Deck 17: Auditing and Evaluating the AIS

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

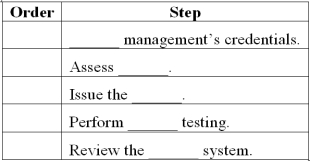

Generic audit steps:

Fill in the blanks with appropriate words or phrases based on the generic steps of financial statement audits. Then, number the steps in the order of their occurrence.

Fill in the blanks with appropriate words or phrases based on the generic steps of financial statement audits. Then, number the steps in the order of their occurrence.

Question

Question

Question

Question

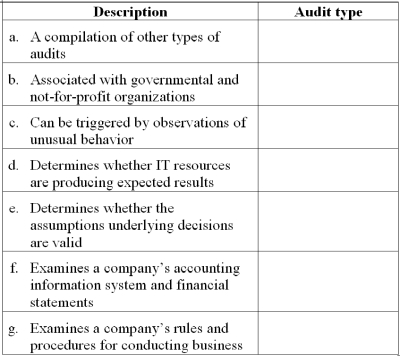

Types of audits Which type of audit is described in each independent item below?

Question

Question

Match between columns

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/53

Play

Full screen (f)

Deck 17: Auditing and Evaluating the AIS

1

In general, inexperienced auditors take on very focused assignments, with the results being reviewed by more experienced auditors. That process upholds an auditing standard in which area?

A) General.

B) Field work.

C) Reporting.

D) Procedural.

A) General.

B) Field work.

C) Reporting.

D) Procedural.

B

2

In most financial statement audits, ___ immediately precedes compliance testing.

A) Assess management's integrity.

B) Evaluate management's credentials.

C) Review the internal control system.

D) Issue an opinion.

A) Assess management's integrity.

B) Evaluate management's credentials.

C) Review the internal control system.

D) Issue an opinion.

C

3

Which of the following is a field work auditing standard?

A) Internal control.

B) Professional care.

C) Consistency.

D) Disclosure.

A) Internal control.

B) Professional care.

C) Consistency.

D) Disclosure.

A

4

Right before issuing the audit report, most financial statement auditors:

A) Prepare financial statements.

B) Plan compliance testing.

C) Review internal controls.

D) Perform compliance testing.

A) Prepare financial statements.

B) Plan compliance testing.

C) Review internal controls.

D) Perform compliance testing.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

5

Which type of audit determines whether the assumptions underlying decisions are valid?

A) Systems audit.

B) Compliance audit.

C) Management audit.

D) Investigative audit.

A) Systems audit.

B) Compliance audit.

C) Management audit.

D) Investigative audit.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

6

In most financial statement audits, what happens immediately after assessing management's integrity?

A) Evaluate management's credentials.

B) Evaluate the internal control system.

C) Plan compliance testing.

D) Conduct compliance testing.

A) Evaluate management's credentials.

B) Evaluate the internal control system.

C) Plan compliance testing.

D) Conduct compliance testing.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

7

An auditor is dating an accounting manager in a firm he is auditing. His behavior is most likely in violation of a ___ standard.

A) General.

B) Field work.

C) Reporting.

D) Forensic.

A) General.

B) Field work.

C) Reporting.

D) Forensic.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

8

A(n) ___ audit examines a company's rules and procedures for doing business.

A) Systems audit.

B) Investigative audit.

C) Operational audit.

D) Management audit.

A) Systems audit.

B) Investigative audit.

C) Operational audit.

D) Management audit.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

9

NASA (National Aeronautics and Space Administration) would be most likely to need which type of audit?

A) Financial statement audit.

B) Compliance audit.

C) Systems audit.

D) International audit.

A) Financial statement audit.

B) Compliance audit.

C) Systems audit.

D) International audit.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following types of audits involves expressing an opinion?

A) Financial statement audit.

B) Operational audit.

C) Management audit.

D) Systems audit.

A) Financial statement audit.

B) Operational audit.

C) Management audit.

D) Systems audit.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

11

Which type of audit is associated most closely with forensic accounting?

A) Investigative audit.

B) Compliance audit.

C) Systems audit.

D) Financial statement audit.

A) Investigative audit.

B) Compliance audit.

C) Systems audit.

D) Financial statement audit.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

12

Auditors exercise judgment when they issue: (i) unqualified opinions, (ii) adverse opinions, (iii) error opinions.

A) i and ii only.

B) ii and iii only.

C) i and iii only.

D) i, ii and iii.

A) i and ii only.

B) ii and iii only.

C) i and iii only.

D) i, ii and iii.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

13

Which type of audit looks "inside the box?"

A) Management audit.

B) Financial statement audit.

C) Compliance audit.

D) Systems audit.

A) Management audit.

B) Financial statement audit.

C) Compliance audit.

D) Systems audit.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

14

The final step in most financial statement audits is:

A) Review the internal control system.

B) Issue an opinion.

C) Prepare financial statements.

D) Perform compliance testing.

A) Review the internal control system.

B) Issue an opinion.

C) Prepare financial statements.

D) Perform compliance testing.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following is not a classification of the AICPA's auditing standards?

A) Financial.

B) General.

C) Field work.

D) Reporting.

A) Financial.

B) General.

C) Field work.

D) Reporting.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is most likely to trigger an investigative audit?

A) An adverse opinion on financial statements.

B) Mathematical errors.

C) Discrepancies between purchase orders and receiving reports.

D) Journal entries that fail to balance.

A) An adverse opinion on financial statements.

B) Mathematical errors.

C) Discrepancies between purchase orders and receiving reports.

D) Journal entries that fail to balance.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

17

Flowcharts and other forms of systems documentation are useful in: (i) operational audits, (ii) investigative audits.

A) i only.

B) ii only.

C) Both i and ii.

D) Neither i nor ii.

A) i only.

B) ii only.

C) Both i and ii.

D) Neither i nor ii.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following is a reporting auditing standard?

A) Training.

B) Supervision.

C) GAAP.

D) Evidence.

A) Training.

B) Supervision.

C) GAAP.

D) Evidence.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is a general auditing standard?

A) Supervision.

B) Disclosure.

C) Opinion.

D) Independence.

A) Supervision.

B) Disclosure.

C) Opinion.

D) Independence.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following occurs first in most audit processes?

A) Assess management's integrity.

B) Evaluate management's credentials.

C) Review the internal control system.

D) Perform compliance testing.

A) Assess management's integrity.

B) Evaluate management's credentials.

C) Review the internal control system.

D) Perform compliance testing.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

21

Examining remittance advices in a financial statement audit helps fulfill which auditing standard?

A) Disclosure.

B) Supervision.

C) GAAP.

D) Evidence.

A) Disclosure.

B) Supervision.

C) GAAP.

D) Evidence.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

22

All of the following link accounting information systems with auditing except:

A) Flowcharting.

B) General ledger software.

C) Field work standards.

D) The sales/collection process.

A) Flowcharting.

B) General ledger software.

C) Field work standards.

D) The sales/collection process.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

23

Which group of auditing standards requires auditors to have a college degree in accounting?

A) General.

B) Field work.

C) Reporting.

D) Auditing standards do not require auditors to have a college degree in accounting.

A) General.

B) Field work.

C) Reporting.

D) Auditing standards do not require auditors to have a college degree in accounting.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

24

"Supervision," as associated with generally accepted auditing standards applies to: (i) inexperienced auditors, (ii) auditors without CPA licenses, (iii) auditors with CPA licenses.

A) i and ii only.

B) ii and iii only.

C) i and iii only.

D) i, ii and iii.

A) i and ii only.

B) ii and iii only.

C) i and iii only.

D) i, ii and iii.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

25

A company's accounting information system reports the book value of computer equipment as $25,000. During compliance testing, an auditor would need to see the computer equipment to verify which assertion?

A) Existence.

B) Valuation.

C) Obligations.

D) Completeness.

A) Existence.

B) Valuation.

C) Obligations.

D) Completeness.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

26

In a financial statement audit, questionnaires and interviews can be helpful in: (i) assessing management's integrity, (ii) reviewing internal controls.

A) i only.

B) ii only.

C) Both i and ii.

D) Neither i nor ii.

A) i only.

B) ii only.

C) Both i and ii.

D) Neither i nor ii.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

27

An auditor carefully documents every conclusion reached and every balance calculated in a financial statement audit because of which auditing standard?

A) Internal control.

B) Independence.

C) Supervision.

D) Professional care.

A) Internal control.

B) Independence.

C) Supervision.

D) Professional care.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

28

The Sarbanes-Oxley Act of 2002 impacts auditors' actions most directly when they:

A) Express an opinion on financial statements.

B) Complete an investigative audit.

C) Review the internal control system.

D) Participate in a SAS 70 audit.

A) Express an opinion on financial statements.

B) Complete an investigative audit.

C) Review the internal control system.

D) Participate in a SAS 70 audit.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

29

The "completeness" assertion associated with financial statement audits is most closely associated with which general auditing standard?

A) Independence.

B) Disclosure.

C) Consistency.

D) Evidence.

A) Independence.

B) Disclosure.

C) Consistency.

D) Evidence.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

30

Which type of audit is not indicated by any of the situations above?

A) Financial statement.

B) Operational.

C) Compliance.

D) Investigative.

A) Financial statement.

B) Operational.

C) Compliance.

D) Investigative.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

31

If management lacks integrity, auditors issue which type of opinion: (i) disclaimer, (ii) adverse.

A) i only.

B) ii only.

C) Neither i nor ii.

D) Either i or ii.

A) i only.

B) ii only.

C) Neither i nor ii.

D) Either i or ii.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following is the most direct subject of an audit opinion?

A) Financial statements.

B) Internal controls.

C) Management's integrity.

D) Independence.

A) Financial statements.

B) Internal controls.

C) Management's integrity.

D) Independence.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

33

In a financial statement audit, interviews to determine risk exposures help fulfill which auditing standard?

A) Internal controls.

B) Disclosure.

C) Consistency.

D) Training.

A) Internal controls.

B) Disclosure.

C) Consistency.

D) Training.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

34

Purchase orders and customer invoices are most closely associated with which type of standard in a financial statement audit?

A) General.

B) Field work.

C) Documentation.

D) Reporting.

A) General.

B) Field work.

C) Documentation.

D) Reporting.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

35

A U.S. auditor prepares a Mexican company's financial statements using international accounting rules, violating:

A) A general standard.

B) A field work standard.

C) A reporting standard.

D) No standard.

A) A general standard.

B) A field work standard.

C) A reporting standard.

D) No standard.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

36

All of the following link accounting information systems with auditing except:

A) Steps for Better Thinking.

B) SAS 70.

C) The human resources business process.

D) Professional certification.

A) Steps for Better Thinking.

B) SAS 70.

C) The human resources business process.

D) Professional certification.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

37

A client refuses to let a financial statement auditor examine certain documents. The auditor is most likely to issue a(n) ___ opinion.

A) Unqualified.

B) Qualified.

C) Disclaimer.

D) Adverse.

A) Unqualified.

B) Qualified.

C) Disclaimer.

D) Adverse.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

38

After examining a firm's accounting information system, an auditor concluded that the firm's financial statements are fairly presented, thus fulfilling which auditing standard?

A) Opinion.

B) Disclosure.

C) GAAP.

D) Evidence.

A) Opinion.

B) Disclosure.

C) GAAP.

D) Evidence.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

39

An auditor might test the accuracy of biometric identification systems, such as fingerprint scanning, in which generic audit step?

A) Step one.

B) Step two.

C) Step three.

D) Step four.

A) Step one.

B) Step two.

C) Step three.

D) Step four.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

40

Why does a financial statement auditor evaluate management's credentials after assessing management's integrity?

A) Because credentials are more objective.

B) Because integrity is less important.

C) Because managers can have integrity without credentials.

D) Because credentials can be falsified more easily than integrity.

A) Because credentials are more objective.

B) Because integrity is less important.

C) Because managers can have integrity without credentials.

D) Because credentials can be falsified more easily than integrity.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

41

The following paragraph applies to Questions 61 - 65:

Your school's accounting club will soon host a one-day seminar on auditing and evaluating accounting information systems. You know you'll be talking with experienced auditors during the seminar; you want to demonstrate your knowledge of auditing to make a good impression.

The Sarbanes-Oxley Act of 2002 contains at least five sections that relate to the audit process: 302, 401, 404, 409 and 802. Explain how each section is related to one or more of the AICPA's ten generally accepted auditing standards.

Your school's accounting club will soon host a one-day seminar on auditing and evaluating accounting information systems. You know you'll be talking with experienced auditors during the seminar; you want to demonstrate your knowledge of auditing to make a good impression.

The Sarbanes-Oxley Act of 2002 contains at least five sections that relate to the audit process: 302, 401, 404, 409 and 802. Explain how each section is related to one or more of the AICPA's ten generally accepted auditing standards.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

42

Generally accepted auditing standards

Draw an original diagram that illustrates the AICPA's ten generally accepted auditing standards. Your diagram should not resemble the one in the text in any way.

Draw an original diagram that illustrates the AICPA's ten generally accepted auditing standards. Your diagram should not resemble the one in the text in any way.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

43

Financial statement audits

A financial statement auditor completed the following steps in a recent engagement. Number the steps in the order of their occurrence based on the generic audit steps discussed in the text.

______

a. Compose an unqualified opinion.

______

b. Confirm the existence of inventory.

______

c. Determine risk exposures.

______

d. Interview employees about management's overall attitude.

______

e. Obtain copies of college transcripts and professional certifications.

A financial statement auditor completed the following steps in a recent engagement. Number the steps in the order of their occurrence based on the generic audit steps discussed in the text.

______

a. Compose an unqualified opinion.

______

b. Confirm the existence of inventory.

______

c. Determine risk exposures.

______

d. Interview employees about management's overall attitude.

______

e. Obtain copies of college transcripts and professional certifications.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

44

All of the following link accounting information systems with auditing except:

A) The conversion process.

B) Financial statements.

C) Enterprise resource planning systems.

D) Reporting standards.

A) The conversion process.

B) Financial statements.

C) Enterprise resource planning systems.

D) Reporting standards.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

45

The following paragraph applies to Questions 61 - 65:

Your school's accounting club will soon host a one-day seminar on auditing and evaluating accounting information systems. You know you'll be talking with experienced auditors during the seminar; you want to demonstrate your knowledge of auditing to make a good impression.

List, in order, the steps commonly associated with a financial statement audit.

Your school's accounting club will soon host a one-day seminar on auditing and evaluating accounting information systems. You know you'll be talking with experienced auditors during the seminar; you want to demonstrate your knowledge of auditing to make a good impression.

List, in order, the steps commonly associated with a financial statement audit.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

46

AIS and auditing connections

List three topics that connect the subject matter of accounting information systems with the subject matter of auditing. Then, draw a diagram that illustrates how the topics are connected.

List three topics that connect the subject matter of accounting information systems with the subject matter of auditing. Then, draw a diagram that illustrates how the topics are connected.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

47

Generic audit steps:

Fill in the blanks with appropriate words or phrases based on the generic steps of financial statement audits. Then, number the steps in the order of their occurrence.

Fill in the blanks with appropriate words or phrases based on the generic steps of financial statement audits. Then, number the steps in the order of their occurrence.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

48

All of the following link accounting information systems with auditing except:

A) The acquisition/payment process.

B) Independence.

C) Bank reconciliations.

D) Data flow diagramming.

A) The acquisition/payment process.

B) Independence.

C) Bank reconciliations.

D) Data flow diagramming.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

49

Investigative audits

An investigative auditor planned to complete the following actions; number them in their preferred order of occurrence.

______

a. Discuss evidence obtained in other steps with the main suspect.

______

b. Interview accounting employees who created journal entries to cover up an inventory theft.

______

c. Obtain copies of purchase orders.

______

d. Question receiving department employees that may have observed inventory theft.

______

e. Review video surveillance tapes.

An investigative auditor planned to complete the following actions; number them in their preferred order of occurrence.

______

a. Discuss evidence obtained in other steps with the main suspect.

______

b. Interview accounting employees who created journal entries to cover up an inventory theft.

______

c. Obtain copies of purchase orders.

______

d. Question receiving department employees that may have observed inventory theft.

______

e. Review video surveillance tapes.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

50

The following paragraph applies to Questions 61 - 65:

Your school's accounting club will soon host a one-day seminar on auditing and evaluating accounting information systems. You know you'll be talking with experienced auditors during the seminar; you want to demonstrate your knowledge of auditing to make a good impression.

Most accounting information systems are organized into five basic parts: inputs, processes, outputs, storage and internal controls. Use that framework to explain how auditing is related to the study of accounting information systems.

Your school's accounting club will soon host a one-day seminar on auditing and evaluating accounting information systems. You know you'll be talking with experienced auditors during the seminar; you want to demonstrate your knowledge of auditing to make a good impression.

Most accounting information systems are organized into five basic parts: inputs, processes, outputs, storage and internal controls. Use that framework to explain how auditing is related to the study of accounting information systems.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

51

Types of audits Which type of audit is described in each independent item below?

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

52

All of the following link accounting information systems with auditing except:

A) Data normalization rules.

B) Communication skills.

C) Knowledge of internal controls.

D) Business documents.

A) Data normalization rules.

B) Communication skills.

C) Knowledge of internal controls.

D) Business documents.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

54

Match between columns

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 53 flashcards in this deck.