Deck 16: Accounting for Mineral Resources

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

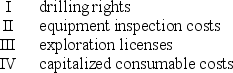

Which of the following E&E costs would be classified as intangibles?

A) I, II and III

B) II, III and IV

C) I, II and IV

D) I, III and IV

A) I, II and III

B) II, III and IV

C) I, II and IV

D) I, III and IV

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/26

Play

Full screen (f)

Deck 16: Accounting for Mineral Resources

1

IFRS 6 is an example of:

A) an industry specific standard

B) a not-for-profit standard

C) a standard applicable to disclosing entities

D) a differential reporting standard based on size based criteria

A) an industry specific standard

B) a not-for-profit standard

C) a standard applicable to disclosing entities

D) a differential reporting standard based on size based criteria

A

2

Which of the following are included in IFRS 6 as factors indicating the E&E assets may be impaired?

I whether the exploration rights for the specific area have expired or are expected to expire in the near future and there is no expectation of renewal

II where there is no budget or plan for the incurrence of further substantial E&E expenditure in the specific area

III where the entity had decided to discontinue E&E activities in the specific area on the basis that such activities have not led to the discovery of commercially viable quantities of mineral resources

IV where the entity has established that the cost of the E&E asset is unlikely to be recovered in full from the successful development or sale of the specific area

A) I, II and III

B) I, II and IV

C) I, III and IV

D) II, III and IV

I whether the exploration rights for the specific area have expired or are expected to expire in the near future and there is no expectation of renewal

II where there is no budget or plan for the incurrence of further substantial E&E expenditure in the specific area

III where the entity had decided to discontinue E&E activities in the specific area on the basis that such activities have not led to the discovery of commercially viable quantities of mineral resources

IV where the entity has established that the cost of the E&E asset is unlikely to be recovered in full from the successful development or sale of the specific area

A) I, II and III

B) I, II and IV

C) I, III and IV

D) II, III and IV

A

3

Which of the following methods is the least applied method to account for exploration and evaluation costs?

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

C

4

The majority of an entity's obligations for removal and restorations costs are incurred during which phase of a project?

A) exploration phase

B) technical feasibility phase

C) development phase

D) evaluation phase

A) exploration phase

B) technical feasibility phase

C) development phase

D) evaluation phase

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following is NOT included as part of the initial cost of exploration and evaluation assets?

A) exploratory drilling

B) miming acquisition rights

C) trenching

D) pre-exploration survey fees

A) exploratory drilling

B) miming acquisition rights

C) trenching

D) pre-exploration survey fees

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

6

Most large oil and gas companies use which of the following methods to account for exploration and evaluation costs?

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

7

Which costs are within the scope of IFRS 6?

A) Pre-exploration and evaluation phase expenditure

B) Exploration and evaluation phase expenditure

C) Development phase expenditure

D) All of the above

A) Pre-exploration and evaluation phase expenditure

B) Exploration and evaluation phase expenditure

C) Development phase expenditure

D) All of the above

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

8

The scope of IFRS 6 is limited to:

A) Exploration and evaluation expenditures

B) Pre-exploration, exploration and evaluation expenditures

C) Exploration, evaluation and development expenditures

D) Pre-exploration, exploration, evaluation and development expenditures

A) Exploration and evaluation expenditures

B) Pre-exploration, exploration and evaluation expenditures

C) Exploration, evaluation and development expenditures

D) Pre-exploration, exploration, evaluation and development expenditures

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following statements is correct?

A) The IASB extractive industries project currently underway excludes disclosure requirements from its scope

B) IFRS 6 was issued by the IASB as an interim measure pending the completion of a comprehensive project dealing with accounting for the extractive industries

C) The IASB extractive industries project currently underway proposed the removal of the 'unit of account' concept in accounting for E&E assets

D) IFRS 6 was issued by the IASB as a result of their recent comprehensive extractive industries project

A) The IASB extractive industries project currently underway excludes disclosure requirements from its scope

B) IFRS 6 was issued by the IASB as an interim measure pending the completion of a comprehensive project dealing with accounting for the extractive industries

C) The IASB extractive industries project currently underway proposed the removal of the 'unit of account' concept in accounting for E&E assets

D) IFRS 6 was issued by the IASB as a result of their recent comprehensive extractive industries project

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

10

IFRS 6 requires disclosure of which of the following?

A) accounting policies relating to pre-exploration costs

B) financing cash flows relating to E&E activities

C) impairment write-downs made on E&E assets

D) accounting policies relating to E&E assets

A) accounting policies relating to pre-exploration costs

B) financing cash flows relating to E&E activities

C) impairment write-downs made on E&E assets

D) accounting policies relating to E&E assets

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following methods tends to be restricted to small mining companies in South Africa?

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following methods involves capitalizing exploration and evaluation costs using a larger cost centre than an area of interest such as a country of region?

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following methods is inconsistent with historical cost accounting?

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

14

In the context of IFRS 6, E&E stands for:

A) evaluation and extraction

B) exploration and evaluation

C) extraction and exploration

D) exploration and expenditure

A) evaluation and extraction

B) exploration and evaluation

C) extraction and exploration

D) exploration and expenditure

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following statements in relation to assessing E&E assets for impairment is correct?

A) The level at which and E&E asset is tested for impairment may consist of one or more cash-generating units

B) IFRS 6 allows the cash-generating unit or group of cash-generating units to which an E&E asset is allocated to be larger than a segment determined in accordance with IFRS 8.

C) IFRS 6 allows E&E assets to be tested for impairment at the individual asset level

D) IFRS 6 does not allow the reversal of impairment write-downs made against E&E assets

A) The level at which and E&E asset is tested for impairment may consist of one or more cash-generating units

B) IFRS 6 allows the cash-generating unit or group of cash-generating units to which an E&E asset is allocated to be larger than a segment determined in accordance with IFRS 8.

C) IFRS 6 allows E&E assets to be tested for impairment at the individual asset level

D) IFRS 6 does not allow the reversal of impairment write-downs made against E&E assets

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

16

The obligation to record a provision for removal and restoration costs arising from mining exploration and evaluation arises through the application of:

A) IFRS 6

B) IAS 37

C) The Framework

D) IFRIC 1

A) IFRS 6

B) IAS 37

C) The Framework

D) IFRIC 1

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following methods best reflects the traditional concept of an asset?

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

18

IFRS 6 Exploration for and Evaluation of Mineral Resources was issued by the IASB in:

A) 2000

B) 2004

C) 2006

D) 2007

A) 2000

B) 2004

C) 2006

D) 2007

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

19

Mineral resources are specifically excluded from the scope of which of the following standards?

I IAS 2 Inventories

II IAS 16 Property, plant & equipment

III IAS 18 Revenue

IV IAS 38 Intangible assets

A) I and III only

B) II and IV only

C) II, III and IV only

D) I, II, III and IV

I IAS 2 Inventories

II IAS 16 Property, plant & equipment

III IAS 18 Revenue

IV IAS 38 Intangible assets

A) I and III only

B) II and IV only

C) II, III and IV only

D) I, II, III and IV

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

20

The IFRS Interpretations Committee issued an interpretation in relation to the accounting for surface mine stripping costs (i.e., removal of rocks, soil and other waste materials to access the relevant mineral deposits) incurred during the production phase. The interpretation proposes:

A) Waste removal (stripping) costs would be capitalised during the production phase of a surface mine, if certain criteria are met

B) This asset would be referred to as a stripping activity asset ('the asset')

C) The asset would initially be recognised at cost plus directly attributable overhead costs.

D) All of the options are correct

A) Waste removal (stripping) costs would be capitalised during the production phase of a surface mine, if certain criteria are met

B) This asset would be referred to as a stripping activity asset ('the asset')

C) The asset would initially be recognised at cost plus directly attributable overhead costs.

D) All of the options are correct

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following is NOT within the scope of the IASB extractive activities project?

A) the definition of reserves and resources

B) whether to expense or capitalize costs recognised after recognition of reserves and resources as assets

C) measurement of reserves and resources on initial recognition as an asset

D) disclosure requirements for reserves and resources

A) the definition of reserves and resources

B) whether to expense or capitalize costs recognised after recognition of reserves and resources as assets

C) measurement of reserves and resources on initial recognition as an asset

D) disclosure requirements for reserves and resources

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following statements in relation to the use of the revaluation model to subsequently account for E&E assets is correct?

A) The revaluation model can only be used to account for tangible E&E assets.

B) The revaluation model can be used for intangible E&E assets where the fair value can be reliably measured.

C) The revaluation model can be used for tangible E&E assets only where there is an active market for the assets.

D) The revaluation model can be used for tangible E&E assets where the fair value can be reliably measured.

A) The revaluation model can only be used to account for tangible E&E assets.

B) The revaluation model can be used for intangible E&E assets where the fair value can be reliably measured.

C) The revaluation model can be used for tangible E&E assets only where there is an active market for the assets.

D) The revaluation model can be used for tangible E&E assets where the fair value can be reliably measured.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following methods best reflects the volatility inherent in E&E activities?

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

A) the area of interest method

B) the successful efforts method

C) the appropriation method

D) the full cost method

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following E&E costs would be classified as intangibles?

A) I, II and III

B) II, III and IV

C) I, II and IV

D) I, III and IV

A) I, II and III

B) II, III and IV

C) I, II and IV

D) I, III and IV

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

25

E&E assets are required to be tested for impairment:

A) when there is an indication that the assets may be impaired

B) at least annually

C) only where commercially feasible reserves are not found through the E&E activities

D) prior to reclassification at the end of E&E activities

A) when there is an indication that the assets may be impaired

B) at least annually

C) only where commercially feasible reserves are not found through the E&E activities

D) prior to reclassification at the end of E&E activities

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

26

Subsequent to initial recognition E&E assets are required to be measured:

A) under the cost model

B) under the revaluation model

C) either under the cost model or revaluation model

D) at the lower of the cost and fair value

A) under the cost model

B) under the revaluation model

C) either under the cost model or revaluation model

D) at the lower of the cost and fair value

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 26 flashcards in this deck.