Deck 8: Accounting for Manufacturing

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

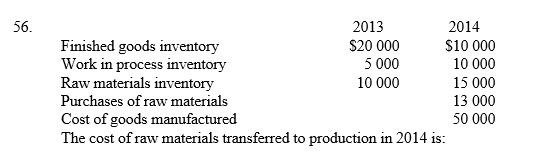

A) $8000.

B) $10 000.

C) $13 000.

D) $18 000.

Question

Question

Question

Question

Question

Question

Question

A) $50 000.

B) $60 000.

C) $55 000.

D) $45 000.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/65

Play

Full screen (f)

Deck 8: Accounting for Manufacturing

1

Which of the following statements is correct?

A) Manufacturing overhead costs are treated as period costs rather than product cost.

B) Product costs are included in inventory until the product is sold.

C) For a retailer all costs and expenses are treated as period costs.

D) Finished goods inventory includes also includes the cost of raw materials.

A) Manufacturing overhead costs are treated as period costs rather than product cost.

B) Product costs are included in inventory until the product is sold.

C) For a retailer all costs and expenses are treated as period costs.

D) Finished goods inventory includes also includes the cost of raw materials.

B

2

Which of the following statements concerning product and period costs is incorrect?

A) The basis of the distinction between product and period costs is the timing of the recognition of an expense in the income statement.

B) Service businesses have both period and product costs.

C) Product costs are included in the cost of inventories until the products are sold.

D) Period costs are not directly required to produce the product.

A) The basis of the distinction between product and period costs is the timing of the recognition of an expense in the income statement.

B) Service businesses have both period and product costs.

C) Product costs are included in the cost of inventories until the products are sold.

D) Period costs are not directly required to produce the product.

B

3

For which purposes do product costs need to be calculated by a manufacturer?

Inventory valuation,Profit determination,Management decision-making

A)Yes Yes Yes

B)Yes No Yes

C)No Yes Yes

D)No No Yes

Inventory valuation,Profit determination,Management decision-making

A)Yes Yes Yes

B)Yes No Yes

C)No Yes Yes

D)No No Yes

Yes Yes Yes

4

As manufacturing overhead costs cannot be traced to products a method must be developed for assigning them to products. Common bases for assignment are all of the following except:

A) direct labour cost.

B) direct labour hours.

C) machine hours.

D) direct labour hours plus direct machine hours.

A) direct labour cost.

B) direct labour hours.

C) machine hours.

D) direct labour hours plus direct machine hours.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

5

Which of these statements is not correct?

A) An expense is the consumption or loss of resources that will result in a decrease in equity.

B) A cost that provides future economic benefits is treated as an asset.

C) To accountants the terms cost and expense always mean the same thing.

D) Many costs eventually become expenses.

A) An expense is the consumption or loss of resources that will result in a decrease in equity.

B) A cost that provides future economic benefits is treated as an asset.

C) To accountants the terms cost and expense always mean the same thing.

D) Many costs eventually become expenses.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

6

Which of these is an example of a period cost?

A) Direct materials

B) Production supervisor's salary

C) Sales salaries

D) Factory rent

A) Direct materials

B) Production supervisor's salary

C) Sales salaries

D) Factory rent

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

7

15. Which of these would normally be classified as direct materials?

Sheet metal used in making tractors, Lubricants used on production machinery, Plastic used in making calculators

A) Yes Yes Yes

B) Yes No Yes

C) No Yes No

D) No No Yes

Sheet metal used in making tractors, Lubricants used on production machinery, Plastic used in making calculators

A) Yes Yes Yes

B) Yes No Yes

C) No Yes No

D) No No Yes

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

8

Raw materials inventory is:

A) stock of materials purchased for conversion into saleable goods.

B) stock of supplies.

C) stock of partly finished goods.

D) materials that have been scrapped.

A) stock of materials purchased for conversion into saleable goods.

B) stock of supplies.

C) stock of partly finished goods.

D) materials that have been scrapped.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

9

Although the terms cost and expense are often used synonymously there is a difference between them. A cost can be an asset or an expense whereas an expense is:

A) the consumption or loss of resources that will result in a decrease in equity.

B) where the future economic benefits have not expired.

C) used to run the business.

D) paid out in cash.

A) the consumption or loss of resources that will result in a decrease in equity.

B) where the future economic benefits have not expired.

C) used to run the business.

D) paid out in cash.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

10

What is the correct order in which the flow of costs in a manufacturing organisation occurs?

I) Charge raw materials, direct labour and factory overhead to work in process

Ii) Purchase stocks of raw materials

Iii) Transfer finished goods to cost of sales

Iv) Transfer finished goods to stock of finished goods

A) i, ii, iii, iv

B) ii, i, iii, iv

C) ii, i, iv, iii

D) ii, iii, i, iv

I) Charge raw materials, direct labour and factory overhead to work in process

Ii) Purchase stocks of raw materials

Iii) Transfer finished goods to cost of sales

Iv) Transfer finished goods to stock of finished goods

A) i, ii, iii, iv

B) ii, i, iii, iv

C) ii, i, iv, iii

D) ii, iii, i, iv

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

11

If projected factory overhead is $360 000 p.a. and projected direct labour hours are 60 000 hours p.a., the overhead application rate is:

A) $60 000.

B) $6 per direct labour hour.

C) $360 000.

D) $0.60 per direct labour hour.

A) $60 000.

B) $6 per direct labour hour.

C) $360 000.

D) $0.60 per direct labour hour.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

12

Issues that must be resolved in accounting for factory overhead are all of the following except:

A) the allocation of common costs between activities.

B) the allocation of product costs.

C) the assignment of service department costs to production departments.

D) how to assign factory overhead costs as product costs.

A) the allocation of common costs between activities.

B) the allocation of product costs.

C) the assignment of service department costs to production departments.

D) how to assign factory overhead costs as product costs.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

13

How many of these inventory accounts are maintained by a manufacturer?

Stock of raw materials

Stock of work in process

Stock of finished goods

A) 0

B) 1

C) 2

D) 3

Stock of raw materials

Stock of work in process

Stock of finished goods

A) 0

B) 1

C) 2

D) 3

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

14

Costs which are not directly required to produce a product but are expensed in the income statement in the period in which they are incurred are called:

A) product costs.

B) other costs.

C) period costs.

D) fixed costs.

A) product costs.

B) other costs.

C) period costs.

D) fixed costs.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

15

How many of the following are reasons why managers need information on manufacturing costs?

Inventory valuation

Profit determination

Evaluation of past performance

Pricing

A) 1

B) 2

C) 3

D) 4

Inventory valuation

Profit determination

Evaluation of past performance

Pricing

A) 1

B) 2

C) 3

D) 4

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

16

Which of these is an example of a product cost?

A) Telephone expense

B) Assembly line worker's wages

C) Depreciation of office furniture

D) Interest expense

A) Telephone expense

B) Assembly line worker's wages

C) Depreciation of office furniture

D) Interest expense

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

17

Work in process inventory is:

A) raw materials that have not been paid for.

B) product that has been partly processed.

C) inventory that is subject to a legal dispute.

D) work that is in the planning process.

A) raw materials that have not been paid for.

B) product that has been partly processed.

C) inventory that is subject to a legal dispute.

D) work that is in the planning process.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

18

Which of these is not a product cost:

A) factory power.

B) wages of factory workers.

C) material used in production.

D) advertising of a new product.

A) factory power.

B) wages of factory workers.

C) material used in production.

D) advertising of a new product.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

19

Product costs are integral to the production of a product and are expensed in the period in which the:

A) related units are sold.

B) related units are produced.

C) costs are paid.

D) costs are incurred.

A) related units are sold.

B) related units are produced.

C) costs are paid.

D) costs are incurred.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following statements is correct?

A) Items such as glue, nails and screws become part of the finished product but are usually classified as factory overhead.

B) The cost of collecting debts from customers is classified as part of factory overhead.

C) Power used for factory lighting and heating is classified as a period cost.

D) Absorption costing splits up factory costs into product and period costs.

A) Items such as glue, nails and screws become part of the finished product but are usually classified as factory overhead.

B) The cost of collecting debts from customers is classified as part of factory overhead.

C) Power used for factory lighting and heating is classified as a period cost.

D) Absorption costing splits up factory costs into product and period costs.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

21

Direct material costs do not include small items that it is uneconomical to trace to products. Which of the following would not be included as a direct materials cost for a furniture manufacturer?

A) Wood

B) Materials

C) Glue

D) Handles

A) Wood

B) Materials

C) Glue

D) Handles

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

22

The true statement in relation to direct costing is:

A) it only recognised direct materials as a product cost.

B) it is sometimes called adaptable costing.

C) it treats all costs as period costs.

D) it only recognises as product costs those factory costs that vary with production.

A) it only recognised direct materials as a product cost.

B) it is sometimes called adaptable costing.

C) it treats all costs as period costs.

D) it only recognises as product costs those factory costs that vary with production.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

23

If expected factory overhead costs are $600 000 and expected direct labour hours are 40 000, what is the overhead application rate per direct labour hour?

A) $15

B) $150

C) $0.66

D) $66

A) $15

B) $150

C) $0.66

D) $66

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

24

Accounting standard IAS 2/AASB 102:

A) only allows the use of direct costing for external financial reporting purposes.

B) allows the use of direct costing and absorption costing for external financial reporting purposes.

C) only allows the use of absorption costing for external financial reporting purposes.

D) does not allow the use of either direct costing or absorption costing for external financial reporting purposes.

A) only allows the use of direct costing for external financial reporting purposes.

B) allows the use of direct costing and absorption costing for external financial reporting purposes.

C) only allows the use of absorption costing for external financial reporting purposes.

D) does not allow the use of either direct costing or absorption costing for external financial reporting purposes.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

25

Direct material costs plus direct labour costs are known as:

A) prime costs.

B) conversion costs.

C) fixed costs.

D) period costs.

A) prime costs.

B) conversion costs.

C) fixed costs.

D) period costs.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

26

A clothing manufacturer has a production department where the clothing is produced and two other departments, a warehouse and a general office, which are known as:

A) auxiliary departments.

B) minor departments.

C) service departments.

D) training departments.

A) auxiliary departments.

B) minor departments.

C) service departments.

D) training departments.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

27

Indirect materials and indirect labour incurred by the factory are classed as:

A) factory overhead.

B) fixed costs.

C) administrative expenses.

D) period costs.

A) factory overhead.

B) fixed costs.

C) administrative expenses.

D) period costs.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

28

Costs that remain constant in total (over the relevant range) as the volume of production changes are known as:

A) indirect costs.

B) direct costs.

C) variable costs.

D) fixed costs.

A) indirect costs.

B) direct costs.

C) variable costs.

D) fixed costs.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

29

Which of these is an example of a fixed cost?

A) Factory rental

B) Factory bonuses linked to the level of production

C) Packaging costs

D) Raw materials

A) Factory rental

B) Factory bonuses linked to the level of production

C) Packaging costs

D) Raw materials

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

30

If total fixed costs are $250 000 what is the per unit overhead cost for Maxima Ltd if 50 000 units are produced? Assume units of production are used as the basis for applying overhead to product.

A) $50

B) $5

C) $0.50

D) $0.05

A) $50

B) $5

C) $0.50

D) $0.05

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

31

Costs can be classified into those that are traceable to products and those that are non- traceable. The costs of raw materials that are directly and economically traceable as an integral part of a product, are called:

A) direct materials costs.

B) direct labour costs.

C) factory overhead costs.

D) cost of sales.

A) direct materials costs.

B) direct labour costs.

C) factory overhead costs.

D) cost of sales.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

32

For a manufacturer all factory costs that are not directly traceable to products are classed as:

A) indirect materials.

B) period costs.

C) factory overhead.

D) variable costs.

A) indirect materials.

B) period costs.

C) factory overhead.

D) variable costs.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

33

Variable costs:

A) remain constant in total regardless of the level of output.

B) increase per unit as output increases.

C) decrease per unit as output decreases.

D) remain constant per unit regardless of the level of output.

A) remain constant in total regardless of the level of output.

B) increase per unit as output increases.

C) decrease per unit as output decreases.

D) remain constant per unit regardless of the level of output.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

34

If total fixed costs are $25 000 what is the per unit overhead cost for R Co if 5000 units are produced? Assume units of production are used as the basis for applying overhead to product.

A) $50

B) $5

C) $0.50

D) $0.05

A) $50

B) $5

C) $0.50

D) $0.05

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

35

Variable costs:

A) remain constant in total regardless of the level of output.

B) increase per unit as output increases.

C) decrease per unit as output decreases.

D) remain constant per unit regardless of the level of output.

A) remain constant in total regardless of the level of output.

B) increase per unit as output increases.

C) decrease per unit as output decreases.

D) remain constant per unit regardless of the level of output.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

36

If the overhead application rate is $10 per direct labour hour and 120 direct labour hours are used in printing a text book how much overhead is included in the total production cost of the book?

A) $10

B) $120

C) $1200

D) $12 000

A) $10

B) $120

C) $1200

D) $12 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

37

The costs of the two service departments, maintenance and quality control, that provide support for the production departments are classed as:

A) factory overhead.

B) selling expenses.

C) administrative expenses.

D) finance expenses.

A) factory overhead.

B) selling expenses.

C) administrative expenses.

D) finance expenses.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

38

Applying overhead to products means:

A) passing on the overhead costs to customers in the price charged.

B) assigning the overhead on a basis that closely relates it to the work performed.

C) directly tracing the overhead to products.

D) calculating the total overhead cost.

A) passing on the overhead costs to customers in the price charged.

B) assigning the overhead on a basis that closely relates it to the work performed.

C) directly tracing the overhead to products.

D) calculating the total overhead cost.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

39

Direct labour costs plus factory overhead costs are known as:

A) prime costs.

B) conversion costs.

C) direct costs.

D) variable costs.

A) prime costs.

B) conversion costs.

C) direct costs.

D) variable costs.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

40

In calculating product costs the wages paid to employees whose time can be directly traced to products are classified as:

A) indirect labour costs.

B) direct labour costs.

C) factory overhead.

D) fixed costs.

A) indirect labour costs.

B) direct labour costs.

C) factory overhead.

D) fixed costs.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

41

Kid Gloves Manufacturing reports the following information for the year. Determine the cost of finished goods manufactured.

Work in process 1 January $7 000

Work in process 31 December 10 000

Finished goods inventory 1 January 5 000

Finished goods inventory 31 December 6 000

Direct materials used 3 000

Direct labour 2 000

Factory overhead 2 000

Selling expenses 3 000

General and administrative expenses 4 000

A) $4000

B) $3000

C) $5000

D) $6000

Work in process 1 January $7 000

Work in process 31 December 10 000

Finished goods inventory 1 January 5 000

Finished goods inventory 31 December 6 000

Direct materials used 3 000

Direct labour 2 000

Factory overhead 2 000

Selling expenses 3 000

General and administrative expenses 4 000

A) $4000

B) $3000

C) $5000

D) $6000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

42

Before the application of overhead costs Chrome & Steel Ltd has the following costs traced to production:

Direct materials Direct labour

Charged to production $50 000 $40 000

Assuming that overhead is applied at the rate of 80% of direct labour cost what is the amount of inventory finished for the period (assume no work in process)?

A) $50 000

B) $90 000

C) $122 000

D) $130 000

Direct materials Direct labour

Charged to production $50 000 $40 000

Assuming that overhead is applied at the rate of 80% of direct labour cost what is the amount of inventory finished for the period (assume no work in process)?

A) $50 000

B) $90 000

C) $122 000

D) $130 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

43

These figures have been extracted from the trial balance of ABC Ltd for June 2014:

Direct materials $5 000

Light and power factory 14 000

Freight outwards 2 000

Office salaries 11 000

Depreciation on factory plant 6 000

Directors' fees 7 000

Salesmen's commission 8 000

Factory wages - direct 30 000

- indirect 10 000

There was no opening or closing work in process. What are total factory overhead expenses?

A) $35 000

B) $30 000

C) $60 000

D) $20 000

Direct materials $5 000

Light and power factory 14 000

Freight outwards 2 000

Office salaries 11 000

Depreciation on factory plant 6 000

Directors' fees 7 000

Salesmen's commission 8 000

Factory wages - direct 30 000

- indirect 10 000

There was no opening or closing work in process. What are total factory overhead expenses?

A) $35 000

B) $30 000

C) $60 000

D) $20 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

44

Assume direct materials, direct labour and factory overhead for the period total $700 000. If work in process at the start is $55 000 and work in process at the end is $40 000, what is the cost of goods manufactured?

A) $700 000

B) $735 000

C) $685 000

D) $715 000

A) $700 000

B) $735 000

C) $685 000

D) $715 000

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

45

What type of business would calculate cost of sales in the income statement as stock of finished goods at start + purchases - stock of finished goods at end?

A) A carpet factory

B) manufacturer private school

C) A lawyer

D) A shoe shop

A) A carpet factory

B) manufacturer private school

C) A lawyer

D) A shoe shop

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

46

A fixed cost is one that:

A) is the same per unit of production regardless of volume.

B) remains constant in total within the relevant production range.

C) increases on a per unit basis as volume increases.

D) does not rise as inflation changes.

A) is the same per unit of production regardless of volume.

B) remains constant in total within the relevant production range.

C) increases on a per unit basis as volume increases.

D) does not rise as inflation changes.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

47

In relation to the cost of goods manufactured report which is not a correct statement?

A) The ending work in process is subtracted to obtain the cost of completed goods manufactured for the period.

B) Cost of goods manufactured is transferred to the cost of sales account.

C) It is prepared to calculate the cost of goods completed in the period.

D) The total of direct materials, direct labour and factory overhead represent the manufacturing costs for the period.

A) The ending work in process is subtracted to obtain the cost of completed goods manufactured for the period.

B) Cost of goods manufactured is transferred to the cost of sales account.

C) It is prepared to calculate the cost of goods completed in the period.

D) The total of direct materials, direct labour and factory overhead represent the manufacturing costs for the period.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

48

A) $8000.

B) $10 000.

C) $13 000.

D) $18 000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

49

The format for the cost of goods manufactured statement is direct materials + direct labour + factory overhead + ????????__________ - work in process at end.

A) Indirect materials

B) Work in process at start

C) Indirect materials

D) Indirect labour

A) Indirect materials

B) Work in process at start

C) Indirect materials

D) Indirect labour

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

50

Mega Manufacturing's accounting records provide the following information. What is the business direct material cost for the period?

Cost of goods manufactured is $35 000

Ending work in process is $11 500

Manufacturing overhead is $12 700

Direct labour is $8 900

Beginning work in process is $7 500

A) $17 400

B) $13 400

C) $9400

D) $6400

Cost of goods manufactured is $35 000

Ending work in process is $11 500

Manufacturing overhead is $12 700

Direct labour is $8 900

Beginning work in process is $7 500

A) $17 400

B) $13 400

C) $9400

D) $6400

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

51

What type of business would calculate cost of sales in the income statement as stock of finished goods at start + purchases - stock of finished goods at end?

A) A service business

B) A manufacturer

C) A retailer

D) A non-profit organisation

A) A service business

B) A manufacturer

C) A retailer

D) A non-profit organisation

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

52

What is the statement prepared by a manufacturer to calculate the cost of the goods manufactured called?

A) Statement of cost of sales

B) Income statement

C) Gross profit statement

D) Cost of goods manufactured statement

A) Statement of cost of sales

B) Income statement

C) Gross profit statement

D) Cost of goods manufactured statement

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

53

Calculate product cost per unit.

Direct materials per unit $50

Direct labour per unit $30

Factory overhead applied at 50% of direct labour cost

A) $50

B) $80

C) $95

D) $105

Direct materials per unit $50

Direct labour per unit $30

Factory overhead applied at 50% of direct labour cost

A) $50

B) $80

C) $95

D) $105

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

54

Assume Coburg Heaters issued $50 500 of direct materials to production, total direct labour costs were $30 000 and total overhead costs were $30 000. If work in process at the start was $10 000 and work in process at the end was $12 000, what is the total cost of goods manufactured for the period?

A) $50 500

B) $80 500

C) $110 500

D) $108 500

A) $50 500

B) $80 500

C) $110 500

D) $108 500

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

55

A) $50 000.

B) $60 000.

C) $55 000.

D) $45 000.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

56

Any increase in unit product cost must result in a decreased profit margin if the selling price of the product cannot be:

A) measured.

B) decreased.

C) increased.

D) calculated.

A) measured.

B) decreased.

C) increased.

D) calculated.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

57

In the general ledger the accounts used to determine the cost of goods manufactured are closed to the manufacturing summary account which is then closed to the:

A) income summary account.

B) cost of sales account.

C) gross profit account.

D) profit account.

A) income summary account.

B) cost of sales account.

C) gross profit account.

D) profit account.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

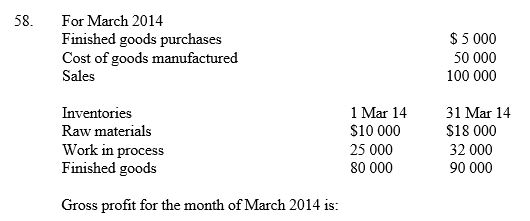

58

When preparing a cost of goods manufactured statement from the following information, what is the total cost of goods manufactured?

Direct materials $6

Advertising expenses 3

Indirect labour 1

Indirect materials 5

Direct labour 2

Other manufacturing overhead 3

A) $23

B) $20

C) $17

D) $16

Direct materials $6

Advertising expenses 3

Indirect labour 1

Indirect materials 5

Direct labour 2

Other manufacturing overhead 3

A) $23

B) $20

C) $17

D) $16

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

59

For a manufacturer, if cost of goods manufactured is $652 000, stock of finished goods at start is $40 000 and stock of finished goods at end is $36 000, calculate the cost of sales.

A) $728 000

B) $648 000

C) $656 000

D) Cannot be calculated with the information available

A) $728 000

B) $648 000

C) $656 000

D) Cannot be calculated with the information available

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

60

In a manufacturing organisation the transfer from the work in process inventory account to the finished goods inventory account represents:

A) work in process at the end of the period.

B) total manufacturing costs incurred for the period.

C) cost of goods finished during the period.

D) cost of sales.

A) work in process at the end of the period.

B) total manufacturing costs incurred for the period.

C) cost of goods finished during the period.

D) cost of sales.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

61

Sustainable manufacturing is of importance to how many of these groups?

I) Management

Ii) Government

Iii) Customers

Iv) Public at large

A) 1

B) 2

C) 3

D) 4

I) Management

Ii) Government

Iii) Customers

Iv) Public at large

A) 1

B) 2

C) 3

D) 4

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

62

Which of the following statements is incorrect?

A) Today, with automation and computerisation, factory overhead costs are often a higher proportion of total manufacturing costs than direct labour costs.

B) A manufacturing entity using a periodic inventory system must rely on the judgement of the accountant and/or the production manager to estimate the value of ending work in process.

C) An overhead application rate is an historical rate.

D) The direct labour rate per unit of output is constant but total direct labour costs increase with an increase in the level of production.

A) Today, with automation and computerisation, factory overhead costs are often a higher proportion of total manufacturing costs than direct labour costs.

B) A manufacturing entity using a periodic inventory system must rely on the judgement of the accountant and/or the production manager to estimate the value of ending work in process.

C) An overhead application rate is an historical rate.

D) The direct labour rate per unit of output is constant but total direct labour costs increase with an increase in the level of production.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

63

For a manufacturer a periodic inventory system has many limitations and deficiencies. These limitations____________ the number of products and producing departments.

A) decrease with

B) increase with

C) are unaffected by

D) are equal to

A) decrease with

B) increase with

C) are unaffected by

D) are equal to

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

64

Which of the following statements concerning sustainable manufacturing is correct?

A) Manufacturing in a sustainable way always involves higher manufacturing costs.

B) Recycling can occur within the production process or at the end of the product's useful life.

C) Businesses in Australia have little interest in sustainable manufacturing.

D) Businesses that operate sustainably make less profit than businesses that ignore sustainability.

A) Manufacturing in a sustainable way always involves higher manufacturing costs.

B) Recycling can occur within the production process or at the end of the product's useful life.

C) Businesses in Australia have little interest in sustainable manufacturing.

D) Businesses that operate sustainably make less profit than businesses that ignore sustainability.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

65

Which of these is a not a limitation of the use of a periodic inventory system by a manufacturer?

A) Costing information is not available before the end of the accounting period.

B) A physical stocktake is necessary before costing information can be determined.

C) The costing information contains estimations and approximations.

D) The method is more costly to implement than the perpetual method.

A) Costing information is not available before the end of the accounting period.

B) A physical stocktake is necessary before costing information can be determined.

C) The costing information contains estimations and approximations.

D) The method is more costly to implement than the perpetual method.

Unlock Deck

Unlock for access to all 65 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 65 flashcards in this deck.