Deck 19: Consolidation: Wholly Owned Subsidiaries

Full screen (f)

Question

Question

Question

Question

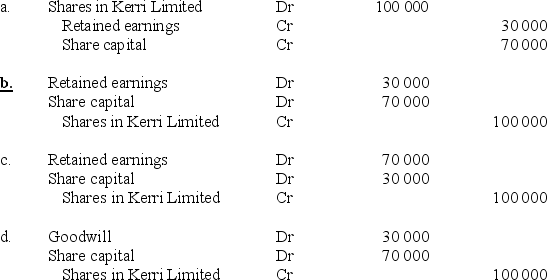

On 1 July 2014,Peter Limited acquired all the issued shares of Kerri Limited for $100 000 when the equity of Kerri Limited consisted of:

Share capital $70 000

Retained earnings 30 000

The pre-acquisition entry at 1 July 2014 is:

Share capital $70 000

Retained earnings 30 000

The pre-acquisition entry at 1 July 2014 is:

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/47

Play

Full screen (f)

Deck 19: Consolidation: Wholly Owned Subsidiaries

1

Water Limited acquired Boy Limited for a purchase consideration of $110 000.At acquisition date the fair value of the Boy Limited's Land asset was $80 000 and the carrying amount was $60 000.If the company tax rate is 30%,which of the following is the appropriate adjustment to recognise the tax effect of the business combination revaluation of land?

A)DR Deferred tax liability $6 000

B)CR Deferred tax liability $6 000

C)DR Deferred tax asset $6 000

D)CR Deferred tax asset $6 000

A)DR Deferred tax liability $6 000

B)CR Deferred tax liability $6 000

C)DR Deferred tax asset $6 000

D)CR Deferred tax asset $6 000

B

2

If a revaluation of the subsidiary's assets is performed on consolidation,the subsidiary's assets are carried into the consolidated statement of financial position at:

A)net present value.

B)current replacement cost.

C)historical cost.

D)fair value.

A)net present value.

B)current replacement cost.

C)historical cost.

D)fair value.

D

3

Sippy Ltd acquired 100% of the share capital of Downs Ltd when the carrying value of Downs Ltd's plant and machinery was $100 000.The fair value of the plant on acquisition date was $150 000.The company tax rate was 30%.What is the amount of the business combination valuation reserve that must be recognised on consolidation?

A)$15 000

B)$35 000

C)$50 000

D)$150 000

A)$15 000

B)$35 000

C)$50 000

D)$150 000

B

4

On 1 July 2014,Peter Limited acquired all the issued shares of Kerri Limited for $100 000 when the equity of Kerri Limited consisted of:

Share capital $70 000

Retained earnings 30 000

The pre-acquisition entry at 1 July 2014 is:

Share capital $70 000

Retained earnings 30 000

The pre-acquisition entry at 1 July 2014 is:

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

5

Easts Limited acquired 100% of the shares in Tigers Limited on a cum div.basis for $200 000.At acquisition date,the subsidiary had a declared dividend of $10 000.The pre-acquisition entry must include the following line:

A)DR Shares in subsidiary $190 000

B)CR Shares in subsidiary $200 000

C)CR Shares in subsidiary $190 000

D)CR Shares in subsidiary $10 000

A)DR Shares in subsidiary $190 000

B)CR Shares in subsidiary $200 000

C)CR Shares in subsidiary $190 000

D)CR Shares in subsidiary $10 000

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

6

Unity Limited acquired 100% of the share capital of Bellvista Limited.Bellvista had issued share capital of $200 000.The book values of Bellvista Limited's assets were: buildings $100 000,machinery $120 000.The fair values of these assets were: buildings $180 000,machinery $140 000.The tax rate is 30%.The fair value of the identifiable net assets is:

A)$270 000.

B)$220 000.

C)$320 000.

D)$200 000.

A)$270 000.

B)$220 000.

C)$320 000.

D)$200 000.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

7

The pre-acquisition entry is necessary to:

A)avoid overstating the equity and net assets of the parent.

B)record the 'Shares in subsidiary' account in the parents records.

C)avoid overstating the equity and net assets of the group.

D)avoid understating the equity and net assets of the group.

A)avoid overstating the equity and net assets of the parent.

B)record the 'Shares in subsidiary' account in the parents records.

C)avoid overstating the equity and net assets of the group.

D)avoid understating the equity and net assets of the group.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

8

The effect of the pre-acquisition entry is to eliminate the 'Shares in subsidiary' asset and the:

A)equity of the subsidiary at the acquisition date.

B)equity of the parent at the acquisition date.

C)net assets of the subsidiary at the acquisition date.

D)net assets of the parent at the acquisition date.

A)equity of the subsidiary at the acquisition date.

B)equity of the parent at the acquisition date.

C)net assets of the subsidiary at the acquisition date.

D)net assets of the parent at the acquisition date.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following statements is incorrect?

A)The business combination valuation reserve is an account recorded in the subsidiary's records.

B)The acquisition analysis may include the recognition of assets and liabilities not recognised in the subsidiary's records.

C)The acquisition analysis will determine whether any goodwill or gain on bargain purchase has arisen as a part of the business combination.

D)An acquisition analysis is prepared at acquisition date to identify the identifiable assets and liabilities of the subsidiary at fair value.

A)The business combination valuation reserve is an account recorded in the subsidiary's records.

B)The acquisition analysis may include the recognition of assets and liabilities not recognised in the subsidiary's records.

C)The acquisition analysis will determine whether any goodwill or gain on bargain purchase has arisen as a part of the business combination.

D)An acquisition analysis is prepared at acquisition date to identify the identifiable assets and liabilities of the subsidiary at fair value.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

10

The preparation of consolidated financial statements involves:

A)adding together the financial statements of the investor and the associate.

B)adjusting entries in the accounting records of the subsidiary.

C)adding together the financial statements of the parent and the subsidiaries.

D)adjusting entries in the accounting records of the parent.

A)adding together the financial statements of the investor and the associate.

B)adjusting entries in the accounting records of the subsidiary.

C)adding together the financial statements of the parent and the subsidiaries.

D)adjusting entries in the accounting records of the parent.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

11

On 1 July 2014 Good Ltd acquired a 100% interest in Life Ltd.At that time Life Ltd had goodwill of $10 000 recorded in its statement of financial position as a result of a previous business combination.The total goodwill arising on Good's acquisition of Life was $24 000.The goodwill to be recognised on consolidation as a result of Good's acquisition of Life is:

A)nil.

B)$10 000.

C)$14 000.

D)$24 000.

A)nil.

B)$10 000.

C)$14 000.

D)$24 000.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

12

If the consideration transferred is greater than the acquired interest in the net fair value of the identifiable assets,liabilities and contingent liabilities of the acquiree:

A)a gain on bargain purchase results.

B)goodwill has been purchased and must be recognised on consolidation.

C)the difference is treated as a special equity reserve in the acquirer's accounting records.

D)the difference is immediately charged to profit or loss in the period in which the business combination occurred.

A)a gain on bargain purchase results.

B)goodwill has been purchased and must be recognised on consolidation.

C)the difference is treated as a special equity reserve in the acquirer's accounting records.

D)the difference is immediately charged to profit or loss in the period in which the business combination occurred.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

13

If a subsidiary's reporting date does not coincide with the parent entity's reporting date,adjustments must be made for the effects of significant transactions that occur between the two reporting dates provided the reporting dates differ by no more than:

A)nine months.

B)three months.

C)one month.

D)six months.

A)nine months.

B)three months.

C)one month.

D)six months.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

14

There is no recognition of a deferred tax item in respect to goodwill because it is a residual amount and the recognition of a deferred tax item would:

A)decrease the carrying amount of goodwill.

B)increase the carrying amount of goodwill.

C)decrease the profit on consolidation.

D)increase the profit on consolidation.

A)decrease the carrying amount of goodwill.

B)increase the carrying amount of goodwill.

C)decrease the profit on consolidation.

D)increase the profit on consolidation.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

15

Kerri Limited has two subsidiary entities,Emily Limited and Georgia Limited.Kerri Limited owns 100% of the shares in both entities.Details of the issued share capital are:

- Kerri Limited $200 000

- Emily Limited $60 000

- Georgia Limited $30 000

The consolidated share capital amount of the Kerri Emily Georgia group is:

A)$230 000.

B)$90 000.

C)$200 000.

D)$290 000.

- Kerri Limited $200 000

- Emily Limited $60 000

- Georgia Limited $30 000

The consolidated share capital amount of the Kerri Emily Georgia group is:

A)$230 000.

B)$90 000.

C)$200 000.

D)$290 000.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

16

Where the consideration transferred is less than the fair value of the identifiable net assets and contingent liabilities acquired,the item must be recognised in the consolidation worksheet as:

A)a transfer to the business combination valuation reserve.

B)goodwill.

C)an increase in the 'Shares in subsidiary' asset.

D)a gain on bargain purchase.

A)a transfer to the business combination valuation reserve.

B)goodwill.

C)an increase in the 'Shares in subsidiary' asset.

D)a gain on bargain purchase.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

17

When Wayne Ltd acquired 100% of the share capital of Carol Ltd,the carrying amount of Carol Ltd's machinery was $200 000.The fair value of the machinery on acquisition date was $160 000.The company tax rate was 30%.What is the amount of the business combination valuation reserve that will be recognised on consolidation?

A)$40 000

B)$12 000

C)$28 000

D)$160 000

A)$40 000

B)$12 000

C)$28 000

D)$160 000

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following statements is incorrect?

A)Where consolidated financial statements are prepared over a number of years,consolidation entries need to be made every time a consolidation worksheet is prepared.

B)Consolidation adjusting entries affect the ledger accounts of the parent and subsidiaries.

C)A consolidation worksheet is used to help the process of adding together the financial statements of the parent and its subsidiaries.

D)There are no consolidated ledger accounts.

A)Where consolidated financial statements are prepared over a number of years,consolidation entries need to be made every time a consolidation worksheet is prepared.

B)Consolidation adjusting entries affect the ledger accounts of the parent and subsidiaries.

C)A consolidation worksheet is used to help the process of adding together the financial statements of the parent and its subsidiaries.

D)There are no consolidated ledger accounts.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

19

Susan Limited has two subsidiary entities,Rachel Limited and Rebecca Limited.Susan Limited owns 100% of the shares in both entities.Details of the cash accounts of each company are: Susan Limited $200 000,Lemon Limited $60 000,Juice Limited $30 000.The balance of the consolidated cash account of the Susan Limited group is:

A)$290 000.

B)$200 000.

C)$260 000.

D)$230 000.

A)$290 000.

B)$200 000.

C)$260 000.

D)$230 000.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

20

Hungry Limited acquired 100% of the share capital of Jane Limited for a purchase consideration of $320 000.At acquisition date,the net fair value of Jane Ltd's assets,liabilities and contingent liabilities was $250 000 including goodwill with a carrying amount of $20 000.The company tax rate is 30%.The unrecorded amount of goodwill that must be recognised on the consolidation worksheet is:

A)$50 000.

B)$70 000.

C)$90 000.

D)$15 000.

A)$50 000.

B)$70 000.

C)$90 000.

D)$15 000.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

21

Business combination valuation adjustment entries record only the parent's share of fair value adjustments relating to a subsidiary's assets,liabilities and contingent liabilities.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

22

Where an investment in a subsidiary is acquired on an ex.div basis,the fair value of the consideration paid should exclude the amount of the dividend.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following assets cannot be revalued above their cost in the accounting records of the subsidiary?

A)Inventory

B)Plant and equipment

C)Goodwill

D)Both a and c

A)Inventory

B)Plant and equipment

C)Goodwill

D)Both a and c

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

24

The acquisition analysis may result in the recognition of assets and liabilities that are not recognised in the subsidiary's accounting records.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

25

In preparing the consolidated financial statements,no adjustments are made in the accounting records of the individual entities that comprise the group.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

26

When preparing the business combination valuation entries,there is no recognition of a deferred tax liability for goodwill.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

27

According to AASB 3 Business Combinations,the key principle relating to the disclosure of information about business combinations is to disclose information that:

A)enables financial statement users to evaluate the nature and financial effect of business combinations that occurred during the reporting period.

B)enables the preparation of the consolidated financial statements in the most cost-effective manner.

C)does not give an advantage to the competitors of a consolidated group.

D)provides financial statement users with information about the parent entity only.

A)enables financial statement users to evaluate the nature and financial effect of business combinations that occurred during the reporting period.

B)enables the preparation of the consolidated financial statements in the most cost-effective manner.

C)does not give an advantage to the competitors of a consolidated group.

D)provides financial statement users with information about the parent entity only.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

28

One year after acquisition date,the goodwill acquired was regarded as having become impaired by $40 000.The appropriate consolidation adjustment in relation to the impairment will include the following line:

A)DR Goodwill $40 000

B)CR Impairment expense $40 000

C)CR Business combination valuation reserve $40 000

D)CR Accumulated impairment losses $40 000

A)DR Goodwill $40 000

B)CR Impairment expense $40 000

C)CR Business combination valuation reserve $40 000

D)CR Accumulated impairment losses $40 000

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

29

In relation to pre-acquisition of a subsidiary entity,which of the following events can cause a change in the pre-acquisition entry subsequent to acquisition date?

I Transfers to post-acquisition retained earnings.

II Depreciation on non-current assets.

III Transfers from pre-acquisition retained earnings.

IV Bonus dividends paid from pre-acquisition equity.

A)I,II,III and IV

B)I,III and IV only

C)II and III only

D)III and IV only

I Transfers to post-acquisition retained earnings.

II Depreciation on non-current assets.

III Transfers from pre-acquisition retained earnings.

IV Bonus dividends paid from pre-acquisition equity.

A)I,II,III and IV

B)I,III and IV only

C)II and III only

D)III and IV only

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

30

An acquisition analysis is prepared at acquisition date to identify the fair values of the identifiable assets and liabilities of the parent.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

31

On 1 January 2012,Cowboys Ltd acquired all the issued shares in Tate Ltd.At that date,the inventory of Tate Ltd had a fair value of $10 000 more than its carrying amount.By 30 June 2013,75% of the inventory was sold to an entity outside of the group.The business combination valuation consolidation adjustment against inventory in relation to the transaction as at 30 June 2013 will be:

A)a debit of $7500.

B)a credit of $5000.

C)a debit of $5000.

D)a debit of $2500.

A)a debit of $7500.

B)a credit of $5000.

C)a debit of $5000.

D)a debit of $2500.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

32

In the case of a reverse acquisition,the subsidiary effectively becomes the acquirer and:

A)its assets and liabilities are measured at cost.

B)the parent's assets and liabilities are measured at fair value.

C)its assets and liabilities are measured at fair value.

D)none of the above.

A)its assets and liabilities are measured at cost.

B)the parent's assets and liabilities are measured at fair value.

C)its assets and liabilities are measured at fair value.

D)none of the above.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

33

The main purpose of the pre-acquisition entry is to ensure no double counting of group net assets and equity.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

34

Where at acquisition date the parent holds shares in the subsidiary that it has previously acquired,this investment must be revalued to fair value at acquisition date.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

35

A post acquisition transfer between retained earnings and a general reserve will result in a corresponding change to the pre-acquisition entry.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

36

Where the carrying amount of a non-current asset is more than its fair value at the date of acquisition,the difference is reflected in the deferred tax liability in the business combination valuation entries.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

37

If the fair value of a depreciable asset is greater than the carrying amount,in the years subsequent to the acquisition date the depreciation expense recorded in the books of the subsidiary will be greater than that for the group.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following statements is correct?

A)AASB 3 Business Combinations requires that any revaluations of a subsidiary's assets at acquisition date must be done in the consolidation worksheet.

B)The revaluation of non-current assets in the subsidiary's records means that the subsidiary has adopted the cost model of accounting for those assets.

C)Revaluations of assets such as goodwill and inventory are not permitted in the accounting records of the subsidiary.

D)Inventory can be revalued to an amount greater than its cost in the records of the subsidiary.

A)AASB 3 Business Combinations requires that any revaluations of a subsidiary's assets at acquisition date must be done in the consolidation worksheet.

B)The revaluation of non-current assets in the subsidiary's records means that the subsidiary has adopted the cost model of accounting for those assets.

C)Revaluations of assets such as goodwill and inventory are not permitted in the accounting records of the subsidiary.

D)Inventory can be revalued to an amount greater than its cost in the records of the subsidiary.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

39

Consolidated financial statements must be prepared using uniform accounting policies for like transactions and other events in similar circumstances.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

40

Where a subsidiary has goodwill already recorded in their books at the date of acquisition,such goodwill should be eliminated in full and then recognised on consolidation.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

41

When inventory that has been subject to a fair value adjustment is sold,the effect on the business combination valuation adjustment in the year of sale includes a debit to cost of sales.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

42

AASB 12 Disclosure of Interests in Other Entities establishes the disclosures relating to a parent's interests in subsidiaries

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

43

The effect of a transfer of pre-acquisition retained earnings to a general reserve on the pre-acquisition entry is to reduce the debit adjustment against retained earnings.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

44

The 'Transfer from business combination valuation reserve' is an appropriation item that is closed to retained earnings at the end of each year.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

45

According to AASB 127 Separate Financial Statements,all dividends paid or payable by the subsidiary to a parent are recognised as revenue in the profit or loss of the parent.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

46

AASB 3Business Combinations prohibits the revaluation of the assets of the subsidiary at acquisition date in the records of the subsidiary.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

47

A reverse acquisition occurs when the legal subsidiary in a business combination obtains control over the legal parent.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 47 flashcards in this deck.