Deck 21: Non-Current Assets: Revaluation, Disposal and Other Aspects

Full screen (f)

Question

Question

Question

Question

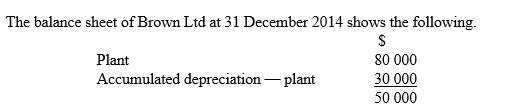

On 1 January 2015, based on a valuer's estimate of fair value, it was decided to revalue the plant to $65 000. The plant was then assessed to have a further useful life of 5 years and an expected residual amount of $5000. What is the journal entry in the books of Brown Ltd to record depreciation on plant on a straight-line basis for the half-year ending 30 June 2015 (balance date)?

On 1 January 2015, based on a valuer's estimate of fair value, it was decided to revalue the plant to $65 000. The plant was then assessed to have a further useful life of 5 years and an expected residual amount of $5000. What is the journal entry in the books of Brown Ltd to record depreciation on plant on a straight-line basis for the half-year ending 30 June 2015 (balance date)?A) Depreciation expense - plant 12 000 Accumulated depreciation- plant 12 000

B) Depreciation expense - plant 6 000 Accumulated depreciation - plant 6 000

C) Accumulated depreciation - plant 6 000 Depreciation expense - plant 6 000

D) Depreciation expense - plant 6 500 Accumulated depreciation- plant 6 500

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

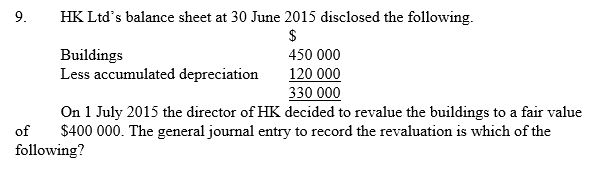

A) Debit gain on revaluation $70 000; credit buildings $70 000

B) Debit accumulated depreciation buildings $70 000; credit gain on revaluation $70 000

C) Debit accumulated depreciation buildings $120 000; credit gain on revaluation $70 000; credit buildings $50 000

D) Debit accumulated depreciation buildings $120 000; credit income account $70 000; credit buildings $50 000

Question

Question

Question

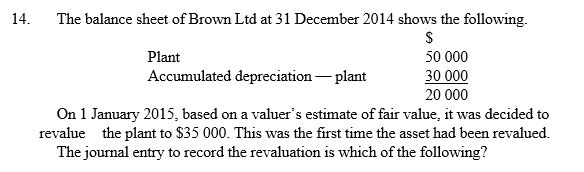

A) Accumulated depreciation - plant 30 000 Plant 15 000

Gain on revaluation plant 15 000

B) Plant 15 000 Gain on revaluation plant 15 000

C) Expense on revaluation of plant 15 000 Plant 15 000

D) Plant 15 000 Expense on revaluation of plant 15 000

Accumulated depreciation - plant 30 000

Question

Question

Question

Question

Question

Question

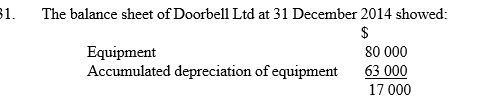

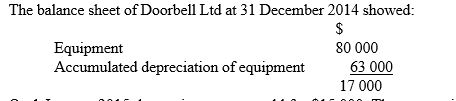

On 1 January 2015 the equipment was sold for $15 000. What is the accounting entry to record the receipt of the proceeds from the sale of the equipment?

On 1 January 2015 the equipment was sold for $15 000. What is the accounting entry to record the receipt of the proceeds from the sale of the equipment?A) Debit bank $15 000; credit proceeds from sale of equipment $15 000

B) Debit bank $17 000; credit proceeds from sale of equipment $17 000

C) Debit bank $15 000; credit equipment $15 000

D) Debit bank $2000; credit proceeds from sale of equipment $2000

Question

Question

Question

Question

Question

Question

Question

On 1 January 2015 the equipment was sold for $15 000. The accounting entry to record the closing of the equipment and the accumulated depreciation of equipment accounts is which of the following?

On 1 January 2015 the equipment was sold for $15 000. The accounting entry to record the closing of the equipment and the accumulated depreciation of equipment accounts is which of the following?A) Debit accumulated depreciation equipment $63 000; credit equipment $63 000

B) Debit accumulated depreciation equipment $63 000; debit carrying amount of equipment $17 000; credit equipment $80 000

C) Debit bank $15 000; credit carrying amount of equipment $15 000

D) Debit accumulated depreciation equipment $17 000; credit equipment $17 000

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

A) $7000.

B) $27 000.

C) $13 000.

D) $0.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/65

Play

Full screen (f)

Deck 21: Non-Current Assets: Revaluation, Disposal and Other Aspects

1

Under the accounting standard dealing with revaluations, IAS 16/AASB 116, an entity is required to:

A) adopt either a cost model or a revaluation model.

B) adopt a revaluation model.

C) adopt a cost model.

D) revalue its assets

A) adopt either a cost model or a revaluation model.

B) adopt a revaluation model.

C) adopt a cost model.

D) revalue its assets

A

2

What is the basic accounting entry for an initial revaluation decrease of a non-depreciable asset?

A) Debit expense on revaluation of asset; credit asset

B) Debit asset; credit expense on the revaluation of asset

C) Debit revaluation surplus reserve; credit asset

D) Debit asset; credit revaluation surplus reserve

A) Debit expense on revaluation of asset; credit asset

B) Debit asset; credit expense on the revaluation of asset

C) Debit revaluation surplus reserve; credit asset

D) Debit asset; credit revaluation surplus reserve

A

3

Accounting standard IAS 16/AASB 116 requires what basis of valuation to be used if assets are valued at other than cost?

A) Market value

B) Fair value

C) No basis of valuation is specified

D) The lower of cost and net realisable value

A) Market value

B) Fair value

C) No basis of valuation is specified

D) The lower of cost and net realisable value

B

4

On 1 January 2015, based on a valuer's estimate of fair value, it was decided to revalue the plant to $65 000. The plant was then assessed to have a further useful life of 5 years and an expected residual amount of $5000. What is the journal entry in the books of Brown Ltd to record depreciation on plant on a straight-line basis for the half-year ending 30 June 2015 (balance date)?A) Depreciation expense - plant 12 000 Accumulated depreciation- plant 12 000

B) Depreciation expense - plant 6 000 Accumulated depreciation - plant 6 000

C) Accumulated depreciation - plant 6 000 Depreciation expense - plant 6 000

D) Depreciation expense - plant 6 500 Accumulated depreciation- plant 6 500

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

5

Accounting standard IAS 16/AASB 116:

A) requires all assets to be revalued every five years.

B) requires all assets to be revalued every three years.

C) requires all assets to be revalued yearly.

D) does not require an entity to revalue its assets.

A) requires all assets to be revalued every five years.

B) requires all assets to be revalued every three years.

C) requires all assets to be revalued yearly.

D) does not require an entity to revalue its assets.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

6

Revaluations that occur must be upward or downward from an asset's:

A) carrying amount.

B) net realisable value.

C) lower of cost and net realisable value.

D) original cost.

A) carrying amount.

B) net realisable value.

C) lower of cost and net realisable value.

D) original cost.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

7

In accounting standard IAS 16/AASB 116 a downward revaluation is now known as a:

A) revaluation depletion.

B) revaluation increment.

C) revaluation decrease.

D) revaluation decrement.

A) revaluation depletion.

B) revaluation increment.

C) revaluation decrease.

D) revaluation decrement.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

8

How many of these are requirements of IAS 16/AASB 116?

An entire class of non-current assets must be revalued together.

If the revaluation model is adopted non-current assets should be revalued to either fair value or the value in use.

Before a depreciable asset is revalued accumulated depreciation should be written back to the asset account.

A) 0

B) 1

C) 2

D) 3

An entire class of non-current assets must be revalued together.

If the revaluation model is adopted non-current assets should be revalued to either fair value or the value in use.

Before a depreciable asset is revalued accumulated depreciation should be written back to the asset account.

A) 0

B) 1

C) 2

D) 3

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

9

FK Ltd's fleet of delivery trucks (original cost $850 000) had a carrying amount on 1 July 2012 of $470 000. On that date their value was revised to $500 000. Future depreciation charges will be based on which amount?

A) $450 000

B) $330 000

C) $500 000

D) $470 000

A) $450 000

B) $330 000

C) $500 000

D) $470 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

10

On 31 December 2014 Millwood Ltd's balance sheet shows motor vehicles at a cost price of $200 000 less accumulated depreciation $50 000. Millwood Ltd uses the cost model to value its assets. On 31 December 2014 an estimate is made that the recoverable amount of the vehicles is $120 000. Under IAS 36/AASB 136 the accounting entry to record the write down of the motor vehicles to recoverable amount is which of the following?

A) Dr Impairment loss on motor vehicles (expense) $80 000; Cr accumulated depreciation $80 000

B) Dr Impairment loss on motor vehicles (expense) $30 000; Cr accumulated depreciation and impairment losses $30 000

C) Dr Impairment loss on motor vehicles (expense) $30 000; Cr motor vehicles $30 000

D) No entry is required

A) Dr Impairment loss on motor vehicles (expense) $80 000; Cr accumulated depreciation $80 000

B) Dr Impairment loss on motor vehicles (expense) $30 000; Cr accumulated depreciation and impairment losses $30 000

C) Dr Impairment loss on motor vehicles (expense) $30 000; Cr motor vehicles $30 000

D) No entry is required

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

11

Which of these terms have the same meaning in accounting?

I) Carrying amount

Ii) Book value

Iii) Written down value

A) i, ii

B) ii, iii

C) i, iii

D) i, ii, iii

I) Carrying amount

Ii) Book value

Iii) Written down value

A) i, ii

B) ii, iii

C) i, iii

D) i, ii, iii

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

12

Which is the true statement?

A) A revaluation decrease should occur if a non-current asset's carrying amount is less than its fair value.

B) An initial revaluation decrease should be treated as a debit to the revaluation surplus reserve.

C) An initial revaluation decrease should be treated as a debit against the current period's profit or loss.

D) An initial revaluation decrease should be disclosed in the profit report as a reduction in other comprehensive income.

A) A revaluation decrease should occur if a non-current asset's carrying amount is less than its fair value.

B) An initial revaluation decrease should be treated as a debit to the revaluation surplus reserve.

C) An initial revaluation decrease should be treated as a debit against the current period's profit or loss.

D) An initial revaluation decrease should be disclosed in the profit report as a reduction in other comprehensive income.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

13

Under IAS 36/AASB 136 Impairment of Assets, how many of these statements are true?

When an asset's carrying amount is less than its recoverable amount the asset is said to suffer impairment.

Impairment losses are accounted for as a revaluation decrease if the revaluation model is used.

Impairment losses must be recognised as an expense in that period if the cost model is used.

A) 0

B) 1

C) 2

D) 3

When an asset's carrying amount is less than its recoverable amount the asset is said to suffer impairment.

Impairment losses are accounted for as a revaluation decrease if the revaluation model is used.

Impairment losses must be recognised as an expense in that period if the cost model is used.

A) 0

B) 1

C) 2

D) 3

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

14

A) Debit gain on revaluation $70 000; credit buildings $70 000

B) Debit accumulated depreciation buildings $70 000; credit gain on revaluation $70 000

C) Debit accumulated depreciation buildings $120 000; credit gain on revaluation $70 000; credit buildings $50 000

D) Debit accumulated depreciation buildings $120 000; credit income account $70 000; credit buildings $50 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

15

Which statement concerning revaluations that reverse prior adjustments in value is untrue?

A) A revaluation decrease that reverses a previous increase should be recognised as a decrease in other comprehensive income to the extent of any credit balance existing in the revaluation surplus reserve account.

B) A revaluation increase that reverses a previous decrease should be recognised in the income statement to the extent that it reverses any previously downward revaluation of the same asset.

C) A debit to a revaluation surplus reserve account that is a reversal of a previous revaluation increase should not exceed the amount of the original credit.

D) When a change in valuation is a reversal of a previous revaluation accumulated depreciation does not have to be written off against the asset before the revaluation is recorded.

A) A revaluation decrease that reverses a previous increase should be recognised as a decrease in other comprehensive income to the extent of any credit balance existing in the revaluation surplus reserve account.

B) A revaluation increase that reverses a previous decrease should be recognised in the income statement to the extent that it reverses any previously downward revaluation of the same asset.

C) A debit to a revaluation surplus reserve account that is a reversal of a previous revaluation increase should not exceed the amount of the original credit.

D) When a change in valuation is a reversal of a previous revaluation accumulated depreciation does not have to be written off against the asset before the revaluation is recorded.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

16

The carrying amount of a depreciable, non-current asset is its:

A) historic cost.

B) cost less residual amount.

C) cost or revalued amount less accumulated depreciation.

D) net realisable value.

A) historic cost.

B) cost less residual amount.

C) cost or revalued amount less accumulated depreciation.

D) net realisable value.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

17

A) Accumulated depreciation - plant 30 000 Plant 15 000

Gain on revaluation plant 15 000

B) Plant 15 000 Gain on revaluation plant 15 000

C) Expense on revaluation of plant 15 000 Plant 15 000

D) Plant 15 000 Expense on revaluation of plant 15 000

Accumulated depreciation - plant 30 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

18

The basic accounting entry for a revaluation decrease of a non-depreciable asset that is not a reversal of an original increase is which of the following?

A) Debit expense on revaluation of asset; credit asset

B) Debit asset; credit expense on the revaluation of asset

C) Debit revaluation surplus reserve; credit asset

D) Debit asset; credit revaluation surplus reserve

A) Debit expense on revaluation of asset; credit asset

B) Debit asset; credit expense on the revaluation of asset

C) Debit revaluation surplus reserve; credit asset

D) Debit asset; credit revaluation surplus reserve

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

19

Which statement relating to revaluations of non-current assets is not true?

A) A revaluation increase is regarded as income to be added to the firm's profit for the year.

B) Future depreciation charges will be based on the revalued carrying amount of the asset.

C) Before assets are revalued any existing accumulated depreciation must be written off against the asset account.

D) A revaluation decrease should be included as a reduction in profit.

A) A revaluation increase is regarded as income to be added to the firm's profit for the year.

B) Future depreciation charges will be based on the revalued carrying amount of the asset.

C) Before assets are revalued any existing accumulated depreciation must be written off against the asset account.

D) A revaluation decrease should be included as a reduction in profit.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

20

A revaluation surplus is what type of account?

A) Asset

B) Liability

C) Income

D) Equity

A) Asset

B) Liability

C) Income

D) Equity

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

21

Which statement relating to the composite-rate depreciation approach untrue?

A) It is often used in practice by business entities with many similar assets in the one class.

B) A single average depreciation rate is applied to the average of the beginning and ending balances of a functional group of assets.

C) No gain or loss is recognised on the disposal of individual assets within the composite group.

D) Composite-rate depreciation always uses the straight-line method of depreciation.

A) It is often used in practice by business entities with many similar assets in the one class.

B) A single average depreciation rate is applied to the average of the beginning and ending balances of a functional group of assets.

C) No gain or loss is recognised on the disposal of individual assets within the composite group.

D) Composite-rate depreciation always uses the straight-line method of depreciation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

22

Midlothian Ltd uses composite-rate depreciation rate at 12.5% p.a. for its office equipment. The office equipment account had a $17 000 balance of the beginning of the period and a $33 000 balance at the end of the accounting period. The annual charge for depreciation is:

A) $2062.

B) $4125.

C) $3125.

D) $6250.

A) $2062.

B) $4125.

C) $3125.

D) $6250.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

23

On 1 January 2015 the equipment was sold for $15 000. What is the accounting entry to record the receipt of the proceeds from the sale of the equipment?A) Debit bank $15 000; credit proceeds from sale of equipment $15 000

B) Debit bank $17 000; credit proceeds from sale of equipment $17 000

C) Debit bank $15 000; credit equipment $15 000

D) Debit bank $2000; credit proceeds from sale of equipment $2000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

24

Carrying amount of equipment is what type of account?

A) Asset

B) Negative asset

C) Expense

D) Negative expense

A) Asset

B) Negative asset

C) Expense

D) Negative expense

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

25

Recoverable amount is the:

A) higher of an asset's fair value less costs to sell, and its value in use.

B) amount expected to be received from the disposal of the asset.

C) amount expected to be recovered from the use of the asset.

D) trade-in or expected amount to be received from the disposal of the asset.

A) higher of an asset's fair value less costs to sell, and its value in use.

B) amount expected to be received from the disposal of the asset.

C) amount expected to be recovered from the use of the asset.

D) trade-in or expected amount to be received from the disposal of the asset.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

26

Proceeds from the sale of equipment is what type of account?

A) Liability

B) Income

C) Expense

D) Negative asset

A) Liability

B) Income

C) Expense

D) Negative asset

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

27

Which statement relating to the composite-rate depreciation approach is not true?

A) A single depreciation rate is applied to the average cost of a functional group of assets.

B) It is only used for items valued at less than $500 each.

C) The composite rate is applied to the average of the beginning and ending balances in the asset account for the year.

D) It is often used in practice by business entities with many similar assets in the one class.

A) A single depreciation rate is applied to the average cost of a functional group of assets.

B) It is only used for items valued at less than $500 each.

C) The composite rate is applied to the average of the beginning and ending balances in the asset account for the year.

D) It is often used in practice by business entities with many similar assets in the one class.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

28

A motor vehicle, which had a carrying amount at the end of the financial year 2011/12 of $18 000, was disposed of on 1 November 2012. Depreciation was calculated on the vehicle at 20% per annum using the diminishing-balance method. What was the depreciation expense charged for the first 4 months of the financial year 2012/13, before the asset was sold?

A) $18 000

B) $0

C) $3600

D) $1200

A) $18 000

B) $0

C) $3600

D) $1200

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

29

On 31 December 2014 an aeroplane with a cost of $200 000 has accumulated depreciation written off of $90 000. If it was sold for $130 000 on 1 January 2015 how much will be recorded as the expense carrying-value on the disposal of the plane?

A) $200 000

B) $130 000

C) $110 000

D) $90 000

A) $200 000

B) $130 000

C) $110 000

D) $90 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

30

On 1 January 2015 the equipment was sold for $15 000. The accounting entry to record the closing of the equipment and the accumulated depreciation of equipment accounts is which of the following?A) Debit accumulated depreciation equipment $63 000; credit equipment $63 000

B) Debit accumulated depreciation equipment $63 000; debit carrying amount of equipment $17 000; credit equipment $80 000

C) Debit bank $15 000; credit carrying amount of equipment $15 000

D) Debit accumulated depreciation equipment $17 000; credit equipment $17 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

31

Billy's Computer Shop purchased some new equipment trading in old equipment with a carrying amount of $10 000. Cash of $9000 was paid to the supplier and a trade-in allowance of $7000 was granted. The new equipment should be recorded at:

A) $19 000.

B) $16 000.

C) $9000.

D) $7000.

A) $19 000.

B) $16 000.

C) $9000.

D) $7000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

32

If a computer with a fully depreciated cost of $30 000 is discarded as worthless, the accounting entry to record the scrapping is which of the following?

A) Debit expense on disposal of asset $30 000; credit computer $30 000

B) Debit expense on disposal of asset $30 000; credit accumulated depreciation computer $30 000

C) Debit accumulated depreciation computer $30 000; credit computer $30 000

D) Debit accumulated depreciation computer $30 000; credit computer $30 000; Debit expense on disposal of asset; credit proceeds of disposal of asset $30 000

A) Debit expense on disposal of asset $30 000; credit computer $30 000

B) Debit expense on disposal of asset $30 000; credit accumulated depreciation computer $30 000

C) Debit accumulated depreciation computer $30 000; credit computer $30 000

D) Debit accumulated depreciation computer $30 000; credit computer $30 000; Debit expense on disposal of asset; credit proceeds of disposal of asset $30 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

33

When an asset is sold the gain or loss on disposal is the difference between the:

A) proceeds of sale and the original cost of the asset.

B) proceeds of sale and the carrying amount of the asset.

C) proceeds of sale and the fair value of the asset.

D) original cost and the accumulated depreciation of the asset.

A) proceeds of sale and the original cost of the asset.

B) proceeds of sale and the carrying amount of the asset.

C) proceeds of sale and the fair value of the asset.

D) original cost and the accumulated depreciation of the asset.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

34

When a non-current asset is sold the gain or loss on disposal is the difference between:

A) fair market value and accumulated depreciation.

B) replacement value and selling price.

C) fair value and selling price.

D) selling price and carrying amount.

A) fair market value and accumulated depreciation.

B) replacement value and selling price.

C) fair value and selling price.

D) selling price and carrying amount.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

35

Assume that a machine with a cost of $9000 has accumulated depreciation of $4800 on the date of its disposal. If it was traded-in for $4000 on a new machine and the balance of $2000 was paid in cash what is the profit or loss on disposal of the old machine? (Ignore GST.)

A) $2000 loss

B) $200 loss

C) $800 gain

D) $3800 loss

A) $2000 loss

B) $200 loss

C) $800 gain

D) $3800 loss

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

36

On 31 December 2014 an aeroplane with a cost of $200 000 has had accumulated depreciation written off of $170 000. If it was sold for a profit of $30 000 on 1 January 2015 how much was recorded as income from the proceeds of the sale?

A) $30 000

B) $60 000

C) Nil

D) $200 000

A) $30 000

B) $60 000

C) Nil

D) $200 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

37

Recoverable amount is the:

A) higher of an asset's fair value less costs to sell, and its value in use.

B) amount expected to be received from the disposal of the asset.

C) amount expected to be recovered from the use of the asset.

D) lower of an assets fair value and its net realisable value.

A) higher of an asset's fair value less costs to sell, and its value in use.

B) amount expected to be received from the disposal of the asset.

C) amount expected to be recovered from the use of the asset.

D) lower of an assets fair value and its net realisable value.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

38

The pair of terms that match is:

I) Non-current fixed assets and depreciation

Ii) Natural resources and amortisation

Iii) Intangible assets and depletion

Iv) Land and depreciation

A) i, ii, iv

B) i, ii, iii, iv

C) ii, iii,

D) i

I) Non-current fixed assets and depreciation

Ii) Natural resources and amortisation

Iii) Intangible assets and depletion

Iv) Land and depreciation

A) i, ii, iv

B) i, ii, iii, iv

C) ii, iii,

D) i

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

39

On 31 December 2013 a printing machine with a cost of $380 000 has accumulated depreciation written off of $140 000. If it is sold for $220 000 on 1 January 2014 what will be the net effect of the sale on the income statement?

A) $20 000 profit

B) $20 000 loss

C) $160 000 loss

D) $80 000 profit

A) $20 000 profit

B) $20 000 loss

C) $160 000 loss

D) $80 000 profit

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

40

Which statement is not correct?

A) If an asset is scrapped as worthless before it is fully depreciated its original cost represents an expense on disposal.

B) If an asset is scrapped as worthless before it is fully depreciated its carrying amount represents an expense on disposal.

C) An amount paid to remove an asset that is scrapped before it is fully depreciated is an addition to the expense recorded on its disposal.

D) When an asset is scrapped during the year an entry should be made to record depreciation expense for the portion of the year before scrapping.

A) If an asset is scrapped as worthless before it is fully depreciated its original cost represents an expense on disposal.

B) If an asset is scrapped as worthless before it is fully depreciated its carrying amount represents an expense on disposal.

C) An amount paid to remove an asset that is scrapped before it is fully depreciated is an addition to the expense recorded on its disposal.

D) When an asset is scrapped during the year an entry should be made to record depreciation expense for the portion of the year before scrapping.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

41

Which of these is not an example of an intangible asset?

I) Trademark

Ii) Oil and gas reserves

Iii) Licences

Iv) Goodwill

A) i, ii

B) iii

C) i, ii, iii

D) ii

I) Trademark

Ii) Oil and gas reserves

Iii) Licences

Iv) Goodwill

A) i, ii

B) iii

C) i, ii, iii

D) ii

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

42

The excess of the purchase price of a business over the fair values of the identifiable net assets acquired is a measure of:

A) fair value.

B) revaluation surplus.

C) purchased goodwill.

D) improvements.

A) fair value.

B) revaluation surplus.

C) purchased goodwill.

D) improvements.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

43

Under IAS 38/AASB 138, which statement concerning internally generated intangible assets is not true?

A) They can only be recognised if their cost can be measured reliably.

B) It is likely that the cost of internally generated brand names, mastheads and customer lists can be measured reliably.

C) The tests for recognising internally generated intangibles are more stringent than for recognising internally generated property, plant and equipment.

D) If patents and copyrights are deemed to be in the research phase all expenditure incurred should be expensed rather than capitalised.

A) They can only be recognised if their cost can be measured reliably.

B) It is likely that the cost of internally generated brand names, mastheads and customer lists can be measured reliably.

C) The tests for recognising internally generated intangibles are more stringent than for recognising internally generated property, plant and equipment.

D) If patents and copyrights are deemed to be in the research phase all expenditure incurred should be expensed rather than capitalised.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

44

Goodwill is defined in IFRS 3/AASB 3 Business Combinations as:

A) an asset having no physical substance.

B) an asset not specifically brought to account.

C) the benefits of a favourable reputation.

D) future economic benefits arising from assets that are not capable of being individually identified and separately recognised.

A) an asset having no physical substance.

B) an asset not specifically brought to account.

C) the benefits of a favourable reputation.

D) future economic benefits arising from assets that are not capable of being individually identified and separately recognised.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

45

Which pairing of non-current assets and acquisition value does not match?

A) Identifiable intangible assets and cost

B) Goodwill and cost of the business combination less the sum of the fair values of the net assets acquired

C) Mineral resources and cost

D) Biological assets and agricultural produce and cost

A) Identifiable intangible assets and cost

B) Goodwill and cost of the business combination less the sum of the fair values of the net assets acquired

C) Mineral resources and cost

D) Biological assets and agricultural produce and cost

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

46

Which statement concerning the accounting treatment of intangible assets under IAS 38/AASB 138 is true?

A) Goodwill can be purchased or sold as a separate asset.

B) Any internally generated trademark or brand name can be recognised as an asset.

C) IAS 38/AASB 138 accepts the view that some intangible assets have unlimited lives and therefore should not be amortised.

D) An intangible asset is defined as an asset without physical substance.

A) Goodwill can be purchased or sold as a separate asset.

B) Any internally generated trademark or brand name can be recognised as an asset.

C) IAS 38/AASB 138 accepts the view that some intangible assets have unlimited lives and therefore should not be amortised.

D) An intangible asset is defined as an asset without physical substance.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

47

A) $7000.

B) $27 000.

C) $13 000.

D) $0.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

48

Which of these are not examples of biological assets?

A) Wool and wine

B) Trees in a pine plantation, coffee bushes on a coffee plantation

C) Sheep and cattle

D) Planted wheat and grape vines

A) Wool and wine

B) Trees in a pine plantation, coffee bushes on a coffee plantation

C) Sheep and cattle

D) Planted wheat and grape vines

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

49

Which statement concerning patents is true?

A) A patent in Australia gives the holder the exclusive right to produce and sell a particular product for a period of 70 years.

B) Research costs spent on internal patent development cannot be recognised as an asset under IAS 38/AASB 138.

C) A patent that is purchased from its holder is debited to an asset account and must be amortised over a 20 year period.

D) A patent that has been capitalised is shown in the balance sheet on one line at its net value.

A) A patent in Australia gives the holder the exclusive right to produce and sell a particular product for a period of 70 years.

B) Research costs spent on internal patent development cannot be recognised as an asset under IAS 38/AASB 138.

C) A patent that is purchased from its holder is debited to an asset account and must be amortised over a 20 year period.

D) A patent that has been capitalised is shown in the balance sheet on one line at its net value.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

50

Under IAS 41/AASB 141 the basis for recording biological assets in the accounting records is:

A) net fair value.

B) market value.

C) historical cost.

D) replacement value.

A) net fair value.

B) market value.

C) historical cost.

D) replacement value.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

51

Which statement relating to mineral resources is untrue?

A) Accounting for mineral resources is governed by IAS 16/AASB 116.

B) The cost at which mineral resources are recorded may include amounts spent on exploration and development.

C) As the mineral resource asset is used up its cost is proportionately transferred to an amortisation (depletion) expense account.

D) The most common approach to the calculation of the depletion of mineral resources is the reducing-balance method.

A) Accounting for mineral resources is governed by IAS 16/AASB 116.

B) The cost at which mineral resources are recorded may include amounts spent on exploration and development.

C) As the mineral resource asset is used up its cost is proportionately transferred to an amortisation (depletion) expense account.

D) The most common approach to the calculation of the depletion of mineral resources is the reducing-balance method.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

52

IFRS 3/AASB 3 requires that if the amount paid for a business is less than the sum of the fair value of the net identifiable assets acquired, and this is a genuine bargain purchase, then the difference is to be:

A) taken directly to an equity account.

B) recognised immediately as a gain in the income statement.

C) offset against any goodwill previously acquired.

D) used to reduce the value of the monetary assets acquired.

A) taken directly to an equity account.

B) recognised immediately as a gain in the income statement.

C) offset against any goodwill previously acquired.

D) used to reduce the value of the monetary assets acquired.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

53

Under IAS 41/AASB 141 the basis for measuring biological assets is:

A) historical cost.

B) fair value less estimated point-of-sale costs.

C) replacement value.

D) estimated market value less estimated point-of-sale costs.

A) historical cost.

B) fair value less estimated point-of-sale costs.

C) replacement value.

D) estimated market value less estimated point-of-sale costs.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

54

Intangible assets may be further classified as:

A) identifiable and unidentifiable.

B) cash and credit.

C) living and non-living.

D) physical and non-physical.

A) identifiable and unidentifiable.

B) cash and credit.

C) living and non-living.

D) physical and non-physical.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

55

A coal mine was purchased for $400 000. Estimated production is 20 000 000 tons of coal after which the mine will be sold for $40 000. During a recent year 6 500 000 tons of coal were produced and sold. Amortisation for the year would be:

A) $117 000.

B) $130 000.

C) $143 000.

D) $150 000.

A) $117 000.

B) $130 000.

C) $143 000.

D) $150 000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

56

How many of these are mineral resources?

Oil

Coal

Natural gas

Uranium

A) 1

B) 2

C) 3

D) 4

Oil

Coal

Natural gas

Uranium

A) 1

B) 2

C) 3

D) 4

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

57

What is the accounting entry to amortise an intangible asset over its useful life?

A) Debit amortisation expense; credit asset

B) Debit accumulated amortisation; credit amortisation of asset

C) Debit amortisation expense; credit accumulated amortisation

D) Debit amortisation expense; credit accumulated depreciation

A) Debit amortisation expense; credit asset

B) Debit accumulated amortisation; credit amortisation of asset

C) Debit amortisation expense; credit accumulated amortisation

D) Debit amortisation expense; credit accumulated depreciation

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

58

How many of these statements are true of the composite rate depreciation approach?

The general asset mix of a functional group of assets is assumed to be the same through new assets are added and old assets are sold.

Additions and retirements are assumed to occur uniformly throughout the year.

The method is often used by business entities with many similar assets in one class.

Profits and losses on disposal of assets are debited/credited to the accumulated depreciation account so no losses or profits on disposal are recorded.

A) 1

B) 2

C) 3

D) 4

The general asset mix of a functional group of assets is assumed to be the same through new assets are added and old assets are sold.

Additions and retirements are assumed to occur uniformly throughout the year.

The method is often used by business entities with many similar assets in one class.

Profits and losses on disposal of assets are debited/credited to the accumulated depreciation account so no losses or profits on disposal are recorded.

A) 1

B) 2

C) 3

D) 4

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

59

According to IAS 38/AASB 138 intangible assets that have been established to have finite useful lives:

A) should be amortised on a systematic basis over their useful lives.

B) amortised over their legal lives.

C) should not be amortised but tested each year for impairment.

D) should be amortised over a period not exceeding 20 years.

A) should be amortised on a systematic basis over their useful lives.

B) amortised over their legal lives.

C) should not be amortised but tested each year for impairment.

D) should be amortised over a period not exceeding 20 years.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

60

Which of these does not contribute to the value of purchased goodwill?

A) Superior management

B) Favourable location

C) Customer loyalty

D) A franchise

A) Superior management

B) Favourable location

C) Customer loyalty

D) A franchise

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

61

King Ltd acquired the business of Prince Ltd for a cash payment of $480 000. The carrying amount of Prince Ltd's assets at the time of purchase was $490 000 while the independent fair value was $460 000. There were no liabilities. What is the value of the purchased goodwill recorded by King Ltd?

A) $(10 000)

B) $0

C) $20 000

D) 30 000

A) $(10 000)

B) $0

C) $20 000

D) 30 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

62

In rare cases the cost of purchasing a business combination may be less than the sum of the fair values of the identifiable assets and liabilities acquired (bargain purchase). Which of the following statements concerning the requirements of IFRS 3/AASB 3 in this situation is true?

A) The buyer and the seller must adjust the value to the consideration to eliminate the bargain purchase.

B) Any bargain purchase difference should be eliminated by adjusting the values of the assets acquired as it is not possible to recognise a bargain purchase.

C) A genuine bargain purchase should be recognised immediately as a gain that is an addition to profit.

D) A genuine bargain purchase should be recognised progressively as an addition to profit over a 20 year period.

A) The buyer and the seller must adjust the value to the consideration to eliminate the bargain purchase.

B) Any bargain purchase difference should be eliminated by adjusting the values of the assets acquired as it is not possible to recognise a bargain purchase.

C) A genuine bargain purchase should be recognised immediately as a gain that is an addition to profit.

D) A genuine bargain purchase should be recognised progressively as an addition to profit over a 20 year period.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

63

On 1 June 2015 Blender Company acquired for $300 000 cash the business of Madcap Inc. The carrying amount of Madcap Inc's net assets at the time of the acquisition was $255 000 while independent valuers calculated their fair value at $275 000. Blender Company should debit 'Goodwill' for the amount of:

A) $0.

B) $15 000.

C) $25 000.

D) $45 000.

A) $0.

B) $15 000.

C) $25 000.

D) $45 000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

64

Which statement about goodwill is true?

A) Goodwill can be purchased or sold as a separate item.

B) Goodwill arises from many factors, such as customer confidence, superior management and a favourable location.

C) Under IFRS 3/AASB 3 goodwill must be amortised.

D) Goodwill is classified as a current asset.

A) Goodwill can be purchased or sold as a separate item.

B) Goodwill arises from many factors, such as customer confidence, superior management and a favourable location.

C) Under IFRS 3/AASB 3 goodwill must be amortised.

D) Goodwill is classified as a current asset.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

65

According to IFRS 3/AASB 3 purchased goodwill:

A) should be written off immediately on recognition.

B) should be written off by a systematic charge against profits using the straight-line method, over a period not exceeding 20 years.

C) should remain in the accounts at cost less any accumulated impairment losses.

D) should be written off over the useful life of the asset.

A) should be written off immediately on recognition.

B) should be written off by a systematic charge against profits using the straight-line method, over a period not exceeding 20 years.

C) should remain in the accounts at cost less any accumulated impairment losses.

D) should be written off over the useful life of the asset.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 65 flashcards in this deck.