Deck 10: Criticisms of Absorption Cost Systems: Incentives to Overproduce

Full screen (f)

Question

Question

Question

Question

Question

An Extreme Version of Variable Costing

Eli Goldratt advocates that all manufacturing costs other than materials be treated as operating expenses for the period. Periodic profits would be calculated as: Operating data for last year are

Operating data for last year are  There is no beginning inventory.

There is no beginning inventory.

Required:

a. Compare profits under absorption costing and Goldratt's method.

b. Evaluate Goldratt's proposal.

Eli Goldratt advocates that all manufacturing costs other than materials be treated as operating expenses for the period. Periodic profits would be calculated as:

Operating data for last year are There is no beginning inventory.Required:

a. Compare profits under absorption costing and Goldratt's method.

b. Evaluate Goldratt's proposal.

Question

Question

Chamiching makes hacksaw blades. Inventory values are determined using the first in, first out (FIFO) method. Production and sales data for the first three years appear below.

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?

A)Variable costing income (VCI) exceeds full costing income (FCI) every year

B)VCI exceeds FCI in Yrs 1 and 2 only

C)VCI exceeds FCI in Yrs 2 and 3 only

D)VCI never exceeds FCI

E)None of the above

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?A)Variable costing income (VCI) exceeds full costing income (FCI) every year

B)VCI exceeds FCI in Yrs 1 and 2 only

C)VCI exceeds FCI in Yrs 2 and 3 only

D)VCI never exceeds FCI

E)None of the above

Question

Question

Question

Question

Chamiching makes hacksaw blades. Inventory values are determined using the first in, first out (FIFO) method. Production and sales data for the first three years appear below.

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, if variable costing is used, which of the following is true?

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, if variable costing is used, which of the following is true?

A)Yr 3's gross profit is $171,687

B)Yr 1's gross profit is $48,000

C)Yr 2's gross profit is $123,200

D)Yr 2's gross profit is $129,513

E)None of the above

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, if variable costing is used, which of the following is true?A)Yr 3's gross profit is $171,687

B)Yr 1's gross profit is $48,000

C)Yr 2's gross profit is $123,200

D)Yr 2's gross profit is $129,513

E)None of the above

Question

Chamiching makes hacksaw blades. Inventory values are determined using the first in, first out (FIFO) method. Production and sales data for the first three years appear below.

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, when variable costing income is reconciled to absorption costing income, which of the following is true?

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, when variable costing income is reconciled to absorption costing income, which of the following is true?

A)In Yr 1, $12,000 is added to variable costing income to find absorption costing income

B)In Yr 3, $6,887 is added to variable costing income to find absorption costing income

C)In Yr 2, $5,113 is deducted from variable costing income to find absorption costing income

D)In Yr 2, $5,113 is added to variable costing income to find absorption costing income

E)None of the above

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, when variable costing income is reconciled to absorption costing income, which of the following is true?A)In Yr 1, $12,000 is added to variable costing income to find absorption costing income

B)In Yr 3, $6,887 is added to variable costing income to find absorption costing income

C)In Yr 2, $5,113 is deducted from variable costing income to find absorption costing income

D)In Yr 2, $5,113 is added to variable costing income to find absorption costing income

E)None of the above

Question

Chamiching makes hacksaw blades. Inventory values are determined using the first in, first out (FIFO) method. Production and sales data for the first three years appear below.

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, if absorption costing is used, which of the following is true?

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, if absorption costing is used, which of the following is true?

A)Yr 1's ending inventory is $12,000

B)Yr 2's gross profit is $112,400

C)Yr 3's cost of goods sold is $123,200

D)Yr 3's goods available for sale is $266,000

E)None of the above

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, if absorption costing is used, which of the following is true?A)Yr 1's ending inventory is $12,000

B)Yr 2's gross profit is $112,400

C)Yr 3's cost of goods sold is $123,200

D)Yr 3's goods available for sale is $266,000

E)None of the above

Question

Chamiching makes hacksaw blades. Inventory values are determined using the first in, first out (FIFO) method. Production and sales data for the first three years appear below.

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?

A)The company should always choose absorption costing as it shows increasing profits every year

B)The company should always choose absorption costing because it facilitates income smoothing

C)Over the three years, Chamiching accumulates the same total income regardless of the choice of inventory costing method

D)b) and c) only

E)a, b and c

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?A)The company should always choose absorption costing as it shows increasing profits every year

B)The company should always choose absorption costing because it facilitates income smoothing

C)Over the three years, Chamiching accumulates the same total income regardless of the choice of inventory costing method

D)b) and c) only

E)a, b and c

Question

Question

Question

Question

Chamiching makes hacksaw blades. Inventory values are determined using the first in, first out (FIFO) method. Production and sales data for the first three years appear below.

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?

A)The variable cost of Yr 2 ending inventory is $6,887

B)The full cost of Yr 2 ending inventory is double the variable cost ending inventory

C)There are 3,000 hacksaw blades in ending inventory

D)The fixed cost per unit in Yr 3 is $2.72

E)None of the above

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?A)The variable cost of Yr 2 ending inventory is $6,887

B)The full cost of Yr 2 ending inventory is double the variable cost ending inventory

C)There are 3,000 hacksaw blades in ending inventory

D)The fixed cost per unit in Yr 3 is $2.72

E)None of the above

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/19

Play

Full screen (f)

Deck 10: Criticisms of Absorption Cost Systems: Incentives to Overproduce

1

Absorption costing of inventories, as required by US GAAP, has been criticized for encouraging managers to increase year-end inventories in order to boost reported profits. Which of the following techniques is the most effective at resolving this problem?

A)Senior management control of inventory levels

B)Adoption of just-in-time (JIT) production system

C)Reward managers based upon the residual income approach

D)Use variable costing to determine income for bonus purposes

E)None of the above

A)Senior management control of inventory levels

B)Adoption of just-in-time (JIT) production system

C)Reward managers based upon the residual income approach

D)Use variable costing to determine income for bonus purposes

E)None of the above

B

2

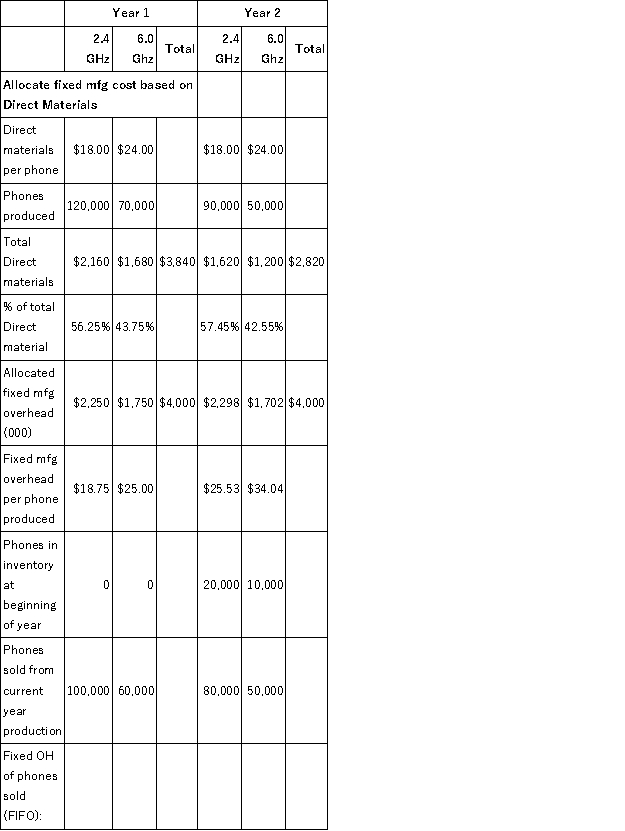

ViCom produces a wide range of consumer electronics. ViCom's Newark, New York, plant produces two types of cordless phones: 2.4 GHz and 6.0 GHz. The following table summarizes operations at the Newark ViCom plant for Year 1 and Year 2.

Fixed manufacturing overhead amounted to $4 million in each year. At the start of Year 1, there were no beginning inventories of either 2.4-GHz or 6.0-GHz cordless phones. ViCom uses FIFO to value inventories.

Required:

a. Prepare variable costing income statements for Year 1 and Year 2.

b. Prepare absorption costing income statements for Year 1 and Year 2. At the end of the year, fixed manufacturing overhead is absorbed to the two phone models using direct material as the allocation base.

c. Prepare a table that reconciles any differences in variable costing and absorption costing net incomes for Year 1 and Year 2.

Fixed manufacturing overhead amounted to $4 million in each year. At the start of Year 1, there were no beginning inventories of either 2.4-GHz or 6.0-GHz cordless phones. ViCom uses FIFO to value inventories.

Required:

a. Prepare variable costing income statements for Year 1 and Year 2.

b. Prepare absorption costing income statements for Year 1 and Year 2. At the end of the year, fixed manufacturing overhead is absorbed to the two phone models using direct material as the allocation base.

c. Prepare a table that reconciles any differences in variable costing and absorption costing net incomes for Year 1 and Year 2.

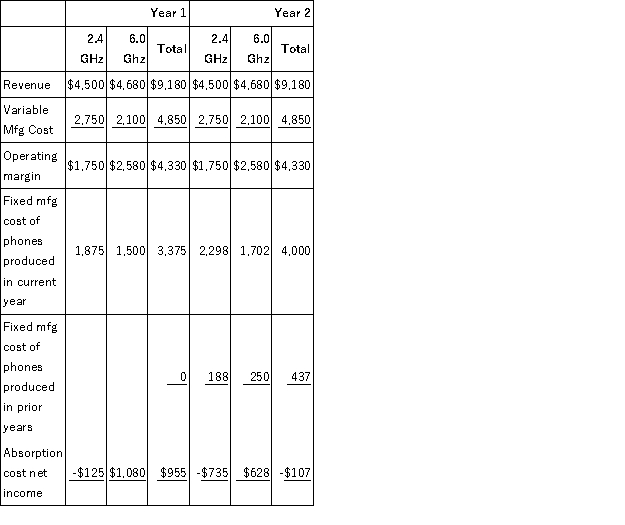

a. Variable cost income statements for Year 1 and Year 2 (thousands)

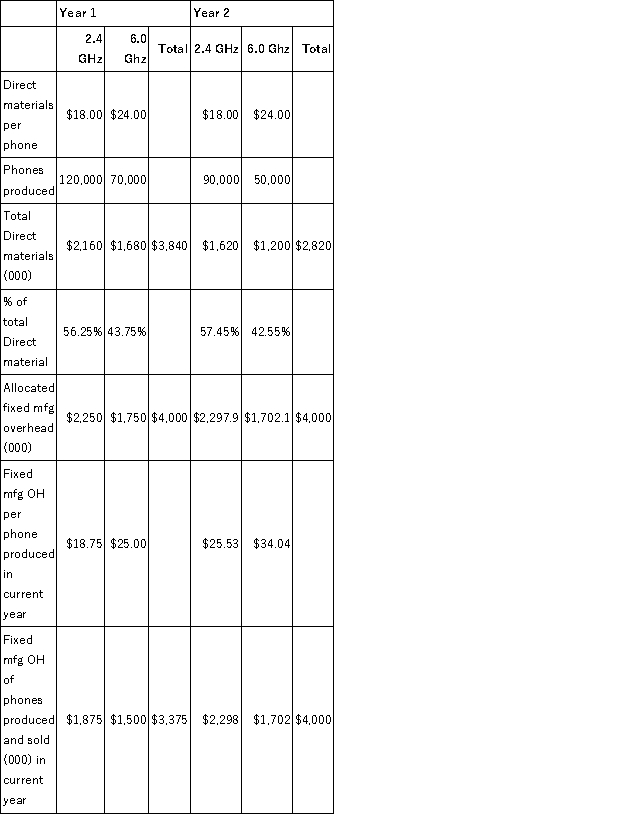

b. Absorption cost income statements for Year 1 and Year 2 using FIFO:

The first step is to allocate the fixed manufacturing overhead to the phones produced based on direct material dollars:

c. Reconciliation of variable and absorption cost net incomes for Year 1 and Year 2 (FIFO): The difference between absorption and variable cost net incomes in Year 1 is $625,000, which is the amount of fixed overhead in the inventory at the end of Year 1. At the end of Year 2, the cumulative difference between absorption and variable cost net incomes is $255,000, which is the amount of fixed overhead remaining in the inventory at the end of Year 2.

If instead of using FIFO, had ViCom used LIFO, the following would be the absorption cost net incomes for Year 1 and Year 2.

b. Absorption cost net income for Year 1 and Year 2 (LIFO). Using these allocated fixed manufacturing costs per phone, the absorption cost income statements (000):

Using these allocated fixed manufacturing costs per phone, the absorption cost income statements (000):  c. Reconciliation of variable and absorption cost net incomes for Year 1 and Year 2 (LIFO):

c. Reconciliation of variable and absorption cost net incomes for Year 1 and Year 2 (LIFO):

b. Absorption cost income statements for Year 1 and Year 2 using FIFO:

The first step is to allocate the fixed manufacturing overhead to the phones produced based on direct material dollars:

c. Reconciliation of variable and absorption cost net incomes for Year 1 and Year 2 (FIFO): The difference between absorption and variable cost net incomes in Year 1 is $625,000, which is the amount of fixed overhead in the inventory at the end of Year 1. At the end of Year 2, the cumulative difference between absorption and variable cost net incomes is $255,000, which is the amount of fixed overhead remaining in the inventory at the end of Year 2.

If instead of using FIFO, had ViCom used LIFO, the following would be the absorption cost net incomes for Year 1 and Year 2.

b. Absorption cost net income for Year 1 and Year 2 (LIFO).

Using these allocated fixed manufacturing costs per phone, the absorption cost income statements (000): c. Reconciliation of variable and absorption cost net incomes for Year 1 and Year 2 (LIFO): 3

Over-Production Incentives, ROA and Residual Income

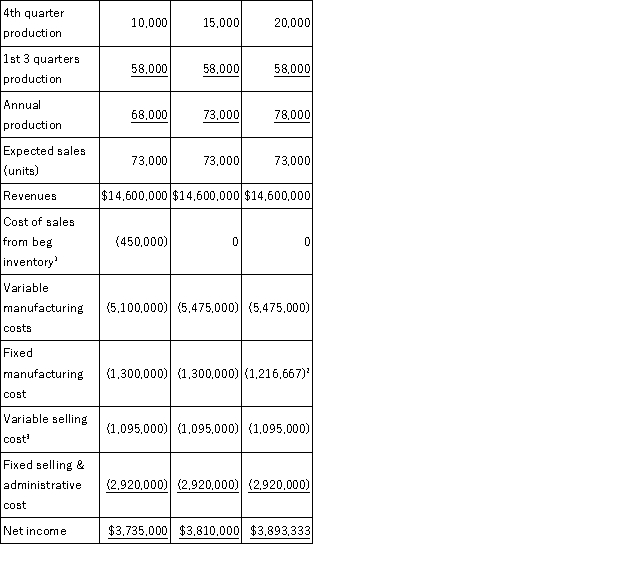

Eaststar manufactures and distributes a complete line of home appliances worldwide. Lynn Tweedie is the U.S. Space Saver Dishwasher product manager for Eaststar Appliances. Her responsibilities include pricing, planning, and sales of Eaststar's Space Saver dishwasher in the United States. It is the end of the third quarter and Tweedie is deciding how many Space Saver washers to produce in the fourth quarter. Given sales from the first three quarters and orders for the last quarter, she expects total sales for the year to be 73,000 washers at $200 per unit. There are 12,000 washers in inventory at a (LIFO) cost of $90 per washer. The factory produced 58,000 washers in the first three quarters of this year and Tweedie is considering ordering an additional 10,000, 15,000, or 20,000 washers in the fourth quarter. The plant's capacity can easily accommodate any of these volume levels without affecting fixed costs or variable cost per unit. The variable manufacturing cost of the washer is $75 and the plant has fixed annual costs of $1.3 million. Manufacturing overhead is allocated to dishwashers based on units. Tweedie's selling and administrative expenses consist of $15 of variable cost per washer and fixed cost of $2.92 million. The dishwasher division has a 17 percent weighted-average cost of capital and invested capital (not including inventories) of $18 million. Eaststar uses full absorption costing.

Required:

a. Prepare a table showing annual accounting earnings prepared under absorption costing for the Space Saver dishwasher for annual production levels of 68,000, 73,000, and 78,000 washers.

b. If Lynn Tweedie's bonus depends on reported accounting earnings from Space Saver dishwashers, what production quantity is she likely to select for the fourth quarter?

c. Prepare a table computing the valuation of the ending inventory (under LIFO) for annual production levels of 68,000, 73,000, and 78,000 washers.

d. If Lynn Tweedie's bonus depends on residual income from Space Saver dishwashers, what production quantity is she likely to select for the fourth quarter?

e. How would your answer change in part (d) if Tweedie's bonus was based on return on assets?

Eaststar manufactures and distributes a complete line of home appliances worldwide. Lynn Tweedie is the U.S. Space Saver Dishwasher product manager for Eaststar Appliances. Her responsibilities include pricing, planning, and sales of Eaststar's Space Saver dishwasher in the United States. It is the end of the third quarter and Tweedie is deciding how many Space Saver washers to produce in the fourth quarter. Given sales from the first three quarters and orders for the last quarter, she expects total sales for the year to be 73,000 washers at $200 per unit. There are 12,000 washers in inventory at a (LIFO) cost of $90 per washer. The factory produced 58,000 washers in the first three quarters of this year and Tweedie is considering ordering an additional 10,000, 15,000, or 20,000 washers in the fourth quarter. The plant's capacity can easily accommodate any of these volume levels without affecting fixed costs or variable cost per unit. The variable manufacturing cost of the washer is $75 and the plant has fixed annual costs of $1.3 million. Manufacturing overhead is allocated to dishwashers based on units. Tweedie's selling and administrative expenses consist of $15 of variable cost per washer and fixed cost of $2.92 million. The dishwasher division has a 17 percent weighted-average cost of capital and invested capital (not including inventories) of $18 million. Eaststar uses full absorption costing.

Required:

a. Prepare a table showing annual accounting earnings prepared under absorption costing for the Space Saver dishwasher for annual production levels of 68,000, 73,000, and 78,000 washers.

b. If Lynn Tweedie's bonus depends on reported accounting earnings from Space Saver dishwashers, what production quantity is she likely to select for the fourth quarter?

c. Prepare a table computing the valuation of the ending inventory (under LIFO) for annual production levels of 68,000, 73,000, and 78,000 washers.

d. If Lynn Tweedie's bonus depends on residual income from Space Saver dishwashers, what production quantity is she likely to select for the fourth quarter?

e. How would your answer change in part (d) if Tweedie's bonus was based on return on assets?

a. Annual earnings for various production levels is given in the following table:

1 5,000 units × $90/unit

2 $1,300,000 × (73,000/78,000)

3 73,000 × $15

b. Tweedie is likely to produce 20,000 washers in the fourth quarter or 78,000 for the year as this level maximizes reported profit.

c. The ending inventory values for various production levels are: d. Residual income for various production levels:

1 Net income - 15% × total invested capital

Based on the above data, Tweedie is likely to produce 78,000 washers, since this level maximizes her residual income.

e. ROA for various production levels: If Tweedie is rewarded based on ROA she is likely to produce 68,000 washers for the year.

1 5,000 units × $90/unit

2 $1,300,000 × (73,000/78,000)

3 73,000 × $15

b. Tweedie is likely to produce 20,000 washers in the fourth quarter or 78,000 for the year as this level maximizes reported profit.

c. The ending inventory values for various production levels are: d. Residual income for various production levels:

1 Net income - 15% × total invested capital

Based on the above data, Tweedie is likely to produce 78,000 washers, since this level maximizes her residual income.

e. ROA for various production levels: If Tweedie is rewarded based on ROA she is likely to produce 68,000 washers for the year.

4

One should always be wary of using unit costs for decision-making, because unit costs:

A)disguise the true nature of how costs vary with production

B)can be multiplied by a different number of units, suggesting that the cost data is scalable

C)generate misleading results when the company faces an increasing cost curve

D)ignore step-fixed costs

E)all of the above

A)disguise the true nature of how costs vary with production

B)can be multiplied by a different number of units, suggesting that the cost data is scalable

C)generate misleading results when the company faces an increasing cost curve

D)ignore step-fixed costs

E)all of the above

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

5

An Extreme Version of Variable Costing

Eli Goldratt advocates that all manufacturing costs other than materials be treated as operating expenses for the period. Periodic profits would be calculated as: Operating data for last year are There is no beginning inventory.

Required:

a. Compare profits under absorption costing and Goldratt's method.

b. Evaluate Goldratt's proposal.

Eli Goldratt advocates that all manufacturing costs other than materials be treated as operating expenses for the period. Periodic profits would be calculated as:

Operating data for last year are There is no beginning inventory.Required:

a. Compare profits under absorption costing and Goldratt's method.

b. Evaluate Goldratt's proposal.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

6

Variable Costing and Over/Under Producing

Cathy's Mats produces and sells artistic placemats for dining room tables. These placemats are manufactured out of recycled plastics. For last year and this year each mat has a variable manufacturing cost of $3, and fixed manufacturing overhead is $150,000 per year (both Last Year and This Year). Cathy's Mats incurs no other costs. The following table summarizes the selling price and the number of mats produced and sold Last Year and This Year: Cathy's Mats uses FIFO (First-in First Out) to value its ending inventory. Last Year Cathy's Mats had no beginning inventory.

Required:

a. Prepare income statements for Last Year and This Year using absorption costing.

b. Prepare income statements for Last Year and This Year using variable costing.

c. Write a short memo explaining why the net income amounts for Last Year and This Year are the same or different in parts (a) and (b).

d. Assume all the same facts (and data) as given in the problem, EXCEPT that This Year Cathy's Mats produced 60,000 mats rather than 50,000 mats. Compute net income for Last Year and This Year using (i) absorption costing and (ii) variable costing.

e. Write a short memo explaining why the net income amounts for Last Year and This Year are the same or different in (i) and (ii) of part (d).

Cathy's Mats produces and sells artistic placemats for dining room tables. These placemats are manufactured out of recycled plastics. For last year and this year each mat has a variable manufacturing cost of $3, and fixed manufacturing overhead is $150,000 per year (both Last Year and This Year). Cathy's Mats incurs no other costs. The following table summarizes the selling price and the number of mats produced and sold Last Year and This Year: Cathy's Mats uses FIFO (First-in First Out) to value its ending inventory. Last Year Cathy's Mats had no beginning inventory.

Required:

a. Prepare income statements for Last Year and This Year using absorption costing.

b. Prepare income statements for Last Year and This Year using variable costing.

c. Write a short memo explaining why the net income amounts for Last Year and This Year are the same or different in parts (a) and (b).

d. Assume all the same facts (and data) as given in the problem, EXCEPT that This Year Cathy's Mats produced 60,000 mats rather than 50,000 mats. Compute net income for Last Year and This Year using (i) absorption costing and (ii) variable costing.

e. Write a short memo explaining why the net income amounts for Last Year and This Year are the same or different in (i) and (ii) of part (d).

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

7

Chamiching makes hacksaw blades. Inventory values are determined using the first in, first out (FIFO) method. Production and sales data for the first three years appear below. In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?

A)Variable costing income (VCI) exceeds full costing income (FCI) every year

B)VCI exceeds FCI in Yrs 1 and 2 only

C)VCI exceeds FCI in Yrs 2 and 3 only

D)VCI never exceeds FCI

E)None of the above

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?A)Variable costing income (VCI) exceeds full costing income (FCI) every year

B)VCI exceeds FCI in Yrs 1 and 2 only

C)VCI exceeds FCI in Yrs 2 and 3 only

D)VCI never exceeds FCI

E)None of the above

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

8

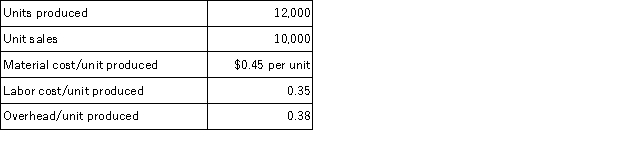

CC uses absorption (full) costing and its direct competitor, FF uses variable costing for internal decision making purposes. Last year, both companies reported the same production and sales volumes. Which is true?

A)If sales are 10,000 units and production 12,000 units, CC's net income exceeds FF's

B)If sales are 10,000 units and production 10,000 units, FF's net income exceeds CC's

C)If sales are 10,000 units and production 8,000 units, FF's net income exceeds CC's

D)If sales are 12,000 units and production 10,000 units, FF's net income equals CC's

E)Unable to determine

A)If sales are 10,000 units and production 12,000 units, CC's net income exceeds FF's

B)If sales are 10,000 units and production 10,000 units, FF's net income exceeds CC's

C)If sales are 10,000 units and production 8,000 units, FF's net income exceeds CC's

D)If sales are 12,000 units and production 10,000 units, FF's net income equals CC's

E)Unable to determine

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

9

How Volume Fluctuations Affect Earnings using Absorption Costing

BBF Corporation is a manufacturer of a synthetic chemical. Gary Voss, president of the company, has been eager to get the operating results for the just-completed fiscal year. He was surprised when the income statement revealed that income before taxes had dropped to $885,500 from $900,000, even though sales volume had increased by 100,000 kilograms. The drop in net income occurred even though Voss had implemented two changes during the past 12 months to improve the company's profitability:

1. In response to a 10 percent increase in production costs, the sales price of the company's product was increased by 12 percent. This action took place on December 1, 1994, the first day of the current fiscal year.

2. The managers of the selling and administrative departments were given strict instructions to spend no more in the current fiscal year than last year.

BBF's accounting department prepared and distributed to top management the comparative income statements presented below. BBG CORPORATION

Statements of Operating Income

For the Years Ended November 30

($000s)

The accounting staff also prepared related financial information to assist management in evaluating the company's performance. BBF uses the FIFO inventory method for finished goods. Budgeted and fixed overhead are equal and the beginning inventory last year has $3.00/kg. of fixed overhead.

Required:

a. Explain to Gary Voss why BBF Corporation's net income decreased in the current fiscal year despite the sales price and sales volume increases.

b. A member of BBF's accounting department has suggested that the company adopt variable (direct) costing for internal reporting purposes.

(i) Prepare an operating income statement through income before taxes for the current year ended November 30, using the variable (direct) costing method.

(ii) Present a numerical reconciliation of the difference in income before taxes using the absorption costing method as currently employed by BBF and the proposed variable costing method.

c. Identify and discuss the advantages and disadvantages of using variable costing for internal reporting purposes.

BBF Corporation is a manufacturer of a synthetic chemical. Gary Voss, president of the company, has been eager to get the operating results for the just-completed fiscal year. He was surprised when the income statement revealed that income before taxes had dropped to $885,500 from $900,000, even though sales volume had increased by 100,000 kilograms. The drop in net income occurred even though Voss had implemented two changes during the past 12 months to improve the company's profitability:

1. In response to a 10 percent increase in production costs, the sales price of the company's product was increased by 12 percent. This action took place on December 1, 1994, the first day of the current fiscal year.

2. The managers of the selling and administrative departments were given strict instructions to spend no more in the current fiscal year than last year.

BBF's accounting department prepared and distributed to top management the comparative income statements presented below. BBG CORPORATION

Statements of Operating Income

For the Years Ended November 30

($000s)

The accounting staff also prepared related financial information to assist management in evaluating the company's performance. BBF uses the FIFO inventory method for finished goods. Budgeted and fixed overhead are equal and the beginning inventory last year has $3.00/kg. of fixed overhead.

Required:

a. Explain to Gary Voss why BBF Corporation's net income decreased in the current fiscal year despite the sales price and sales volume increases.

b. A member of BBF's accounting department has suggested that the company adopt variable (direct) costing for internal reporting purposes.

(i) Prepare an operating income statement through income before taxes for the current year ended November 30, using the variable (direct) costing method.

(ii) Present a numerical reconciliation of the difference in income before taxes using the absorption costing method as currently employed by BBF and the proposed variable costing method.

c. Identify and discuss the advantages and disadvantages of using variable costing for internal reporting purposes.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

10

Variable and Absorption Costing

Valux manufactures a single product and sells it for $10 per unit. At the beginning of the year there were 1,000 units in inventory. Upon further investigation, you discover that units produced last year had $3.00 of fixed manufacturing cost and $2.00 of variable manufacturing cost. During the year Valux produced 10,000 units of product. Each unit produced generated $3.00 of variable manufacturing cost. Total fixed manufacturing cost for the current year was $40,000. There were no inventories at the end of the year.

Required:

a. Prepare two income statements for the current year, one on a variable cost basis and the other on an absorption cost basis.

b. Explain any difference between the two net income numbers and provide calculations supporting your explanation of the difference.

Valux manufactures a single product and sells it for $10 per unit. At the beginning of the year there were 1,000 units in inventory. Upon further investigation, you discover that units produced last year had $3.00 of fixed manufacturing cost and $2.00 of variable manufacturing cost. During the year Valux produced 10,000 units of product. Each unit produced generated $3.00 of variable manufacturing cost. Total fixed manufacturing cost for the current year was $40,000. There were no inventories at the end of the year.

Required:

a. Prepare two income statements for the current year, one on a variable cost basis and the other on an absorption cost basis.

b. Explain any difference between the two net income numbers and provide calculations supporting your explanation of the difference.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

11

Chamiching makes hacksaw blades. Inventory values are determined using the first in, first out (FIFO) method. Production and sales data for the first three years appear below. In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, if variable costing is used, which of the following is true?

A)Yr 3's gross profit is $171,687

B)Yr 1's gross profit is $48,000

C)Yr 2's gross profit is $123,200

D)Yr 2's gross profit is $129,513

E)None of the above

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, if variable costing is used, which of the following is true?A)Yr 3's gross profit is $171,687

B)Yr 1's gross profit is $48,000

C)Yr 2's gross profit is $123,200

D)Yr 2's gross profit is $129,513

E)None of the above

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

12

Chamiching makes hacksaw blades. Inventory values are determined using the first in, first out (FIFO) method. Production and sales data for the first three years appear below. In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, when variable costing income is reconciled to absorption costing income, which of the following is true?

A)In Yr 1, $12,000 is added to variable costing income to find absorption costing income

B)In Yr 3, $6,887 is added to variable costing income to find absorption costing income

C)In Yr 2, $5,113 is deducted from variable costing income to find absorption costing income

D)In Yr 2, $5,113 is added to variable costing income to find absorption costing income

E)None of the above

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, when variable costing income is reconciled to absorption costing income, which of the following is true?A)In Yr 1, $12,000 is added to variable costing income to find absorption costing income

B)In Yr 3, $6,887 is added to variable costing income to find absorption costing income

C)In Yr 2, $5,113 is deducted from variable costing income to find absorption costing income

D)In Yr 2, $5,113 is added to variable costing income to find absorption costing income

E)None of the above

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

13

Chamiching makes hacksaw blades. Inventory values are determined using the first in, first out (FIFO) method. Production and sales data for the first three years appear below. In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, if absorption costing is used, which of the following is true?

A)Yr 1's ending inventory is $12,000

B)Yr 2's gross profit is $112,400

C)Yr 3's cost of goods sold is $123,200

D)Yr 3's goods available for sale is $266,000

E)None of the above

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, if absorption costing is used, which of the following is true?A)Yr 1's ending inventory is $12,000

B)Yr 2's gross profit is $112,400

C)Yr 3's cost of goods sold is $123,200

D)Yr 3's goods available for sale is $266,000

E)None of the above

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

14

Chamiching makes hacksaw blades. Inventory values are determined using the first in, first out (FIFO) method. Production and sales data for the first three years appear below. In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?

A)The company should always choose absorption costing as it shows increasing profits every year

B)The company should always choose absorption costing because it facilitates income smoothing

C)Over the three years, Chamiching accumulates the same total income regardless of the choice of inventory costing method

D)b) and c) only

E)a, b and c

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?A)The company should always choose absorption costing as it shows increasing profits every year

B)The company should always choose absorption costing because it facilitates income smoothing

C)Over the three years, Chamiching accumulates the same total income regardless of the choice of inventory costing method

D)b) and c) only

E)a, b and c

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

15

Finlandia Frankfurters (FF), incorporated in Finland, uses variable costing for external reporting. On 1st January, it is purchased by Belgian Bagels, which uses absorption costing, and FF is obliged to adopt the parent company's accounting method for the purposes of filing consolidated accounts. At the time of the merger, FF had 4,000 units in inventory and production costs remained stable over the following year. Which is true about FF's income in the first post-merger year?

A)If sales are 10,000 units and production 12,000 units, variable costing income (VCI) exceeds full costing income (FCI)

B)If sales are 10,000 units and production 10,000 units, FCI exceeds VCI

C)If sales are 10,000 units and production 8,000 units, VCI exceeds FCI

D)If sales are 12,000 units and production 10,000 units, FCI exceeds VCI

E)Unable to determine

A)If sales are 10,000 units and production 12,000 units, variable costing income (VCI) exceeds full costing income (FCI)

B)If sales are 10,000 units and production 10,000 units, FCI exceeds VCI

C)If sales are 10,000 units and production 8,000 units, VCI exceeds FCI

D)If sales are 12,000 units and production 10,000 units, FCI exceeds VCI

E)Unable to determine

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

16

Variable Costing Can Still Create Incentives to Over Produce

Cope Products uses a flexible budget to set the overhead rate at the beginning of the year based on units produced. In year 1 budgeted fixed overhead is $1 million and budgeted variable overhead is $2 per unit. Direct material and direct labor together are $5 per unit. Blauvelt sells the completed product for $30. There is no beginning inventory. Budgeted volume is 80,000 units. Production and sales are 80,000 units. Actual overhead incurred in year 1 is $1,160,000. Any under- or over-absorbed overhead is written off to cost of goods sold.

In year 2, budgeted volume and production are again both 80,000 units. However, only 60,000 units are sold. Budgeted fixed overhead is $1 million and budgeted variable overhead is $2 per unit. Direct material and direct labor are $5 per unit. Final selling price remains at $30 per unit. Actual overhead incurred in year 2 is $1.35 million.

Required:

a. Calculate net income in year 1 first using absorption costing and then using variable costing. Explain any difference between the two net income numbers.

b. Calculate net income in year 2 using absorption costing, where the overhead rate used to assign overhead to products is based on actual overhead incurred.

c. Calculate net income in year 2 using variable costing, where any difference between budgeted overhead and actual overhead is treated as a fixed cost.

d. Calculate net income in year 2 using variable costing, where any difference between budgeted overhead and actual overhead is treated as a variable cost.

e. Explain why your answers in parts (b), (c), and (d) differ.

Cope Products uses a flexible budget to set the overhead rate at the beginning of the year based on units produced. In year 1 budgeted fixed overhead is $1 million and budgeted variable overhead is $2 per unit. Direct material and direct labor together are $5 per unit. Blauvelt sells the completed product for $30. There is no beginning inventory. Budgeted volume is 80,000 units. Production and sales are 80,000 units. Actual overhead incurred in year 1 is $1,160,000. Any under- or over-absorbed overhead is written off to cost of goods sold.

In year 2, budgeted volume and production are again both 80,000 units. However, only 60,000 units are sold. Budgeted fixed overhead is $1 million and budgeted variable overhead is $2 per unit. Direct material and direct labor are $5 per unit. Final selling price remains at $30 per unit. Actual overhead incurred in year 2 is $1.35 million.

Required:

a. Calculate net income in year 1 first using absorption costing and then using variable costing. Explain any difference between the two net income numbers.

b. Calculate net income in year 2 using absorption costing, where the overhead rate used to assign overhead to products is based on actual overhead incurred.

c. Calculate net income in year 2 using variable costing, where any difference between budgeted overhead and actual overhead is treated as a fixed cost.

d. Calculate net income in year 2 using variable costing, where any difference between budgeted overhead and actual overhead is treated as a variable cost.

e. Explain why your answers in parts (b), (c), and (d) differ.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

17

Average Costs and Variable Costs as Performance Measures

The manager of the manufacturing unit of a company is responsible for the costs of the manufacturing unit. The president is in the process of deciding whether to evaluate the manager of the manufacturing unit by the average cost per unit or the variable cost per unit. Quality and timely delivery would be used in conjunction with the cost measure to reward the manager.

Required:

a. What problems are associated with using the average cost per unit as a performance measure?

b. What problems are associated with using the variable cost per unit as a performance measure?

The manager of the manufacturing unit of a company is responsible for the costs of the manufacturing unit. The president is in the process of deciding whether to evaluate the manager of the manufacturing unit by the average cost per unit or the variable cost per unit. Quality and timely delivery would be used in conjunction with the cost measure to reward the manager.

Required:

a. What problems are associated with using the average cost per unit as a performance measure?

b. What problems are associated with using the variable cost per unit as a performance measure?

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

18

Chamiching makes hacksaw blades. Inventory values are determined using the first in, first out (FIFO) method. Production and sales data for the first three years appear below. In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?

A)The variable cost of Yr 2 ending inventory is $6,887

B)The full cost of Yr 2 ending inventory is double the variable cost ending inventory

C)There are 3,000 hacksaw blades in ending inventory

D)The fixed cost per unit in Yr 3 is $2.72

E)None of the above

In the first year, variable costs accounted for half of the full costs. Total fixed production costs increased each subsequent year by 20%, as a result of step-fixed costs and a general inflationary price increase. For Chamiching, which of the following is true?A)The variable cost of Yr 2 ending inventory is $6,887

B)The full cost of Yr 2 ending inventory is double the variable cost ending inventory

C)There are 3,000 hacksaw blades in ending inventory

D)The fixed cost per unit in Yr 3 is $2.72

E)None of the above

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

19

Incentives to Over Produce

An October 25, 1999, article in BusinessWeek by

D.Brady, "Why Xerox Is Struggling," reported:

President and Chief Executive

G.Richard Thoman is a big-picture guy.For the past two years, he has preached a digital revolution at the copier giant.Get down to the detail, though, and it's clear that the revolution isn't going as planned: In both copiers and printers, Xerox is losing ground.On October 18, the company announced lower than expected earnings and the stock price tumbled more than 13% on that day.Xerox stock is down 60% from its recent high of $60 in July.Xerox blamed the bad news on short-term surprises: sagging productivity in the sales force after a big reorganization as well as weakness in Brazil.But the sheer scope of bad news shocked even Thoman, who told investors in a conference call that he was "disappointed and sad about this quarter."

Thoman took the top job in April and vowed annual earnings growth in the "mid-to-high teens."

Beginning November 1, 1999, Xerox factories increased their hours from five eight-hour days a week to six ten-hour days a week through the end of the year.The factory managers were told to build inventories in expectation of higher sales in the fourth quarter of 1999.Fourth-quarter sales were expected to be higher because of anticipation that the new sales force reorganization would increase sales.Required:

Offer an alternative reason(s) for Xerox's decision to increase output in its factories.

An October 25, 1999, article in BusinessWeek by

D.Brady, "Why Xerox Is Struggling," reported:

President and Chief Executive

G.Richard Thoman is a big-picture guy.For the past two years, he has preached a digital revolution at the copier giant.Get down to the detail, though, and it's clear that the revolution isn't going as planned: In both copiers and printers, Xerox is losing ground.On October 18, the company announced lower than expected earnings and the stock price tumbled more than 13% on that day.Xerox stock is down 60% from its recent high of $60 in July.Xerox blamed the bad news on short-term surprises: sagging productivity in the sales force after a big reorganization as well as weakness in Brazil.But the sheer scope of bad news shocked even Thoman, who told investors in a conference call that he was "disappointed and sad about this quarter."

Thoman took the top job in April and vowed annual earnings growth in the "mid-to-high teens."

Beginning November 1, 1999, Xerox factories increased their hours from five eight-hour days a week to six ten-hour days a week through the end of the year.The factory managers were told to build inventories in expectation of higher sales in the fourth quarter of 1999.Fourth-quarter sales were expected to be higher because of anticipation that the new sales force reorganization would increase sales.Required:

Offer an alternative reason(s) for Xerox's decision to increase output in its factories.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 19 flashcards in this deck.