Deck 23: Single Period Binomial Heath Jarrow Morton Model

Full screen (f)

Question

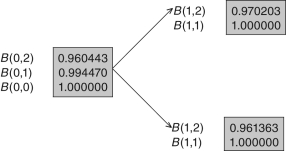

Use the following tree to answer the questions that follow.

What are the forward rates f(1,1)in the up and down nodes?

A) 0.0307,0.0402

B) 0.0102,0.0010

C) 0.0102,0.0102

D) 0.0056,0.0056

E) 0.0354,0.0056

What are the forward rates f(1,1)in the up and down nodes?

A) 0.0307,0.0402

B) 0.0102,0.0010

C) 0.0102,0.0102

D) 0.0056,0.0056

E) 0.0354,0.0056

Question

Question

Question

Use the following tree to answer the questions that follow.

What are the dollar returns on the one-period zero-coupon bond in the up and down nodes?

A) 1.0307,1.0402

B) 1.0102,1.0010

C) 1.0102,1.0102

D) 1.0056,1.0056

E) 1.0056,1.0402

What are the dollar returns on the one-period zero-coupon bond in the up and down nodes?

A) 1.0307,1.0402

B) 1.0102,1.0010

C) 1.0102,1.0102

D) 1.0056,1.0056

E) 1.0056,1.0402

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following tree to answer the questions that follow.

What are the forward rates f (0,1),f (0,0)?

A) 0.0307,0.0402

B) 0.0102,0.0010

C) 0.0102,0.0102

D) 0.0056,0.0056

E) 0.0354,0.0056

What are the forward rates f (0,1),f (0,0)?

A) 0.0307,0.0402

B) 0.0102,0.0010

C) 0.0102,0.0102

D) 0.0056,0.0056

E) 0.0354,0.0056

Question

Use the fact that the pseudo-probability of default at time zero is (1/ 2)to answer the questions that follow.

Use the fact that the pseudo-probability of default at time zero is (1/ 2)to answer the questions that follow.Consider a caplet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

A) 0.0307,0.0402

B) 0.0042,0.0000

C) 0.0354,0.0056

D) 0.0050,0.0050

E) 0.0000,0.0050

Question

Question

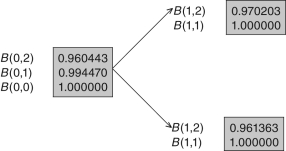

Use the following tree to answer the questions that follow.

What are the dollar returns on the two-period zero coupon-bond in the up and down nodes?

A) 1.0307,1.0402

B) 1.0102,1.0010

C) 1.0102,1.0102

D) 1.0056,1.0056

E) 1.0354,1.0056

What are the dollar returns on the two-period zero coupon-bond in the up and down nodes?

A) 1.0307,1.0402

B) 1.0102,1.0010

C) 1.0102,1.0102

D) 1.0056,1.0056

E) 1.0354,1.0056

Question

Question

Question

Use the fact that the pseudo-probability of default at time zero is (1/ 2)to answer the questions that follow.Consider a caplet with maturity time 1 and strike price 0.035.What is the time 0 value of the caplet?

A) 0.0025

B) 0.0000

C) 0.0042

D) 0.0050

E) 0.0021

Question

Use the fact that the pseudo-probability of default at time zero is (1/ 2)to answer the questions that follow.Consider a floorlet with maturity time 1 and strike price 0.035.What is the time 0 value of the floorlet?

A) 0.0025

B) 0.0000

C) 0.0042

D) 0.0050

E) 0.0021

Question

Use the fact that the pseudo-probability of default at time zero is (1/ 2)to answer the questions that follow.Consider a floorlet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

A) 0.0307,0.0402

B) 0.0042,0.0000

C) 0.0354,0.0056

D) 0.0050,0.0050

E) 0.0000,0.0050

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/23

Play

Full screen (f)

Deck 23: Single Period Binomial Heath Jarrow Morton Model

1

Use the following tree to answer the questions that follow.

What are the forward rates f(1,1)in the up and down nodes?

A) 0.0307,0.0402

B) 0.0102,0.0010

C) 0.0102,0.0102

D) 0.0056,0.0056

E) 0.0354,0.0056

What are the forward rates f(1,1)in the up and down nodes?

A) 0.0307,0.0402

B) 0.0102,0.0010

C) 0.0102,0.0102

D) 0.0056,0.0056

E) 0.0354,0.0056

A

2

Which of the following statements is correct?

A) The buyer of an interest rate floor earns an amount on each payment date that is equal to the floor rate (or the strike rate)on the contract times the notional.

B) The buyer of an interest rate floor earns an amount on each payment date that has a minimum value equal to the floor rate (or the strike rate)on the contract times the notional.

C) The buyer of an interest rate floor earns profits when interest rates increase,so it is contract that is bullish on interest rates.

D) If the buyer of an interest rate floor issues a floating rate bond that pays bbalibor,then its borrowing cost equals the floor rate (or the strike rate)times the notional.

E) If the buyer of an interest rate floor purchases a floating rate bond that earns bbalibor,then it earns at least the floor rate (or the strike rate)times the notional on each payment date.

A) The buyer of an interest rate floor earns an amount on each payment date that is equal to the floor rate (or the strike rate)on the contract times the notional.

B) The buyer of an interest rate floor earns an amount on each payment date that has a minimum value equal to the floor rate (or the strike rate)on the contract times the notional.

C) The buyer of an interest rate floor earns profits when interest rates increase,so it is contract that is bullish on interest rates.

D) If the buyer of an interest rate floor issues a floating rate bond that pays bbalibor,then its borrowing cost equals the floor rate (or the strike rate)times the notional.

E) If the buyer of an interest rate floor purchases a floating rate bond that earns bbalibor,then it earns at least the floor rate (or the strike rate)times the notional on each payment date.

E

3

Suppose that a company has issued a floating rate note paying (bbalibor).To create an interest rate collar that confines the payments between 3 percent and 7 percent,the company should trade the following interest rate derivatives:

A) buy a cap with a strike rate of 6.50 percent and sell a floor with a strike rate of 2.50 percent

B) buy a cap with a strike rate of 7.00 percent and sell a floor with a strike rate of 3.00 percent

C) buy a cap with a strike rate of 6.50 percent and sell a floor with a strike rate of 3.50 percent

D) sell a cap with a strike rate of 7.00 percent and buy a floor with a strike rate of 3.00 percent

E) sell a floor with a strike rate of 6.50 percent and buy a floor with a strike rate of 2.50 percent

A) buy a cap with a strike rate of 6.50 percent and sell a floor with a strike rate of 2.50 percent

B) buy a cap with a strike rate of 7.00 percent and sell a floor with a strike rate of 3.00 percent

C) buy a cap with a strike rate of 6.50 percent and sell a floor with a strike rate of 3.50 percent

D) sell a cap with a strike rate of 7.00 percent and buy a floor with a strike rate of 3.00 percent

E) sell a floor with a strike rate of 6.50 percent and buy a floor with a strike rate of 2.50 percent

B

4

Use the following tree to answer the questions that follow.

What are the dollar returns on the one-period zero-coupon bond in the up and down nodes?

A) 1.0307,1.0402

B) 1.0102,1.0010

C) 1.0102,1.0102

D) 1.0056,1.0056

E) 1.0056,1.0402

What are the dollar returns on the one-period zero-coupon bond in the up and down nodes?

A) 1.0307,1.0402

B) 1.0102,1.0010

C) 1.0102,1.0102

D) 1.0056,1.0056

E) 1.0056,1.0402

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

5

The writer of an interest rate floor contract:

A) has the obligation to buy the underlying bond at a fixed price

B) has the obligation to sell the underlying bond at a fixed price

C) has the obligation to pay (the strike rate minus the spot rate)times the notional

D) has the obligation to pay (the spot rate minus the strike rate)times the notional in case it's a positive number

E) has the obligation to pay (the strike rate minus the spot rate)times the notional in case it's a positive number

A) has the obligation to buy the underlying bond at a fixed price

B) has the obligation to sell the underlying bond at a fixed price

C) has the obligation to pay (the strike rate minus the spot rate)times the notional

D) has the obligation to pay (the spot rate minus the strike rate)times the notional in case it's a positive number

E) has the obligation to pay (the strike rate minus the spot rate)times the notional in case it's a positive number

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following statements is correct?

A) The buyer of an interest rate cap earns an amount on each payment date that is equal to the cap rate (or the strike rate)on the contract times the notional.

B) The buyer of an interest rate cap earns an amount on each payment date that is,at a minimum,the cap rate (or the strike rate)on the contract times the notional.

C) The buyer of an interest rate cap earns profits when interest rates decline,so it is contract that is bearish on interest rates.

D) If the buyer of an interest rate cap borrows using a floating rate bond that pays bbalibor,then its borrowing cost in any period is no larger than the cap rate (or the strike rate of the contract)times the notional.

E) If the buyer of an interest rate cap purchases a floating rate bond that earns bbalibor,then it earns the cap rate (or the strike rate)times the notional each payment date.

A) The buyer of an interest rate cap earns an amount on each payment date that is equal to the cap rate (or the strike rate)on the contract times the notional.

B) The buyer of an interest rate cap earns an amount on each payment date that is,at a minimum,the cap rate (or the strike rate)on the contract times the notional.

C) The buyer of an interest rate cap earns profits when interest rates decline,so it is contract that is bearish on interest rates.

D) If the buyer of an interest rate cap borrows using a floating rate bond that pays bbalibor,then its borrowing cost in any period is no larger than the cap rate (or the strike rate of the contract)times the notional.

E) If the buyer of an interest rate cap purchases a floating rate bond that earns bbalibor,then it earns the cap rate (or the strike rate)times the notional each payment date.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

7

The following is NOT an assumption underlying the binomial HJM option pricing model:

A) no market frictions

B) no credit risk

C) competitive and well-functioning markets

D) no interest rate uncertainty

E) the forward rates follow a lognormal process

A) no market frictions

B) no credit risk

C) competitive and well-functioning markets

D) no interest rate uncertainty

E) the forward rates follow a lognormal process

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following statements about the binomial interest rate option pricing model is INCORRECT?

A) The binomial model is popular because it is accessible and easy to understand.

B) The binomial model is a useful teaching tool.

C) The binomial model is a versatile model that can price a variety of derivatives.

D) The binomial model illustrates the main tenets of martingale pricing,the key technique that lies at the heart of derivative pricing.

E) The binomial model is more accurate than the Heath-Jarrow-Morton model because it makes a more realistic assumption about the bond price evolution than the HJM model.

A) The binomial model is popular because it is accessible and easy to understand.

B) The binomial model is a useful teaching tool.

C) The binomial model is a versatile model that can price a variety of derivatives.

D) The binomial model illustrates the main tenets of martingale pricing,the key technique that lies at the heart of derivative pricing.

E) The binomial model is more accurate than the Heath-Jarrow-Morton model because it makes a more realistic assumption about the bond price evolution than the HJM model.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

9

An interest rate cap is:

A) a European call option on the spot interest rate

B) an American call option on the spot interest rate

C) a portfolio of European call options on the spot interest rate

D) a portfolio of American call options on the spot interest rate

E) a portfolio of European put options on the spot interest rate

A) a European call option on the spot interest rate

B) an American call option on the spot interest rate

C) a portfolio of European call options on the spot interest rate

D) a portfolio of American call options on the spot interest rate

E) a portfolio of European put options on the spot interest rate

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

10

Assume zero-coupon bond prices are B(0,0)=$1,B(0,1)= $0.967846,B(0,2)=$0.943010.What is the spot rate of interest?

A) 0.0604

B) 0.0332

C) 0.0263

D) 0.0371

E) None of these answers are correct.

A) 0.0604

B) 0.0332

C) 0.0263

D) 0.0371

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following statements about an interest rate cap is correct?

A) For a company that has borrowed using a floating-rate loan,a long position in an interest rate cap prevents interest costs from going above a fixed level.

B) For a company that has purchased a floating-rate loan,a long position in an interest rate cap provides protection against the interest cost going above some fixed level.

C) An interest rate cap guarantees a forward rate that is binding at a future date.

D) An interest rate cap guarantees payments if spot prices move outside an interval,with caps at the top and bottom.

E) None of these answers are correct.

A) For a company that has borrowed using a floating-rate loan,a long position in an interest rate cap prevents interest costs from going above a fixed level.

B) For a company that has purchased a floating-rate loan,a long position in an interest rate cap provides protection against the interest cost going above some fixed level.

C) An interest rate cap guarantees a forward rate that is binding at a future date.

D) An interest rate cap guarantees payments if spot prices move outside an interval,with caps at the top and bottom.

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

12

The writer of an interest rate cap:

A) has the obligation to sell the underlying bond at a fixed price

B) has the obligation to buy the underlying bond at a fixed price

C) has the obligation to pay (the spot rate minus the strike rate)times the notional

D) has the obligation to pay (the spot rate minus the strike rate)times the notional in case it's a positive number

E) has the obligation to pay (the strike rate minus the spot rate)times the notional in case it's a positive number

A) has the obligation to sell the underlying bond at a fixed price

B) has the obligation to buy the underlying bond at a fixed price

C) has the obligation to pay (the spot rate minus the strike rate)times the notional

D) has the obligation to pay (the spot rate minus the strike rate)times the notional in case it's a positive number

E) has the obligation to pay (the strike rate minus the spot rate)times the notional in case it's a positive number

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

13

A necessary and sufficient condition to rule out arbitrage profits in the single-period HJM binomial tree is that the following must hold:

A) "up factor down factor dollar return" [U D (1 + R)] for all zero-coupon bonds

B) U (1 + R) D for all zero-coupon bonds

C) the pseudo-probabilities must be equal for all zero-coupon bond/money market account pairs

D) the pseudo-probabilities must be equal to 1/2

E) None of these answers are correct.

A) "up factor down factor dollar return" [U D (1 + R)] for all zero-coupon bonds

B) U (1 + R) D for all zero-coupon bonds

C) the pseudo-probabilities must be equal for all zero-coupon bond/money market account pairs

D) the pseudo-probabilities must be equal to 1/2

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

14

An interest rate floor is:

A) a European put option on the spot interest rate

B) an American put option on the spot interest rate

C) a portfolio of European put options on the spot interest rate

D) a portfolio of American put options on the spot interest rate

E) a portfolio of European call options on the spot interest rate

A) a European put option on the spot interest rate

B) an American put option on the spot interest rate

C) a portfolio of European put options on the spot interest rate

D) a portfolio of American put options on the spot interest rate

E) a portfolio of European call options on the spot interest rate

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

15

Use the following tree to answer the questions that follow.

What are the forward rates f (0,1),f (0,0)?

A) 0.0307,0.0402

B) 0.0102,0.0010

C) 0.0102,0.0102

D) 0.0056,0.0056

E) 0.0354,0.0056

What are the forward rates f (0,1),f (0,0)?

A) 0.0307,0.0402

B) 0.0102,0.0010

C) 0.0102,0.0102

D) 0.0056,0.0056

E) 0.0354,0.0056

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

16

Use the fact that the pseudo-probability of default at time zero is (1/ 2)to answer the questions that follow.Consider a caplet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

A) 0.0307,0.0402

B) 0.0042,0.0000

C) 0.0354,0.0056

D) 0.0050,0.0050

E) 0.0000,0.0050

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

17

Assume zero-coupon bond prices are B(0,0)= $1,B(0,1)= $0.967846,B(0,2)= $0.943010.What is the forward rate f (0,1)?

A) 0.0332

B) 0.0375

C) 0.0263

D) 0.0604

E) None of these answers are correct.

A) 0.0332

B) 0.0375

C) 0.0263

D) 0.0604

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

18

Use the following tree to answer the questions that follow.

What are the dollar returns on the two-period zero coupon-bond in the up and down nodes?

A) 1.0307,1.0402

B) 1.0102,1.0010

C) 1.0102,1.0102

D) 1.0056,1.0056

E) 1.0354,1.0056

What are the dollar returns on the two-period zero coupon-bond in the up and down nodes?

A) 1.0307,1.0402

B) 1.0102,1.0010

C) 1.0102,1.0102

D) 1.0056,1.0056

E) 1.0354,1.0056

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

19

Suppose that a portfolio manager has purchased a floating rate bond.To create a zero-cost collar,the manager should trade the following interest rate derivatives that have equal values:

A) sell a cap with a higher strike rate and buy a floor with a lower strike rate

B) buy a cap with a higher strike rate and sell a floor with a lower strike rate

C) sell a floor with a higher strike rate and buy a cap with a lower strike rate

D) buy a floor with a higher strike rate and sell a cap with a lower strike rate

E) None of these answers are correct.

A) sell a cap with a higher strike rate and buy a floor with a lower strike rate

B) buy a cap with a higher strike rate and sell a floor with a lower strike rate

C) sell a floor with a higher strike rate and buy a cap with a lower strike rate

D) buy a floor with a higher strike rate and sell a cap with a lower strike rate

E) None of these answers are correct.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following statements is INCORRECT?

A) Vasicek built one of the first generalized interest rate option pricing models.

B) Spot rate models for valuing interest rate options required the estimation of risk-premium.

C) Spot rate models for valuing interest rate options could not easily match the initial yield curve.

D) The Heath-Jarrow-Morton model is a continuous-time and multifactor model.

E) Black's model,a subcase of the Heath-Jarrow-Morton model,is widely used by traders.

A) Vasicek built one of the first generalized interest rate option pricing models.

B) Spot rate models for valuing interest rate options required the estimation of risk-premium.

C) Spot rate models for valuing interest rate options could not easily match the initial yield curve.

D) The Heath-Jarrow-Morton model is a continuous-time and multifactor model.

E) Black's model,a subcase of the Heath-Jarrow-Morton model,is widely used by traders.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

21

Use the fact that the pseudo-probability of default at time zero is (1/ 2)to answer the questions that follow.Consider a caplet with maturity time 1 and strike price 0.035.What is the time 0 value of the caplet?

A) 0.0025

B) 0.0000

C) 0.0042

D) 0.0050

E) 0.0021

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

22

Use the fact that the pseudo-probability of default at time zero is (1/ 2)to answer the questions that follow.Consider a floorlet with maturity time 1 and strike price 0.035.What is the time 0 value of the floorlet?

A) 0.0025

B) 0.0000

C) 0.0042

D) 0.0050

E) 0.0021

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

23

Use the fact that the pseudo-probability of default at time zero is (1/ 2)to answer the questions that follow.Consider a floorlet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

A) 0.0307,0.0402

B) 0.0042,0.0000

C) 0.0354,0.0056

D) 0.0050,0.0050

E) 0.0000,0.0050

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 23 flashcards in this deck.