Deck 24: Statement of Cash Flows

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

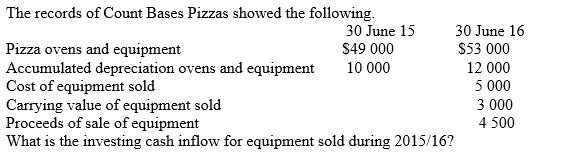

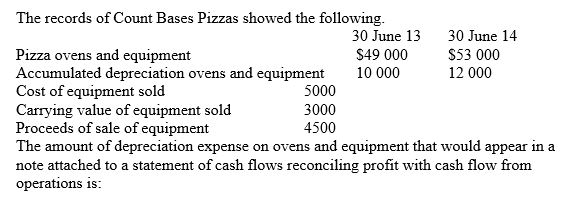

A) Carrying value of equipment sold $3000

B) Equipment sold $4000

C) Proceeds of sale of equipment $4500

D) Cost of equipment sold $5000

Question

Question

Question

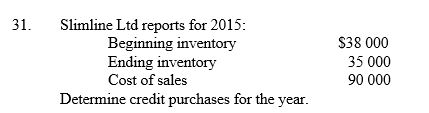

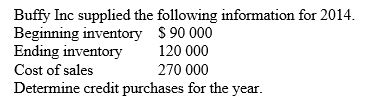

A) $87 000

B) $90 000

C) $93 000

D) $125 000

Question

Question

Question

B

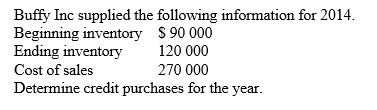

A) $300 000

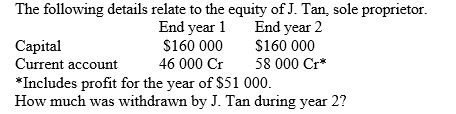

B) $270 000

C) $330 000

D) $420 000

A) $300 000

B) $270 000

C) $330 000

D) $420 000

Question

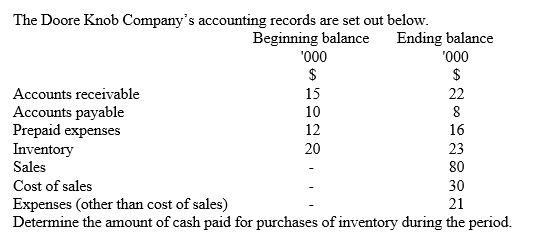

A) $25 000

B) $29 000

C) $35 000

D) $33 000

Question

A) $2000.

B) $4000.

C) $3000.

D) $5000.

Question

B

A) Equipment purchased $4000

B) Equipment purchased $9000

C) Equipment purchased $5000

D) Equipment purchased $3000

A) Equipment purchased $4000

B) Equipment purchased $9000

C) Equipment purchased $5000

D) Equipment purchased $3000

Question

Question

Question

A) $117 000

B) $120 000

C) $123 000

D) $144 000

Question

Question

Question

Question

Question

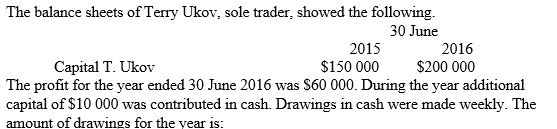

A) $40 000.

B) $60 000.

C) $20 000.

D) $50 000.

Question

A) $94 000

B) $100 000

C) $106 000

D) Unable to be calculated

Question

A) $12 000

B) $39 000

C) $63 000

D) Cannot be calculated from the information provided

Question

Question

A) $195 000.

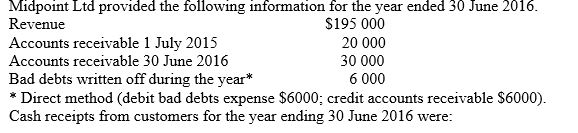

B) $179 000.

C) $185 000.

D) $191 000.

Question

Question

Question

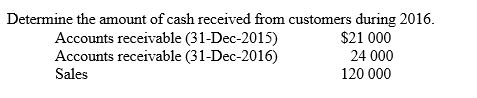

A) $2000

B) $26 000

C) $24 000

D) $28 000

Question

Question

A) $89 000.

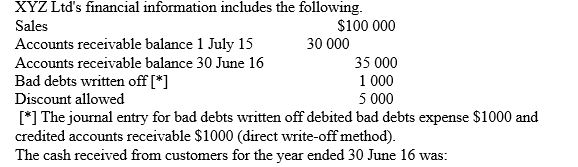

B) $91 000.

C) $94 000.

D) $101 000.

Question

A) $4000

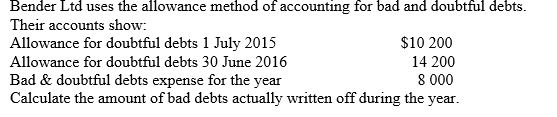

B) $11 000

C) $8000

D) $6200

Question

Question

Question

Question

Question

Question

Question

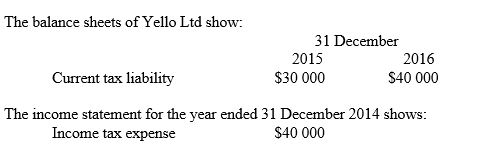

What amount in respect of income tax will appear in the statement of cash flows for the year ended 31 December 2016, assuming tax is paid annually in arrears and there are no over or under provisions of tax.

What amount in respect of income tax will appear in the statement of cash flows for the year ended 31 December 2016, assuming tax is paid annually in arrears and there are no over or under provisions of tax.A) Nil

B) $30 000

C) $40 000

D) $70 000

Question

Question

Question

Question

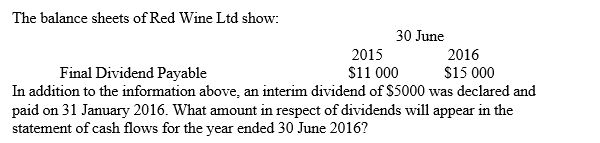

A) $5000

B) $15 000

C) $16 000

D) $20 000

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/65

Play

Full screen (f)

Deck 24: Statement of Cash Flows

1

A firm reported that accounts receivable increased by $30 000 between the current and the prior year. If accrual-basis sales were $200 000 the amount of cash received from customers during the year was:

A) $200 000.

B) $230 000.

C) $170 000.

D) $30 000.

A) $200 000.

B) $230 000.

C) $170 000.

D) $30 000.

C

2

When an annual statement of cash flows is prepared the sum of the three major components, operating activities, investing activities and financing activities, add up to:

A) the ending working capital.

B) the change in the cash at bank account balance over the year.

C) the ending cash at bank account balance.

D) profit for the period.

A) the ending working capital.

B) the change in the cash at bank account balance over the year.

C) the ending cash at bank account balance.

D) profit for the period.

B

3

Which of these classifications is used in the statement of cash flows?

A) Selling activities

B) Administrative activities

C) Borrowing activities

D) Operating activities

A) Selling activities

B) Administrative activities

C) Borrowing activities

D) Operating activities

D

4

Which of these are methods that are used to prepare a statement of cash flows?

I) Use information obtained directly from the primary records of cash transactions.

Ii) Use the information in the accrual-based income statement and balance sheets but remove the effect of non-cash items.

Iii) Use the information in the accrual-based income statement and balance sheets but add the effect of non-cash items.

A) iii

B) ii. iii

C) i

D) i. ii

I) Use information obtained directly from the primary records of cash transactions.

Ii) Use the information in the accrual-based income statement and balance sheets but remove the effect of non-cash items.

Iii) Use the information in the accrual-based income statement and balance sheets but add the effect of non-cash items.

A) iii

B) ii. iii

C) i

D) i. ii

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

5

In IAS 7/AASB 107, short-term, highly liquid investments that are readily convertible into known amounts of cash and that are subject to an insignificant risk of change in value, are known as:

A) cash.

B) cash equivalents.

C) accounts receivable.

D) bills of exchange.

A) cash.

B) cash equivalents.

C) accounts receivable.

D) bills of exchange.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

6

The accounting standard dealing with the statement of cash flows is:

A) IAS 7/AASB 107.

B) IAS 1/AASB 1001.

C) IAS/19/AASB 1019.

D) IAS 18/AASB 118.

A) IAS 7/AASB 107.

B) IAS 1/AASB 1001.

C) IAS/19/AASB 1019.

D) IAS 18/AASB 118.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

7

Which statement concerning the treatment of the purchase and sale of non-current assets in a statement of cash flows is incorrect?

A) The carrying value of a non-current asset that has been sold is treated as an investing outflow.

B) The proceeds of sale from a non-current asset are treated as an investing inflow.

C) The cash purchase of a non-current asset is treated as an investing outflow.

D) Inflows and outflows for the purchase and sale of non-current assets must not be netted off against each other.

A) The carrying value of a non-current asset that has been sold is treated as an investing outflow.

B) The proceeds of sale from a non-current asset are treated as an investing inflow.

C) The cash purchase of a non-current asset is treated as an investing outflow.

D) Inflows and outflows for the purchase and sale of non-current assets must not be netted off against each other.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

8

The 'bottom line' in the profit or loss statement is profit. The 'bottom line' in the statement of cash flows is:

A) cash flow from operations.

B) net increase (decrease) in the cash balance over the period.

C) net cash at the end of the year.

D) net cash at the beginning of the year.

A) cash flow from operations.

B) net increase (decrease) in the cash balance over the period.

C) net cash at the end of the year.

D) net cash at the beginning of the year.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

9

All of these are requirements of IAS 7/AASB 107, except:

A) gross cash flows, rather than net flows, are to be reported.

B) comparative figures for the previous year must be provided as well as current year figures.

C) a note reconciling gross profit with cash paid for cost of sales is to be provided.

D) the net increase or decrease in cash held must be reconciled with the cash items appearing in the balance sheet.

A) gross cash flows, rather than net flows, are to be reported.

B) comparative figures for the previous year must be provided as well as current year figures.

C) a note reconciling gross profit with cash paid for cost of sales is to be provided.

D) the net increase or decrease in cash held must be reconciled with the cash items appearing in the balance sheet.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

10

Which statement concerning the concept of cash adopted by IAS 7/AASB 107 is incorrect?

A) Transfers between items included in the definition of cash and cash equivalents are not reported in the statement of cash flows.

B) As a general rule liquid investments with a term of three month or less, with insignificant risk of changes in value, fall within the definition of cash or cash equivalents.

C) Accounts receivable are generally included in the definition of cash and cash equivalents.

D) Depending on the conditions that apply, a bank overdraft may be treated as a financing activity.

A) Transfers between items included in the definition of cash and cash equivalents are not reported in the statement of cash flows.

B) As a general rule liquid investments with a term of three month or less, with insignificant risk of changes in value, fall within the definition of cash or cash equivalents.

C) Accounts receivable are generally included in the definition of cash and cash equivalents.

D) Depending on the conditions that apply, a bank overdraft may be treated as a financing activity.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

11

The primary purpose of a statement of cash flows is to provide information about:

A) profit.

B) long-term financial position.

C) gross profit.

D) cash inflows and cash outflows.

A) profit.

B) long-term financial position.

C) gross profit.

D) cash inflows and cash outflows.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

12

How many of these would be classified as investing activities on a statement of cash flows?

Purchase of a computer

Issue of debentures

Sale of land

Payment of dividends

A) One

B) Two

C) Three

D) Four

Purchase of a computer

Issue of debentures

Sale of land

Payment of dividends

A) One

B) Two

C) Three

D) Four

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

13

IAS 7/AASB 107 defines activities that relate to changes in the size and composition of the financial structure of an entity as:

A) borrowing activities.

B) investing activities.

C) financing activities.

D) share capital and reserves.

A) borrowing activities.

B) investing activities.

C) financing activities.

D) share capital and reserves.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

14

What effect does this journal entry have on cash flows?

Dr Depreciation expense $88 200

Cr Accumulated depreciation $88 200

A) Increase outflows

B) Decrease outflows

C) No effect on outflows or inflows

D) Decrease inflows

Dr Depreciation expense $88 200

Cr Accumulated depreciation $88 200

A) Increase outflows

B) Decrease outflows

C) No effect on outflows or inflows

D) Decrease inflows

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

15

For a dairy farmer which of these is not an operating cash outflow?

A) Payment of GST

B) Payment of wages

C) Payment to suppliers

D) Payment for the purchase of land

A) Payment of GST

B) Payment of wages

C) Payment to suppliers

D) Payment for the purchase of land

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

16

Under IAS 7/AASB 107 how many of these items is required to be disclosed in a note attached to the statement of cash flows?

A reconciliation of cash and cash equivalents with the items reported in the balance sheet.

A reconciliation of net cash from operating activities with profit after income tax.

Details of cash flows from the acquisition and disposal of subsidiaries.

A) 0

B) 1

C) 2

D) 3

A reconciliation of cash and cash equivalents with the items reported in the balance sheet.

A reconciliation of net cash from operating activities with profit after income tax.

Details of cash flows from the acquisition and disposal of subsidiaries.

A) 0

B) 1

C) 2

D) 3

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is not classified as a financing activity by IAS 7/AASB 107?

A) Dividends paid to shareholders

B) The sale of shares that have been held as an investment

C) The issue of shares by a company to raise capital

D) Repayment of borrowings

A) Dividends paid to shareholders

B) The sale of shares that have been held as an investment

C) The issue of shares by a company to raise capital

D) Repayment of borrowings

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

18

The primary purpose of a statement of cash flows is to provide information about:

A) assets and liabilities.

B) profitability.

C) cash inflows and cash outflows.

D) working capital.

A) assets and liabilities.

B) profitability.

C) cash inflows and cash outflows.

D) working capital.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

19

Which assertion relating to the statement of cash flows is incorrect?

A) Cash flows from one activity are not normally offset against cash flows from a different activity.

B) GST is not included anywhere in the statement of cash flows.

C) Cash outflows are shown in brackets.

D) The statement is headed 'for the period ended'.

A) Cash flows from one activity are not normally offset against cash flows from a different activity.

B) GST is not included anywhere in the statement of cash flows.

C) Cash outflows are shown in brackets.

D) The statement is headed 'for the period ended'.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

20

How would the purchase of government bonds by a golf club be reported in the statement of cash flows?

A) Investing outflow

B) Investing inflow

C) Financing outflow

D) Financing inflow

A) Investing outflow

B) Investing inflow

C) Financing outflow

D) Financing inflow

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

21

A) Carrying value of equipment sold $3000

B) Equipment sold $4000

C) Proceeds of sale of equipment $4500

D) Cost of equipment sold $5000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

22

From the following information, determine the amount of cash received from customers during 2014.

Accounts receivable (31-Dec-2013) $63 000

Accounts receivable (31-Dec-2014) 54 000

Sales 270 000

A) $171 000

B) $189 000

C) $261 000

D) $279 000

Accounts receivable (31-Dec-2013) $63 000

Accounts receivable (31-Dec-2014) 54 000

Sales 270 000

A) $171 000

B) $189 000

C) $261 000

D) $279 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

23

The statement of profit or loss shows interest revenue for the year of $31 000 and the balance sheet show interest receivable at the beginning of the year of $3000 and at the end of the year of $4000. Determine the amount of interest received in cash for the year.

A) $31 000

B) $32 000

C) $30 000

D) $33 000

A) $31 000

B) $32 000

C) $30 000

D) $33 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

24

A) $87 000

B) $90 000

C) $93 000

D) $125 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

25

If cost of sales is $500 000, inventory has increased by $8000 and creditors have decreased by $15 000 what is the amount of cash paid for the purchase of goods for resale?

A) $500 000

B) $507 000

C) $523 000

D) $493 000

A) $500 000

B) $507 000

C) $523 000

D) $493 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

26

The ledger account for buildings had a balance of $520 000 at the beginning of the year and a balance of $750 000 at the end of the year. If the buildings have been revalued upwards by $100 000 during the year what is the investing outflow for the period, for buildings, assuming no buildings were sold?

A) $130 000

B) $230 000

C) $750 000

D) $100 000

A) $130 000

B) $230 000

C) $750 000

D) $100 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

27

B

A) $300 000

B) $270 000

C) $330 000

D) $420 000

A) $300 000

B) $270 000

C) $330 000

D) $420 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

28

A) $25 000

B) $29 000

C) $35 000

D) $33 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

29

A) $2000.

B) $4000.

C) $3000.

D) $5000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

30

B

A) Equipment purchased $4000

B) Equipment purchased $9000

C) Equipment purchased $5000

D) Equipment purchased $3000

A) Equipment purchased $4000

B) Equipment purchased $9000

C) Equipment purchased $5000

D) Equipment purchased $3000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

31

When preparing the note attached to the cash flow statement reconciling profit and cash flow from operations, proceeds from the disposal of non-current assets are:

A) added back to the profit.

B) sometimes added back to the profit and sometimes subtracted from the profit depending on whether a loss or profit on disposal is incurred.

C) subtracted from the profit.

D) do not appear in the reconciliation.

A) added back to the profit.

B) sometimes added back to the profit and sometimes subtracted from the profit depending on whether a loss or profit on disposal is incurred.

C) subtracted from the profit.

D) do not appear in the reconciliation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

32

The statement of profit or loss of Zang Co shows accrual-basis interest income for the year ended 30 June 2016 as $400. The comparative balance sheets show that interest receivable at 30 June 2015 and 30 June 2016 was $45 and $80 respectively. Determine the amount of cash received by way of interest during the year.

A) $45

B) $365

C) $400

D) $435

A) $45

B) $365

C) $400

D) $435

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

33

A) $117 000

B) $120 000

C) $123 000

D) $144 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

34

If wages expense is $350 000, wages accrued at the beginning of the period are $3600 and wages accrued at the end of the period are $5600 what amount for wages paid will appear in the statement of cash flows?

A) $350 000

B) $359 200

C) $348 000

D) $352 000

A) $350 000

B) $359 200

C) $348 000

D) $352 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

35

During the year a firm reported that accounts receivable had increased by $35 000. If accrual basis sales were $200 000 the amount of cash received from customers during the year must have been:

A) $165 000.

B) $190 000.

C) $210 000.

D) $235 000.

A) $165 000.

B) $190 000.

C) $210 000.

D) $235 000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

36

Under IAS 7/AASB 107 which of these needs to be disclosed in the notes attached to the statement of cash flows?

A) Standby credit arrangements

B) The closing bank balance

C) The opening bank balance

D) Proceeds from a share issue

A) Standby credit arrangements

B) The closing bank balance

C) The opening bank balance

D) Proceeds from a share issue

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

37

John Co had a cost of sales, during the year just ended, of $280 000. During the year accounts payable and inventory each increased by $12 000. What amount of cash was paid for purchases during the year?

A) $256 000

B) $268 000

C) $280 000

D) $292 000

A) $256 000

B) $268 000

C) $280 000

D) $292 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

38

A) $40 000.

B) $60 000.

C) $20 000.

D) $50 000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

39

A) $94 000

B) $100 000

C) $106 000

D) Unable to be calculated

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

40

A) $12 000

B) $39 000

C) $63 000

D) Cannot be calculated from the information provided

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

41

A statement of cash flows is being prepared using accrual based information. In calculating cash receipts from customers' bad debts written off, when the direct write- off method is used is:

A) added to accrual-basis revenue.

B) not adjusted.

C) subtracted from accrual-basis revenue.

D) shown as a cash outgoing.

A) added to accrual-basis revenue.

B) not adjusted.

C) subtracted from accrual-basis revenue.

D) shown as a cash outgoing.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

42

A) $195 000.

B) $179 000.

C) $185 000.

D) $191 000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

43

For a statement of cash flows, when preparing the note reconciling a net loss and cash flow from operations, depreciation is:

A) added back to the net loss.

B) subtracted from net loss.

C) does not appear in the reconciliation.

D) appears as part of the profit figure.

A) added back to the net loss.

B) subtracted from net loss.

C) does not appear in the reconciliation.

D) appears as part of the profit figure.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

44

How many of these are non-cash transactions?

Expense for impairment of goodwill

A share dividend

A discount allowed

A bad debt write-off

A) 1

B) 2

C) 3

D) 4

Expense for impairment of goodwill

A share dividend

A discount allowed

A bad debt write-off

A) 1

B) 2

C) 3

D) 4

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

45

A) $2000

B) $26 000

C) $24 000

D) $28 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

46

Given the following information, calculate the net cash from operating activities for the period.

Profit $780 000

Accounts receivable decreased by 5000

Proceeds from the sale of equipment 34 000

Inventory increased by 22 000

Depreciation expense 36 000

Carrying value of equipment sold 1000

A) $832 000

B) $766 000

C) $810 000

D) $805 000

Profit $780 000

Accounts receivable decreased by 5000

Proceeds from the sale of equipment 34 000

Inventory increased by 22 000

Depreciation expense 36 000

Carrying value of equipment sold 1000

A) $832 000

B) $766 000

C) $810 000

D) $805 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

47

A) $89 000.

B) $91 000.

C) $94 000.

D) $101 000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

48

A) $4000

B) $11 000

C) $8000

D) $6200

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

49

Assume tax is paid annually in a lump sum. The beginning balance in the current tax liability account is $70 000 and the ending balance is $79 000. There was no under or over provision of tax for the year. What is the amount of tax paid to be included in the statement of cash flows for the period?

A) Nil

B) $70 000

C) $80 000

D) $79 000

A) Nil

B) $70 000

C) $80 000

D) $79 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

50

Which of these is a transaction that would be reported in the statement of cash flows itself rather than in the notes?

A) A bonus share issue

B) Amortisation of goodwill

C) Interim dividend paid

D) The acquisition of another entity by means of a share issue

A) A bonus share issue

B) Amortisation of goodwill

C) Interim dividend paid

D) The acquisition of another entity by means of a share issue

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

51

The accrual-basis tax expense in the income statement is $60 000, the beginning balance in the current tax liability account is $50 000 and the ending balance is $70 000. What is the amount of tax paid to be included in the statement of cash flows for the year?

A) $20 000

B) $40 000

C) $50 000

D) $60 000

A) $20 000

B) $40 000

C) $50 000

D) $60 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

52

When preparing the note reconciling profit/loss and cash flow from operations, depreciation is:

A) subtracted from a profit.

B) does not appear in the reconciliation.

C) added back to a loss.

D) added back to a profit.

A) subtracted from a profit.

B) does not appear in the reconciliation.

C) added back to a loss.

D) added back to a profit.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

53

Uri Ltd uses the allowance method of accounting for bad and doubtful debts. Bad and doubtful debts expense shown in the income statement is $7000 and the amount of bad debts actually written off is $5000. If sales are $330 000 and customer's balances have increased by $15 000 over the period, calculate the amount to be shown in the statement of cash flows for receipts from customers.

A) $330 000

B) $320 000

C) $310 000

D) $315 000

A) $330 000

B) $320 000

C) $310 000

D) $315 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

54

Given the following information for a recent financial period determine the net cash flow from operating activities. Use the indirect approach.

Accounts receivable decreased by $6000

Profit was $18 000

Depreciation was $2000

Prepaid expense decreased by $3000

A) $15 000

B) $18 000

C) $21 000

D) $29 000

Accounts receivable decreased by $6000

Profit was $18 000

Depreciation was $2000

Prepaid expense decreased by $3000

A) $15 000

B) $18 000

C) $21 000

D) $29 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

55

What amount in respect of income tax will appear in the statement of cash flows for the year ended 31 December 2016, assuming tax is paid annually in arrears and there are no over or under provisions of tax.A) Nil

B) $30 000

C) $40 000

D) $70 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

56

Discount allowed is a:

A) cash item that is included as an outflow in the statement of cash flows.

B) cash item that is adjusted in a note attached to the statement of cash flows.

C) non-cash items that is deducted from accrual based revenue and thus not included in the statement of cash flows.

D) cash item that is included as an inflow in the statement of cash flows.

A) cash item that is included as an outflow in the statement of cash flows.

B) cash item that is adjusted in a note attached to the statement of cash flows.

C) non-cash items that is deducted from accrual based revenue and thus not included in the statement of cash flows.

D) cash item that is included as an inflow in the statement of cash flows.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

57

According to AASB's Interpretation 1031, how many of these statements relating to the treatment of GST in the statement of cash flows are true?

All GST outlays and GST collections are regarded as effecting operating activities.

Cash flows from operating activities are reported at gross amounts inclusive of GST.

Cash flows from investing activities are shown net of GST, with GST on investing activities included as part of operating activities.

A) 0

B) 1

C) 2

D) 3

All GST outlays and GST collections are regarded as effecting operating activities.

Cash flows from operating activities are reported at gross amounts inclusive of GST.

Cash flows from investing activities are shown net of GST, with GST on investing activities included as part of operating activities.

A) 0

B) 1

C) 2

D) 3

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

58

In its most recent financial year the Arrow Ltd reported that Accounts payable increased $13 000; inventory decreased $6000; profit was $41 000 and depreciation expense was $5000. On the statement of cash flows, what is net cash flow from operating activities is? (Use the indirect approach.)

A) $53 000

B) $65 000

C) $43 000

D) $55 000

A) $53 000

B) $65 000

C) $43 000

D) $55 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

59

A) $5000

B) $15 000

C) $16 000

D) $20 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

60

Which statement is untrue?

A) The statement of cash flows can provide information about the causes of changes in the entity's cash position over the period.

B) Analysis of an entity's cash flow position requires an examination of trends in statement of cash flows items over several years.

C) The statement of cash flows can explain the effects of operating activities on the entity's cash position.

D) The statement of cash flows effectively duplicates the function of the cash budget.

A) The statement of cash flows can provide information about the causes of changes in the entity's cash position over the period.

B) Analysis of an entity's cash flow position requires an examination of trends in statement of cash flows items over several years.

C) The statement of cash flows can explain the effects of operating activities on the entity's cash position.

D) The statement of cash flows effectively duplicates the function of the cash budget.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

61

How many of these are limitations of a statement of cash flows?

Only past cash flows are reported

Cash flows can be manipulated,e.g. postponing expenditures

Non-cash transactions can be significant in affecting future investing and financing cash flows

A) 0

B) 1

C) 2

D) 3

Only past cash flows are reported

Cash flows can be manipulated,e.g. postponing expenditures

Non-cash transactions can be significant in affecting future investing and financing cash flows

A) 0

B) 1

C) 2

D) 3

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

62

Which statement concerning the indirect method of preparing a cash flow statement is true?

A) The indirect method is more costly to implement that the direct method.

B) The investing and financing sections of a cash flow statement differ depending on whether the direct or indirect method of preparation is used.

C) The direct, rather than the indirect method of preparation, is the method preferred by standard setters.

D) With the indirect method depreciation is deducted from profit to arrive at net cash from operating activities.

A) The indirect method is more costly to implement that the direct method.

B) The investing and financing sections of a cash flow statement differ depending on whether the direct or indirect method of preparation is used.

C) The direct, rather than the indirect method of preparation, is the method preferred by standard setters.

D) With the indirect method depreciation is deducted from profit to arrive at net cash from operating activities.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

63

How many of these are non-cash transactions or events?

Barter transaction

Purchase of a building partly financed by a mortgage

Takeover paid for with shares in the acquiring company

Credit sale

A) 1

B) 2

C) 3

D) 4

Barter transaction

Purchase of a building partly financed by a mortgage

Takeover paid for with shares in the acquiring company

Credit sale

A) 1

B) 2

C) 3

D) 4

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

64

Which statement concerning the interpretation of a statement of cash flows is untrue?

A) The statement of cash flows as required under IAS 7/AASB 107 only goes some of the way in enabling users to establish the liquidity/solvency position of an entity.

B) Ways in which cash flows can be manipulated include delaying cash payments and employing finance leases.

C) It is the indirect method rather than the direct method of preparation that is preferred by the standard setters.

D) The notes to the statement of cash flows are important in interpreting the firm's cash position.

A) The statement of cash flows as required under IAS 7/AASB 107 only goes some of the way in enabling users to establish the liquidity/solvency position of an entity.

B) Ways in which cash flows can be manipulated include delaying cash payments and employing finance leases.

C) It is the indirect method rather than the direct method of preparation that is preferred by the standard setters.

D) The notes to the statement of cash flows are important in interpreting the firm's cash position.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

65

Which of these is not a way in which cash flows may be manipulated?

A) Deferring repayment of debts

B) Charging excessive depreciation

C) Use of barter

D) Use of lease financing

A) Deferring repayment of debts

B) Charging excessive depreciation

C) Use of barter

D) Use of lease financing

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 65 flashcards in this deck.