Deck 17: Statement of Cash Flows

Full screen (f)

Question

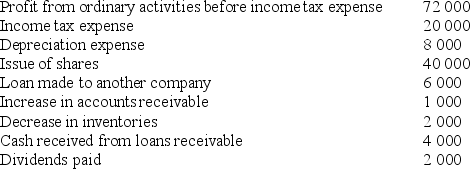

A company reported the following information for a financial year:

What is the net cash inflow (outflow) from financing activities?

A) $38 000 net cash inflow.

B) $40,000 net cash inflow.

C) $42,000 net cash inflow.

D) $(2000) net cash outflow.

What is the net cash inflow (outflow) from financing activities?

A) $38 000 net cash inflow.

B) $40,000 net cash inflow.

C) $42,000 net cash inflow.

D) $(2000) net cash outflow.

Question

Question

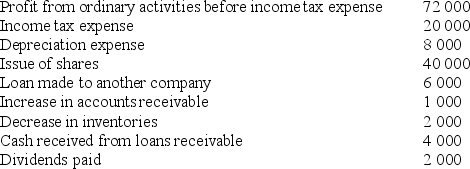

A company reported the following information for a financial year:

What is the net cash inflow from operating activities?

A) $45 000.

B) $59 000.

C) $60 000.

D) $61 000.

What is the net cash inflow from operating activities?

A) $45 000.

B) $59 000.

C) $60 000.

D) $61 000.

Question

Question

During the financial year, Cresswell Limited had a cost of sales amounting to $260 000. Opening and ending balances of related accounts were:

A discount of $2000 for prompt payment was received. The amount of cash paid for goods purchased during the year was:

A) $259 000.

B) $263 000.

C) $275 000.

D) $279 000.

A discount of $2000 for prompt payment was received. The amount of cash paid for goods purchased during the year was:

A) $259 000.

B) $263 000.

C) $275 000.

D) $279 000.

Question

Question

Question

Question

Question

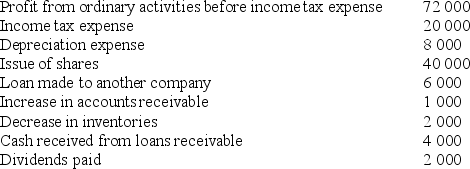

A company reported the following information for a financial year:

What is the net cash inflow (outflow) from investing activities?

A) $2000 net cash inflow.

B) $6000 net cash inflow.

C) $(2000) net cash outflow.

D) $(4000) net cash outflow.

What is the net cash inflow (outflow) from investing activities?

A) $2000 net cash inflow.

B) $6000 net cash inflow.

C) $(2000) net cash outflow.

D) $(4000) net cash outflow.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/29

Play

Full screen (f)

Deck 17: Statement of Cash Flows

1

A company reported the following information for a financial year:

What is the net cash inflow (outflow) from financing activities?

A) $38 000 net cash inflow.

B) $40,000 net cash inflow.

C) $42,000 net cash inflow.

D) $(2000) net cash outflow.

What is the net cash inflow (outflow) from financing activities?

A) $38 000 net cash inflow.

B) $40,000 net cash inflow.

C) $42,000 net cash inflow.

D) $(2000) net cash outflow.

A

2

Brett Limited had a profit after tax of $850 000 for the financial year. Included in this profit was:

Depreciation expense of $120 000

Gain on sale of investments of $28 000

Also, accounts receivable increased by $39 000 and inventories decreased by $12 000. The cash flow from operating activities during the year was:

A) $731 000.

B) $785 000.

C) $915 000.

D) $969 000.

Depreciation expense of $120 000

Gain on sale of investments of $28 000

Also, accounts receivable increased by $39 000 and inventories decreased by $12 000. The cash flow from operating activities during the year was:

A) $731 000.

B) $785 000.

C) $915 000.

D) $969 000.

C

3

A company reported the following information for a financial year:

What is the net cash inflow from operating activities?

A) $45 000.

B) $59 000.

C) $60 000.

D) $61 000.

What is the net cash inflow from operating activities?

A) $45 000.

B) $59 000.

C) $60 000.

D) $61 000.

D

4

Katsis Limited had the following cash flows during the reporting period:

Purchase of intangibles $20 000

Proceeds from sale of plant $28 000

Receipts from customers $832 000

Payments to suppliers $593 000

Interest received $17 600

Income taxes paid $45 500

The net cash flows from operating activities was:

A) $211 100.

B) $219 100.

C) $239 100.

D) $256 600.

Purchase of intangibles $20 000

Proceeds from sale of plant $28 000

Receipts from customers $832 000

Payments to suppliers $593 000

Interest received $17 600

Income taxes paid $45 500

The net cash flows from operating activities was:

A) $211 100.

B) $219 100.

C) $239 100.

D) $256 600.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

5

During the financial year, Cresswell Limited had a cost of sales amounting to $260 000. Opening and ending balances of related accounts were:

A discount of $2000 for prompt payment was received. The amount of cash paid for goods purchased during the year was:

A) $259 000.

B) $263 000.

C) $275 000.

D) $279 000.

A discount of $2000 for prompt payment was received. The amount of cash paid for goods purchased during the year was:

A) $259 000.

B) $263 000.

C) $275 000.

D) $279 000.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

6

Operating activities on a statement of cash flows are generally associated with:

A) movements in non-current liabilities of an entity.

B) revenues and expenses of an entity.

C) acquisitions of non-current assets of an entity.

D) changes in equity of an entity.

A) movements in non-current liabilities of an entity.

B) revenues and expenses of an entity.

C) acquisitions of non-current assets of an entity.

D) changes in equity of an entity.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

7

Warner Limited classifies interest paid and interest received a operating activities. Warner Limited had the following cash flows during a reporting period:

Consideration paid to acquire a subsidiary, net of cash acquired $250 000

Dividends paid $65 000

Repayment of borrowings $90 000

Interest paid on borrowings $57 000

Proceeds from sale of plant $215 000

What is the amount of the cash flows in relation to financing activities of Warner Limited for the reporting period?

A) Net cash inflow $155 000.

B) Net cash outflow $155 000.

C) Net cash inflow $212 000.

D) Net cash outflow $212 000.

Consideration paid to acquire a subsidiary, net of cash acquired $250 000

Dividends paid $65 000

Repayment of borrowings $90 000

Interest paid on borrowings $57 000

Proceeds from sale of plant $215 000

What is the amount of the cash flows in relation to financing activities of Warner Limited for the reporting period?

A) Net cash inflow $155 000.

B) Net cash outflow $155 000.

C) Net cash inflow $212 000.

D) Net cash outflow $212 000.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following items must be separately disclosed in the statement of cash flows?

I - Dividends paid

II - Interest received

III - Dividends received

IV - Interest paid

V - Auditor's remuneration paid

A) I, II, III and IV only.

B) II, III and IV only.

C) I, II and V only.

D) II, III, IV and V only.

I - Dividends paid

II - Interest received

III - Dividends received

IV - Interest paid

V - Auditor's remuneration paid

A) I, II, III and IV only.

B) II, III and IV only.

C) I, II and V only.

D) II, III, IV and V only.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following items would be presented in a statement of cash flows?

A) Payment of dividends through a share investment scheme.

B) Acquisition of an investment in a subsidiary for consideration consisting of an exchange of non-current assets and liabilities.

C) Proceeds from the issue of debentures.

D) Depositing cash on hand in the bank account.

A) Payment of dividends through a share investment scheme.

B) Acquisition of an investment in a subsidiary for consideration consisting of an exchange of non-current assets and liabilities.

C) Proceeds from the issue of debentures.

D) Depositing cash on hand in the bank account.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

10

A company reported the following information for a financial year:

What is the net cash inflow (outflow) from investing activities?

A) $2000 net cash inflow.

B) $6000 net cash inflow.

C) $(2000) net cash outflow.

D) $(4000) net cash outflow.

What is the net cash inflow (outflow) from investing activities?

A) $2000 net cash inflow.

B) $6000 net cash inflow.

C) $(2000) net cash outflow.

D) $(4000) net cash outflow.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

11

During the financial year Marina Limited had sales of $720 000. The opening balance of accounts receivable was $103 000, and the closing balance was $139 000. Bad debts amounting to $34 000 were written off during the period. The cash receipts from customers during the year amounted to:

A) $650 000.

B) $718 000.

C) $722 000.

D) $790 000.

A) $650 000.

B) $718 000.

C) $722 000.

D) $790 000.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

12

During the financial year Sugianto Limited had sales of $42 000. The opening balance of accounts receivable was $9000, and the closing balance was $12 700. Bad debts amounting to $700 were written off during the period. The cash receipts from sales during the year amounted to:

A) $37 600.

B) $39 000.

C) $38 300.

D) $45 700.

A) $37 600.

B) $39 000.

C) $38 300.

D) $45 700.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

13

Items classified as financing activities on an entity's statement of cash flows are usually associated with:

A) movements in non-current liabilities and equity.

B) sales of goods and services by the entity.

C) disposal of non-current assets.

D) purchase on shares by the entity.

A) movements in non-current liabilities and equity.

B) sales of goods and services by the entity.

C) disposal of non-current assets.

D) purchase on shares by the entity.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

14

In accordance with AASB 107/IAS 7 Statement of Cash Flows investing and financing transactions that do NOT require the use of cash or cash equivalents should be:

A) excluded from a statement of cash flows.

B) presented in a statement of cash flows before operating, investing and financing activities.

C) presented in the statement of cash flows after operating activities and before investing and financing activities.

D) presented in a statement of cash flows after the operating, investing and financing activities.

A) excluded from a statement of cash flows.

B) presented in a statement of cash flows before operating, investing and financing activities.

C) presented in the statement of cash flows after operating activities and before investing and financing activities.

D) presented in a statement of cash flows after the operating, investing and financing activities.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

15

The following cash flow activities are regarded as investing cash flows:

A) income taxes paid.

B) interest paid.

C) acquisition of subsidiary net of cash acquired.

D) proceeds from issue of debentures.

A) income taxes paid.

B) interest paid.

C) acquisition of subsidiary net of cash acquired.

D) proceeds from issue of debentures.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

16

According to AASB 107/IAS 7 Statement of Cash Flows, which of the following items does NOT fall within the definition of cash?

A) Bank notes and coins.

B) Non-bank bills that are readily convertible to cash.

C) Deposits on the short-term money market with a term of less than 3 months.

D) Accounts receivable.

A) Bank notes and coins.

B) Non-bank bills that are readily convertible to cash.

C) Deposits on the short-term money market with a term of less than 3 months.

D) Accounts receivable.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

17

The following information was extracted from the records of Ustinof Limited:

Opening balance of equipment, $360 000

Closing balance of equipment, $400 000

Cost of new equipment, $80 000

Proceeds from sale of equipment, $6000 (Cost $40 000; Carrying amount $10 000)

The total cash flows from investing activities is determined as:

A) $40 000 cash outflow.

B) $74 000 cash outflow.

C) $76 000 cash outflow.

D) $80 000 cash outflow.

Opening balance of equipment, $360 000

Closing balance of equipment, $400 000

Cost of new equipment, $80 000

Proceeds from sale of equipment, $6000 (Cost $40 000; Carrying amount $10 000)

The total cash flows from investing activities is determined as:

A) $40 000 cash outflow.

B) $74 000 cash outflow.

C) $76 000 cash outflow.

D) $80 000 cash outflow.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

18

The following item is classified as part of 'investing activities' in the statement of cash flows:

A) depreciation of non-current assets.

B) gain on sale of investments.

C) acquisition of non-current assets.

D) proceeds from an issue of shares.

A) depreciation of non-current assets.

B) gain on sale of investments.

C) acquisition of non-current assets.

D) proceeds from an issue of shares.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following items is classified as part of 'operating activities' in the statement of cash flows?

A) Depreciation of non-current assets.

B) Receipts from customers from the sale of goods.

C) Bad debts expense.

D) Proceeds from the sale of non-current assets.

A) Depreciation of non-current assets.

B) Receipts from customers from the sale of goods.

C) Bad debts expense.

D) Proceeds from the sale of non-current assets.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

20

The following item is classified as a 'financing activity' in the statement of cash flows:

A) payment of dividends through a dividend reinvestment scheme.

B) cash received from accounts receivable.

C) cash payment on redemption of the company's debentures.

D) cash payment to purchase debentures of another entity.

A) payment of dividends through a dividend reinvestment scheme.

B) cash received from accounts receivable.

C) cash payment on redemption of the company's debentures.

D) cash payment to purchase debentures of another entity.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

21

Cash flows arising from each of the following activities of a financial institution may be reported on a net basis:

I - Cash payments and receipts for the acceptance and repayment of deposits with a fixed maturity date.

II - The placement of deposits with and withdrawal of deposits from other financial institutions.

III - Cash advances and loans made to customers and the repayment of those advances and loans.

IV - Cash receipts and payments for the acceptance and repayment of deposits with no fixed maturity date.

A) I, II and IV.

B) II, III and IV.

C) I, III and IV.

D) I, II and III.

I - Cash payments and receipts for the acceptance and repayment of deposits with a fixed maturity date.

II - The placement of deposits with and withdrawal of deposits from other financial institutions.

III - Cash advances and loans made to customers and the repayment of those advances and loans.

IV - Cash receipts and payments for the acceptance and repayment of deposits with no fixed maturity date.

A) I, II and IV.

B) II, III and IV.

C) I, III and IV.

D) I, II and III.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

22

AASB 107/IAS 7 encourages, but does NOT require, the disclosure of:

I - The amount of undrawn borrowing facilities that may be available for future operating activities and to settle capital commitments, indicating any restrictions on the use of these facilities.

II - The aggregate amount of cash flows that represent increases in operating capacity separately from those cash flows that are required to maintain operating capacity.

III - The amount of the cash flows arising from the operating, investing and financing activities of each reportable segment.

IV - The name(s) of the entity's bankers.

A) I, II and IV.

B) II, III and IV.

C) I, III and IV.

D) I, II and III.

I - The amount of undrawn borrowing facilities that may be available for future operating activities and to settle capital commitments, indicating any restrictions on the use of these facilities.

II - The aggregate amount of cash flows that represent increases in operating capacity separately from those cash flows that are required to maintain operating capacity.

III - The amount of the cash flows arising from the operating, investing and financing activities of each reportable segment.

IV - The name(s) of the entity's bankers.

A) I, II and IV.

B) II, III and IV.

C) I, III and IV.

D) I, II and III.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

23

The components of cash and cash equivalents:

A) may be disclosed at the option of the entity and reconciled to amounts reported in the statement of financial position.

B) must be disclosed and reconciled to amounts reported in the statement of profit or loss and other comprehensive income.

C) must be disclosed and reconciled to amounts reported in the statement of financial position.

D) must be disclosed and reconciled to amounts reported in the statement of changes in equity.

A) may be disclosed at the option of the entity and reconciled to amounts reported in the statement of financial position.

B) must be disclosed and reconciled to amounts reported in the statement of profit or loss and other comprehensive income.

C) must be disclosed and reconciled to amounts reported in the statement of financial position.

D) must be disclosed and reconciled to amounts reported in the statement of changes in equity.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

24

For cash flow reporting purposes, operating activities include:

A) buying and selling of non-current assets.

B) incurring and extinguishing equity and debt.

C) acquisition and disposal of investments.

D) activities not otherwise classified as financing and investing.

A) buying and selling of non-current assets.

B) incurring and extinguishing equity and debt.

C) acquisition and disposal of investments.

D) activities not otherwise classified as financing and investing.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

25

An item or transaction will qualify for classification as a cash equivalent:

A) only if it has a remaining term of more than three months but no more than six months.

B) only if its term to maturity is no greater than twelve months.

C) only if it has a fixed maturity date of greater than twelve months.

D) only if it has a maturity of less than three months.

A) only if it has a remaining term of more than three months but no more than six months.

B) only if its term to maturity is no greater than twelve months.

C) only if it has a fixed maturity date of greater than twelve months.

D) only if it has a maturity of less than three months.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

26

The basis of measurement used in the statement of cash flows is:

A) accrual.

B) cash and cash equivalents.

C) net present value.

D) market value.

A) accrual.

B) cash and cash equivalents.

C) net present value.

D) market value.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

27

Cash flows arising from investing or financing activities may be reported on a net basis when:

A) cash receipts and payments for items in which the turnover is slow, the amounts are large, and the maturities are short.

B) cash receipts and payments for items in which the turnover is quick, the amounts small, and the maturities are short.

C) cash receipts and payments for items in which the turnover is quick, the amounts are large, and the maturities are short.

D) cash receipts and payments for items in which the turnover is quick, the amounts are large, and the maturities are long-term.

A) cash receipts and payments for items in which the turnover is slow, the amounts are large, and the maturities are short.

B) cash receipts and payments for items in which the turnover is quick, the amounts small, and the maturities are short.

C) cash receipts and payments for items in which the turnover is quick, the amounts are large, and the maturities are short.

D) cash receipts and payments for items in which the turnover is quick, the amounts are large, and the maturities are long-term.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

28

The method of presentation method of operating cash flows that separates gross cash inflows from cash outflows is known as the:

A) equity method.

B) direct method.

C) set-off method.

D) net method.

A) equity method.

B) direct method.

C) set-off method.

D) net method.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

29

Bank borrowings are ordinarily classified as:

A) operating activities, except for bank overdrafts that are repayable on demand and which form an integral part of an entity's cash management.

B) investing activities, except for bank overdrafts that are repayable on demand and which form an integral part of an entity's cash management.

C) financing activities, except for bank overdrafts that are repayable on demand.

D) financing activities, except for bank overdrafts that are repayable on demand and which form an integral part of an entity's cash management.

A) operating activities, except for bank overdrafts that are repayable on demand and which form an integral part of an entity's cash management.

B) investing activities, except for bank overdrafts that are repayable on demand and which form an integral part of an entity's cash management.

C) financing activities, except for bank overdrafts that are repayable on demand.

D) financing activities, except for bank overdrafts that are repayable on demand and which form an integral part of an entity's cash management.

Unlock Deck

Unlock for access to all 29 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 29 flashcards in this deck.