Deck 10: Cash Management and Control

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

A) $85 000

B) $50 000

C) $66 000

D) $70 000

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

A) $6400.

B) $12 400.

C) $9600.

D) $8000.

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/65

Play

Full screen (f)

Deck 10: Cash Management and Control

1

What are the two basic types of internal controls?

A) Internal audit and internal check

B) Bank reconciliations and stocktakes

C) Administrative and accounting controls

D) Selling and general controls

A) Internal audit and internal check

B) Bank reconciliations and stocktakes

C) Administrative and accounting controls

D) Selling and general controls

C

2

Which of these is not a measure of good internal control?

A) Banking cash daily

B) Reconciling a control account with its subsidiary ledger

C) Combining authority to purchase goods and sign cheques

D) Requiring all employees to take annual leave

A) Banking cash daily

B) Reconciling a control account with its subsidiary ledger

C) Combining authority to purchase goods and sign cheques

D) Requiring all employees to take annual leave

C

3

Which of these does not represent proper internal control of cash receipts?

A) Daily banking of receipts.

B) Two people opening the mail.

C) Paying accounts directly out of the cash register.

D) Balancing the cash register after each employees' shift.

A) Daily banking of receipts.

B) Two people opening the mail.

C) Paying accounts directly out of the cash register.

D) Balancing the cash register after each employees' shift.

C

4

The cash short and over ledger account, which records the difference between the total of the cash register tape and the actual cash counted from the register:

A) appears on the balance sheet as liability.

B) is closed to the profit or loss summary account.

C) is deducted from the bank account balance in the ledger.

D) is included in the bank reconciliation.

A) appears on the balance sheet as liability.

B) is closed to the profit or loss summary account.

C) is deducted from the bank account balance in the ledger.

D) is included in the bank reconciliation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

5

Which of these is not included in the definition of cash?

A) Cheque

B) EFTPOS transactions

C) Bills receivable

D) Petty cash

A) Cheque

B) EFTPOS transactions

C) Bills receivable

D) Petty cash

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

6

Which of these is not a benefit of a sound system of internal control?

A) Greater reliability of the accounting information

B) A highly marketable product

C) Fewer errors

D) Less likelihood of fraud

A) Greater reliability of the accounting information

B) A highly marketable product

C) Fewer errors

D) Less likelihood of fraud

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

7

The overall procedures adopted by a business to safeguard its assets, promote the reliability of accounting data and encourage compliance with management policies are:

A) internal controls.

B) bank reconciliations.

C) physical controls.

D) cash budgets.

A) internal controls.

B) bank reconciliations.

C) physical controls.

D) cash budgets.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

8

Mechanical and electronic controls should be used, where possible, to protect assets and improve the accuracy of the accounting process. An example of such a device is:

I A burglar alarm

Ii A virus scanner

Iii Electronic funds transfer

Iv Insurance

A) i, ii, iii

B) i, ii, iii, iv

C) i, iii, iv

D) ii, iii, iv

I A burglar alarm

Ii A virus scanner

Iii Electronic funds transfer

Iv Insurance

A) i, ii, iii

B) i, ii, iii, iv

C) i, iii, iv

D) ii, iii, iv

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following is not a feature of good internal control?

A) Regular stocktakes

B) Labelling of fixed assets

C) Regular bank reconciliations

D) Making cash payments from unbanked cash receipts

A) Regular stocktakes

B) Labelling of fixed assets

C) Regular bank reconciliations

D) Making cash payments from unbanked cash receipts

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

10

Which of these is not an important principle for the control of cash payments?

A) Employees who sign cheques should not accept delivery of goods.

B) Only senior staff should have the authority to approve invoices for payment.

C) Cheques should be written out promptly even if the invoice is not yet provided.

D) Once the cheque is written the invoice should be stamped 'paid'.

A) Employees who sign cheques should not accept delivery of goods.

B) Only senior staff should have the authority to approve invoices for payment.

C) Cheques should be written out promptly even if the invoice is not yet provided.

D) Once the cheque is written the invoice should be stamped 'paid'.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

11

Which of these is a limitation of internal control?

I The cost of the controls

II The possibility of collusion between two or more employees

III The accounting standards

A) I and III

B) II and III

C) I and II

D) I, II and III

I The cost of the controls

II The possibility of collusion between two or more employees

III The accounting standards

A) I and III

B) II and III

C) I and II

D) I, II and III

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following statements concerning internal control is true?

A) Double entry accounting is an internal control.

B) Fraud will be eliminated by good internal control.

C) Physical counts of stock on hand are not part of internal control procedures.

D) It is OK to pay accounts out of unbanked receipts as long as a note is made of what has occurred.

A) Double entry accounting is an internal control.

B) Fraud will be eliminated by good internal control.

C) Physical counts of stock on hand are not part of internal control procedures.

D) It is OK to pay accounts out of unbanked receipts as long as a note is made of what has occurred.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

13

Which of these is not necessarily one of the benefits of effective internal control?

A) More accurate accounting data

B) Safeguarding assets

C) A sound liquidity position

D) A more efficient accounting system

A) More accurate accounting data

B) Safeguarding assets

C) A sound liquidity position

D) A more efficient accounting system

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

14

The asset most commonly subject to misappropriation is:

A) furniture and fittings.

B) investments.

C) land and buildings.

D) cash.

A) furniture and fittings.

B) investments.

C) land and buildings.

D) cash.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

15

Internal controls that apply to computerised accounting systems include which of the following?

I Programming controls

II Passwords

III Back ups

IV Computer viruses

A) I, II, and III

B) I, II and IV

C) I, III and IV

D) II, III and IV

I Programming controls

II Passwords

III Back ups

IV Computer viruses

A) I, II, and III

B) I, II and IV

C) I, III and IV

D) II, III and IV

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

16

How many of these are features of good internal control of cash payments?

Separation of record-keeping and the authority to sign cheques

The use of a business bank account allowing all major payments to be made by cheque or electronic transfer

Preparing regular bank reconciliation statements

The use of a petty cash fund to cover small incidental cash payments

A) One

B) Two

C) Three

D) Four

Separation of record-keeping and the authority to sign cheques

The use of a business bank account allowing all major payments to be made by cheque or electronic transfer

Preparing regular bank reconciliation statements

The use of a petty cash fund to cover small incidental cash payments

A) One

B) Two

C) Three

D) Four

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

17

If the cash in the cash register is $1450 and the cash register tape at the end of the shift shows a total of $1368, this would indicate:

A) cash over of $82.

B) a cash shortage of $82.

C) the cash register and the tape agree.

D) the cashier is dishonest.

A) cash over of $82.

B) a cash shortage of $82.

C) the cash register and the tape agree.

D) the cashier is dishonest.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

18

Which of these is not a characteristic of good internal control?

A) Insurance of assets

B) Joint of responsibility for assets

C) Rotation of employees over a range of tasks

D) Regular bank reconciliations

A) Insurance of assets

B) Joint of responsibility for assets

C) Rotation of employees over a range of tasks

D) Regular bank reconciliations

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

19

Which of these is not a good internal control practice?

A) Handwriting cheques

B) The use of passwords for computer access

C) The pre-numbering of documents

D) Random checks of the petty cash balance

A) Handwriting cheques

B) The use of passwords for computer access

C) The pre-numbering of documents

D) Random checks of the petty cash balance

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

20

As a business grows and the owner must rely more on others to help in managing operations, internal control becomes:

A) more important.

B) less important.

C) unnecessary.

D) growth has no effect on the importance of internal control.

A) more important.

B) less important.

C) unnecessary.

D) growth has no effect on the importance of internal control.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

21

The main purpose of a bank reconciliation is:

A) to prove the accuracy of the debtors' ledger.

B) to prove the accuracy of the general ledger.

C) to prove the accuracy of the ledger bank account.

D) to prove the accuracy of the bookkeeper.

A) to prove the accuracy of the debtors' ledger.

B) to prove the accuracy of the general ledger.

C) to prove the accuracy of the ledger bank account.

D) to prove the accuracy of the bookkeeper.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

22

Which of these is not a principle of internal control?

A) Separation of record keeping and custody of assets

B) Division of responsibility for related transactions

C) Establishing clear lines of responsibility

D) Placing excess cash on fixed deposit to earn interest

A) Separation of record keeping and custody of assets

B) Division of responsibility for related transactions

C) Establishing clear lines of responsibility

D) Placing excess cash on fixed deposit to earn interest

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

23

The municipality of Stonybank had an unadjusted ledger bank balance at 31 March of $28 000 Dr. The bank statement for the month shows a balance of $16 300 Cr. It also shows bank charges of $255 and dividends directly paid into the bank of $500. Deposits not yet credited are $14 545 and unpresented cheques are $2600. What is the cash at bank ledger balance at 31 March?

A) $28 245

B) $40 190

C) $39 945

D) $23 045

A) $28 245

B) $40 190

C) $39 945

D) $23 045

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

24

The deposit column of Jeremy Company's bank statement shows a direct credit of $1000. Assuming the account is not in overdraft, when reconciling the bank account, this amount will be:

A) deducted from the bank statement balance in the reconciliation.

B) added to the bank statement balance in the reconciliation.

C) deducted from the general ledger bank balance.

D) added to the general ledger bank balance.

A) deducted from the bank statement balance in the reconciliation.

B) added to the bank statement balance in the reconciliation.

C) deducted from the general ledger bank balance.

D) added to the general ledger bank balance.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

25

When reconciling the bank ledger account and the bank statement, if both are in overdraft, unpresented cheques will be:

A) deducted from the bank statement balance in the reconciliation.

B) added to the bank statement balance in the reconciliation.

C) deducted from the general ledger bank balance.

D) added to the general ledger bank balance.

A) deducted from the bank statement balance in the reconciliation.

B) added to the bank statement balance in the reconciliation.

C) deducted from the general ledger bank balance.

D) added to the general ledger bank balance.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

26

When reconciling a bank account with a positive balance, interest charged by the bank is:

A) added to the bank statement balance in the reconciliation.

B) deduced from the bank statement balance in the reconciliation.

C) deducted from the general ledger bank balance.

D) added to the general ledger bank balance.

A) added to the bank statement balance in the reconciliation.

B) deduced from the bank statement balance in the reconciliation.

C) deducted from the general ledger bank balance.

D) added to the general ledger bank balance.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

27

When reconciling a bank account with a positive balance, bank fees and interest charged by the bank are:

A) added to the general ledger bank balance.

B) deducted from the general ledger bank balance.

C) deducted from the bank statement balance in the reconciliation.

D) added to the bank statement balance in the reconciliation.

A) added to the general ledger bank balance.

B) deducted from the general ledger bank balance.

C) deducted from the bank statement balance in the reconciliation.

D) added to the bank statement balance in the reconciliation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

28

Kathryn's account is not in overdraft. When preparing the bank reconciliation she found that the bank had incorrectly debited her account with $120. The proper procedure is to:

A) deduct $120 from the bank balance in the general ledger and notify the bank.

B) deduct $120 from the bank balance in the general ledger.

C) add $120 to the bank statement balance in the bank reconciliation and notify the bank.

D) do nothing as the bank will adjust the error when they balance.

A) deduct $120 from the bank balance in the general ledger and notify the bank.

B) deduct $120 from the bank balance in the general ledger.

C) add $120 to the bank statement balance in the bank reconciliation and notify the bank.

D) do nothing as the bank will adjust the error when they balance.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

29

Fletcher and Associates had an unadjusted bank account ledger balance at 31 May of $750 Dr. The bank statement at the same date showed a balance of $1090 Cr. Bank service charges for the month were $20 and outstanding cheques totalled $400. The bank statement revealed that the bank had collected dividends for the firm of $120 and a deposit of $150 is not yet recorded on the statement. What is the corrected bank account ledger balance at 31 May?

A) $1190

B) $650

C) $850

D) $1000

A) $1190

B) $650

C) $850

D) $1000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

30

Assuming the account is not in overdraft, when reconciling the ledger with the bank statement a deposit in transit should be:

A) subtracted from the general ledger bank balance.

B) added to the general ledger bank balance.

C) subtracted from the bank statement balance in the reconciliation.

D) added to the bank statement balance in the reconciliation.

A) subtracted from the general ledger bank balance.

B) added to the general ledger bank balance.

C) subtracted from the bank statement balance in the reconciliation.

D) added to the bank statement balance in the reconciliation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

31

Which of these would not appear as a debit on TT's bank statement?

A) A dishonoured cheque

B) Employees' salaries paid by electronic funds transfer

C) A cheque paid to a creditor by TT

D) A cheque received by TT from a debtor

A) A dishonoured cheque

B) Employees' salaries paid by electronic funds transfer

C) A cheque paid to a creditor by TT

D) A cheque received by TT from a debtor

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

32

Ignoring GST, the accounting entry that would need to be made for a debtor's cheque for $3400 that has been dishonoured is which of the following?

A) Debit bank $3400; credit debtors $3400

B) Debit debtors $3400; credit bank $3400

C) Debit debtors $3400; credit creditors $3400

D) Debit debtors $3400; credit discount allowed $3400

A) Debit bank $3400; credit debtors $3400

B) Debit debtors $3400; credit bank $3400

C) Debit debtors $3400; credit creditors $3400

D) Debit debtors $3400; credit discount allowed $3400

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following statements relating to a bank statement is true?

A) The customer is viewed as a debtor.

B) It constitutes a source document for the firm for direct debits and credits such as bank charges.

C) A deposit is listed in the debit column.

D) A positive amount in the bank account will be shown as a debit balance.

A) The customer is viewed as a debtor.

B) It constitutes a source document for the firm for direct debits and credits such as bank charges.

C) A deposit is listed in the debit column.

D) A positive amount in the bank account will be shown as a debit balance.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

34

While preparing the bank reconciliation Sara discovered that the bank had incorrectly paid one cheque for a larger amount than was written by the company (bank error). The bank account has a positive balance. The proper procedure is to:

A) add the error to the bank balance in the general ledger.

B) deduct the error from the bank balance in the general ledger and notify the bank.

C) add the error to the bank statement balance in the reconciliation and notify the bank.

D) deduct the error from the bank statement balance in the reconciliation.

A) add the error to the bank balance in the general ledger.

B) deduct the error from the bank balance in the general ledger and notify the bank.

C) add the error to the bank statement balance in the reconciliation and notify the bank.

D) deduct the error from the bank statement balance in the reconciliation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

35

The cornerstone of the internal control of cash is:

A) the bank reconciliation.

B) a strong safe.

C) a petty cash system.

D) the double entry accounting system.

A) the bank reconciliation.

B) a strong safe.

C) a petty cash system.

D) the double entry accounting system.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

36

Which statement relating to dishonoured cheques is true?

A) They appear as credits on the bank statement.

B) They are cheques from debtors deposited into the firm's bank account but not paid by the drawer's bank due to lack of funds or for other reasons.

C) They must be listed in the bank reconciliation.

D) They can be adjusted for by making a negative entry in the sales journal.

A) They appear as credits on the bank statement.

B) They are cheques from debtors deposited into the firm's bank account but not paid by the drawer's bank due to lack of funds or for other reasons.

C) They must be listed in the bank reconciliation.

D) They can be adjusted for by making a negative entry in the sales journal.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

37

The correct order in which the steps in the bank reconciliation process occur is:

I) Tick off the items in the prior reconciliation with the bank statement

Ii) Prepare the bank reconciliation

Iii) Tick off the cash journals with the bank statement

Iv) Update the cash journals with unticked items from the bank statement

A) i, ii, iii, iv

B) iv, iii, ii, i

C) i, iii, iv, ii

D) i, iv, iii, ii

I) Tick off the items in the prior reconciliation with the bank statement

Ii) Prepare the bank reconciliation

Iii) Tick off the cash journals with the bank statement

Iv) Update the cash journals with unticked items from the bank statement

A) i, ii, iii, iv

B) iv, iii, ii, i

C) i, iii, iv, ii

D) i, iv, iii, ii

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

38

When reconciling the ledger with the bank statement (assuming a positive bank balance) a returned (dishonoured) cheque should be:

A) subtracted from the general ledger bank balance.

B) ignored as the bank will adjust the statement in the next period.

C) subtracted from the bank statement balance.

D) added to the bank statement balance in the reconciliation.

A) subtracted from the general ledger bank balance.

B) ignored as the bank will adjust the statement in the next period.

C) subtracted from the bank statement balance.

D) added to the bank statement balance in the reconciliation.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

39

Mojo Ltd received its monthly bank statement showing a balance of $27 629 Cr at 31 January. On this date cash received from ratepayers and not yet deposited at the bank totalled $4321 and outstanding cheques were $857. The amount to appear as cash at bank on the 31 January balance sheet is:

A) $22 451.

B) $28 486.

C) $31 093.

D) $24 165.

A) $22 451.

B) $28 486.

C) $31 093.

D) $24 165.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

40

When preparing a bank reconciliation what would cause the bank statement balance to be less than the adjusted cash balance in the general ledger? (Assume the bank is not in overdraft.)

A) Bank service charges

B) Dishonoured cheques

C) Outstanding deposits

D) Outstanding cheques

A) Bank service charges

B) Dishonoured cheques

C) Outstanding deposits

D) Outstanding cheques

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

41

Malaysian Carpets makes all sales on credit, with 60% of the payment received in the month of sale and 40% in the month following sale. Budgeted sales are

February $100 000

March $120 000

What is the estimated amount received from debtors in March?

A) $220 000

B) $120 000

C) $112 000

D) $108 000

February $100 000

March $120 000

What is the estimated amount received from debtors in March?

A) $220 000

B) $120 000

C) $112 000

D) $108 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

42

A) $85 000

B) $50 000

C) $66 000

D) $70 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

43

The entry at the end of the month to reimburse the petty cash for the amount spent is which of the following?

A) Debit petty cash asset; credit bank

B) Debit bank; credit petty cash asset

C) Debit petty cash asset; credit petty cash expenses

D) Debit petty cash expenses; credit bank

A) Debit petty cash asset; credit bank

B) Debit bank; credit petty cash asset

C) Debit petty cash asset; credit petty cash expenses

D) Debit petty cash expenses; credit bank

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

44

Which is the entry to initially establish the petty cash fund?

A) Debit bank; credit petty cash asset

B) Debit petty cash asset; credit petty cash expenses

C) Debit petty cash expenses; credit bank

D) Debit petty cash asset; credit bank

A) Debit bank; credit petty cash asset

B) Debit petty cash asset; credit petty cash expenses

C) Debit petty cash expenses; credit bank

D) Debit petty cash asset; credit bank

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following is not an advantage of cash budgeting?

A) Idle funds are kept to a minimum.

B) Cash shortages can be predicted.

C) Future planning is facilitated.

D) Cash is safeguarded.

A) Idle funds are kept to a minimum.

B) Cash shortages can be predicted.

C) Future planning is facilitated.

D) Cash is safeguarded.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

46

If the petty cash fund was not reimbursed at the time the financial statements were prepared:

A) expenses would be understated and equity overstated.

B) petty cash asset would be overstated and expenses understated.

C) petty cash expenses would be overstated and bank would be understated.

D) expenses would be overstated and petty cash asset would be understated.

A) expenses would be understated and equity overstated.

B) petty cash asset would be overstated and expenses understated.

C) petty cash expenses would be overstated and bank would be understated.

D) expenses would be overstated and petty cash asset would be understated.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

47

Wellwash Washing Machines makes all sales on credit, with 75% of the payment received in the month of sale, 20% in the month following the sale and 5% never collected. Budgeted sales are:

October $80 000

November $90 000

What is the estimated amount received from debtors in November?

A) $170 000

B) $83 500

C) $67 500

D) $90 000

October $80 000

November $90 000

What is the estimated amount received from debtors in November?

A) $170 000

B) $83 500

C) $67 500

D) $90 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following statements relating to a cash budget is true?

A) It is a statement of expected income and expenses.

B) Non-cash items such as depreciation are included.

C) It is usually prepared on a weekly basis.

D) The shorter the time period involved the easier it is to predict future cash flows.

A) It is a statement of expected income and expenses.

B) Non-cash items such as depreciation are included.

C) It is usually prepared on a weekly basis.

D) The shorter the time period involved the easier it is to predict future cash flows.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

49

The bank statement of a business shows an overdraft of $10 000 at 31 March. In reconciling the account at that date indicate the treatment you would give to cheque no. 461 for $30 that was drawn on 25 March but had not yet been presented for payment.

A) Subtract from the bank statement balance in the bank reconciliation.

B) Add to the bank statement balance in the bank reconciliation.

C) Record in the cash receipts journal.

D) Record in the cash payments journal.

A) Subtract from the bank statement balance in the bank reconciliation.

B) Add to the bank statement balance in the bank reconciliation.

C) Record in the cash receipts journal.

D) Record in the cash payments journal.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

50

Which of these is not an advantage of cash budgeting?

A) It helps to maintain the credit standing of the business.

B) It encourages careful assessment of all proposed expenditures.

C) It keeps to a minimum idle cash funds.

D) It increases sales.

A) It helps to maintain the credit standing of the business.

B) It encourages careful assessment of all proposed expenditures.

C) It keeps to a minimum idle cash funds.

D) It increases sales.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

51

Gourmet Cookware makes all sales on credit with 60% of the payment being received in the month of sale, 30% in the month following sale and the remaining 10% in the subsequent month.

Budgeted sales are as follows

January $100 000

February $140 000

March $120 000

The budgeted balance of debtors at 31 March is:

A) $48 000.

B) $62 000.

C) $74 000.

D) $120 000.

Budgeted sales are as follows

January $100 000

February $140 000

March $120 000

The budgeted balance of debtors at 31 March is:

A) $48 000.

B) $62 000.

C) $74 000.

D) $120 000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

52

The 30 April bank reconciliation of Melbourne Co was prepared using the information below.

Outstanding deposit $750

Ledger bank balance $4350 Dr (adjusted)

Unpresented cheques $530

What was the bank statement balance at 30 April?

A) $3070 Dr

B) $4130 Cr

C) $4350 Cr

D) $5630 Dr

Outstanding deposit $750

Ledger bank balance $4350 Dr (adjusted)

Unpresented cheques $530

What was the bank statement balance at 30 April?

A) $3070 Dr

B) $4130 Cr

C) $4350 Cr

D) $5630 Dr

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

53

Bendigo Resources makes all sales on credit with 40% of the payment received in the month of sale, 40% in the month following the sale and the remaining 20% in the subsequent month.

Budgeted sales are as follows:

January $100 000

February $140 000

March $120 000

The budgeted receipts from debtors during March are:

A) $100 000.

B) $120 000.

C) $124 000.

D) $196 000.

Budgeted sales are as follows:

January $100 000

February $140 000

March $120 000

The budgeted receipts from debtors during March are:

A) $100 000.

B) $120 000.

C) $124 000.

D) $196 000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

54

A cash budget measures?

A) Estimated liquidity

B) Estimated profitability

C) Estimated working capital

D) Estimated financial position

A) Estimated liquidity

B) Estimated profitability

C) Estimated working capital

D) Estimated financial position

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

55

The petty cash account is what type of account?

A) Asset

B) Expense

C) Equity

D) Liability

A) Asset

B) Expense

C) Equity

D) Liability

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

56

Which of these is not an essential feature of the imprest petty cash system?

A) Deciding on a fixed sum that becomes the imprest amount or 'float'.

B) Several people being authorised to reimburse expenses.

C) Cash in the fund together with vouchers always equalling the imprest amount.

D) Replenishment of the fund for the exact amount spent in the period.

A) Deciding on a fixed sum that becomes the imprest amount or 'float'.

B) Several people being authorised to reimburse expenses.

C) Cash in the fund together with vouchers always equalling the imprest amount.

D) Replenishment of the fund for the exact amount spent in the period.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

57

A cash budget measures:

A) estimated future cash position.

B) estimated financial position.

C) estimated profitability.

D) working capital.

A) estimated future cash position.

B) estimated financial position.

C) estimated profitability.

D) working capital.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

58

Which of these is not a broad principle of cash management that helps ensure that a business remains solvent?

A) Collect cash owing from accounts receivable as quickly as possible.

B) Pay accounts payable just before the due date rather than when the statement is first received.

C) Buy all capital equipment on hire purchase.

D) Invest any cash that is surplus to requirements to earn a return for the business.

A) Collect cash owing from accounts receivable as quickly as possible.

B) Pay accounts payable just before the due date rather than when the statement is first received.

C) Buy all capital equipment on hire purchase.

D) Invest any cash that is surplus to requirements to earn a return for the business.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

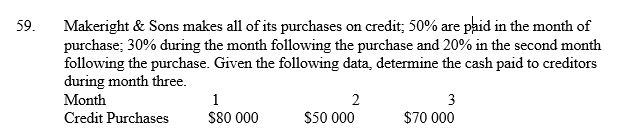

59

A) $6400.

B) $12 400.

C) $9600.

D) $8000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

60

Kathryn's account is not in overdraft. When preparing the bank reconciliation she found that the bank had incorrectly debited her account with $120. The proper procedure is to:

A) deduct $120 from the bank balance in the general ledger and notify the bank.

B) deduct $120 from the bank balance in the general ledger.

C) add $120 to the bank statement balance in the bank reconciliation and notify the bank.

D) do nothing as the bank will adjust the error when it balances.

A) deduct $120 from the bank balance in the general ledger and notify the bank.

B) deduct $120 from the bank balance in the general ledger.

C) add $120 to the bank statement balance in the bank reconciliation and notify the bank.

D) do nothing as the bank will adjust the error when it balances.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

61

Which of these principles of cash managements is untrue?

A) There are disadvantages for a business in holding very low levels of inventory.

B) The longer the operating cycle the longer it takes to pay creditors.

C) It is generally a mistake to delay paying creditors if it means discounts on offer are lost.

D) Generally cash surplus to requirements should be used to acquire necessary non-current assets rather than being kept on fixed deposit.

A) There are disadvantages for a business in holding very low levels of inventory.

B) The longer the operating cycle the longer it takes to pay creditors.

C) It is generally a mistake to delay paying creditors if it means discounts on offer are lost.

D) Generally cash surplus to requirements should be used to acquire necessary non-current assets rather than being kept on fixed deposit.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

62

The ratio that measures solvency by relating cash flows from operating activities to total liabilities is the:

A) gearing ratio.

B) operations index.

C) turnover of cash flow ratio.

D) cash flow adequacy ratio.

A) gearing ratio.

B) operations index.

C) turnover of cash flow ratio.

D) cash flow adequacy ratio.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

63

Which of these is a principle of good cash management?

A) Keeping inventory at a level where no item required by a customer is ever out of stock.

B) Paying creditors before the due date.

C) Investing surplus cash.

D) Offering large cash discounts to debtors to pay within 30 days.

A) Keeping inventory at a level where no item required by a customer is ever out of stock.

B) Paying creditors before the due date.

C) Investing surplus cash.

D) Offering large cash discounts to debtors to pay within 30 days.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

64

The ratio that measures solvency by relating cash flows from operating activities to current liabilities is the:

A) working capital ratio.

B) cash flow adequacy ratio.

C) short-term cash flow adequacy ratio.

D) times interest ratio.

A) working capital ratio.

B) cash flow adequacy ratio.

C) short-term cash flow adequacy ratio.

D) times interest ratio.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

65

The ability of a firm to pay its debts as they fall due is known as:

A) cash management.

B) being in surplus.

C) solvency.

D) the acid test.

A) cash management.

B) being in surplus.

C) solvency.

D) the acid test.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 65 flashcards in this deck.