Deck 8: Tools Used in Gathering Audit Evidence

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

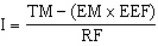

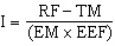

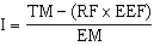

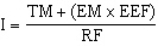

In MUS sampling,the formula for the sampling interval is

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/108

Play

Full screen (f)

Deck 8: Tools Used in Gathering Audit Evidence

1

Statistical sampling is used when an auditor chooses to examine all purchases of equipment exceeding $1,000.00 and to test the remaining items by analytical procedures.

False

2

Sample size varies directly with the expected failure rate.

True

3

The auditor must define the population to which sampling relates if the auditor is to use statistical sampling for substantive tests of account balances.

True

4

An attribute is defined as a characteristic of the population of interest to the auditor.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

5

For tests of control procedures the most commonly used statistical method is Attribute Sampling.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

6

The use of haphazard selection of a sample allows for random,statistical evaluation.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

7

The most efficient method of testing a large population is the use of nonstatistical sampling.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

8

When performing substantive tests using sampling methods,the auditor's main concern is the risk of incorrect rejection.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

9

The risk of incorrect acceptance of an account balance as correct,when in fact it is not correct,bears directly on the effectiveness of an audit.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

10

The tolerable misstatement is the confidence level needed to infer population values.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

11

Audit sampling is the application of an audit procedure to less than 100 percent of the items within an account balance or class of transactions for the purpose of evaluating some characteristic.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

12

Increasing the expected failure rate will cause the sample size to increase.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

13

The expected failure rate is the auditor's best estimate of the percentage of transactions processed for which the control procedure is not effectively applied.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

14

The tolerable failure rate is the minimum rate of control procedure failure that can occur sufficient to cause the auditor to re-assess the preliminary assessment of control risk to a higher level.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

15

The individual auditable elements defined by the auditor are the sampling units.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

16

The classical sampling methods include difference estimation,ratio estimation,and mean-per-unit sampling.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

17

The sample size decreases as the allowance for sampling error decreases.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

18

An auditor uses sampling to determine the reasonableness of an account balance by performing detailed analysis of items making up the account balance.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

19

Audit sampling implies the gathering of evidence to use as a basis for making valid inferences about the characteristics of the population as a whole without examining every transaction.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

20

Statistical sampling assists auditors in determining the sufficiency of evidence gathered.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

21

If the statistical confidence level is 90 percent,the test of details (TD)risk is 10 percent.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

22

Monetary unit sampling (MUS)is a widely used statistical sampling method because it results in an efficient sample size and concentrates on the dollar value of the account balances.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

23

In the formula where I = TM - (EM ´ EEF)/RF;I is the sampling interval in number of units.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

24

Population items with a zero balance have the same chance of being chosen as those with dollar balances when using MUS sampling.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

25

Classical methods of sampling are relatively easier to use than is MUS sampling.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

26

The design of MUS sampling requires the auditor to determine audit risk,tolerable misstatement,and the expected misstatement in the account balance.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

27

Nonstatistical samples should be based on the same audit considerations as those used for statistical sampling.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

28

Sampling risk is defined as the risk that an inference drawn from a sample will be incorrect.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

29

An example of sampling an attribute includes testing a purchase order for the proper signature.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

30

Attribute Sampling for testing controls should only be done by the auditor at the end of the fiscal period under audit.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

31

Analytical procedures are designed to provide dependent evidence about account balances-to replace the client's underlying estimation process.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

32

Random sampling can be used to determine sample size or evaluate sampling results even if the auditor does not plan on using statistical sampling.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

33

The design of MUS sampling requires the auditor to determine detection risk,tolerable misstatement,and the expected misstatement in the account balance.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

34

MUS sampling is designed to test whether there is an acceptable risk of account balance understatement.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

35

One of the most rigorous approaches to analytical procedures is regression analysis.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

36

Extracting data from the client's computer system is one of the tasks performed by GAS.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

37

Statistical sampling combines the theory of probability and statistical inference with audit judgment and experience.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

38

The auditor's tolerable failure rate for Attribute Sampling is the point in which control failures support the planned assessment of audit risk.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

39

Evaluating statistical sample results is one of the task performed by GAAS.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

40

In the formula where I = TM - (EM ´ EEF)/RF;I is the sampling interval in dollars.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

41

Using Attribute Sampling the auditor normally tests for multiple attributes using the same source documents.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

42

Incorrect acceptance is directly related to

A)the efficiency of the audit.

B)the ineffectiveness of the audit.

C)the cost of the audit.

D)all of the above.

A)the efficiency of the audit.

B)the ineffectiveness of the audit.

C)the cost of the audit.

D)all of the above.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

43

In Attribute Sampling if the achieved upper limit exceeds the tolerable rate the auditor can rely upon the control as working.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

44

Random number,systematic sampling and material value sampling are acceptable sample selection methods for statistical sampling.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

45

In Attribute Sampling if the selected item cannot be located,the auditor considers that control procedure as not working.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

46

Which one of the following is a decision the auditor needs to make about attribute sampling?

A)Management selection of sample size

B)Period covered by testing

C)Population size

D)Whether to use dollar unit or variables sampling

A)Management selection of sample size

B)Period covered by testing

C)Population size

D)Whether to use dollar unit or variables sampling

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

47

Nonsampling risk includes all of the following except

A)misinterpretation of information.

B)use of improper audit procedure.

C)improper projection of results to the population.

D)carelessness of the auditor.

E)all of the above.

A)misinterpretation of information.

B)use of improper audit procedure.

C)improper projection of results to the population.

D)carelessness of the auditor.

E)all of the above.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

48

Sampling risk is the risk that

A)the sample will not contain characteristics representative of the population such that inferences made about that population will be incorrect.

B)the population will not contain characteristics representative of the sample such that inferences made about that sample will be incorrect.

C)Neither A nor B is correct.

D)Both A and B are correct.

A)the sample will not contain characteristics representative of the population such that inferences made about that population will be incorrect.

B)the population will not contain characteristics representative of the sample such that inferences made about that sample will be incorrect.

C)Neither A nor B is correct.

D)Both A and B are correct.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

49

The auditor's risk of concluding that the book value of inventory is correct when it is materially misstated is the risk of

A)incorrect rejection.

B)incorrect acceptance.

C)insufficient sample size.

D)none of the above.

A)incorrect rejection.

B)incorrect acceptance.

C)insufficient sample size.

D)none of the above.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

50

In MUS sampling basic precision is the upper misstatement limit when no misstatements are detected in a MUS sample.It is computed by multiplying the sampling interval by the error expansion factor.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

51

Audit sampling is used to obtain evidence about each of the following except

A)the effectiveness of control procedures.

B)the efficiency of control procedures.

C)the dollar accuracy of account balances.

D)the dollar accuracy of classes of transactions.

A)the effectiveness of control procedures.

B)the efficiency of control procedures.

C)the dollar accuracy of account balances.

D)the dollar accuracy of classes of transactions.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

52

Random number and systematic sampling are acceptable sample selection methods for statistical sampling.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

53

The audit objective of Attribute Sampling is to test the correctness of an account balance.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

54

Control risk that is assessed excessively high leads to:

A)audit inefficiency.

B)a less expensive audit.

C)reduction of substantive testing.

D)errors that are more likely to occur than anticipated.

A)audit inefficiency.

B)a less expensive audit.

C)reduction of substantive testing.

D)errors that are more likely to occur than anticipated.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

55

In analysis of the results of audit sampling,an auditor may determine that the sample size must be increased.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

56

Which one of the following accounting constraints supports the concept of audit sampling?

A)Conservatism

B)Materiality

C)Cost-benefit

D)Industry practice

A)Conservatism

B)Materiality

C)Cost-benefit

D)Industry practice

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

57

Random number,haphazard selection and block sampling are acceptable sample selection methods for nonstatistical sampling.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

58

Which one of the following is not a decision the auditor needs to make about attribute sampling?

A)Sample size

B)Selection of items included in the sample

C)Evaluation of sample information

D)Whether to document all phases

A)Sample size

B)Selection of items included in the sample

C)Evaluation of sample information

D)Whether to document all phases

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

59

Stratification of the population into several homogeneous subpopulations generally creates audit efficiency.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

60

The auditor is most concerned with which of the following?

A)Risk of incorrect rejection

B)Risk of incorrect acceptance

C)Risk of excess sample size

D)Risk of errors in the population

A)Risk of incorrect rejection

B)Risk of incorrect acceptance

C)Risk of excess sample size

D)Risk of errors in the population

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

61

When using MUS sampling,an auditor found that the sampling interval should be $15,755.If selecting the sample manually,the auditor should round the sample interval to

A)$16,000.

B)$15,000.

C)$14,000.

D)$10,000.

A)$16,000.

B)$15,000.

C)$14,000.

D)$10,000.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

62

When planning a test of details using MUS sampling,tolerable misstatement is usually set

A)higher than planning materiality.

B)lower than planning materiality.

C)either higher or lower than planning materiality.

D)the same as materiality.

A)higher than planning materiality.

B)lower than planning materiality.

C)either higher or lower than planning materiality.

D)the same as materiality.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

63

Which one of the following issues need not be addressed when planning an audit sample to test control procedures?

A)Audit objective of the test

B)Minimum rate of control procedure failure

C)Expected rate of control procedure failure

D)Auditor's allowable risk of assessing control risk too low

A)Audit objective of the test

B)Minimum rate of control procedure failure

C)Expected rate of control procedure failure

D)Auditor's allowable risk of assessing control risk too low

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

64

Statistical sampling is best known for combining

A)binomial and confidence intervals.

B)random and haphazard selection.

C)hypergeometric distribution with audit risk.

D)probability and statistical inference with audit judgment.

A)binomial and confidence intervals.

B)random and haphazard selection.

C)hypergeometric distribution with audit risk.

D)probability and statistical inference with audit judgment.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

65

Which one of the following is not a typical step used to implement an attribute estimation sampling plan?

A)Define the attributes of interest and what constitutes failure(s)

B)Select and audit the sample items

C)Evaluate the sample results

D)Define the nonstatistical sampling method that is most effective and efficient

A)Define the attributes of interest and what constitutes failure(s)

B)Select and audit the sample items

C)Evaluate the sample results

D)Define the nonstatistical sampling method that is most effective and efficient

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

66

When confirming receivables in testing for overstatements,there are few or no misstatements expected,and the selection is based on dollars,the auditor is likely to use

A)MUS sampling.

B)stratified mean-per-unit sampling.

C)ratio estimation sampling.

D)attribute sampling.

A)MUS sampling.

B)stratified mean-per-unit sampling.

C)ratio estimation sampling.

D)attribute sampling.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

67

Factors that the auditor should consider when choosing between nonstatistical and statistical sampling include

A)whether the audit staff is adequately trained to use statistical sampling.

B)whether the population lends itself to a random-based selection method.

C)whether the auditor wants an objective measure of the risk of drawing a wrong conclusion.

D)all of the above.

A)whether the audit staff is adequately trained to use statistical sampling.

B)whether the population lends itself to a random-based selection method.

C)whether the auditor wants an objective measure of the risk of drawing a wrong conclusion.

D)all of the above.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

68

Nonstatistical sampling may be utilized for Tests of Controls Substantive Testing

A)Yes Yes

B)Yes No

C)No No

D)No Yes

A)Yes Yes

B)Yes No

C)No No

D)No Yes

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

69

The statistical sampling method most commonly used to test control procedures is

A)variable sampling.

B)ratio estimation sampling.

C)attribute estimation sampling.

D)dollar unit sampling.

A)variable sampling.

B)ratio estimation sampling.

C)attribute estimation sampling.

D)dollar unit sampling.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

70

When determining the sample size,the auditor must realize that for most purposes:

A)sampling risk is high.

B)tolerable failure rate is predetermined.

C)a failure rate is not to be expected.

D)population size is not a major factor.

A)sampling risk is high.

B)tolerable failure rate is predetermined.

C)a failure rate is not to be expected.

D)population size is not a major factor.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

71

The design of a MUS sample requires the auditor to determine all of the following except

A)detection risk.

B)inherent risk.

C)tolerable misstatement.

D)expected misstatement in the account balance.

A)detection risk.

B)inherent risk.

C)tolerable misstatement.

D)expected misstatement in the account balance.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

72

The probability proportional to size sampling is designed to test for

A)overstatements.

B)understatements.

C)neither understatements nor overstatements.

D)either understatements or overstatements.

A)overstatements.

B)understatements.

C)neither understatements nor overstatements.

D)either understatements or overstatements.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

73

The sample size varies directly with

A)the expected failure rate.

B)the tolerable error rate.

C)the allowable risk of assessing control risk too low.

D)the nonsampling risk.

A)the expected failure rate.

B)the tolerable error rate.

C)the allowable risk of assessing control risk too low.

D)the nonsampling risk.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

74

Probability proportional to size sampling is designed to test for overstatement of an account balance while classical variable methods are designed to test for

A)both overstatement and understatement.

B)understatement only.

C)overstatement only.

D)exact dollar balances.

A)both overstatement and understatement.

B)understatement only.

C)overstatement only.

D)exact dollar balances.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

75

The steps used in sampling during substantive testing includes the determination of each of the following except

A)the audit objective.

B)the method of selecting a sample.

C)expected misstatement conditions.

D)control failure risk.

A)the audit objective.

B)the method of selecting a sample.

C)expected misstatement conditions.

D)control failure risk.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

76

While auditors may use either statistical or nonstatistical sampling,some auditors restrict the use of nonstatistical sampling mainly because it is

A)less effective.

B)less objective.

C)less efficient.

D)less risky.

A)less effective.

B)less objective.

C)less efficient.

D)less risky.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

77

In MUS sampling,the formula for the sampling interval is

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

78

In analyzing misstatements using sampling techniques,the auditor should analyze the misstatements

A)qualitatively and quantitatively.

B)absolutely and proportionately.

C)haphazardly and randomly.

D)methodically and systematically.

A)qualitatively and quantitatively.

B)absolutely and proportionately.

C)haphazardly and randomly.

D)methodically and systematically.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

79

Haphazard sampling is an acceptable method of sampling provided the auditor believes the sample to be

A)statistically sound.

B)representative of the population.

C)representative of the sample.

D)in the upper stratum.

A)statistically sound.

B)representative of the population.

C)representative of the sample.

D)in the upper stratum.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

80

The maximum rate of control procedure failure that can occur and still support the preliminary assessment of control risk is

A)tolerable failure rate.

B)allowable risk of assessing control risk too low.

C)expected failure rate.

D)allowance for sampling error.

A)tolerable failure rate.

B)allowable risk of assessing control risk too low.

C)expected failure rate.

D)allowance for sampling error.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 108 flashcards in this deck.