Deck 5: Portfolio Management

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

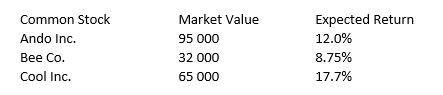

What is the expected return of the three stock portfolio described below? Common Stock Market Value Expected Return

A) 18.45%

B) 12.82%

C) 13.38%

D) 15.27%

E) 16.67%

A) 18.45%

B) 12.82%

C) 13.38%

D) 15.27%

E) 16.67%

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/15

Play

Full screen (f)

Deck 5: Portfolio Management

1

The slope of the utility curves for a strongly risk-averse investor, relative to the slope of the utility curves for a less risk-averse investor, will

A) be steeper.

B) be flatter.

C) be vertical.

D) be horizontal.

E) none of the above.

A) be steeper.

B) be flatter.

C) be vertical.

D) be horizontal.

E) none of the above.

A

2

A portfolio is considered to be efficient if

A) no other portfolio offers higher expected returns with the same risk.

B) no other portfolio offers lower risk with the same expected return.

C) there is no portfolio with a higher return.

D) choices a and b

E) all of the above

A) no other portfolio offers higher expected returns with the same risk.

B) no other portfolio offers lower risk with the same expected return.

C) there is no portfolio with a higher return.

D) choices a and b

E) all of the above

D

3

You are given a two asset portfolio with a fixed correlation coefficient. If the weights of the two assets are varied the expected portfolio return would be ____ and the expected portfolio standard deviation would be ____.

A) nonlinear, elliptical

B) nonlinear, circular

C) linear, elliptical

D) linear, circular

E) circular, elliptical

A) nonlinear, elliptical

B) nonlinear, circular

C) linear, elliptical

D) linear, circular

E) circular, elliptical

C

4

When assessing the risk impact of adding a new security to a portfolio, it is necessary to consider the

A) new security's variance

B) variance of every security in the portfolio

C) weight of every security in the portfolio

D) average covariance of the new security with every security in the portfolio

E) all of the above

A) new security's variance

B) variance of every security in the portfolio

C) weight of every security in the portfolio

D) average covariance of the new security with every security in the portfolio

E) all of the above

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

5

If equal risk is added moving along the envelope curve containing the best possible combinations the return will

A) decrease at an increasing rate.

B) decrease at a decreasing rate.

C) increase at an increasing rate.

D) increase at a decreasing rate.

E) remain constant.

A) decrease at an increasing rate.

B) decrease at a decreasing rate.

C) increase at an increasing rate.

D) increase at a decreasing rate.

E) remain constant.

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

6

All of the following are assumptions of the Markowitz model except

A) risk is measured based on the variability of returns.

B) investors maximise one-period expected utility.

C) investors' utility curves demonstrate properties of diminishing marginal utility of wealth.

D) investors base decisions solely on expected return and time.

E) all of the above

A) risk is measured based on the variability of returns.

B) investors maximise one-period expected utility.

C) investors' utility curves demonstrate properties of diminishing marginal utility of wealth.

D) investors base decisions solely on expected return and time.

E) all of the above

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following statements about the correlation coefficient is false?

A) The values range between −1 to +1.

B) A value of +1 implies that the returns for the two stocks move together in a completely linear manner.

C) A value of −1 implies that the returns move in a completely opposite direction.

D) A value of zero means that the returns are independent.

E) None of the above (that is, all statements are true)

A) The values range between −1 to +1.

B) A value of +1 implies that the returns for the two stocks move together in a completely linear manner.

C) A value of −1 implies that the returns move in a completely opposite direction.

D) A value of zero means that the returns are independent.

E) None of the above (that is, all statements are true)

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

8

A positive covariance between two variables indicates that

A) the two variables move in different directions.

B) the two variables move in the same direction.

C) the two variables are low risk.

D) the two variables are high risk.

E) the two variables are risk free.

A) the two variables move in different directions.

B) the two variables move in the same direction.

C) the two variables are low risk.

D) the two variables are high risk.

E) the two variables are risk free.

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

9

When individuals evaluate their portfolios they should evaluate

A) all domestic and foreign stocks.

B) all marketable securities.

C) all marketable securities and other liquid assets.

D) all assets.

E) all assets and liabilities.

A) all domestic and foreign stocks.

B) all marketable securities.

C) all marketable securities and other liquid assets.

D) all assets.

E) all assets and liabilities.

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

10

The purpose of calculating the covariance between two stocks is to provide a(n) ____ measure of their movement together.

A) absolute

B) relative

C) indexed

D) loglinear

E) squared

A) absolute

B) relative

C) indexed

D) loglinear

E) squared

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

11

All of the following are common risk measurements except

A) standard deviation.

B) variance.

C) semivariance.

D) covariance.

E) range of returns.

A) standard deviation.

B) variance.

C) semivariance.

D) covariance.

E) range of returns.

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

12

An individual investor's utility curves specify the tradeoffs he or she is willing to make between

A) high risk and low risk assets.

B) high return and low return assets.

C) covariance and correlation.

D) return and risk.

E) efficient portfolios.

A) high risk and low risk assets.

B) high return and low return assets.

C) covariance and correlation.

D) return and risk.

E) efficient portfolios.

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

13

As the correlation coefficient between two assets decreases, the shape of the efficient frontier

A) approaches a horizontal straight line.

B) bends out.

C) bends in.

D) approaches a vertical straight line.

E) none of the above.

A) approaches a horizontal straight line.

B) bends out.

C) bends in.

D) approaches a vertical straight line.

E) none of the above.

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

14

Semivariance, when applied to portfolio theory, is concerned with

A) The square root of deviations from the mean.

B) All deviations below the mean.

C) All deviations above the mean.

D) All deviations.

E) The summation of the squared deviations from the mean.

A) The square root of deviations from the mean.

B) All deviations below the mean.

C) All deviations above the mean.

D) All deviations.

E) The summation of the squared deviations from the mean.

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

15

What is the expected return of the three stock portfolio described below? Common Stock Market Value Expected Return

A) 18.45%

B) 12.82%

C) 13.38%

D) 15.27%

E) 16.67%

A) 18.45%

B) 12.82%

C) 13.38%

D) 15.27%

E) 16.67%

Unlock Deck

Unlock for access to all 15 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 15 flashcards in this deck.