Deck 13: Overhead and Marketing Variances

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Developing Additional Variances for Performance Evaluation

Saidwell Company manufactures washers and dryers on a single assembly line in its main factory. The market has deteriorated over the last five years and competition has made cost control very important. Management has been concerned about the materials costs of both washers and dryers. There have been no model changes in the past two years, and economic conditions have allowed the company to negotiate price reductions for many key parts.

Saidwell uses a standard cost system in accounting for materials. Purchases are charged to inventory at a standard price, and purchase discounts are considered an administrative cost reduction. Production is charged at the standard price of the materials used. Thus, the price variance is isolated at time of purchase as the difference between gross contract price and standard price multiplied by the quantity purchased. When a substitute part is used in production, a price variance equal to the difference in the standard prices of the materials is recognized at the time of substitution. The quantity variance is the actual quantity used compared with the standard quantity allowed, with the difference multiplied by the standard price.

The materials variances for several of the parts Saidwell uses are unfavorable. Part #4121 is one item that has an unfavorable variance. Saidwell knows that some of these parts are defective and will fail. The failure is discovered during production. The normal defective rate is 5 percent of normal input. The original contract price of this part was $0.285 per unit; thus, Saidwell set the standard unit price at $0.285. The unit contract purchase price of Part #4121 was increased to $0.325 from the original $0.285 due to a parts specification change. Saidwell chose not to change the standard; it treated the increase in price as a price variance. In addition, the contract terms were changed from payment due in 30 days to a 4 percent discount if paid in 10 days or full payment due in 30 days. These new contractual terms were the consequence of negotiations resulting from changes in the economy.

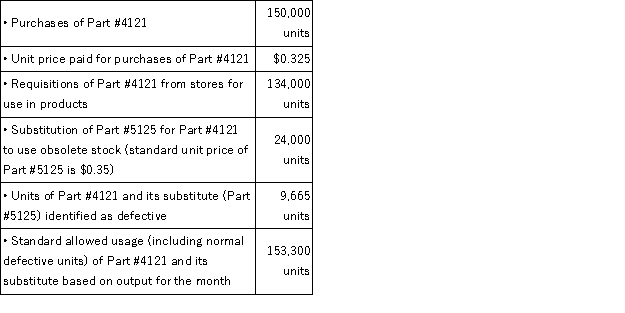

Data regarding the use of Part #4121 during December are as follows. Saidwell's material variances related to Part #4121 for December were reported as follows:

Saidwell's material variances related to Part #4121 for December were reported as follows:  Bob Speck, the purchasing director, claims the unfavorable price variance is misleading. Speck says that his department has worked hard to obtain price concessions and purchase discounts from suppliers. In addition, Speck says engineering changes in several parts have increased their prices, even though the part identification has not changed. These price increases are not his department's responsibility. Speck declares that price variances no longer measure purchasing's performance.

Bob Speck, the purchasing director, claims the unfavorable price variance is misleading. Speck says that his department has worked hard to obtain price concessions and purchase discounts from suppliers. In addition, Speck says engineering changes in several parts have increased their prices, even though the part identification has not changed. These price increases are not his department's responsibility. Speck declares that price variances no longer measure purchasing's performance.

Jim Buddle, the manufacturing manager, thinks the responsibility for the quantity variance should be shared. Buddle states that manufacturing cannot control quality associated with less expensive parts, substitutions of material to use up otherwise obsolete stock, or engineering changes that increase the quantity of materials used.

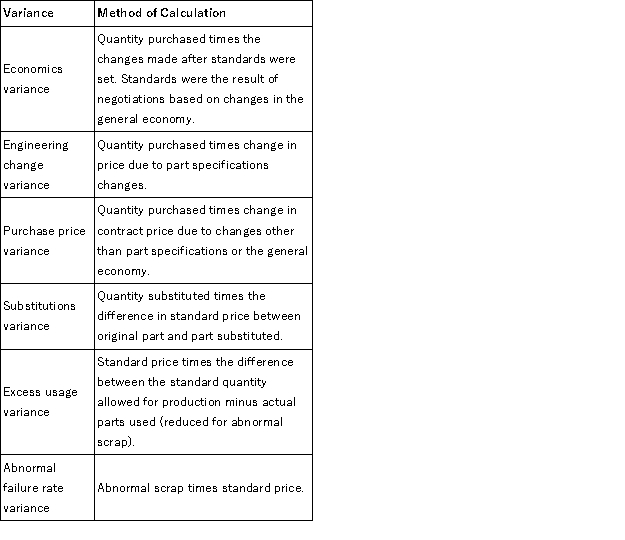

The accounting manager, Mike Kohl, suggests that the computation of variances be changed to identify variations from standard with the causes and functional areas responsible for the variances. Kohl recommends the following system of materials variances and the method of computation for each: Required:

Required:

a. Discuss the appropriateness of Saidwell Company's current method of variance analysis for materials and indicate whether the claims of Bob Speck and Jim Buddle are valid.

b. Compute the materials variances for Part #4121 for December using the system recommended by Mike Kohl.

c. Who would be responsible for each of the variances in Mike Kohl's system of variance analysis for materials?

Saidwell Company manufactures washers and dryers on a single assembly line in its main factory. The market has deteriorated over the last five years and competition has made cost control very important. Management has been concerned about the materials costs of both washers and dryers. There have been no model changes in the past two years, and economic conditions have allowed the company to negotiate price reductions for many key parts.

Saidwell uses a standard cost system in accounting for materials. Purchases are charged to inventory at a standard price, and purchase discounts are considered an administrative cost reduction. Production is charged at the standard price of the materials used. Thus, the price variance is isolated at time of purchase as the difference between gross contract price and standard price multiplied by the quantity purchased. When a substitute part is used in production, a price variance equal to the difference in the standard prices of the materials is recognized at the time of substitution. The quantity variance is the actual quantity used compared with the standard quantity allowed, with the difference multiplied by the standard price.

The materials variances for several of the parts Saidwell uses are unfavorable. Part #4121 is one item that has an unfavorable variance. Saidwell knows that some of these parts are defective and will fail. The failure is discovered during production. The normal defective rate is 5 percent of normal input. The original contract price of this part was $0.285 per unit; thus, Saidwell set the standard unit price at $0.285. The unit contract purchase price of Part #4121 was increased to $0.325 from the original $0.285 due to a parts specification change. Saidwell chose not to change the standard; it treated the increase in price as a price variance. In addition, the contract terms were changed from payment due in 30 days to a 4 percent discount if paid in 10 days or full payment due in 30 days. These new contractual terms were the consequence of negotiations resulting from changes in the economy.

Data regarding the use of Part #4121 during December are as follows.

Saidwell's material variances related to Part #4121 for December were reported as follows: Bob Speck, the purchasing director, claims the unfavorable price variance is misleading. Speck says that his department has worked hard to obtain price concessions and purchase discounts from suppliers. In addition, Speck says engineering changes in several parts have increased their prices, even though the part identification has not changed. These price increases are not his department's responsibility. Speck declares that price variances no longer measure purchasing's performance.Jim Buddle, the manufacturing manager, thinks the responsibility for the quantity variance should be shared. Buddle states that manufacturing cannot control quality associated with less expensive parts, substitutions of material to use up otherwise obsolete stock, or engineering changes that increase the quantity of materials used.

The accounting manager, Mike Kohl, suggests that the computation of variances be changed to identify variations from standard with the causes and functional areas responsible for the variances. Kohl recommends the following system of materials variances and the method of computation for each:

Required:a. Discuss the appropriateness of Saidwell Company's current method of variance analysis for materials and indicate whether the claims of Bob Speck and Jim Buddle are valid.

b. Compute the materials variances for Part #4121 for December using the system recommended by Mike Kohl.

c. Who would be responsible for each of the variances in Mike Kohl's system of variance analysis for materials?

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/16

Play

Full screen (f)

Deck 13: Overhead and Marketing Variances

1

Wendy Wall (WW) makes wall units. For the year, the following details have been budgeted. Output, 10,000 units; factory overheads $1,250,000, of which 60% is variable. Each wall unit should take 2.5 hours of direct labor to produce. WW produced 9,500 units with 24,000 DLH used and $1,175,000 actual overhead was incurred. Overhead is allocated based on direct labor hours (DLH). What is Wendy's total overhead absorbed?

A)$1,175,000

B)$1,200,000

C)$1,187,500

D)$1,250,000

E)None of the above

A)$1,175,000

B)$1,200,000

C)$1,187,500

D)$1,250,000

E)None of the above

C

2

The overhead volume variance:

A)captures the difference between planned overheads and actual overheads

B)measures underutilized capacity

C)measures the opportunity cost of actual capacity utilization differing from planned capacity utilization

D)as a performance measure encourages overproduction

E)all of the above

A)captures the difference between planned overheads and actual overheads

B)measures underutilized capacity

C)measures the opportunity cost of actual capacity utilization differing from planned capacity utilization

D)as a performance measure encourages overproduction

E)all of the above

D

3

Boris Bangles planned to sell 280,000 banjos at $400 each, but actually sold 250,000 at $425 each. Which is true of BB's sales price variances?

A)$6.25 million unfav

B)$12 million fav

C)$6.25 million fav

D)$5.75 million fav

E)None of the above

A)$6.25 million unfav

B)$12 million fav

C)$6.25 million fav

D)$5.75 million fav

E)None of the above

C

4

Basic Overhead Variances

Derf Company applies overhead on the basis of direct labor hours. Two direct labor hours are required for each product unit. Planned production for the period was set at 9,000 units. Manufacturing overhead for the period is budgeted at $135,000, of which 20 percent is fixed. The 17,200 hours worked during the period resulted in production of 8,500 units. Manufacturing overhead cost incurred was $136,500.

Required:

Calculate the following three overhead variances:

1. Overhead volume variance.

2. Overhead efficiency variance.

3. Overhead spending variance.

Derf Company applies overhead on the basis of direct labor hours. Two direct labor hours are required for each product unit. Planned production for the period was set at 9,000 units. Manufacturing overhead for the period is budgeted at $135,000, of which 20 percent is fixed. The 17,200 hours worked during the period resulted in production of 8,500 units. Manufacturing overhead cost incurred was $136,500.

Required:

Calculate the following three overhead variances:

1. Overhead volume variance.

2. Overhead efficiency variance.

3. Overhead spending variance.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

5

Karpoff Kremes (KK) planned to sell 40,000 Kings at $20 each and 20,000 Kweens at $15 each. Actual sales of the former were 45,000 and 25,000 of the latter, at $19 and $16 respectively. Which is true of KK?

A)The price variance is $20,000 fav

B)The quantity variance is $175,000 unfav

C)The price variance is $20,000 unfav

D)The quantity variance is $20,000 unfav

E)None of the above

A)The price variance is $20,000 fav

B)The quantity variance is $175,000 unfav

C)The price variance is $20,000 unfav

D)The quantity variance is $20,000 unfav

E)None of the above

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

6

The following information is for the third quarter of this year: Required:

Calculate the following three overhead variances:

1. Overhead volume variance

2. Overhead efficiency variance

3. Overhead spending variance

Calculate the following three overhead variances:

1. Overhead volume variance

2. Overhead efficiency variance

3. Overhead spending variance

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

7

Overhead Variances

Overhead is applied on the basis of direct labor hours. Three direct labor hours are required for each product unit. Planned production for the period was set at 8,000 units. Manufacturing overhead for the period is budgeted at $204,000, of which 30 percent is fixed. The 26,200 hours worked during the period resulted in production of 8,500 units. Manufacturing overhead cost incurred was $220,500.

Required:

Calculate the following three overhead variances:

1. Overhead volume variance

2. Overhead efficiency variance

3. Overhead spending variance

Overhead is applied on the basis of direct labor hours. Three direct labor hours are required for each product unit. Planned production for the period was set at 8,000 units. Manufacturing overhead for the period is budgeted at $204,000, of which 30 percent is fixed. The 26,200 hours worked during the period resulted in production of 8,500 units. Manufacturing overhead cost incurred was $220,500.

Required:

Calculate the following three overhead variances:

1. Overhead volume variance

2. Overhead efficiency variance

3. Overhead spending variance

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

8

Wendy Wall (WW) makes wall units. For the year, the following details have been budgeted. Output, 10,000 units; factory overheads $1,250,000, of which 60% is variable. Each wall unit should take 2.5 hours of direct labor to produce. WW produced 9,500 units with 24,000 DLH used and $1,175,000 actual overhead was incurred. Overhead is allocated based on direct labor hours (DLH). What is true of Wendy's overhead variances?

A)Overhead spending variance is $45,000 fav

B)Overhead efficiency variance is $7,500 fav

C)Overhead volume variance is $25,000 fav

D)Overhead spending variance is $37,500 fav

E)None of the above

A)Overhead spending variance is $45,000 fav

B)Overhead efficiency variance is $7,500 fav

C)Overhead volume variance is $25,000 fav

D)Overhead spending variance is $37,500 fav

E)None of the above

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

9

Wendy Wall (WW) makes wall units. For the year, the following details have been budgeted. Output, 10,000 units; factory overheads $1,250,000, of which 60% is variable. Each wall unit should take 2.5 hours of direct labor to produce. WW produced 9,500 units with 24,000 DLH used and $1,175,000 actual overhead was incurred. Overhead is allocated based on direct labor hours (DLH). What is Wendy's total overhead variance?

A)$75,000 over absorbed

B)$12,500 over absorbed

C)$12,500 under absorbed

D)$25,000 over absorbed

E)None of the above

A)$75,000 over absorbed

B)$12,500 over absorbed

C)$12,500 under absorbed

D)$25,000 over absorbed

E)None of the above

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

10

Karpoff Kremes (KK) planned to sell 40,000 Kings at $20 each and 20,000 Kweens at $15 each. Actual sales of the former were 45,000 and 25,000 of the latter, at $19 and $16 respectively. Which is true of KK's mix variance?

A)$0

B)$175,000 fav

C)$28,333 fav

D)$8,333 unfav

E)Unable to determine

A)$0

B)$175,000 fav

C)$28,333 fav

D)$8,333 unfav

E)Unable to determine

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

11

Which of these is true?

A)Budgeted volume = Actual output × units allowed

B)Actual volume = Budgeted output × actual units allowed

C)Expected volume = Standard volume

D)Standard volume = Actual output × # cost driver units allowed

E)None of the above

A)Budgeted volume = Actual output × units allowed

B)Actual volume = Budgeted output × actual units allowed

C)Expected volume = Standard volume

D)Standard volume = Actual output × # cost driver units allowed

E)None of the above

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

12

Developing Additional Variances for Performance Evaluation

Saidwell Company manufactures washers and dryers on a single assembly line in its main factory. The market has deteriorated over the last five years and competition has made cost control very important. Management has been concerned about the materials costs of both washers and dryers. There have been no model changes in the past two years, and economic conditions have allowed the company to negotiate price reductions for many key parts.

Saidwell uses a standard cost system in accounting for materials. Purchases are charged to inventory at a standard price, and purchase discounts are considered an administrative cost reduction. Production is charged at the standard price of the materials used. Thus, the price variance is isolated at time of purchase as the difference between gross contract price and standard price multiplied by the quantity purchased. When a substitute part is used in production, a price variance equal to the difference in the standard prices of the materials is recognized at the time of substitution. The quantity variance is the actual quantity used compared with the standard quantity allowed, with the difference multiplied by the standard price.

The materials variances for several of the parts Saidwell uses are unfavorable. Part #4121 is one item that has an unfavorable variance. Saidwell knows that some of these parts are defective and will fail. The failure is discovered during production. The normal defective rate is 5 percent of normal input. The original contract price of this part was $0.285 per unit; thus, Saidwell set the standard unit price at $0.285. The unit contract purchase price of Part #4121 was increased to $0.325 from the original $0.285 due to a parts specification change. Saidwell chose not to change the standard; it treated the increase in price as a price variance. In addition, the contract terms were changed from payment due in 30 days to a 4 percent discount if paid in 10 days or full payment due in 30 days. These new contractual terms were the consequence of negotiations resulting from changes in the economy.

Data regarding the use of Part #4121 during December are as follows. Saidwell's material variances related to Part #4121 for December were reported as follows: Bob Speck, the purchasing director, claims the unfavorable price variance is misleading. Speck says that his department has worked hard to obtain price concessions and purchase discounts from suppliers. In addition, Speck says engineering changes in several parts have increased their prices, even though the part identification has not changed. These price increases are not his department's responsibility. Speck declares that price variances no longer measure purchasing's performance.

Jim Buddle, the manufacturing manager, thinks the responsibility for the quantity variance should be shared. Buddle states that manufacturing cannot control quality associated with less expensive parts, substitutions of material to use up otherwise obsolete stock, or engineering changes that increase the quantity of materials used.

The accounting manager, Mike Kohl, suggests that the computation of variances be changed to identify variations from standard with the causes and functional areas responsible for the variances. Kohl recommends the following system of materials variances and the method of computation for each: Required:

a. Discuss the appropriateness of Saidwell Company's current method of variance analysis for materials and indicate whether the claims of Bob Speck and Jim Buddle are valid.

b. Compute the materials variances for Part #4121 for December using the system recommended by Mike Kohl.

c. Who would be responsible for each of the variances in Mike Kohl's system of variance analysis for materials?

Saidwell Company manufactures washers and dryers on a single assembly line in its main factory. The market has deteriorated over the last five years and competition has made cost control very important. Management has been concerned about the materials costs of both washers and dryers. There have been no model changes in the past two years, and economic conditions have allowed the company to negotiate price reductions for many key parts.

Saidwell uses a standard cost system in accounting for materials. Purchases are charged to inventory at a standard price, and purchase discounts are considered an administrative cost reduction. Production is charged at the standard price of the materials used. Thus, the price variance is isolated at time of purchase as the difference between gross contract price and standard price multiplied by the quantity purchased. When a substitute part is used in production, a price variance equal to the difference in the standard prices of the materials is recognized at the time of substitution. The quantity variance is the actual quantity used compared with the standard quantity allowed, with the difference multiplied by the standard price.

The materials variances for several of the parts Saidwell uses are unfavorable. Part #4121 is one item that has an unfavorable variance. Saidwell knows that some of these parts are defective and will fail. The failure is discovered during production. The normal defective rate is 5 percent of normal input. The original contract price of this part was $0.285 per unit; thus, Saidwell set the standard unit price at $0.285. The unit contract purchase price of Part #4121 was increased to $0.325 from the original $0.285 due to a parts specification change. Saidwell chose not to change the standard; it treated the increase in price as a price variance. In addition, the contract terms were changed from payment due in 30 days to a 4 percent discount if paid in 10 days or full payment due in 30 days. These new contractual terms were the consequence of negotiations resulting from changes in the economy.

Data regarding the use of Part #4121 during December are as follows.

Saidwell's material variances related to Part #4121 for December were reported as follows: Bob Speck, the purchasing director, claims the unfavorable price variance is misleading. Speck says that his department has worked hard to obtain price concessions and purchase discounts from suppliers. In addition, Speck says engineering changes in several parts have increased their prices, even though the part identification has not changed. These price increases are not his department's responsibility. Speck declares that price variances no longer measure purchasing's performance.Jim Buddle, the manufacturing manager, thinks the responsibility for the quantity variance should be shared. Buddle states that manufacturing cannot control quality associated with less expensive parts, substitutions of material to use up otherwise obsolete stock, or engineering changes that increase the quantity of materials used.

The accounting manager, Mike Kohl, suggests that the computation of variances be changed to identify variations from standard with the causes and functional areas responsible for the variances. Kohl recommends the following system of materials variances and the method of computation for each:

Required:a. Discuss the appropriateness of Saidwell Company's current method of variance analysis for materials and indicate whether the claims of Bob Speck and Jim Buddle are valid.

b. Compute the materials variances for Part #4121 for December using the system recommended by Mike Kohl.

c. Who would be responsible for each of the variances in Mike Kohl's system of variance analysis for materials?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

13

Which of these is true?

A)Budgeted fixed factory overheads = Budgeted overheads per unit × actual volume

B)Budgeted fixed factory overheads = Budgeted overheads per unit × standard volume

C)Budgeted factory overheads = Budgeted fixed overheads per unit × budgeted volume + actual variable overheads

D)Budgeted factory overheads = Budgeted fixed overheads per unit × standard volume + budgeted variable overheads

E)None of the above

A)Budgeted fixed factory overheads = Budgeted overheads per unit × actual volume

B)Budgeted fixed factory overheads = Budgeted overheads per unit × standard volume

C)Budgeted factory overheads = Budgeted fixed overheads per unit × budgeted volume + actual variable overheads

D)Budgeted factory overheads = Budgeted fixed overheads per unit × standard volume + budgeted variable overheads

E)None of the above

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

14

Which is true of BB's sales quantity variances?

A)$12 million unfav

B)$5.75 million fav

C)$5.75 million unfav

D)$6.25 million unfav

E)None of the above

A)$12 million unfav

B)$5.75 million fav

C)$5.75 million unfav

D)$6.25 million unfav

E)None of the above

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

15

Karpoff Kremes (KK) planned to sell 40,000 Kings at $20 each and 20,000 Kweens at $15 each. Actual sales of the former were 45,000 and 25,000 of the latter, at $19 and $16 respectively. Which is true of KK's sales variance?

A)$183,333 fav

B)$155,000 fav

C)$163,333 fav

D)$175,000 fav

E)None of the above

A)$183,333 fav

B)$155,000 fav

C)$163,333 fav

D)$175,000 fav

E)None of the above

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

16

Wendy Wall (WW) makes wall units. For the year, the following details have been budgeted. Output, 10,000 units; factory overheads $1,250,000, of which 60% is variable. Each wall unit should take 2.5 hours of direct labor to produce. WW produced 9,500 units with 24,000 DLH used and $1,175,000 actual overhead was incurred. Overhead is allocated based on direct labor hours (DLH). What is the correct overhead absorption rate (to nearest cent)?

A)$52.63

B)$50.00

C)$49.47

D)$47.00

E)None of the above

A)$52.63

B)$50.00

C)$49.47

D)$47.00

E)None of the above

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 16 flashcards in this deck.