Deck 31: Associates and Joint Ventures

Full screen (f)

Question

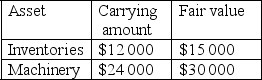

On 1 July 20X3 Alpha Ltd acquired a 25% share of Beta Ltd. At that date the following assets had carrying amounts different to their fair values in Beta's books:

All inventories were sold to third parties by 30 June 20X4. On 1 July 20X3, the machinery had a remaining useful life of 3 years.

The tax rate is 30%.

The adjustment required to the Investment in Associate account at 30 June 20X4 in relation to the above assets is:

A) $875

B) $1250

C) $3500

D) $5000

All inventories were sold to third parties by 30 June 20X4. On 1 July 20X3, the machinery had a remaining useful life of 3 years.

The tax rate is 30%.

The adjustment required to the Investment in Associate account at 30 June 20X4 in relation to the above assets is:

A) $875

B) $1250

C) $3500

D) $5000

Question

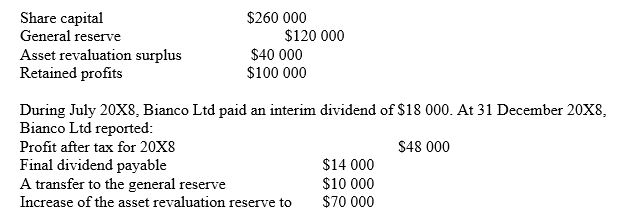

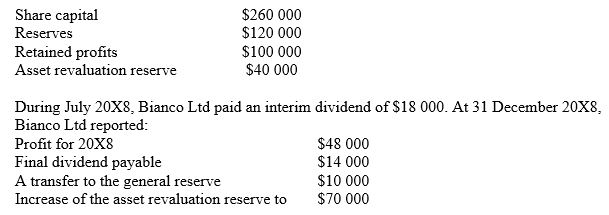

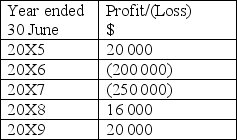

Nero Ltd purchased a 30% shareholding in Bianco Ltd on 1 January 20X8 for $180 000. Bianco Ltd's assets were recorded at fair values and its owners' equity, totalling $520 000, was represented as follows:

The equity carrying amount of the investment in Bianco Ltd at 31 December 20X8 is:

The equity carrying amount of the investment in Bianco Ltd at 31 December 20X8 is:

A) $193 800.

B) $202 200.

C) $203 400.

D) $211 200.

The equity carrying amount of the investment in Bianco Ltd at 31 December 20X8 is:A) $193 800.

B) $202 200.

C) $203 400.

D) $211 200.

Question

Question

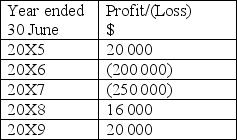

On 1 July 20X4 Joey Ltd acquired 25% of the shares of Leo Ltd for $100 000. At that date the equity of Leo Ltd was $400 000, with all identifiable assets and liabilities being measured at fair value. Profits/(losses) made since the date of acquisition are as follows:

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 20X6 the equity accounted balance of the investment in Leo was:

A) $50 000.

B) $55 000.

C) $100 000.

D) $105 000.

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 20X6 the equity accounted balance of the investment in Leo was:

A) $50 000.

B) $55 000.

C) $100 000.

D) $105 000.

Question

Question

Question

Question

The equity method of accounting for an investment in an associate includes the following steps:

A) I.

B) II.

C) III.

D) IV.

A) I.

B) II.

C) III.

D) IV.

Question

Question

Question

Question

The following are regarded as factors indicating the existence of significant influence over another entity:

A) I.

B) II.

C) III.

D) IV.

A) I.

B) II.

C) III.

D) IV.

Question

Question

Question

Question

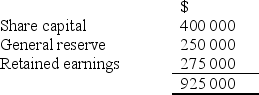

On 1 July 20X8 Berardo Ltd acquired 25% of the ordinary issued share capital of Ricky Ltd for $375 000. This investment gave rise to significant influence.

The share capital and reserves of Ricky Ltd at 1 July 20X8 were:

All the identifiable net assets of Ricky Ltd were stated at fair value at the date of acquisition except for a building whose carrying value was $50 000 less than the fair value. Goodwill arising on Berardo's acquisition of Ricky was:

A) $131 250

B) $135 000

C) $143 750

D) $150 000

The share capital and reserves of Ricky Ltd at 1 July 20X8 were:

All the identifiable net assets of Ricky Ltd were stated at fair value at the date of acquisition except for a building whose carrying value was $50 000 less than the fair value. Goodwill arising on Berardo's acquisition of Ricky was:

A) $131 250

B) $135 000

C) $143 750

D) $150 000

Question

Question

Nero Ltd purchased a 30% shareholding in Bianco Ltd on 1 January 20X8 for $180 000. Bianco Ltd's assets were recorded at fair values and its owners' equity, totalling $520 000, was represented as follows:

Assuming that Nero Ltd applies the equity method in its own books, the entry to record the dividend receivable from Bianco Ltd at 31 December 20X9 would include:

A) a credit to the dividend revenue account.

B) a credit to the investment in associate account.

C) a debit to the dividend revenue account.

D) a debit to the investment in associate account.

Assuming that Nero Ltd applies the equity method in its own books, the entry to record the dividend receivable from Bianco Ltd at 31 December 20X9 would include:

A) a credit to the dividend revenue account.

B) a credit to the investment in associate account.

C) a debit to the dividend revenue account.

D) a debit to the investment in associate account.

Question

Question

Question

On 1 July 20X4 Joey Ltd acquired 25% of the shares of Leo Ltd for $100 000. At that date the equity of Leo Ltd was $400 000, with all identifiable assets and liabilities being measured at fair value. Profits/(losses) made since the date of acquisition are as follows:

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 20X8 the equity accounted balance of the investment in Leo was:

A) nil.

B) ($3500).

C) $4000.

D) $16 000.

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 20X8 the equity accounted balance of the investment in Leo was:

A) nil.

B) ($3500).

C) $4000.

D) $16 000.

Question

Question

Question

On 1 July 20X4 Joey Ltd acquired 25% of the shares of Leo Ltd for $100 000. At that date the equity of Leo Ltd was $400 000, with all identifiable assets and liabilities being measured at fair value. Profits/(losses) made since the date of acquisition are as follows:

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 20X9 the equity accounted balance of the investment in Leo was:

A) nil.

B) $1500.

C) $5000.

D) $20 000.

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 20X9 the equity accounted balance of the investment in Leo was:

A) nil.

B) $1500.

C) $5000.

D) $20 000.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/26

Play

Full screen (f)

Deck 31: Associates and Joint Ventures

1

On 1 July 20X3 Alpha Ltd acquired a 25% share of Beta Ltd. At that date the following assets had carrying amounts different to their fair values in Beta's books:

All inventories were sold to third parties by 30 June 20X4. On 1 July 20X3, the machinery had a remaining useful life of 3 years.

The tax rate is 30%.

The adjustment required to the Investment in Associate account at 30 June 20X4 in relation to the above assets is:

A) $875

B) $1250

C) $3500

D) $5000

All inventories were sold to third parties by 30 June 20X4. On 1 July 20X3, the machinery had a remaining useful life of 3 years.

The tax rate is 30%.

The adjustment required to the Investment in Associate account at 30 June 20X4 in relation to the above assets is:

A) $875

B) $1250

C) $3500

D) $5000

A

2

Nero Ltd purchased a 30% shareholding in Bianco Ltd on 1 January 20X8 for $180 000. Bianco Ltd's assets were recorded at fair values and its owners' equity, totalling $520 000, was represented as follows:

The equity carrying amount of the investment in Bianco Ltd at 31 December 20X8 is:

A) $193 800.

B) $202 200.

C) $203 400.

D) $211 200.

The equity carrying amount of the investment in Bianco Ltd at 31 December 20X8 is:A) $193 800.

B) $202 200.

C) $203 400.

D) $211 200.

A

3

When goodwill is acquired by an investor in an associate, the amortisation of goodwill is:

A) spread evenly across the useful life of the investment.

B) not permitted.

C) included in the determination of the investor's share of the associate's profit or loss.

D) included in the revaluation of the investment.

A) spread evenly across the useful life of the investment.

B) not permitted.

C) included in the determination of the investor's share of the associate's profit or loss.

D) included in the revaluation of the investment.

B

4

On 1 July 20X4 Joey Ltd acquired 25% of the shares of Leo Ltd for $100 000. At that date the equity of Leo Ltd was $400 000, with all identifiable assets and liabilities being measured at fair value. Profits/(losses) made since the date of acquisition are as follows:

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 20X6 the equity accounted balance of the investment in Leo was:

A) $50 000.

B) $55 000.

C) $100 000.

D) $105 000.

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 20X6 the equity accounted balance of the investment in Leo was:

A) $50 000.

B) $55 000.

C) $100 000.

D) $105 000.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

5

Clovelly Ltd owns 25% of Bronte Ltd. Bronte's profit after tax for the year ended 30 June 20X5 is $30 000. The tax rate is 30%. On 1 July 20X3, Bronte Ltd sold an item of plant to Clovelly Ltd for $8000. The carrying amount of the asset on this date in Bronte Ltd's records was $3000. The plant had a remaining useful life of 5 years. Clovelly's share of Bronte's profit for the year ended 30 June 20X5 is:

A) $6800.

B) $7325.

C) $7675.

D) $7750.

A) $6800.

B) $7325.

C) $7675.

D) $7750.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

6

For the purposes of equity accounting, significant influence is regarded as the power of an investor to:

A) control the financial and operating policies of an associate.

B) participate in the financial and operating policy decisions of an investee.

C) participate in the day-to-day management of a joint venture interest.

D) dominate the financing decisions of an entity.

A) control the financial and operating policies of an associate.

B) participate in the financial and operating policy decisions of an investee.

C) participate in the day-to-day management of a joint venture interest.

D) dominate the financing decisions of an entity.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

7

For the purposes of equity accounting for an investment in an associate, it is presumed that the investor has significant influence over the other entity where the investor holds:

A) between 1% and 5% of the voting power of the investee.

B) between 5% and 10% of the voting power of the investee.

C) 20% or more of the voting power of the investee.

D) 50% or more of the voting power of the investee.

A) between 1% and 5% of the voting power of the investee.

B) between 5% and 10% of the voting power of the investee.

C) 20% or more of the voting power of the investee.

D) 50% or more of the voting power of the investee.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

8

The equity method of accounting for an investment in an associate includes the following steps:

A) I.

B) II.

C) III.

D) IV.

A) I.

B) II.

C) III.

D) IV.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

9

Where there are transactions between the investor and associate that result in an unrealised profit, the investor's share of the associate's profit is:

A) not affected at all regardless of whether the transaction is an upstream or downstream one.

B) affected only if the transaction is an upstream one.

C) affected only if the transaction is a downstream one.

D) affected regardless of whether the transaction is an upstream or downstream one.

A) not affected at all regardless of whether the transaction is an upstream or downstream one.

B) affected only if the transaction is an upstream one.

C) affected only if the transaction is a downstream one.

D) affected regardless of whether the transaction is an upstream or downstream one.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following statements is correct?

A) All joint arrangements are accounted for under AASB 128/IAS 28.

B) Joint arrangements classified as joint ventures are accounted for under AASB 11.

C) Joint arrangements classified as joint ventures are accounted for under AASB 128/IAS 28.

D) Joint arrangements classified as joint operations are accounted for under AASB 128/IAS 28.

A) All joint arrangements are accounted for under AASB 128/IAS 28.

B) Joint arrangements classified as joint ventures are accounted for under AASB 11.

C) Joint arrangements classified as joint ventures are accounted for under AASB 128/IAS 28.

D) Joint arrangements classified as joint operations are accounted for under AASB 128/IAS 28.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

11

Where an investor sells inventories to an associate and the inventories are still on hand at the end of the year the investor's share of the associate's profits is:

A) not affected as unrealised profits are only considered to arise in a parent-subsidiary relationship.

B) not affected as the unrealised profit is in the books of the investor, not the associate.

C) increased by the investor's share of the unrealised profit.

D) decreased by the investor's share of the unrealised profit.

A) not affected as unrealised profits are only considered to arise in a parent-subsidiary relationship.

B) not affected as the unrealised profit is in the books of the investor, not the associate.

C) increased by the investor's share of the unrealised profit.

D) decreased by the investor's share of the unrealised profit.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

12

The following are regarded as factors indicating the existence of significant influence over another entity:

A) I.

B) II.

C) III.

D) IV.

A) I.

B) II.

C) III.

D) IV.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

13

Gunawan Limited acquired a 20% share in Juliano Limited for $18 000. Gunawan Limited has no other investments. At the date on which it became an associate, Juliano Limited had the following equity (which reflected the fair value of net assets on that date):

Share capital $50 000

Retained earnings $40 000

At the end of the financial year following the investment, Juliano Limited generated a profit of $6000. After applying the equity method of accounting, Gunawan Limited will have the following carrying amount for the investment:

A) $9 200

B) $16 800

C) $18 000

D) $19 200

Share capital $50 000

Retained earnings $40 000

At the end of the financial year following the investment, Juliano Limited generated a profit of $6000. After applying the equity method of accounting, Gunawan Limited will have the following carrying amount for the investment:

A) $9 200

B) $16 800

C) $18 000

D) $19 200

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

14

Where an acquisition in an associate results in an excess the excess is accounted for in the year of acquisition as follows:

A) as a credit against the investment in associate account.

B) as a credit against the share of associate profit account.

C) as a debit against the share of associates retained earnings.

D) no adjustment is required due to the single line method of accounting followed under the equity method.

A) as a credit against the investment in associate account.

B) as a credit against the share of associate profit account.

C) as a debit against the share of associates retained earnings.

D) no adjustment is required due to the single line method of accounting followed under the equity method.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

15

Clovelly Ltd, owns 25% of Bronte Ltd. Bronte's profit after tax for the year ended 30 June 20X3 is $30 000. The tax rate is 30%. During the year ended 30 June 20X4, Bronte sold $5000 worth of inventories to Clovelly. These items had previously cost Bronte $3000. All the items remain unsold by the Clovelly at 30 June 20X3. Clovelly's share of Bronte's profit for the year ended 30 June 20X3 is:

A) $5500.

B) $6250.

C) $7150.

D) $7000.

A) $5500.

B) $6250.

C) $7150.

D) $7000.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

16

On 1 July 20X8 Berardo Ltd acquired 25% of the ordinary issued share capital of Ricky Ltd for $375 000. This investment gave rise to significant influence.

The share capital and reserves of Ricky Ltd at 1 July 20X8 were:

All the identifiable net assets of Ricky Ltd were stated at fair value at the date of acquisition except for a building whose carrying value was $50 000 less than the fair value. Goodwill arising on Berardo's acquisition of Ricky was:

A) $131 250

B) $135 000

C) $143 750

D) $150 000

The share capital and reserves of Ricky Ltd at 1 July 20X8 were:

All the identifiable net assets of Ricky Ltd were stated at fair value at the date of acquisition except for a building whose carrying value was $50 000 less than the fair value. Goodwill arising on Berardo's acquisition of Ricky was:

A) $131 250

B) $135 000

C) $143 750

D) $150 000

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

17

Adjustments made for the purpose of calculating the incremental adjustment to the share of profit of an associate are:

A) recognised in the books of the investor.

B) recognised in the books of the investee.

C) notional adjustments and not recorded in the books of the investee.

D) relate to realised transactions and so are recognised directly by the investee.

A) recognised in the books of the investor.

B) recognised in the books of the investee.

C) notional adjustments and not recorded in the books of the investee.

D) relate to realised transactions and so are recognised directly by the investee.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

18

Nero Ltd purchased a 30% shareholding in Bianco Ltd on 1 January 20X8 for $180 000. Bianco Ltd's assets were recorded at fair values and its owners' equity, totalling $520 000, was represented as follows:

Assuming that Nero Ltd applies the equity method in its own books, the entry to record the dividend receivable from Bianco Ltd at 31 December 20X9 would include:

A) a credit to the dividend revenue account.

B) a credit to the investment in associate account.

C) a debit to the dividend revenue account.

D) a debit to the investment in associate account.

Assuming that Nero Ltd applies the equity method in its own books, the entry to record the dividend receivable from Bianco Ltd at 31 December 20X9 would include:

A) a credit to the dividend revenue account.

B) a credit to the investment in associate account.

C) a debit to the dividend revenue account.

D) a debit to the investment in associate account.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

19

Where an investor sells inventories to an associate in a prior year and the inventories are sold by the associate during the current year the investment in associate account is:

A) unaffected.

B) decreased by the investor's share of the realised profit.

C) increased by the investor's share of the realised profit.

D) increased by the full amount of the realised profit.

A) unaffected.

B) decreased by the investor's share of the realised profit.

C) increased by the investor's share of the realised profit.

D) increased by the full amount of the realised profit.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

20

Investor Limited acquired a 30% interest in Investee Limited for $27 000. Investor holds other equity investments but does not prepare consolidated financial statements. Investee Limited revalued its buildings class of assets by $10 000 during the current financial period. The balance of the Investment in Associate account at the end of the current financial period is:

A) $11 100.

B) $18 100.

C) $27 000.

D) $30 000.

A) $11 100.

B) $18 100.

C) $27 000.

D) $30 000.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

21

On 1 July 20X4 Joey Ltd acquired 25% of the shares of Leo Ltd for $100 000. At that date the equity of Leo Ltd was $400 000, with all identifiable assets and liabilities being measured at fair value. Profits/(losses) made since the date of acquisition are as follows:

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 20X8 the equity accounted balance of the investment in Leo was:

A) nil.

B) ($3500).

C) $4000.

D) $16 000.

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 20X8 the equity accounted balance of the investment in Leo was:

A) nil.

B) ($3500).

C) $4000.

D) $16 000.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

22

When disclosing information about investments in associates, AASB 12/IFRS 12 Disclosure of Interests in Other Entitites, requires separate disclosure of which of the following?

I - Carrying amounts of investments in associates, in the statement of financial position.

II - Share of profit or loss of associates, in the statement of profit or loss and other comprehensive income.

III - Shares of changes recognised directly in the associate's equity, in the statement of changes in equity.

IV - Unrecognised share of losses in associates, in the Notes to the accounts.

A) I, II, III and IV.

B) I, II and IV only.

C) II, III and IV only.

D) I, II and III only.

I - Carrying amounts of investments in associates, in the statement of financial position.

II - Share of profit or loss of associates, in the statement of profit or loss and other comprehensive income.

III - Shares of changes recognised directly in the associate's equity, in the statement of changes in equity.

IV - Unrecognised share of losses in associates, in the Notes to the accounts.

A) I, II, III and IV.

B) I, II and IV only.

C) II, III and IV only.

D) I, II and III only.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

23

Where an investor has discontinued the use of the equity method because the associate has incurred losses it must disclose the:

A) unrecognised share of current period and cumulative losses of the associate.

B) reason why it has discontinued the method.

C) accounting policy it has adopted in place of the equity method.

D) effect on the statement of changes in equity if it had continued to use the method.

A) unrecognised share of current period and cumulative losses of the associate.

B) reason why it has discontinued the method.

C) accounting policy it has adopted in place of the equity method.

D) effect on the statement of changes in equity if it had continued to use the method.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

24

On 1 July 20X4 Joey Ltd acquired 25% of the shares of Leo Ltd for $100 000. At that date the equity of Leo Ltd was $400 000, with all identifiable assets and liabilities being measured at fair value. Profits/(losses) made since the date of acquisition are as follows:

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 20X9 the equity accounted balance of the investment in Leo was:

A) nil.

B) $1500.

C) $5000.

D) $20 000.

There have been no dividends paid or movements in reserves since the date of acquisition.

At 30 June 20X9 the equity accounted balance of the investment in Leo was:

A) nil.

B) $1500.

C) $5000.

D) $20 000.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

25

If an associate incurs losses the investor is required to:

A) ignore the losses for the purposes of equity accounting adjustments.

B) recognise losses only to the point where the carrying amount is equal to the initial investment.

C) recognise losses to the point where the carrying amount of the investment is zero.

D) reclassify the investment as a current asset.

A) ignore the losses for the purposes of equity accounting adjustments.

B) recognise losses only to the point where the carrying amount is equal to the initial investment.

C) recognise losses to the point where the carrying amount of the investment is zero.

D) reclassify the investment as a current asset.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

26

Investments in associates accounted for using the equity method are presented in the statement of financial position amongst:

A) equity.

B) non-current liabilities.

C) current assets.

D) non-current assets.

A) equity.

B) non-current liabilities.

C) current assets.

D) non-current assets.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 26 flashcards in this deck.