Deck 13: Inventories

Full screen (f)

Question

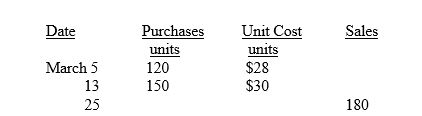

Hunter Coy sells calculators. At the beginning of March, 100 Z1200 scientific calculators were on hand for which the firm had paid $25 each. Purchases and sales for the month were as follows.

If Hunter Coy uses a periodic system with a LIFO cost flow assumption March's cost of sales for the Z1200 scientific calculators is:

A) $3360.

B) $4500.

C) $5020.

D) $5340.

If Hunter Coy uses a periodic system with a LIFO cost flow assumption March's cost of sales for the Z1200 scientific calculators is:

A) $3360.

B) $4500.

C) $5020.

D) $5340.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

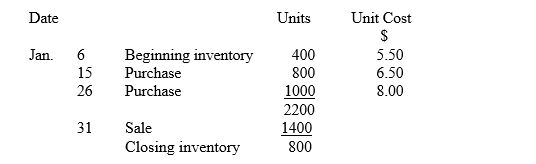

Tully Sales uses a periodic inventory system with the weighted average method of cost assignment. The following data are available.

The cost of sales for January is: (calculate your answer to the nearest whole dollar).

A) $7 000

B) $8 000

C) $9 800

D) $15 400

The cost of sales for January is: (calculate your answer to the nearest whole dollar).

A) $7 000

B) $8 000

C) $9 800

D) $15 400

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/56

Play

Full screen (f)

Deck 13: Inventories

1

Hunter Coy sells calculators. At the beginning of March, 100 Z1200 scientific calculators were on hand for which the firm had paid $25 each. Purchases and sales for the month were as follows.

If Hunter Coy uses a periodic system with a LIFO cost flow assumption March's cost of sales for the Z1200 scientific calculators is:

A) $3360.

B) $4500.

C) $5020.

D) $5340.

If Hunter Coy uses a periodic system with a LIFO cost flow assumption March's cost of sales for the Z1200 scientific calculators is:

A) $3360.

B) $4500.

C) $5020.

D) $5340.

D

2

A major theoretical problem in accounting for inventory is:

A) counting the stock.

B) calculating the cost of purchases.

C) deciding which goods are obsolete.

D) allocating costs between cost of sales and stock on hand.

A) counting the stock.

B) calculating the cost of purchases.

C) deciding which goods are obsolete.

D) allocating costs between cost of sales and stock on hand.

D

3

Which inventory valuation method gives the highest profit when inventory costs are rising?

A) FIFO.

B) LIFO.

C) Weighted average.

D) It is not possible to calculate which method gives the highest profit.

A) FIFO.

B) LIFO.

C) Weighted average.

D) It is not possible to calculate which method gives the highest profit.

A

4

The specific identification method of costing inventory would be unsuitable for which of the following?

A) Works of art

B) Motor vehicles

C) Gold jewellery

D) Petrol at a service station

A) Works of art

B) Motor vehicles

C) Gold jewellery

D) Petrol at a service station

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

5

Inventory is defined as goods held for resale in the ordinary course of business. Which of the following would not be included in inventory for any type of business?

A) Furniture

B) Cash at bank

C) Work in process

D) Land held for resale

A) Furniture

B) Cash at bank

C) Work in process

D) Land held for resale

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

6

The accounting standards governing determination of the cost of inventories are:

A) IAS 3/AASB 3.

B) IAS 8/AASB 8.

C) IAS 2/AASB 102.

D) IAS 34/AASB 134.

A) IAS 3/AASB 3.

B) IAS 8/AASB 8.

C) IAS 2/AASB 102.

D) IAS 34/AASB 134.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

7

A business performing a physical count of inventory on hand is known as a:

A) count.

B) stocklist.

C) stocktake.

D) stockvalue.

A) count.

B) stocklist.

C) stocktake.

D) stockvalue.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

8

Fairy Gardens Ltd uses a periodic inventory system with the weighted average method of cost assignment. The following data are available.

The cost of the ending inventory to the nearest dollar is:

A) $ 5 000.

B) $12 250.

C) $13 000.

D) $49 000.

The cost of the ending inventory to the nearest dollar is:

A) $ 5 000.

B) $12 250.

C) $13 000.

D) $49 000.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

9

Below is an extract from an income statement.

The cost of sales is:

A) $29 500.

B) $32 000.

C) $34 400.

D) $36 900.

The cost of sales is:

A) $29 500.

B) $32 000.

C) $34 400.

D) $36 900.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

10

Blueberry Ltd uses the FIFO assumption with the periodic inventory method.

Sales during year were 18 units. The value of closing stock at the end of the period is:

A) $236

B) $336

C) $415

D) $651

Sales during year were 18 units. The value of closing stock at the end of the period is:

A) $236

B) $336

C) $415

D) $651

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following statements relating to the periodic inventory system is incorrect?

A) Inventory purchases are recorded in the Purchases account.

B) The balance in the Inventory account represents the cost of the inventory on hand at the beginning of the period.

C) The Inventory account is classified as a non-current asset.

D) A stocktake must be performed to determine the ending inventory balance.

A) Inventory purchases are recorded in the Purchases account.

B) The balance in the Inventory account represents the cost of the inventory on hand at the beginning of the period.

C) The Inventory account is classified as a non-current asset.

D) A stocktake must be performed to determine the ending inventory balance.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following is not one of the methods used to assign costs between cost of sales and closing inventory?

A) First-in first-out

B) Weighted average

C) Specific identification

D) Lower of cost and net realisable value

A) First-in first-out

B) Weighted average

C) Specific identification

D) Lower of cost and net realisable value

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following is a disadvantage to business of the LIFO method of applying costs to inventory?

A) It is difficult for a computer program to apply the method.

B) It understates the balance sheet value for inventory.

C) Current income is matched with the most recent costs of acquiring goods.

D) If it is allowed for tax purposes, in times of rising prices it results in less tax being paid in the current period.

A) It is difficult for a computer program to apply the method.

B) It understates the balance sheet value for inventory.

C) Current income is matched with the most recent costs of acquiring goods.

D) If it is allowed for tax purposes, in times of rising prices it results in less tax being paid in the current period.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

14

Which item should not be included in the income statement's cost of inventory?

A) The purchase price of the goods.

B) Cost for normal storage of the goods.

C) Costs incurred in preparing the goods for sale

D) Costs associated with receiving and inspecting the goods

A) The purchase price of the goods.

B) Cost for normal storage of the goods.

C) Costs incurred in preparing the goods for sale

D) Costs associated with receiving and inspecting the goods

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

15

Inventory is normally classified in the balance sheet as a:

A) current liability.

B) current asset.

C) negative asset.

D) non-current asset.

A) current liability.

B) current asset.

C) negative asset.

D) non-current asset.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

16

A physical stocktake is carried out:

A) only under the periodic inventory system.

B) only under the perpetual inventory system.

C) under neither the periodic nor the perpetual systems.

D) under both the periodic and perpetual inventory systems.

A) only under the periodic inventory system.

B) only under the perpetual inventory system.

C) under neither the periodic nor the perpetual systems.

D) under both the periodic and perpetual inventory systems.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is not a step in a properly conducted stocktake?

A) Sale of all damaged goods.

B) Account for all pre-numbered inventory tickets.

C) Recount some items by a supervisor or auditor.

D) Attach an inventory ticket to stock items that have been counted.

A) Sale of all damaged goods.

B) Account for all pre-numbered inventory tickets.

C) Recount some items by a supervisor or auditor.

D) Attach an inventory ticket to stock items that have been counted.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following is not included in the cost of inventory as defined by IAS 2/AASB 102?

A) Cost of purchase.

B) Import duties.

C) GST.

D) Costs incurred in bringing the inventory to its present location and condition.

A) Cost of purchase.

B) Import duties.

C) GST.

D) Costs incurred in bringing the inventory to its present location and condition.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

19

Marlin Co. uses a periodic inventory system with the specific identification method of cost assignment. Inventory purchases for the month of August were:

On 24 August 1200 units from beginning inventory and 1000 units from the 16 August purchase were sold. What was the value of ending inventory at 31 August?

A) $21 600

B) $36 700

C) $39 600

D) $58 300

On 24 August 1200 units from beginning inventory and 1000 units from the 16 August purchase were sold. What was the value of ending inventory at 31 August?

A) $21 600

B) $36 700

C) $39 600

D) $58 300

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

20

In performing a stocktake care must be taken with goods in transit. Which of the following statements is correct?

A) Stock on consignment is regarded as sold by the consignor.

B) Stock on consignment is included in the stock of the consignee.

C) Stock on consignment is included in the stock of the consignor.

D) Goods in transit should be included in both the purchaser's and the seller's inventory.

A) Stock on consignment is regarded as sold by the consignor.

B) Stock on consignment is included in the stock of the consignee.

C) Stock on consignment is included in the stock of the consignor.

D) Goods in transit should be included in both the purchaser's and the seller's inventory.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

21

The main aspect of the perpetual method of accounting for inventory is:

A) a stocktake is performed.

B) it is useful for high value, low volume items.

C) cost of sales is calculated at the end of the accounting period.

D) all movements in each item of stock are tracked via detailed inventory records.

A) a stocktake is performed.

B) it is useful for high value, low volume items.

C) cost of sales is calculated at the end of the accounting period.

D) all movements in each item of stock are tracked via detailed inventory records.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following statements concerning the perpetual inventory method is incorrect?

A) A stocktake is required to estimate cost of sales.

B) Cost of sales is calculated for each transaction.

C) A continuous record is kept of all movements in inventory.

D) With the increased use of computers it has become the most common system.

A) A stocktake is required to estimate cost of sales.

B) Cost of sales is calculated for each transaction.

C) A continuous record is kept of all movements in inventory.

D) With the increased use of computers it has become the most common system.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

23

Which statement relating to the moving average method of costing inventories, used with the perpetual inventory system, is incorrect?

A) A new average cost is calculated after each sale.

B) A new average cost is calculated after each purchase return.

C) In periods of rising prices the profit result is between that of the FIFO and LIFO methods.

D) The formula for average cost is cost of goods available for sale divided by units for sale.

A) A new average cost is calculated after each sale.

B) A new average cost is calculated after each purchase return.

C) In periods of rising prices the profit result is between that of the FIFO and LIFO methods.

D) The formula for average cost is cost of goods available for sale divided by units for sale.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following statements relating to the lower of cost and net realisable value rule is incorrect?

A) The rule is based on the accounting principle of prudence (conservatism).

B) It results in probable losses being recorded in the period when they are first noticed rather than when the sale occurs.

C) The gross profit reported in the period when the rule is applied is higher than it otherwise would be.

D) The rule is applied separately to each item of inventory or to each group of inventory.

A) The rule is based on the accounting principle of prudence (conservatism).

B) It results in probable losses being recorded in the period when they are first noticed rather than when the sale occurs.

C) The gross profit reported in the period when the rule is applied is higher than it otherwise would be.

D) The rule is applied separately to each item of inventory or to each group of inventory.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

25

Products can be uniquely identified by using:

A) ledger account numbers.

B) purchase order numbers.

C) photos.

D) bar codes.

A) ledger account numbers.

B) purchase order numbers.

C) photos.

D) bar codes.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following are advantages of the weighted average method of applying costs to inventory?

I) It is not subject to profit manipulation.

II) The profit and closing inventory values tend to be 'smoothed' compared to other methods.

III) It is simple to understand.

A) I and II only

B) I and III only

C) II and III only

D) I, II and III

I) It is not subject to profit manipulation.

II) The profit and closing inventory values tend to be 'smoothed' compared to other methods.

III) It is simple to understand.

A) I and II only

B) I and III only

C) II and III only

D) I, II and III

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

27

Which statement relating to the determination of the cost of inventory in a computerised system is not true?

A) Computerised inventory systems are now used by most firms.

B) The system can automatically produce reorder information.

C) Computerised systems generally use the periodic inventory system.

D) Determining the cost of inventory is greatly simplified compared to a manual system.

A) Computerised inventory systems are now used by most firms.

B) The system can automatically produce reorder information.

C) Computerised systems generally use the periodic inventory system.

D) Determining the cost of inventory is greatly simplified compared to a manual system.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

28

Tully Sales uses a periodic inventory system with the weighted average method of cost assignment. The following data are available.

The cost of sales for January is: (calculate your answer to the nearest whole dollar).

A) $7 000

B) $8 000

C) $9 800

D) $15 400

The cost of sales for January is: (calculate your answer to the nearest whole dollar).

A) $7 000

B) $8 000

C) $9 800

D) $15 400

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

29

With the perpetual method of accounting for inventory the first-in first-out assumption is applied to:

A) inventory at the end of the month.

B) cost of sales at the end of the month.

C) cost of sales at the end of the accounting year.

D) each sale via stock cards or computer records.

A) inventory at the end of the month.

B) cost of sales at the end of the month.

C) cost of sales at the end of the accounting year.

D) each sale via stock cards or computer records.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

30

Which statement is correct?

A) LIFO assumes that cost of sales consists of the oldest purchases.

B) LIFO assumes that stock at end consists of the most recent purchases.

C) LIFO assumes the last goods purchased are the first goods sold.

D) LIFO assumes the first goods purchased are the first goods sold.

A) LIFO assumes that cost of sales consists of the oldest purchases.

B) LIFO assumes that stock at end consists of the most recent purchases.

C) LIFO assumes the last goods purchased are the first goods sold.

D) LIFO assumes the first goods purchased are the first goods sold.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

31

If inventory costs are decreasing, profit will be highest if the inventory method used is:

A) FIFO.

B) LIFO.

C) weighted average.

D) It is not possible to answer the question.

A) FIFO.

B) LIFO.

C) weighted average.

D) It is not possible to answer the question.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

32

NET Computers sold 20 modems for $60 on 30 April. At that date, the stock card for the modems sold had a total of 50 modems on hand at an average cost of $45.50 each. What is the cost of the modems recognised in the income statement? Assume the weighted average method of costing is used.

A) $910

B) $1 200

C) $2 275

D) $3 000

A) $910

B) $1 200

C) $2 275

D) $3 000

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

33

Which statement concerning inventory is incorrect?

A) Consistency rules out ever switching to an alternative accounting method.

B) Consistency is an important consideration when alternative accounting methods exist.

C) Once an inventory costing method is selected management should not deliberately switch to another to manipulate profits.

D) Accounting data produced in different accounting periods is not comparable if arbitrary changes in accounting methods are permitted.

A) Consistency rules out ever switching to an alternative accounting method.

B) Consistency is an important consideration when alternative accounting methods exist.

C) Once an inventory costing method is selected management should not deliberately switch to another to manipulate profits.

D) Accounting data produced in different accounting periods is not comparable if arbitrary changes in accounting methods are permitted.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

34

With the perpetual method of accounting for inventory, the costing assumption, such as first-in first-out, is applied to:

A) inventory at the end of the month.

B) cost of sales at the end of the accounting year.

C) each sale via stock cards or computer records.

D) the current asset inventory in the balance sheet.

A) inventory at the end of the month.

B) cost of sales at the end of the accounting year.

C) each sale via stock cards or computer records.

D) the current asset inventory in the balance sheet.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

35

Assuming rising inventory prices, which statement is correct?

A) FIFO reports a lower profit than other methods.

B) FIFO reports a lower value for cost of sales than other methods.

C) FIFO reports a lower value for closing inventory than other methods.

D) Using FIFO, it is not possible to calculate whether cost of sales/inventory is lower or higher than it would be if other assumptions about inventory valuation were made.

A) FIFO reports a lower profit than other methods.

B) FIFO reports a lower value for cost of sales than other methods.

C) FIFO reports a lower value for closing inventory than other methods.

D) Using FIFO, it is not possible to calculate whether cost of sales/inventory is lower or higher than it would be if other assumptions about inventory valuation were made.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

36

The lower of cost or net realisable value procedure is used with which of the following inventory methods?

I) FIFO

II) LIFO

III) Weighted average

IV) The perpetual method

A) IV only

B) I and III only

C) I, II, III and IV

D) I, III and IV only

I) FIFO

II) LIFO

III) Weighted average

IV) The perpetual method

A) IV only

B) I and III only

C) I, II, III and IV

D) I, III and IV only

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

37

Fabulous Furniture uses a periodic inventory system. Many purchases and sales of goods occur during the financial year. For Fabulous Furniture, the balance in the general ledger inventory account:

A) will usually be zero except at a balance sheet date.

B) does not change until a stocktake is carried out.

C) represents the goods on hand at any given point in time.

D) reports the goods purchased since the beginning of the accounting period.

A) will usually be zero except at a balance sheet date.

B) does not change until a stocktake is carried out.

C) represents the goods on hand at any given point in time.

D) reports the goods purchased since the beginning of the accounting period.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

38

In the event of rising inventory prices, the method of inventory valuation that gives the highest profit and the highest ending inventory is the:

A) FIFO method.

B) LIFO method.

C) Weighted average.

D) Perpetual method.

A) FIFO method.

B) LIFO method.

C) Weighted average.

D) Perpetual method.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

39

Which statement relating to the moving average method of costing inventories, used with the perpetual inventory system, is correct?

A) A new average cost is calculated after each sale.

B) A new average cost is calculated after each purchase.

C) A new average cost is calculated at the end of each month.

D) A new average cost is calculated after each sale and each purchase.

A) A new average cost is calculated after each sale.

B) A new average cost is calculated after each purchase.

C) A new average cost is calculated at the end of each month.

D) A new average cost is calculated after each sale and each purchase.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

40

Under IAS 2/AASB 102 the costing method that is not permitted is:

A) FIFO.

B) LIFO.

C) weighted/moving average.

D) specific identification.

A) FIFO.

B) LIFO.

C) weighted/moving average.

D) specific identification.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

41

The following are possible sources of error in calculating closing inventory except for:

A) Mistakes in counting during the stocktake.

B) An incorrect cut-off between accounting periods.

C) Mistakes in dealing with goods on consignment.

D) Mistakes in the price at which the goods are sold to customers.

A) Mistakes in counting during the stocktake.

B) An incorrect cut-off between accounting periods.

C) Mistakes in dealing with goods on consignment.

D) Mistakes in the price at which the goods are sold to customers.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

42

The following information concerning inventory is required to be disclosed in the external financial reports except for:

A) Finished goods

B) Work in process

C) Inventory turnover ratio

D) Method of valuation,e.g. FIFO, weighted average

A) Finished goods

B) Work in process

C) Inventory turnover ratio

D) Method of valuation,e.g. FIFO, weighted average

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

43

All of the following statements about the presentation of inventory in financial reports are correct except for:

A) The general basis of valuation should be shown,e.g. cost, NRV.

B) The assumption used to assign costs to inventory should be disclosed.

C) Inventory should be classified into its current and non-current components.

D) Inventory shown on the balance sheet should always be in a saleable condition.

A) The general basis of valuation should be shown,e.g. cost, NRV.

B) The assumption used to assign costs to inventory should be disclosed.

C) Inventory should be classified into its current and non-current components.

D) Inventory shown on the balance sheet should always be in a saleable condition.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following statements is incorrect?

A) In certain circumstances, some inventory items will be valued at above cost.

B) In certain circumstances, some inventory items will be valued at below cost.

C) Inventory is normally valued at cost.

D) Net realisable value is related to estimated market value.

A) In certain circumstances, some inventory items will be valued at above cost.

B) In certain circumstances, some inventory items will be valued at below cost.

C) Inventory is normally valued at cost.

D) Net realisable value is related to estimated market value.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

45

Ricardo Clothing uses a periodic inventory system and committed an error that overstated inventory at the end of Year One. Assuming no further errors occur during the following year, at the end of Year Two:

A) profit is understated; equity is overstated.

B) profit is understated; equity is correct.

C) profit is overstated; equity is correct.

D) profit is overstated; equity is overstated.

A) profit is understated; equity is overstated.

B) profit is understated; equity is correct.

C) profit is overstated; equity is correct.

D) profit is overstated; equity is overstated.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

46

The formula, cost of sales/average inventory, measures the:

A) gross profit ratio.

B) number of times, on average, that inventory is turned over per year.

C) mark-up on inventory expressed as a percentage of the cost price.

D) mark-up on inventory expressed as a percentage of the selling price.

A) gross profit ratio.

B) number of times, on average, that inventory is turned over per year.

C) mark-up on inventory expressed as a percentage of the cost price.

D) mark-up on inventory expressed as a percentage of the selling price.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following statements relating to the lower of cost and net realisable is incorrect?

A) It results in probable losses being recorded in the period when they are first noticed rather than when the sale occurs.

B) The rule is based on the accounting principle of conservatism (prudence).

C) The rule is applied separately to each item of inventory or to groups of inventory items.

D) The gross profit reported in the period when the rule is applied is higher than it otherwise would be.

A) It results in probable losses being recorded in the period when they are first noticed rather than when the sale occurs.

B) The rule is based on the accounting principle of conservatism (prudence).

C) The rule is applied separately to each item of inventory or to groups of inventory items.

D) The gross profit reported in the period when the rule is applied is higher than it otherwise would be.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

48

Under the FIFO method sales returns are costed back into inventory at:

A) an average cost price.

B) the most recent cost price attached to a sale.

C) a price determined by the accountant.

D) the original cost price that was attached to the original sale.

A) an average cost price.

B) the most recent cost price attached to a sale.

C) a price determined by the accountant.

D) the original cost price that was attached to the original sale.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

49

Which of the following are reasons for the selling value of some inventory items falling below their cost price?

I) Obsolescence

II) Damage

III) Past use-by date

IV) A rise in the market price

A) I and II only.

B) II and III only.

C) I, II and III only.

D) I, II, III and IV.

I) Obsolescence

II) Damage

III) Past use-by date

IV) A rise in the market price

A) I and II only.

B) II and III only.

C) I, II and III only.

D) I, II, III and IV.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

50

The ratio that indicates an entity's overall mark-up on goods sold is the:

A) gross profit ratio.

B) profit margin ratio.

C) inventory turnover ratio.

D) return on inventory ratio.

A) gross profit ratio.

B) profit margin ratio.

C) inventory turnover ratio.

D) return on inventory ratio.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

51

The end of the financial year for Ziggie's Trading Company is 30 June 2019. At that date, ending inventory was understated by $3 650. The profit for the year ending 30 June 2019 will be:

A) understated.

B) overstated.

C) correctly stated.

D) dependant on whether or not the inventory increased during 2019.

A) understated.

B) overstated.

C) correctly stated.

D) dependant on whether or not the inventory increased during 2019.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

52

Stanley Inc. has an historical gross profit percentage of 40%. Net purchases for six months were $2800 and sales were $4000. Inventory at the end of the previous period was $300. If Stanley Inc. prepares an interim balance sheet, the amount that can be estimated for closing inventory is:

A) $300.

B) $700.

C) $1600.

D) $2400.

A) $300.

B) $700.

C) $1600.

D) $2400.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

53

Novice Co purchased goods for $2500. While on display, the goods were damaged and it is estimated that they can now only be sold for $1800. Additional marketing and distribution costs are $200. The net realisable value of the goods is:

A) $700.

B) $500.

C) $1600.

D) $2300.

A) $700.

B) $500.

C) $1600.

D) $2300.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

54

If Michelle knows that the ending inventory at retail for her corner store is $22 000 and her cost to retail percentage is 45%, her ending inventory at cost can be estimated as:

A) $9 900.

B) $12 100.

C) $31 900.

D) $40 000.

A) $9 900.

B) $12 100.

C) $31 900.

D) $40 000.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

55

In relation to inventory, net realisable value is the estimated:

A) discounted value.

B) replacement value.

C) selling price less stock loss.

D) selling price less anticipated further costs to complete the sale.

A) discounted value.

B) replacement value.

C) selling price less stock loss.

D) selling price less anticipated further costs to complete the sale.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following statements concerning the retail inventory method of estimating closing stock is incorrect?

A) It can be applied with or without a physical stocktake being carried out.

B) A stocktake is carried out, valued at retail and then converted to cost by applying the historical gross profit percentage.

C) The ratio of cost to retail is goods available for sale at cost divided by the goods available for sale at retail.

D) Differences in the mix of inventory compared to the mix used to determine the cost ratio does not affect the accuracy of the method.

A) It can be applied with or without a physical stocktake being carried out.

B) A stocktake is carried out, valued at retail and then converted to cost by applying the historical gross profit percentage.

C) The ratio of cost to retail is goods available for sale at cost divided by the goods available for sale at retail.

D) Differences in the mix of inventory compared to the mix used to determine the cost ratio does not affect the accuracy of the method.

Unlock Deck

Unlock for access to all 56 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 56 flashcards in this deck.