Deck 15: Revenue

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

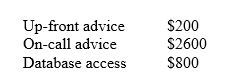

TelCo provides a bundled service offering to a customer for $3000 upfront. The services provided are as follows:

Upfront advice

'on-call' advice

Database access for a 2-year period

If TelCo were to charge a separate fee for each service if sold separately the fee would be:

Using the relative fair value approach the amount of revenue recognised in relation to the on-call advice is:

A) indeterminable based on the facts provided.

B) $1000.

C) $2167.

D) $2600.

Upfront advice

'on-call' advice

Database access for a 2-year period

If TelCo were to charge a separate fee for each service if sold separately the fee would be:

Using the relative fair value approach the amount of revenue recognised in relation to the on-call advice is:

A) indeterminable based on the facts provided.

B) $1000.

C) $2167.

D) $2600.

Question

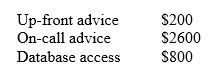

TelCo provides a bundled service offering to a customer for $3000 upfront. The services provided are as follows:

Upfront advice

'on-call' advice

Database access for a 2-year period

If TelCo were to charge a separate fee for each service if sold separately the fee would be:

The revenue that would be recorded by TelCo at the inception of the agreement is:

*a) $166

B) $833

C) $1500

D) $3000

Upfront advice

'on-call' advice

Database access for a 2-year period

If TelCo were to charge a separate fee for each service if sold separately the fee would be:

The revenue that would be recorded by TelCo at the inception of the agreement is:

*a) $166

B) $833

C) $1500

D) $3000

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/23

Play

Full screen (f)

Deck 15: Revenue

1

Under AASB 118 interest revenue is recognised as follows:

A) on a straight line method.

B) on an effective interest method.

C) on either an effective interest method, or a straight line method, depending on which method the entity feels provides the most relevant and reliable information.

D) at the time of receipt of the interest.

A) on a straight line method.

B) on an effective interest method.

C) on either an effective interest method, or a straight line method, depending on which method the entity feels provides the most relevant and reliable information.

D) at the time of receipt of the interest.

B

2

House Proud Pty Ltd is operating a promotion selling furniture under the following conditions:

Initial deposit of 20% of purchase price.

Immediate delivery of furniture.

Interest rate of 12.5%pa charged on the outstanding balance.

Repayment of the balance (including the interest) over 24 equal monthly instalments.

House Proud retains legal title to the furniture until the final monthly payment has been made.

House Proud would recognise revenue as follows:

A) Recognise interest as it is received (monthly) and recognise the revenue on the sale of the goods once the final payment has been received.

B) Recognise all revenue as it is received

C) Recognise interest as it is received (monthly) and recognise the revenue on the sale of the goods upfront.

D) Recognise the whole amount of revenue upfront

Initial deposit of 20% of purchase price.

Immediate delivery of furniture.

Interest rate of 12.5%pa charged on the outstanding balance.

Repayment of the balance (including the interest) over 24 equal monthly instalments.

House Proud retains legal title to the furniture until the final monthly payment has been made.

House Proud would recognise revenue as follows:

A) Recognise interest as it is received (monthly) and recognise the revenue on the sale of the goods once the final payment has been received.

B) Recognise all revenue as it is received

C) Recognise interest as it is received (monthly) and recognise the revenue on the sale of the goods upfront.

D) Recognise the whole amount of revenue upfront

A

3

When consideration is deferred and there is a below-market rate of interest charged the fair value of the consideration should be determined:

A) as the nominal amount of the cash receivable.

B) by discounting all future receipts using an imputed rate of interest.

C) by discounting all future receipts using the interest rate in the contract.

D) as the recommended retail price of the item sold.

A) as the nominal amount of the cash receivable.

B) by discounting all future receipts using an imputed rate of interest.

C) by discounting all future receipts using the interest rate in the contract.

D) as the recommended retail price of the item sold.

B

4

Easter Pty Ltd operates a facility making chocolate Easter eggs. Easter has a policy that all unsold chocolate eggs can be returned for a full refund within 1 week of Easter Sunday. On 1 March 2014, Easter sold 500 pallets of packaged eggs at $100 per pallet. Historical data indicates that 20% of the stock will be returned for a refund. Within one month of Easter Sunday (by the end of April 2014) 10% of the eggs were retuned for refund. Using the expected sales approach, how much revenue would be recognised by Easter at the end of April 2014?

A) Nil.

B) $40 000.

C) $45 000.

D) $50 000.

A) Nil.

B) $40 000.

C) $45 000.

D) $50 000.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following is NOT a condition that needs to be satisfied prior to recognising revenue from the rendering of services using the 'percentage of completion' method?

A) The amount of revenue can be measured reliably.

B) The stage of completion of the transaction can be measured reliably.

C) The costs of the transaction (including future costs) can be measured reliably.

D) The contract is non-cancellable.

A) The amount of revenue can be measured reliably.

B) The stage of completion of the transaction can be measured reliably.

C) The costs of the transaction (including future costs) can be measured reliably.

D) The contract is non-cancellable.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

6

The IFRS 15 Revenue from Contracts with Customers is inconsistent with the principles within which of the following?

A) The Conceptual Framework for Financial Reporting.

B) AASB 118 Revenue.

C) IFRIC 13 Customer Loyalty Programmes.

D) All of the options are correct.

A) The Conceptual Framework for Financial Reporting.

B) AASB 118 Revenue.

C) IFRIC 13 Customer Loyalty Programmes.

D) All of the options are correct.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following disclosures are required under AASB 118?

I - Total income, allocated between revenue and other gains.

II - The accounting policies adopted for revenue recognition.

III - The amount of each significant category of revenue recognised during the period.

IV - The amount of revenue arising from exchanges of goods and services.

A) I and II only.

B) II, III and IV only.

C) I, II and III only.

D) I, II, III and IV.

I - Total income, allocated between revenue and other gains.

II - The accounting policies adopted for revenue recognition.

III - The amount of each significant category of revenue recognised during the period.

IV - The amount of revenue arising from exchanges of goods and services.

A) I and II only.

B) II, III and IV only.

C) I, II and III only.

D) I, II, III and IV.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following are excluded from the scope of AASB 118?

I The initial recognition of agricultural produce.

II Insurance contracts within the scope of AASB 4.

III The extraction of mineral ores.

IV Lease agreements.

A) I, II only.

B) II, III and IV only.

C) I, III and IV only.

D) I, II, III and IV.

I The initial recognition of agricultural produce.

II Insurance contracts within the scope of AASB 4.

III The extraction of mineral ores.

IV Lease agreements.

A) I, II only.

B) II, III and IV only.

C) I, III and IV only.

D) I, II, III and IV.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

9

Big Bank Limited provides Good Sport Pty Ltd with a five-year loan to finance the construction of a new sporting stadium. Good Sport had the choice of paying a market rate of interest (7.5% at the inception of the loan) or paying interest at a rate of 1.5% below the market rate, and paying in addition a fixed 'arrangement fee' of $200 000 to compensate Big Bank for charging an interest rate below the fair market value. Good Sport chose the second option.

Big Bank should recognise revenue from the arrangement fee as:

A) fee revenue as services are provided by Big Bank.

B) fee revenue on the completion of the significant act of drawing down the loan.

C) interest revenue on the completion of the significant act of drawing down the loan.

D) interest revenue over the life of the loan in accordance with the effective interest method.

Big Bank should recognise revenue from the arrangement fee as:

A) fee revenue as services are provided by Big Bank.

B) fee revenue on the completion of the significant act of drawing down the loan.

C) interest revenue on the completion of the significant act of drawing down the loan.

D) interest revenue over the life of the loan in accordance with the effective interest method.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following is NOT excluded from the scope of AASB 118 Revenue?

A) Accounting for share of joint venture revenue.

B) Subscriptions.

C) Revenue arising from primary production activities.

D) Revenue arising from oil and gas exploration.

A) Accounting for share of joint venture revenue.

B) Subscriptions.

C) Revenue arising from primary production activities.

D) Revenue arising from oil and gas exploration.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

11

Deefer Limited sold an item of machinery on 1 July 2014 on the following terms:

Initial payment of $25 000

Annual payments of $25 000 for 5 years (total $125 000).

The buyers incremental rate of interest is 7.5% and the present value of the future annual payments is $101 147.

At the time of sale of the machine Deefer would recognise revenue of:

A) $25 000.

B) $125 000.

C) $126 147.

D) $150 000.

Initial payment of $25 000

Annual payments of $25 000 for 5 years (total $125 000).

The buyers incremental rate of interest is 7.5% and the present value of the future annual payments is $101 147.

At the time of sale of the machine Deefer would recognise revenue of:

A) $25 000.

B) $125 000.

C) $126 147.

D) $150 000.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following items are defined in AASB 118?

A) Income.

B) Revenue.

C) Gains.

D) All of the above.

A) Income.

B) Revenue.

C) Gains.

D) All of the above.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

13

The two elements of performance referred to in the conceptual framework are:

A) assets and liabilities.

B) revenue and expenses.

C) liabilities and equity.

D) expenses and income.

A) assets and liabilities.

B) revenue and expenses.

C) liabilities and equity.

D) expenses and income.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

14

Orange Pty Ltd develops and sells off-the-shelf accounting software packages. The retail price of each package is $399 (GST inclusive). Included with each purchase are 'free' upgrades for a period of 12 months after the date of purchase. These upgrades can be purchased separately for $80 (GST inclusive).

At the date of purchase of the software package by a customer, Orange should record revenue of:

A) $290.00.

B) $319.00.

C) $362.72.

D) $399.00.

At the date of purchase of the software package by a customer, Orange should record revenue of:

A) $290.00.

B) $319.00.

C) $362.72.

D) $399.00.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

15

The effect that IFRIC Interpretation titled Agreements for the Construction of Real Estate will have the following effect for entities that undertake off-the-plan real estate sales is that:

A) the percentage of completion method of revenue recognition will be discontinued.

B) the use of the completed contracts method of revenue recognition will be discontinued.

C) the amount of revenue recognised on such sales will reduce.

D) the amount of revenue recognised on such sales will increase.

A) the percentage of completion method of revenue recognition will be discontinued.

B) the use of the completed contracts method of revenue recognition will be discontinued.

C) the amount of revenue recognised on such sales will reduce.

D) the amount of revenue recognised on such sales will increase.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

16

The following information relates to SellIT:

5000 units of stock were sold for $10 per unit

The cost of that stock to SellIT was $4.50 per unit

Other costs incurred during the period totalled $10 000

Proceeds on sale of an item of plant during the period was $2000

The carrying amount of the plant at the date of disposal was $500.

SellIT would recognise the following amount as revenue for the period:

A) $27 500.

B) $50 000.

C) $51 500.

D) $52 000.

5000 units of stock were sold for $10 per unit

The cost of that stock to SellIT was $4.50 per unit

Other costs incurred during the period totalled $10 000

Proceeds on sale of an item of plant during the period was $2000

The carrying amount of the plant at the date of disposal was $500.

SellIT would recognise the following amount as revenue for the period:

A) $27 500.

B) $50 000.

C) $51 500.

D) $52 000.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

17

TelCo provides a bundled service offering to a customer for $3000 upfront. The services provided are as follows:

Upfront advice

'on-call' advice

Database access for a 2-year period

If TelCo were to charge a separate fee for each service if sold separately the fee would be:

Using the relative fair value approach the amount of revenue recognised in relation to the on-call advice is:

A) indeterminable based on the facts provided.

B) $1000.

C) $2167.

D) $2600.

Upfront advice

'on-call' advice

Database access for a 2-year period

If TelCo were to charge a separate fee for each service if sold separately the fee would be:

Using the relative fair value approach the amount of revenue recognised in relation to the on-call advice is:

A) indeterminable based on the facts provided.

B) $1000.

C) $2167.

D) $2600.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

18

TelCo provides a bundled service offering to a customer for $3000 upfront. The services provided are as follows:

Upfront advice

'on-call' advice

Database access for a 2-year period

If TelCo were to charge a separate fee for each service if sold separately the fee would be:

The revenue that would be recorded by TelCo at the inception of the agreement is:

*a) $166

B) $833

C) $1500

D) $3000

Upfront advice

'on-call' advice

Database access for a 2-year period

If TelCo were to charge a separate fee for each service if sold separately the fee would be:

The revenue that would be recorded by TelCo at the inception of the agreement is:

*a) $166

B) $833

C) $1500

D) $3000

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is NOT an example of an agency arrangement where the selling entity would recognise revenue on a net basis?

A) A travel agent selling an airline ticket to a customer, charging the customer $200 and remitting $180 to the airline.

B) A supermarket selling groceries to a customer for $110 and remitting $10 GST to the government.

C) A distributor receiving stock from its supplier on a sale-or-return basis. The sales price per unit is $120 and the cost per unit is $75.

D) A licensed hotel selling keno tickets to customers for $5.00 and remitting $4.50 per ticket to the state gaming authority.

A) A travel agent selling an airline ticket to a customer, charging the customer $200 and remitting $180 to the airline.

B) A supermarket selling groceries to a customer for $110 and remitting $10 GST to the government.

C) A distributor receiving stock from its supplier on a sale-or-return basis. The sales price per unit is $120 and the cost per unit is $75.

D) A licensed hotel selling keno tickets to customers for $5.00 and remitting $4.50 per ticket to the state gaming authority.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following is NOT an example of an entity retaining significant risks and rewards of ownership?

A) The entity retains an obligation for unsatisfactory performance not covered by normal warranty provisions.

B) The receipt of revenue from a particular sale is contingent on the buyer reselling the goods.

C) The goods are shipped subject to installation, and the installation is a significant part of the contract that has not yet been completed by the entity.

D) The buyer has the right to rescind the purchase for a reason specified in the sales contract. The entity is confident that this option will not be exercised.

A) The entity retains an obligation for unsatisfactory performance not covered by normal warranty provisions.

B) The receipt of revenue from a particular sale is contingent on the buyer reselling the goods.

C) The goods are shipped subject to installation, and the installation is a significant part of the contract that has not yet been completed by the entity.

D) The buyer has the right to rescind the purchase for a reason specified in the sales contract. The entity is confident that this option will not be exercised.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

21

The introduction of IFRIC 13 Customer Loyalty Programmes had the following impact on revenue recognition policies for entities in the airline industry:

A) no impact.

B) reduced the amount of revenue able to be recognised.

C) increased the amount of revenue able to be recognised.

D) changed the timing of the recognition of revenue.

A) no impact.

B) reduced the amount of revenue able to be recognised.

C) increased the amount of revenue able to be recognised.

D) changed the timing of the recognition of revenue.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

22

On 1 July 2010 ABC Ltd purchased a 5-year $1000 5% debenture for $957.88. The current market rate of interest is 6%. The maturity date is 30 June 2015. Interest is payable annually on 30 June.

The interest income that ABC would recognise for the year ended 30 June 2011 is:

A) $47.89.

B) $50.00.

C) $57.47.

D) $60.00.

The interest income that ABC would recognise for the year ended 30 June 2011 is:

A) $47.89.

B) $50.00.

C) $57.47.

D) $60.00.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

23

In terms of revenue related disclosures on the face of the statement of profit or loss and other comprehensive income:

A) AASB 101 Presentation of Financial Statements requires revenue by category to be disclosed on the face of the statement of profit or loss and other comprehensive income.

B) AASB 118 Revenue requires revenue by category to be disclosed on the face of the statement of profit or loss and other comprehensive income.

C) AASB 101 Presentation of Financial Statements requires total revenue to be disclosed on the face of the statement of profit or loss and other comprehensive income.

D) AASB 118 Revenue requires total revenue to be disclosed on the face of the statement of profit or loss and other comprehensive income.

A) AASB 101 Presentation of Financial Statements requires revenue by category to be disclosed on the face of the statement of profit or loss and other comprehensive income.

B) AASB 118 Revenue requires revenue by category to be disclosed on the face of the statement of profit or loss and other comprehensive income.

C) AASB 101 Presentation of Financial Statements requires total revenue to be disclosed on the face of the statement of profit or loss and other comprehensive income.

D) AASB 118 Revenue requires total revenue to be disclosed on the face of the statement of profit or loss and other comprehensive income.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 23 flashcards in this deck.