Deck 9: Property, Plant and Equipment

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

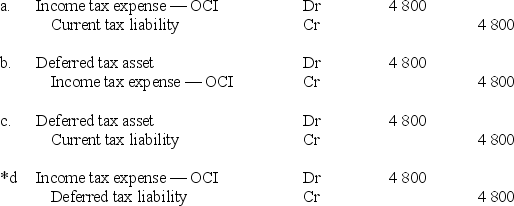

On 30 June 2014,Walters Limited had an item of plant with an original cost of $140 000 and accumulated depreciation of $56 000.At this date,the fair value of the plant was $100 000 and Walters Limited revalued the plant.Assuming a tax rate of 30%,the tax effect of the revaluation would be recorded as which of the following?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

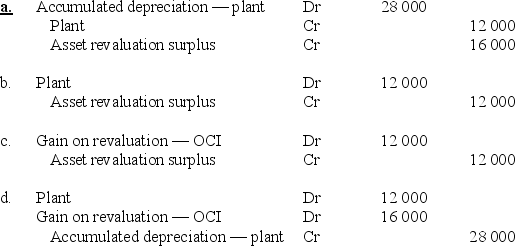

On 30 June 2014,Walters Limited had an item of plant with an original cost of $140 000 and accumulated depreciation of $56 000.At this date,the fair value of the plant was $100 000.The net effect of the journal entries necessary to record the revaluation of the plant by Walters to fair value on 30 June 2014 in accordance with AASB 116 Property,Plant and Equipment is which of the following?

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/47

Play

Full screen (f)

Deck 9: Property, Plant and Equipment

1

After an asset has been initially recognised,an entity has a choice between the cost model and the:

A)liquidation value model.

B)accrual model.

C)revaluation model.

D)realisable value model.

A)liquidation value model.

B)accrual model.

C)revaluation model.

D)realisable value model.

C

2

The cost of an asset less its residual value is referred to as its:

A)book value.

B)residual amount.

C)depreciable amount.

D)carrying amount.

A)book value.

B)residual amount.

C)depreciable amount.

D)carrying amount.

C

3

Property,plant and equipment includes items that are:

A)intangible.

B)held for resale.

C)held for investment.

D)used in an entity's production process.

A)intangible.

B)held for resale.

C)held for investment.

D)used in an entity's production process.

D

4

Hunt Limited applied the straight-line method of depreciation to its non-current assets.The cost of the buildings was $850 000,the residual value is $150 000 and the useful life is 10 years.The annual depreciation expense is:

A)$100 000.

B)$15 000.

C)$85 000.

D)$70 000.

A)$100 000.

B)$15 000.

C)$85 000.

D)$70 000.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

5

According to AASB 116 Property,Plant and Equipment,the cost of property,plant and equipment is only recognised as an asset if it is probable that the future economic benefits will flow to the entity and if:

A)the cost can be reliably measured.

B)it is a physical asset.

C)the asset has been received by the purchaser.

D)the asset is held for rental.

A)the cost can be reliably measured.

B)it is a physical asset.

C)the asset has been received by the purchaser.

D)the asset is held for rental.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

6

On 1 July 2009,Barba Limited acquired an item of equipment for $105 000 which it depreciated using the straight line basis.The equipment had an estimated useful life of 10 years and its residual value was $15 000.The carrying amount of the equipment in the financial statements dated 30 June 2014 is:

A)$60 000.

B)$45 000.

C)$52 500.

D)$0.

A)$60 000.

B)$45 000.

C)$52 500.

D)$0.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

7

Under the cost model,after initial recognition an item of property,plant and equipment must be carried at its:

A)estimated liquidation value.

B)cost less accumulated depreciation and less accumulated impairment losses.

C)initial cost.

D)current replacement cost.

A)estimated liquidation value.

B)cost less accumulated depreciation and less accumulated impairment losses.

C)initial cost.

D)current replacement cost.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

8

For the purpose of the initial recognition of an item of property,plant and equipment,the date on which the fair values should be measured is referred to as the:

A)acquisition date.

B)recognition date.

C)measurement date.

D)fair value date.

A)acquisition date.

B)recognition date.

C)measurement date.

D)fair value date.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

9

Webcke Limited acquired an item of machinery with an expected useful life of 4 years.The expected total production output over this period was: year 1,30 000 units; year 2,25 000 units; year 3,15 000 units; year 4,10 000 units.The machinery cost $85 000 and the residual value is $15 000.The amount of depreciation expense recorded in the first year is:

A)$26 250.

B)$31 875.

C)$21 875.

D)$17 500.

A)$26 250.

B)$31 875.

C)$21 875.

D)$17 500.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

10

Under AASB 116 Property,Plant and Equipment,the purpose of calculating the depreciation charge for a period on an item of property,plant and equipment is to measure:

A)the fall in the fair value of the asset across the period.

B)a change in the re-sale value of the asset that has occurred over the period.

C)a reduction in the estimated market value of the asset across the period.

D)the consumption of economic benefits over the period.

A)the fall in the fair value of the asset across the period.

B)a change in the re-sale value of the asset that has occurred over the period.

C)a reduction in the estimated market value of the asset across the period.

D)the consumption of economic benefits over the period.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

11

For the purposes of recognising an item of property,plant and equipment,the acquisition date is defined in AASB 3 Business Combination as the date:

A)on which the acquirer obtains control of the acquiree.

B)the contract to exchange the assets is signed.

C)on which the offer to acquire the asset becomes unconditional.

D)the consideration is paid.

A)on which the acquirer obtains control of the acquiree.

B)the contract to exchange the assets is signed.

C)on which the offer to acquire the asset becomes unconditional.

D)the consideration is paid.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following depreciation methods is most appropriate when the asset's benefits are expected to be received evenly over its useful life?

A)Consistent benefit method

B)Straight-line method

C)Diminishing balance method

D)Unit-of-production method

A)Consistent benefit method

B)Straight-line method

C)Diminishing balance method

D)Unit-of-production method

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

13

When changing from the revaluation to the cost model of measurement for non-current assets,the model must be applied:

A)in the current and future accounting periods.

B)only to assets acquired after date of changing to the cost model.

C)retrospectively.

D)prospectively.

A)in the current and future accounting periods.

B)only to assets acquired after date of changing to the cost model.

C)retrospectively.

D)prospectively.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following are not examples of directly attributable costs that should be included in the cost of acquisition for property,plant and equipment?

A)Costs of site preparation

B)Installation and assembly costs

C)Initial delivery and handling costs

D)Costs of opening a new facility

A)Costs of site preparation

B)Installation and assembly costs

C)Initial delivery and handling costs

D)Costs of opening a new facility

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

15

A non-current property,plant and equipment asset is depreciated using the straight-line method over a 10 year useful life.The asset was revalued upwards after four years of use.There is no change in the remaining useful life of six years or to the residual value.Which of the following relationships reflects the effect of the revaluation on the future depreciation of the asset?

Depreciation Annual depreciation

Rate expense

A)Same Higher

B)Same Same

C)Higher Higher

D)Higher Same

Depreciation Annual depreciation

Rate expense

A)Same Higher

B)Same Same

C)Higher Higher

D)Higher Same

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is not an example of a separate class of property,plant and equipment?

A)Office equipment

B)Land and buildings

C)Inventory

D)Motor vehicles

A)Office equipment

B)Land and buildings

C)Inventory

D)Motor vehicles

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

17

Estimated future restoration costs associated with mining land are:

A)expensed in the period in which they are incurred.

B)recorded directly into equity.

C)regarded as contingent liability and are disclosed in the notes to the financial statements.

D)capitalised into the cost of the land.

A)expensed in the period in which they are incurred.

B)recorded directly into equity.

C)regarded as contingent liability and are disclosed in the notes to the financial statements.

D)capitalised into the cost of the land.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

18

The depreciation expense calculated using the diminishing balance method reflects:

A)an increasing pattern of benefits over the asset's useful life.

B)a decreasing pattern of benefits over the asset's useful life.

C)a constant pattern of benefits over the asset's useful life.

D)a fluctuating pattern of benefits over the asset's useful life.

A)an increasing pattern of benefits over the asset's useful life.

B)a decreasing pattern of benefits over the asset's useful life.

C)a constant pattern of benefits over the asset's useful life.

D)a fluctuating pattern of benefits over the asset's useful life.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

19

Property,plant and equipment are assets that:

A)are expected to be used up within the current financial period.

B)are held for resale within the current period.

C)are tangible in nature.

D)have a remaining productive life of less than one financial year.

A)are expected to be used up within the current financial period.

B)are held for resale within the current period.

C)are tangible in nature.

D)have a remaining productive life of less than one financial year.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

20

An entity acquired an item of plant in exchange for an item of equipment.The equipment has a carrying amount of $15 000 and a fair value of $20 000.The journal entry to record the acquisition of the plant will show:

A)a loss on acquisition of $5000.

B)a gain on sale of $5000.

C)proceeds on sale of equipment of $15 000.

D)proceeds on sale of plant of $15 000.

A)a loss on acquisition of $5000.

B)a gain on sale of $5000.

C)proceeds on sale of equipment of $15 000.

D)proceeds on sale of plant of $15 000.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

21

Where an entity acquires a bundle of assets and the total cost of the assets is greater than the sum of the fair values of the assets acquired,a bargain purchase has been made.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

22

Depreciation is not recognised if an asset's residual value exceeds its carrying amount.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

23

When using the revaluation model:

A)ongoing record keeping costs are generally lower than if the cost model were used.

B)the values reported for property,plant and equipment will provide more relevant information to users of the financial statements.

C)depreciation expenses will generally be lower than under the cost model.

D)the entity's financial statements will be consistent with US GAAP requirements.

A)ongoing record keeping costs are generally lower than if the cost model were used.

B)the values reported for property,plant and equipment will provide more relevant information to users of the financial statements.

C)depreciation expenses will generally be lower than under the cost model.

D)the entity's financial statements will be consistent with US GAAP requirements.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

24

Costs of training staff in the use of a new asset are capitalised into the initial cost of the asset under AASB 116 Property,Plant and Equipment.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

25

Expenditure designed to improve the quality of the output of an asset are capitalised into the cost of the asset in accordance with paragraph 7 of AASB 116 Property,Plant and Equipment.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

26

On 30 June 2014,Walters Limited had an item of plant with an original cost of $140 000 and accumulated depreciation of $56 000.At this date,the fair value of the plant was $100 000 and Walters Limited revalued the plant.Assuming a tax rate of 30%,the tax effect of the revaluation would be recorded as which of the following?

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

27

Depreciation is an accounting process which involves a systematic allocation of the depreciable amount of an asset over its useful life.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

28

The residual value of a non-current asset is the amount or consideration actually received by an entity at the date of the asset's disposal.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

29

Costs of testing whether an asset is functioning property should be capitalised into the initial cost of the asset under AASB 116 Property,Plant and Equipment.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

30

Costs of removal or dismantling an asset at the end of its useful life are measured on a present value basis and capitalised into the initial cost of the asset.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

31

Under AASB 116 Property,Plant and Equipment,the revaluation model is applied to:

A)all assets on an individual basis.

B)individual current assets only.

C)individual property,plant and equipment assets only.

D)property,plant and equipment assets on a class-by-class basis.

A)all assets on an individual basis.

B)individual current assets only.

C)individual property,plant and equipment assets only.

D)property,plant and equipment assets on a class-by-class basis.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

32

The units-of-production method of recognising depreciation is only suitable for use by entities involved in manufacturing.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

33

Once an entity has selected a depreciation method to use to depreciate an asset,it must use that same method for the entire useful life of the asset.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

34

Copely Limited had an existing asset revaluation surplus in respect to an item of plant that had been derecognised.An appropriate journal entry to transfer the surplus to retained earnings would include which of the following?

A)DR Gain on revaluation - OCI

B)CR Asset revaluation surplus

C)DR Retained earnings

D)CR Retained earnings

A)DR Gain on revaluation - OCI

B)CR Asset revaluation surplus

C)DR Retained earnings

D)CR Retained earnings

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following statements is not correct in relation to the disclosure of property,plant and equipment balances?

A)Paragraph 79 of AASB 116 contains information that entities are encouraged to disclose,but not required to do so.

B)An entity must disclose the useful life estimates for each class of assets.

C)A summary of movements in the revaluation surplus must be disclosed.

D)Information on assets carried at revalued amounts must be disclosed on an individual asset basis.

A)Paragraph 79 of AASB 116 contains information that entities are encouraged to disclose,but not required to do so.

B)An entity must disclose the useful life estimates for each class of assets.

C)A summary of movements in the revaluation surplus must be disclosed.

D)Information on assets carried at revalued amounts must be disclosed on an individual asset basis.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

36

When an item of property,plant and equipment is sold,the resulting gain or loss is calculated as the difference between the:

A)net proceeds from sale and the asset's original cost.

B)asset's estimated fair value and its carrying amount at the date of sale.

C)asset's original cost and its accumulated depreciation at the date of sale.

D)net proceeds from sale and the asset's carrying amount at the date of sale.

A)net proceeds from sale and the asset's original cost.

B)asset's estimated fair value and its carrying amount at the date of sale.

C)asset's original cost and its accumulated depreciation at the date of sale.

D)net proceeds from sale and the asset's carrying amount at the date of sale.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

37

On initial recognition of property,plant and equipment,the cost only comprises the purchase price plus an initial estimate of dismantling and/or restoration costs.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

38

Fair value is defined in AASB 116 Property,Plant and Equipment as the amount for which an asset can be exchanged between knowledgeable willing parties in an arm's length transaction.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

39

On 30 June 2014,Walters Limited had an item of plant with an original cost of $140 000 and accumulated depreciation of $56 000.At this date,the fair value of the plant was $100 000.The net effect of the journal entries necessary to record the revaluation of the plant by Walters to fair value on 30 June 2014 in accordance with AASB 116 Property,Plant and Equipment is which of the following?

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

40

Under AASB 116 Property,Plant and Equipment,subsequent to initial recognition property,plant and equipment assets can only be measured using the revaluation model.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

41

One of the reasons for selecting the cost model over the revaluation model is because of the increased relevance of such measures.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

42

Items of property,plant and equipment may only be derecognised if they are sold.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

43

Disclosures under AASB 116 Property,Plant and Equipment are required on an asset-by-asset basis where the revaluation model has been used.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

44

The revaluation model must be applied to classes of assets.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

45

A revaluation increment reversing a previous revaluation decrement must be credited to the profit or loss.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

46

When a property,plant and equipment asset is derecognised through sale,any associated asset revaluation surplus must always be transferred to retained earnings.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

47

The expected physical wear and tear on an asset should be taken into account when determining the useful life of the asset.

Unlock Deck

Unlock for access to all 47 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 47 flashcards in this deck.