) people throughout the organization

D) the audit committee

A) senior management

B) the board of directors

C) people throughout the organization

D) the audit committee

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

24

Financial statements must be presented fairly as a result of a compilation engagement.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

25

Review engagements involve both substantive and compliance testing.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

26

Accounting principles require that interim financial statements be prepared.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

27

In providing guidance to accountants, which ranks highest?

A) Research study.

B) Criteria of Control guidance.

C) CPA Canada Handbook Recommendation.

D) CPA Canada Handbook Guideline.

A) Research study.

B) Criteria of Control guidance.

C) CPA Canada Handbook Recommendation.

D) CPA Canada Handbook Guideline.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

28

An accountant who is not independent can compile financial statements for a private company as long as the fact of lack of independence is disclosed in the body of the report.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

29

Auditing standards apply to work on all audited financial statements but not to work on other assurance engagements.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

30

In a compilation engagement, the accountant performs no audit procedures.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

31

Snow, CPA, was engaged by Master Limited to examine and report on management's written assertion about the effectiveness of Master's internal control system over financial reporting. Snow's report should state that ________.

A) because of the inherent limitations in any system of internal control, errors or irregularities may occur and not be detected.

B) management's assertion is based on criteria established by the Chartered Professional Accounts of Canada.

C) the results of Snow's tests will form the basis for Snow's opinion on the fairness of Master's financial statements in conformity with GAAP.

D) the purpose of the engagement is to enable Snow to plan an audit and determine the nature, timing, and extent of tests to be performed.

A) because of the inherent limitations in any system of internal control, errors or irregularities may occur and not be detected.

B) management's assertion is based on criteria established by the Chartered Professional Accounts of Canada.

C) the results of Snow's tests will form the basis for Snow's opinion on the fairness of Master's financial statements in conformity with GAAP.

D) the purpose of the engagement is to enable Snow to plan an audit and determine the nature, timing, and extent of tests to be performed.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following best describes a CPA's engagement to report on an entity's internal controls over financial reporting?

A) An assurance engagement to examine and report on management's written assertions about the effectiveness of its internal control system.

B) An audit engagement to render an opinion on the entity's internal control system.

C) A prospective engagement to project, for a period of time not to exceed one year, and report on the expected benefits of the entity's internal control structure.

D) A consulting engagement to provide constructive advice to the entity on its internal control system.

A) An assurance engagement to examine and report on management's written assertions about the effectiveness of its internal control system.

B) An audit engagement to render an opinion on the entity's internal control system.

C) A prospective engagement to project, for a period of time not to exceed one year, and report on the expected benefits of the entity's internal control structure.

D) A consulting engagement to provide constructive advice to the entity on its internal control system.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

33

Personal financial planning has become a big source of business for professional accounting firms.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

34

In a compilation engagement, the financial statements must at least comply with GAAP.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

35

Few, if any, procedures are performed during a compilation engagement.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

36

Review engagement standards require that the accountant performing the engagement have an objective state of mind.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

37

Review engagements provide a moderate level of assurance.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

38

The auditor learned the following in the course of an audit engagement. Which of the items, discovered by the auditor, need NOT be communicated to the audit committee?

A) The theft of several items of inventory by warehouse employees.

B) Management's significant accounting policies.

C) Significant audit adjustments recommended by the auditors.

D) All of these items should be communicated to the audit committee.

A) The theft of several items of inventory by warehouse employees.

B) Management's significant accounting policies.

C) Significant audit adjustments recommended by the auditors.

D) All of these items should be communicated to the audit committee.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

39

According to auditing standards, reportable matters ________.

A) must be searched for by auditors

B) must be reported by auditors if they come to their attention

C) may only be reported to management

D) may be reported on verbally or in writing

A) must be searched for by auditors

B) must be reported by auditors if they come to their attention

C) may only be reported to management

D) may be reported on verbally or in writing

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

40

An auditor has been engaged to report on management's report on internal control. Management's report points to a material weakness in its system of internal controls over inventory. The auditor's report should be a(n) ________.

A) adverse opinion

B) qualified opinion for a GAAP departure

C) clean opinion

D) clean opinion with an emphasis of matter paragraph

A) adverse opinion

B) qualified opinion for a GAAP departure

C) clean opinion

D) clean opinion with an emphasis of matter paragraph

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

41

When should reviews of interim financial information be performed?

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

42

This question relates to other public accounting services and reports. For each statement numbered 1 through 5, match the statement to the correct engagement or report (A through E) and place the identifying letter in the space provided.

A. A review engagement of the financial statements of a private company

B. A compilation engagement

C. A review of the interim financial statements of a public company

D. A report on financial statements prepared in accordance with an appropriate disclosed basis of accounting

E. Accuracy

____ 1. The information should be in accordance with to generally accepted accounting principles.

____ 2. In our opinion, the schedule of accounts receivable referred to above presents fairly, in all material respects.

____ 3. from information provided by management.

____ 4. As described in Note 2, these financial statements were prepared in accordance with accounting principles prescribed for School Boards in Ontario.

____ 5. does not constitute an audit and consequently I do not express an audit opinion.

A. A review engagement of the financial statements of a private company

B. A compilation engagement

C. A review of the interim financial statements of a public company

D. A report on financial statements prepared in accordance with an appropriate disclosed basis of accounting

E. Accuracy

____ 1. The information should be in accordance with to generally accepted accounting principles.

____ 2. In our opinion, the schedule of accounts receivable referred to above presents fairly, in all material respects.

____ 3. from information provided by management.

____ 4. As described in Note 2, these financial statements were prepared in accordance with accounting principles prescribed for School Boards in Ontario.

____ 5. does not constitute an audit and consequently I do not express an audit opinion.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

43

Under CPA Canada rules, the auditor verifies the accuracy of management's internal controls statement just as he or she verifies the accuracy of financial statements.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

44

Interim financial information is a basic and necessary element of financial statements that conform to GAAP.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

45

George Wilson CPA is on the board of directors of a small manufacturing company, Smith Plastics, Inc. The president of the company, John Smith, has asked George to prepare financial statements for the company to be submitted to Vancouver Dominion Bank as part of a loan request. Mr. Smith tells George that the bank would like a review or an audit, but would settle for a compilation from a CPA. He would like George to do the compilation.

Required:

Under what conditions, if any, would George Wilson be allowed to compile the financial statements of Smith Plastics, Inc.?

Required:

Under what conditions, if any, would George Wilson be allowed to compile the financial statements of Smith Plastics, Inc.?

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

46

What does the extent of review procedures of interim financial information depend on?

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

47

Donna Prima, CPA, was engaged to review the financial statements of Rooster Restaurants, Inc., a private company. During her review, Donna found that Rooster had not capitalized leases as required under GAAP. The result was so material, that Donna modified the standard review report to state that "the financial statements are not in accordance with GAAP."

Required:

Is Prima's report in accordance with professional standards? If not, what should she have done under the circumstances? Explain.

Required:

Is Prima's report in accordance with professional standards? If not, what should she have done under the circumstances? Explain.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

48

List three matters which the auditor is responsible for reporting on to the audit committee of a public company.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

49

Auditors are obligated to search for "reportable matters."

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

50

When providing assurance on internal control, the auditor provides a negative assurance report.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

51

What is meant by "audit of internal control over financial reporting?"

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 51 flashcards in this deck.