Deck 20: Managing Credit Risk on the Balance Sheet

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

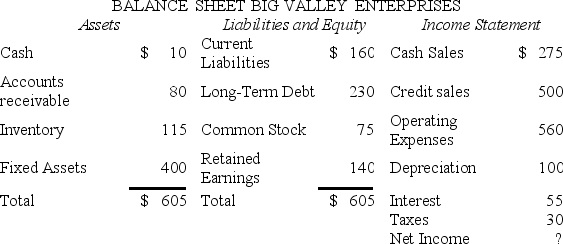

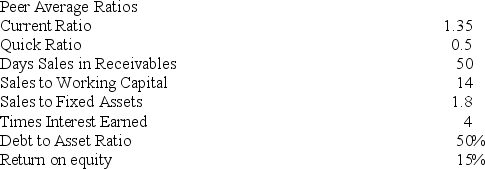

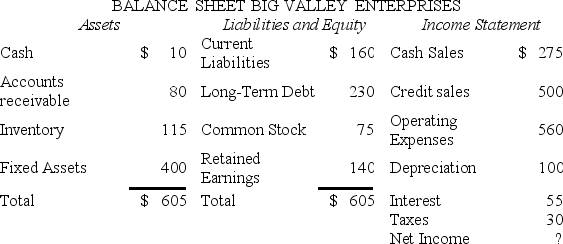

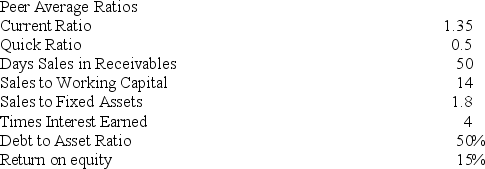

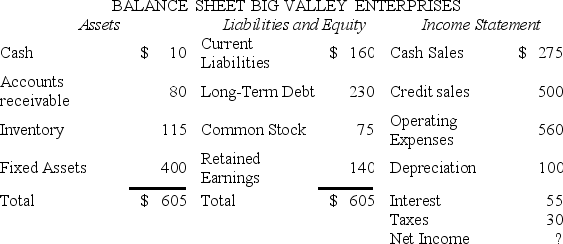

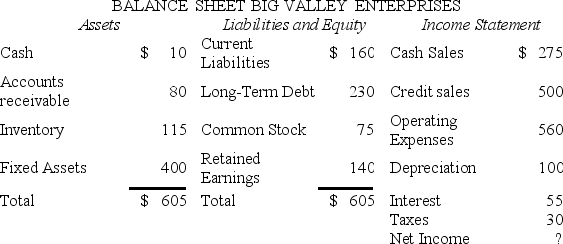

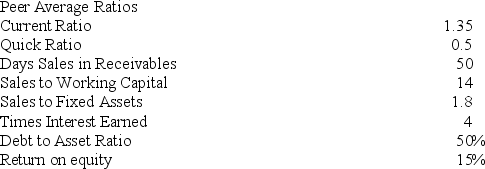

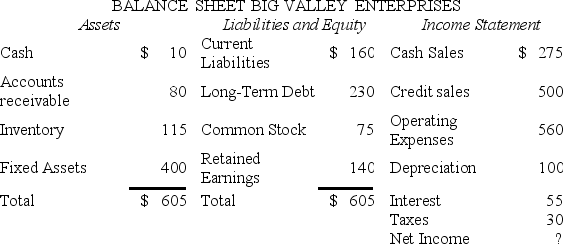

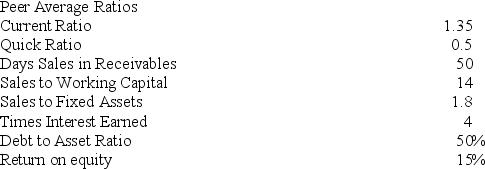

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Big Valley's fixed asset efficiency score is ________ which is ________that of the typical firm in the industry.

A)1.8; the same as

B)1.54; lower than

C)1.94; higher than

D)2.15; higher than

E)1.32; lower than

Question

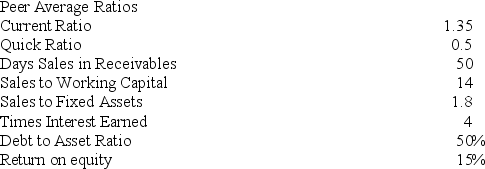

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Big Valley's use of debt to finance assets indicates that Big Valley has ________ the typical firm in the industry.

A)more long-term solvency risk than

B)the same long-term solvency risk as

C)less interest expense than

D)less long-term solvency risk than

E)a lower market value of equity to book value of equity ratio than

Question

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Big Valley's return on equity indicates that the firm generates a ________ return to their shareholders than their peers.

A)2.04 percent higher

B)3.02 percent higher

C)15.25 percent higher

D)5.75 percent lower

E)1.05 percent lower

Question

Question

GDS cutoff: 30 percent

TDS cutoff: 35 percent

Using only the TDS criteria,which one of the following statements is true?

A)Joe gets the loan,but Bill does not.

B)Bill gets the loan,but Joe does not.

C)Both get the loan.

D)Neither gets the loan.

E)The bank does not have money to make the loan.

Question

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Big Valley's current ratio indicates that Big Valley is ________ liquid than the typical firm in the industry,and Big Valley's quick ratio indicates that Big Valley is ________ liquid than the typical firm.

A)more; more

B)more; less

C)less; less

D)less; more

E)similar; similar

Question

Question

Question

Question

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Big Valley is collecting their receivables about ________ than the typical firm.

A)22 percent more quickly

B)12 percent more quickly

C)17 percent more slowly

D)12 percent more slowly

E)16 percent more quickly

Question

Question

Question

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Altman's Z-score model is Z = 1.2X1 + 1.4X2 + 3.3X3 + 0.6X4 + 1.0X5.

X1 = Working Capital/Total Assets

X2 = Retained Earnings/Total Assets

X3 = EBIT/Total Assets

X4 = Market Value Equity/Book Value Long-Term Debt

X5 = Sales/Total Assets

Using the Altman's Z model,Big Valley's Z-score is

A)3.22.

B)2.88.

C)2.65.

D)2.11.

E)1.85.

Question

Question

Question

Question

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Big Valley has a times interest earned ratio that is ________,which indicates that Big Valley has ________ long-term insolvency risk than the typical firm in the industry.

A)4; the same

B)3.91; less

C)3.91; more

D)4.58; more

E)4.58; less

Question

GDS cutoff: 30 percent

TDS cutoff: 35 percent

Using only the GDS criteria,which one of the following statements is true?

A)Joe gets the loan,but Bill does not.

B)Bill gets the loan,but Joe does not.

C)Both get the loan.

D)Neither gets the loan.

E)The bank does not have money to make the loan.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/63

Play

Full screen (f)

Deck 20: Managing Credit Risk on the Balance Sheet

1

The five Cs of credit are financial capacity,collateral,conditions,connections with the bank,and capital.

False

2

Management of credit risk is achieved through diversification effect by combining numerous loans in a portfolio.

True

3

Issuance of short-term debt would result in an increase in cash flow from operations on the statement of cash flows.

False

4

The risk-adjusted return on capital (RAROC)model calculates the actual or promised annual cash flow on a loan as a percentage of the amount lent.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

5

Credit analysis of a mid-market corporate borrower differs from the analysis of a small business in that the analysis of the mid-market borrower is more focused on the business itself and less on the business owners.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

6

Individuals with higher levels of income must have higher GDS and TDS ratios to qualify for a loan.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

7

A firm's cash account grew by $300 over the year when the firm had cash flow from financing of −$150 and cash flow from investing of $100. The firm's operating cash flow must have been +$250.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

8

If you were a loan officer evaluating a small business credit application for a loan secured by working capital,you would generally want to see a higher (rather than lower)number of days in inventory and number of days' sales in receivables.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

9

The more variable a borrower's cash flows are,the lower the fixed charge coverage ratio should be to limit risk.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

10

Credit scoring models are probabilistic models based on economic and financial borrower characteristics aiming to determining the likelihood of default of a borrower.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

11

Asset management ratios are used in credit analysis to help understand the borrower's ability to generate sales from the amount invested in some asset category.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

12

Collateral on a mortgage is normally only considered if the applicant has enough income to service the loan.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

13

Analysis of the statement of cash flows involves assessment of operating,financing and investing cash flows and analysis of the resulting net income.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

14

Provision for loan losses,net charge-offs,and the percentage of nonperforming loans all increased dramatically in 2007.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

15

Gross debt service usually must be greater than 30 percent before a residential mortgage will be approved.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

16

Junk bonds usually yield lower returns than investment-grade bonds due to their speculative feature.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

17

If you are a lender evaluating a loan application and you calculate the following ratio: (EBIT + Lease Payments)/[Interest + Lease Payments + (Sinking Fund/(1 − T))],then you are calculating a debt service ratio and it should be less than one in order to approve the loan.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

18

As long as overall cash flow growth is positive,a bank loan officer would not be concerned if cash flow from operations was projected to be negative over the term of the loan.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

19

A rising sales to working capital ratio may indicate a potential borrower is using its net current assets more efficiently.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

20

Residential mortgage loan applications have the most diverse application processes that differ from one institution to the other.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

21

Which one of the following five Cs of credit is NOT correctly defined?

A)Capacity-Whether the borrower has enough other credit available to pay off the loan in the event of cash flow problems.

B)Capital-The borrower's equity.

C)Character-A measure of the borrower's intention/willingness to repay the loan.

D)Conditions-Assessing how economic conditions could affect the borrower's ability to repay the loan.

E)Collateral-An asset of the borrower that the lender may seize in the event of default on the loan.

A)Capacity-Whether the borrower has enough other credit available to pay off the loan in the event of cash flow problems.

B)Capital-The borrower's equity.

C)Character-A measure of the borrower's intention/willingness to repay the loan.

D)Conditions-Assessing how economic conditions could affect the borrower's ability to repay the loan.

E)Collateral-An asset of the borrower that the lender may seize in the event of default on the loan.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

22

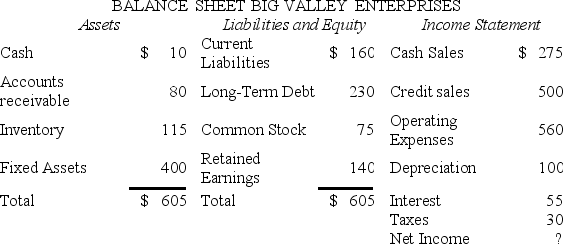

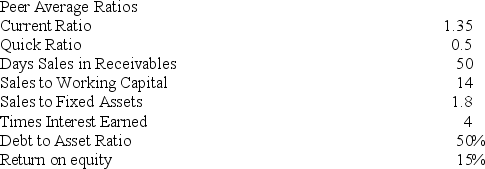

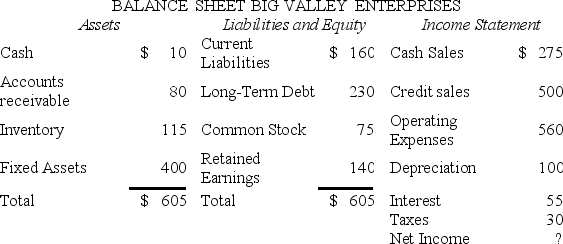

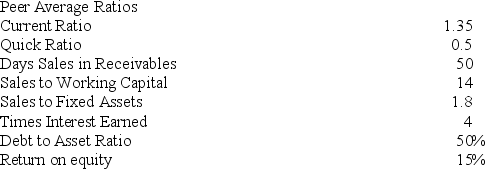

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Big Valley's fixed asset efficiency score is ________ which is ________that of the typical firm in the industry.

A)1.8; the same as

B)1.54; lower than

C)1.94; higher than

D)2.15; higher than

E)1.32; lower than

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

23

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Big Valley's use of debt to finance assets indicates that Big Valley has ________ the typical firm in the industry.

A)more long-term solvency risk than

B)the same long-term solvency risk as

C)less interest expense than

D)less long-term solvency risk than

E)a lower market value of equity to book value of equity ratio than

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

24

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Big Valley's return on equity indicates that the firm generates a ________ return to their shareholders than their peers.

A)2.04 percent higher

B)3.02 percent higher

C)15.25 percent higher

D)5.75 percent lower

E)1.05 percent lower

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

25

________ is the process of taking possession of the mortgaged property to satisfy the debt in the event of failure to repay the mortgage and foregoing claim to any deficiency.

A)Perfecting collateral

B)Foreclosure

C)Power of sale

D)Conditions precedent

E)Lien enforcement

A)Perfecting collateral

B)Foreclosure

C)Power of sale

D)Conditions precedent

E)Lien enforcement

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

26

GDS cutoff: 30 percent

TDS cutoff: 35 percent

Using only the TDS criteria,which one of the following statements is true?

A)Joe gets the loan,but Bill does not.

B)Bill gets the loan,but Joe does not.

C)Both get the loan.

D)Neither gets the loan.

E)The bank does not have money to make the loan.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

27

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Big Valley's current ratio indicates that Big Valley is ________ liquid than the typical firm in the industry,and Big Valley's quick ratio indicates that Big Valley is ________ liquid than the typical firm.

A)more; more

B)more; less

C)less; less

D)less; more

E)similar; similar

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

28

Nonperforming loans are loans that are past due ________ that are not accruing interest.

A)30 days

B)60 days

C)90 days

D)120 days

E)180 days

A)30 days

B)60 days

C)90 days

D)120 days

E)180 days

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

29

A corporate loan applicant has cash of $40,receivables of $50,and inventory of $20. The applicant also has current debts of $65. If the bank's policy requires a current ratio of 1.75 or better and an acid test ratio of 1.25 or better,would the applicant receive the loan?

A)Yes,because the applicant's current ratio and acid test ratios are acceptable.

B)No,because the applicant's current ratio and acid test ratios are both unacceptable.

C)No,because although the applicant's current ratio is acceptable,its acid test ratio is not.

D)No,because although the applicant's acid test ratio is acceptable,its current ratio is not.

E)Yes,because the bank will make the loan regardless of the results.

A)Yes,because the applicant's current ratio and acid test ratios are acceptable.

B)No,because the applicant's current ratio and acid test ratios are both unacceptable.

C)No,because although the applicant's current ratio is acceptable,its acid test ratio is not.

D)No,because although the applicant's acid test ratio is acceptable,its current ratio is not.

E)Yes,because the bank will make the loan regardless of the results.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

30

A corporate customer obtains a $1.5 million loan from a bank. The customer agrees to pay a 6.25 percent interest rate and agrees to make compensating balances of 4 percent of the loan amount. These will be held in noninterest-bearing transactions deposits at the bank for one year. The bank charges a 1 percent loan origination fee on the amount borrowed. Reserve requirements are 10 percent. What is the expected rate of return to the bank (k)(to the nearest basis point)?

A)6.95 percent

B)7.52 percent

C)7.99 percent

D)8.01 percent

E)8.45 percent

A)6.95 percent

B)7.52 percent

C)7.99 percent

D)8.01 percent

E)8.45 percent

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

31

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Big Valley is collecting their receivables about ________ than the typical firm.

A)22 percent more quickly

B)12 percent more quickly

C)17 percent more slowly

D)12 percent more slowly

E)16 percent more quickly

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

32

A firm with a low Z-score has high

A)insolvency risk.

B)interest rate risk.

C)liquidity risk.

D)international risk.

E)None of these options are correct.

A)insolvency risk.

B)interest rate risk.

C)liquidity risk.

D)international risk.

E)None of these options are correct.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

33

Individual credit-scoring models typically include all of the following information except

A)income.

B)length of time in residence.

C)credit history.

D)age.

E)ethnic background.

A)income.

B)length of time in residence.

C)credit history.

D)age.

E)ethnic background.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

34

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Altman's Z-score model is Z = 1.2X1 + 1.4X2 + 3.3X3 + 0.6X4 + 1.0X5.

X1 = Working Capital/Total Assets

X2 = Retained Earnings/Total Assets

X3 = EBIT/Total Assets

X4 = Market Value Equity/Book Value Long-Term Debt

X5 = Sales/Total Assets

Using the Altman's Z model,Big Valley's Z-score is

A)3.22.

B)2.88.

C)2.65.

D)2.11.

E)1.85.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

35

The base loan rate accounts for

I. the FI's weighted average cost of capital.

II. the FI's marginal cost of funds.

III. the credit risk of the loan.

A)I only

B)I and II only

C)II and III only

D)I and III only

E)I,II,and III

I. the FI's weighted average cost of capital.

II. the FI's marginal cost of funds.

III. the credit risk of the loan.

A)I only

B)I and II only

C)II and III only

D)I and III only

E)I,II,and III

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

36

In analyzing credit risk for a loan to a major diversified corporation,the bank typically has which of the following advantages?

I. Market-based models to analyze credit risk

II. Greater negotiating power due to the size of the loan required

III. Ratings agency measures of default risk

A)I only

B)I and II only

C)II and III only

D)I and III only

E)I,II,and III

I. Market-based models to analyze credit risk

II. Greater negotiating power due to the size of the loan required

III. Ratings agency measures of default risk

A)I only

B)I and II only

C)II and III only

D)I and III only

E)I,II,and III

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

37

Which one of the following is usually the better predictor of default?

A)Standard & Poor's credit rating

B)Moody's credit rating

C)Altman Z-score

D)Moody's Analytics EDF

E)All of these choices are correct.

A)Standard & Poor's credit rating

B)Moody's credit rating

C)Altman Z-score

D)Moody's Analytics EDF

E)All of these choices are correct.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

38

Interest is Big Valley's only fixed cash charge.

Big Valley's market value of equity to book value of debt ratio = 1.5.

Big Valley has a times interest earned ratio that is ________,which indicates that Big Valley has ________ long-term insolvency risk than the typical firm in the industry.

A)4; the same

B)3.91; less

C)3.91; more

D)4.58; more

E)4.58; less

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

39

GDS cutoff: 30 percent

TDS cutoff: 35 percent

Using only the GDS criteria,which one of the following statements is true?

A)Joe gets the loan,but Bill does not.

B)Bill gets the loan,but Joe does not.

C)Both get the loan.

D)Neither gets the loan.

E)The bank does not have money to make the loan.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

40

Mid-market commercial lending may be typically defined as borrowers

I. with sales revenue between $5 million and $100 million.

II. with a recognizable corporate structure.

III. with ready access to deep and liquid capital markets.

A)I only

B)II only

C)III only

D)I and II only

E)I,II,and III

I. with sales revenue between $5 million and $100 million.

II. with a recognizable corporate structure.

III. with ready access to deep and liquid capital markets.

A)I only

B)II only

C)III only

D)I and II only

E)I,II,and III

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

41

Based on an option valuation method,the EDF model:

A)determine if the equity is mispriced.

B)calculate the market value of the lender's investment.

C)estimates the probability that a firm will default over a specified period of time.

D)estimate the likelihood that the Z-score model is correct.

E)estimates the probability that the firm's rating will change over a period of time.

A)determine if the equity is mispriced.

B)calculate the market value of the lender's investment.

C)estimates the probability that a firm will default over a specified period of time.

D)estimate the likelihood that the Z-score model is correct.

E)estimates the probability that the firm's rating will change over a period of time.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

42

The conditions specified in a credit agreement that must be fulfilled before a drawdown is allowed are called

A)collateral perfection.

B)power of sale conditions.

C)conditions precedent.

D)foreclosure agreements.

E)audit review terms.

A)collateral perfection.

B)power of sale conditions.

C)conditions precedent.

D)foreclosure agreements.

E)audit review terms.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

43

A bank is using the RAROC to evaluate large business loans. The benchmark rate of return is 7.55 percent. The one-year loan interest rate is 8.00 percent and the bank must pay 7.40 percent to raise the funds. The cost to service the loan is 0.3 percent. If the loan defaults,92 percent of the money lent will be lost. Based on historical default rates,the extreme worst-case loss scenario is about 5 percent. Should the bank make the loan? Why or why not?

A)Yes,because the RAROC is 7.11 percent.

B)No,because the RAROC is 7.11 percent.

C)Yes,because the RAROC is 6.52 percent.

D)No,because the RAROC is 6.52 percent.

E)No,because the RAROC is more than 7.55 percent.

A)Yes,because the RAROC is 7.11 percent.

B)No,because the RAROC is 7.11 percent.

C)Yes,because the RAROC is 6.52 percent.

D)No,because the RAROC is 6.52 percent.

E)No,because the RAROC is more than 7.55 percent.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

44

Explain what each ratio in the Altman credit model measures and explain why higher values of each of the variables predict lower default probability.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

45

For most business loans,growing earnings are not a sufficient reason to grant a loan. Why?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

46

The ratio that measures the firm's efficiency in utilizing its assets to generate revenue is:

A)Current ratio

B)Debt ratio

C)Time interest earned ratio

D)Total Assets turnover ratio

E)Cash-flow-to-debt ratio

A)Current ratio

B)Debt ratio

C)Time interest earned ratio

D)Total Assets turnover ratio

E)Cash-flow-to-debt ratio

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

47

In concept,the RAROC measure indicates a loan is acceptable if the RAROC is greater than the

A)borrower's ROE.

B)lender's ROA.

C)borrower's ROA.

D)lender's ROE.

E)NCO rate.

A)borrower's ROE.

B)lender's ROA.

C)borrower's ROA.

D)lender's ROE.

E)NCO rate.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

48

Explain the purpose/benefits in adding a credit-scoring model to evaluate a loan application.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

49

Which ratio measures the firm's ability to pay current interest and lease payments?

A)Current ratio

B)Debt ratio

C)Time interest earned ratio

D)Total Assets turnover ratio

E)Cash-flow-to-debt ratio

A)Current ratio

B)Debt ratio

C)Time interest earned ratio

D)Total Assets turnover ratio

E)Cash-flow-to-debt ratio

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

50

Explain how the Moody's Analytics Model predicts bankruptcy probability.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

51

What are the five Cs of credit? Briefly describe each.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

52

A corporate loan applicant has had a growing cash account for the last three years,but cash flow from operations has been negative in every year. Would this concern you if you were the loan officer charged with approving the loan? If so,why? If not,why not?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

53

If you were a loan officer evaluating a small business credit application for a loan and you wanted to ensure that the applicant had more than sufficient cash flow to pay off its existing debt,the applicant's cash-flow-to-debt ratio would have to be greater than

A)one.

B)zero.

C)the TIE ratio.

D)the interest rate on the debt.

E)peer average ratio.

A)one.

B)zero.

C)the TIE ratio.

D)the interest rate on the debt.

E)peer average ratio.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

54

Why won't a loan officer usually approve a loan solely on the basis of collateral?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

55

Business credit-scoring models suffer from several weaknesses. These include which of the following?

I. Credit-score models are not statistically sound tools to use in making a lending decision.

I. The appropriate weights on a credit-score model are likely to change unpredictably over time.

II. These models ignore non-quantifiable behavioral factors,such as a relationship with the bank and reputation.

IV. Credit-scoring models discriminate against minorities.

A)I and II only

B)II and III only

C)II,III,and IV only

D)I,II,and III only

E)I,II,III,and IV

I. Credit-score models are not statistically sound tools to use in making a lending decision.

I. The appropriate weights on a credit-score model are likely to change unpredictably over time.

II. These models ignore non-quantifiable behavioral factors,such as a relationship with the bank and reputation.

IV. Credit-scoring models discriminate against minorities.

A)I and II only

B)II and III only

C)II,III,and IV only

D)I,II,and III only

E)I,II,III,and IV

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

56

A bank charges a commercial borrower a 6.55 percent interest rate on a one-year loan. The bank also charges a 0.5 percent origination fee and requires compensating balances of 7 percent in the form of demand deposits. Reserve requirements are 10 percent. What is the promised gross rate of return on the loan?

A)8.45 percent

B)7.89 percent

C)9.10 percent

D)7.52 percent

E)6.95 percent

A)8.45 percent

B)7.89 percent

C)9.10 percent

D)7.52 percent

E)6.95 percent

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

57

Before allowing the borrower to actually acquire the funds for a mid-market collateralized loan,what must the lender ensure? What type of monitoring occurs by the lender after the loan is granted?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

58

A $40,000 one-year loan with a 1 percent origination fee and a 7.50 percent interest rate is funded with money on which the bank owes 3 percent. What is the expected pretax dollar spread on the loan? If the bank needs to net at least 3.5 percent on the funds lent to make its ROE,how many dollars can the bank spend on credit investigation,loan servicing,and so forth? Would the bank be able to spend more if the loan amount was greater? What does this example suggest about credit analysis?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

59

Describe the credit analysis process for a mid-market corporate loan applicant.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

60

As a business lender,you would prefer that the borrower have stable or growing cash flows resulting from which part of the statement of cash flows?

A)Financing cash flows

B)Cash flows from investment

C)Operating cash flows

D)Dividends

E)Common Stock

A)Financing cash flows

B)Cash flows from investment

C)Operating cash flows

D)Dividends

E)Common Stock

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

61

Why is bank lending to large corporations more difficult than making loans to small or mid-size firms? What additional factors are involved? Do banks have some additional tools to help in assessing credit risk of large firms? What are some examples?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

62

A bank can charge a corporate borrower 6.25 percent on a loan. The borrower is asking for a $600,000 loan. The extreme loss rate on this loan type is 4.0 percent and,when default occurs,about 15 percent of the loan amount is recovered. The interest and noninterest cost of the loan is 5.85 percent. What is the RAROC of the loan? Under what circumstances should the bank make the loan?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

63

A bank has a base loan rate of 4.75 percent and for the loan under consideration it would apply a 2 percent risk premium. The bank also requires compensating balances (noninterest-bearing)equal to 5 percent of the loan amount. The bank's reserve requirements are 10 percent. The bank charges 1 percent of the loan amount as an origination fee. The borrower is asking for a $500,000 loan. Calculate the ROA on the loan.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 63 flashcards in this deck.