Deck 18: Accounting Policies and Other Disclosures

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

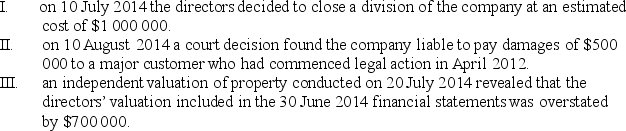

Prior to the finalisation of the financial statements for the year ended 30 June 2014, a company experienced a number of material events, including:

In respect of the events listed above, it will be necessary to adjust the financial statements, by way of general journal entries, for:

A) I, II and III.

B) II only, and make a note disclosure for I and III.

C) III only, and make a note disclosure for I and II.

D) II and III only, and make a note disclosure for I.

In respect of the events listed above, it will be necessary to adjust the financial statements, by way of general journal entries, for:

A) I, II and III.

B) II only, and make a note disclosure for I and III.

C) III only, and make a note disclosure for I and II.

D) II and III only, and make a note disclosure for I.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/14

Play

Full screen (f)

Deck 18: Accounting Policies and Other Disclosures

1

Correcting the recognition, measurement and disclosure of amounts of financial statement elements as if a prior period error had never occurred is known as:

A) historical restatement.

B) retrospective restatement.

C) retrospective application.

D) prior period application.

A) historical restatement.

B) retrospective restatement.

C) retrospective application.

D) prior period application.

B

2

Which of the following is not required to be disclosed in an entity's accounting policy note?

A) That the financial statements are general purpose financial statements.

B) The measurement bases used in the preparation of the financial statements.

C) That the financial statements have been prepared on the going concern basis.

D) A description of the entity's key accounting policies.

A) That the financial statements are general purpose financial statements.

B) The measurement bases used in the preparation of the financial statements.

C) That the financial statements have been prepared on the going concern basis.

D) A description of the entity's key accounting policies.

C

3

The correction of a material error that occurred in a previous period must be accounted for by:

A) ignoring it; errors made in prior periods can't be corrected.

B) an adjustment in future accounting periods.

C) a prospective adjustment to the financial statements.

D) a retrospective restatement in the first financial statements issued after the discovery of the error.

A) ignoring it; errors made in prior periods can't be corrected.

B) an adjustment in future accounting periods.

C) a prospective adjustment to the financial statements.

D) a retrospective restatement in the first financial statements issued after the discovery of the error.

D

4

If an accounting policy change is voluntary, which of the following disclosures is required by AASB 108/IAS 8?

A) The nature of the change.

B) The reasons that applying the new accounting policy provides reliable and more relevant information.

C) The amount of the adjustment relating to periods prior to those presented to the extent practicable.

D) All of the options are correct.

A) The nature of the change.

B) The reasons that applying the new accounting policy provides reliable and more relevant information.

C) The amount of the adjustment relating to periods prior to those presented to the extent practicable.

D) All of the options are correct.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

5

According to AASB 108, omissions or misstatements are material if they:

A) are greater than 10% of the relevant base amount.

B) are as a result of fraud.

C) could influence the economic decisions that users make on the basis of the financial statements.

D) are less than 10% of the relevant base amount.

A) are greater than 10% of the relevant base amount.

B) are as a result of fraud.

C) could influence the economic decisions that users make on the basis of the financial statements.

D) are less than 10% of the relevant base amount.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

6

Events occurring after the end of the reporting period which provide evidence of conditions that existed at the end of the reporting period are known as:

A) non-adjusting events.

B) reporting events.

C) adjusting events.

D) disclosing events.

A) non-adjusting events.

B) reporting events.

C) adjusting events.

D) disclosing events.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following does not involve the use of estimates by an entity in preparing its financial statements?

A) Doubtful debts expense

B) Depreciation expense

C) The original purchase price of an asset

D) Employee benefit liabilities such as long-service leave

A) Doubtful debts expense

B) Depreciation expense

C) The original purchase price of an asset

D) Employee benefit liabilities such as long-service leave

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following statements is correct?

A) Extensive guidance is given in accounting standards on the concept of materiality.

B) The disclosure provisions of accounting standards must always be applied even if the resulting information is immaterial.

C) Materiality only ever depends on the size of an item.

D) The disclosure provisions of accounting standards do not need to be applied if the resulting information is immaterial.

A) Extensive guidance is given in accounting standards on the concept of materiality.

B) The disclosure provisions of accounting standards must always be applied even if the resulting information is immaterial.

C) Materiality only ever depends on the size of an item.

D) The disclosure provisions of accounting standards do not need to be applied if the resulting information is immaterial.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

9

A company's workforce went on strike for an indefinite period commencing on 5 August 2014. The strike was expected to cause severe financial conditions for the company. The financial statements for the year ended 30 June 2014 were expected to be finalised by 7 August 2014. In accordance with AASB 110 Events after the Reporting Period, the appropriate treatment regarding this event is:

A) disclosure as a note to the financial statements, as it is a non-adjusting event.

B) disclosure as a note to the financial statements, as it is an adjusting event.

C) to adjust the financial statements, as it is a non-adjusting event.

D) to adjust the financial statements, as it is an adjusting event.

A) disclosure as a note to the financial statements, as it is a non-adjusting event.

B) disclosure as a note to the financial statements, as it is an adjusting event.

C) to adjust the financial statements, as it is a non-adjusting event.

D) to adjust the financial statements, as it is an adjusting event.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

10

The financial statements of an entity are authorised for issue on:

A) the day the directors' declaration is signed.

B) 30 June each year.

C) the last day of the financial year.

D) the day the auditor's report is signed.

A) the day the directors' declaration is signed.

B) 30 June each year.

C) the last day of the financial year.

D) the day the auditor's report is signed.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

11

Errors can occur for which of the following reasons?

A) Mistakes in applying accounting policies

B) Misinterpretation of facts

C) Fraud

D) All of the options are correct

A) Mistakes in applying accounting policies

B) Misinterpretation of facts

C) Fraud

D) All of the options are correct

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

12

In determining whether an item is material, consideration must be given to:

A) its size only.

B) both its size and nature.

C) its nature only.

D) none of the options are correct.

A) its size only.

B) both its size and nature.

C) its nature only.

D) none of the options are correct.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

13

Prior to the finalisation of the financial statements for the year ended 30 June 2014, a company experienced a number of material events, including:

In respect of the events listed above, it will be necessary to adjust the financial statements, by way of general journal entries, for:

A) I, II and III.

B) II only, and make a note disclosure for I and III.

C) III only, and make a note disclosure for I and II.

D) II and III only, and make a note disclosure for I.

In respect of the events listed above, it will be necessary to adjust the financial statements, by way of general journal entries, for:

A) I, II and III.

B) II only, and make a note disclosure for I and III.

C) III only, and make a note disclosure for I and II.

D) II and III only, and make a note disclosure for I.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

14

Canetoads Ltd has discovered that the estimated useful life made on a material depreciable asset was incorrect due to a change in the way the asset was being used. The correct accounting treatment of this event is to:

A) disclose the change in the notes to the financial statements.

B) treat it as an error and adjust retrospectively.

C) treat it as a change in an accounting estimate and adjust prospectively.

D) treat it as a change in an accounting estimate and adjust retrospectively.

A) disclose the change in the notes to the financial statements.

B) treat it as an error and adjust retrospectively.

C) treat it as a change in an accounting estimate and adjust prospectively.

D) treat it as a change in an accounting estimate and adjust retrospectively.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 14 flashcards in this deck.