Deck 16: Managing Costs and Quality

Full screen (f)

Question

Question

Question

Question

Question

The following are the expected quality costs for a firm for a selected period.

A) $32 000

B) $29 000

C) $31 000

D) $33 000

A) $32 000

B) $29 000

C) $31 000

D) $33 000

Question

Question

Question

The following are the expected quality costs for a firm for a selected period.

A) $33 000

B) $37 500

C) $42 000

D) $37 000

A) $33 000

B) $37 500

C) $42 000

D) $37 000

Question

Question

Question

Question

Question

Question

Question

The following are the expected quality costs for a firm for a selected period.

A) $10 500

B) $9000

C) $11 000

D) $8500

A) $10 500

B) $9000

C) $11 000

D) $8500

Question

The following are the expected quality costs for a firm for a selected period.

A) $5000

B) $7500

C) $8500

D) $9500

A) $5000

B) $7500

C) $8500

D) $9500

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

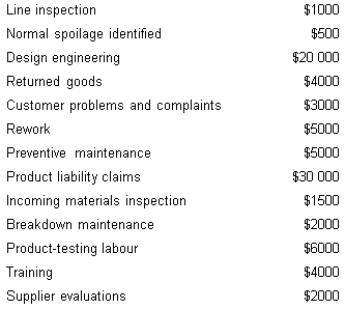

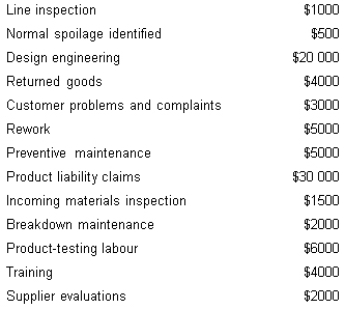

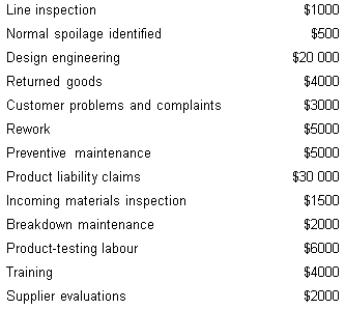

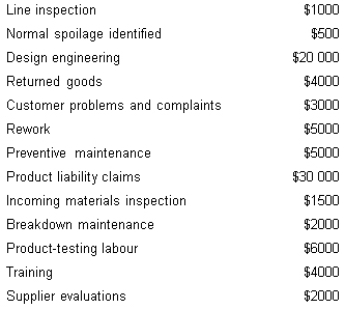

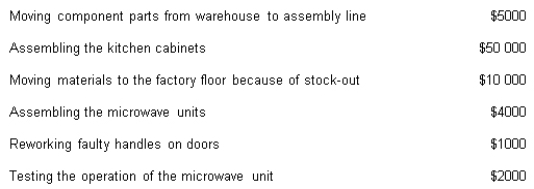

From the following list of costs, determine the amount of non-value-added cost.

A) $17 000

B) $18 000

C) $16 000

D) $8000

A) $17 000

B) $18 000

C) $16 000

D) $8000

Question

Question

Question

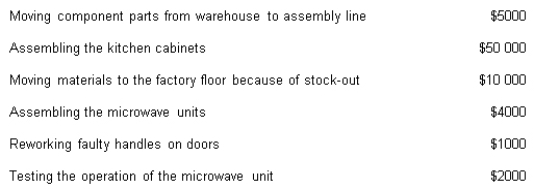

From the following list of costs for a kitchen manufacturer, determine the amount of value-added cost.

A) $57 000

B) $54 000

C) $58 000

D) $59 000

A) $57 000

B) $54 000

C) $58 000

D) $59 000

Question

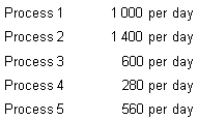

Assume a production process that typically moves the following number of products through its five processes:

Assuming there is room for improvement in all processes, in what order of processes would the firm apply the theory of constraints to remove the bottlenecks?

A) 4 first, and then any order

B) 2, 1, 3, 5, 4

C) Work must be carried out in order of the physical flow of activities, i.e. 1, 2, 3, 4, 5

D) 4, 5, 3, 1, 2

Assuming there is room for improvement in all processes, in what order of processes would the firm apply the theory of constraints to remove the bottlenecks?

A) 4 first, and then any order

B) 2, 1, 3, 5, 4

C) Work must be carried out in order of the physical flow of activities, i.e. 1, 2, 3, 4, 5

D) 4, 5, 3, 1, 2

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

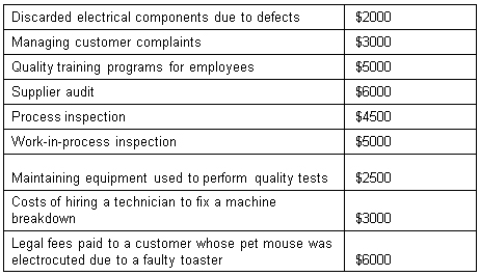

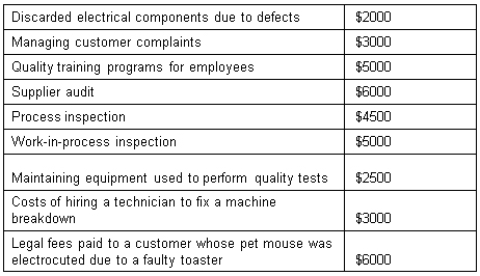

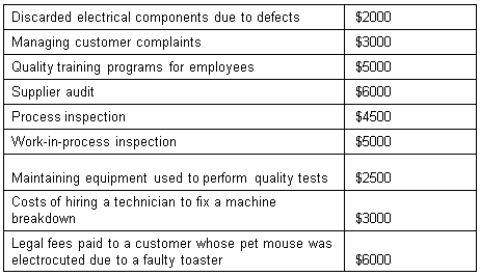

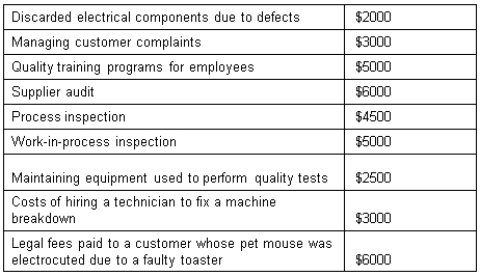

Lazy Linda Kitchen Appliances manufactures small kitchen appliances such as toasters and blenders. Last month Lazy Linda recorded the following quality costs:

Lazy Linda's total appraisal cost was:

A) $5000.

B) $9500.

C) $12 000.

D) $18 000.

Lazy Linda's total appraisal cost was:

A) $5000.

B) $9500.

C) $12 000.

D) $18 000.

Question

Question

Question

Question

Question

Lazy Linda Kitchen Appliances manufactures small kitchen appliances such as toasters and blenders. Last month Lazy Linda recorded the following quality costs:

Lazy Linda's total external failure cost was:

A) $6000.

B) $9000.

C) $12 000.

D) $15 000.

Lazy Linda's total external failure cost was:

A) $6000.

B) $9000.

C) $12 000.

D) $15 000.

Question

Lazy Linda Kitchen Appliances manufactures small kitchen appliances such as toasters and blenders. Last month Lazy Linda recorded the following quality costs:

Lazy Linda's total prevention cost was:

A) $5000.

B) $11 000.

C) $14 000.

D) $15 500.

Lazy Linda's total prevention cost was:

A) $5000.

B) $11 000.

C) $14 000.

D) $15 500.

Question

Lazy Linda Kitchen Appliances manufactures small kitchen appliances such as toasters and blenders. Last month Lazy Linda recorded the following quality costs:

Lazy Linda's total internal failure cost was:

A) $9500.

B) $7500.

C) $5000.

D) $2000.

Lazy Linda's total internal failure cost was:

A) $9500.

B) $7500.

C) $5000.

D) $2000.

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/92

Play

Full screen (f)

Deck 16: Managing Costs and Quality

1

Prevention costs refer to costs incurred:

A) in preventing defects.

B) because defective products or services are delivered to customers.

C) in determining customer demand.

D) when defective products or services are detected before leaving the business.

A) in preventing defects.

B) because defective products or services are delivered to customers.

C) in determining customer demand.

D) when defective products or services are detected before leaving the business.

A

2

Quality of conformance refers to:

A) the degree to which the product meets its design specifications.

B) the extent to which the actual product is designed for its intended use.

C) an ideal that can never be attained.

D) a cost control that is achievable.

A) the degree to which the product meets its design specifications.

B) the extent to which the actual product is designed for its intended use.

C) an ideal that can never be attained.

D) a cost control that is achievable.

A

3

External failure costs refer to costs incurred:

A) in preventing defects.

B) in determining whether defects exist.

C) because defective products or services are delivered to customers.

D) when defective products or services are detected before leaving the business.

A) in preventing defects.

B) in determining whether defects exist.

C) because defective products or services are delivered to customers.

D) when defective products or services are detected before leaving the business.

C

4

In order to have a high-quality finished product:

A) appraisal costs must exceed external failure costs.

B) the product's design specifications must meet customers' expectations.

C) the product must meet the standards of its design.

D) the product's design specifications must meet customers' expectations AND the product must meet the standards of its design.

A) appraisal costs must exceed external failure costs.

B) the product's design specifications must meet customers' expectations.

C) the product must meet the standards of its design.

D) the product's design specifications must meet customers' expectations AND the product must meet the standards of its design.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

5

The following are the expected quality costs for a firm for a selected period.

A) $32 000

B) $29 000

C) $31 000

D) $33 000

A) $32 000

B) $29 000

C) $31 000

D) $33 000

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following statements is/are false?

A) Cost of quality reports analyse quality costs as a percentage of total sales.

B) An increase in quality costs indicates deterioration in quality performance.

C) There can be interactions between the quality costs.

D) The traditional view of quality costs is that total quality costs can be minimised by driving the defect rate down to the acceptable quality level.

A) Cost of quality reports analyse quality costs as a percentage of total sales.

B) An increase in quality costs indicates deterioration in quality performance.

C) There can be interactions between the quality costs.

D) The traditional view of quality costs is that total quality costs can be minimised by driving the defect rate down to the acceptable quality level.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

7

Internal failure costs refer to costs incurred:

A) in determining whether defects exist.

B) because defective products or services are delivered to customers.

C) in determining customer demand.

D) when defective products or services are detected before leaving the business.

A) in determining whether defects exist.

B) because defective products or services are delivered to customers.

C) in determining customer demand.

D) when defective products or services are detected before leaving the business.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

8

The following are the expected quality costs for a firm for a selected period.

A) $33 000

B) $37 500

C) $42 000

D) $37 000

A) $33 000

B) $37 500

C) $42 000

D) $37 000

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following statements is/are correct?

A) Quality of design and quality of conformance are both important concepts in the measurement of excellence.

B) Quality of design is the degree to which a product meets design specifications.

C) Quality of conformance is the degree to which a product conforms to customer expectations.

D) All of the given answers

A) Quality of design and quality of conformance are both important concepts in the measurement of excellence.

B) Quality of design is the degree to which a product meets design specifications.

C) Quality of conformance is the degree to which a product conforms to customer expectations.

D) All of the given answers

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

10

Consider a situation where an activity-based costing system is in use rather than a traditional volume-based costing system. Which of the following statements is/are true?

A) The use of activity-based costing eliminates the need to consider qualitative factors.

B) When an activity-based costing system is used, facility level costs will have to be analysed differently to the way they would be under a traditional volume-based costing system.

C) When an activity-based costing system is used, unit level costs will have to be analysed differently to the way they would be under a traditional volume-based costing system.

D) None of the given answers

A) The use of activity-based costing eliminates the need to consider qualitative factors.

B) When an activity-based costing system is used, facility level costs will have to be analysed differently to the way they would be under a traditional volume-based costing system.

C) When an activity-based costing system is used, unit level costs will have to be analysed differently to the way they would be under a traditional volume-based costing system.

D) None of the given answers

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following statements is/are true in relation to activity-based management (ABM)?

I) ABM is primarily concerned with customer value.

Ii) Activity-based costing is the primary source of data for ABM.

Iii) ABM is primarily concerned with the control of inputs.

A) i and ii

B) i and iii

C) ii and iii

D) All of the given answers

I) ABM is primarily concerned with customer value.

Ii) Activity-based costing is the primary source of data for ABM.

Iii) ABM is primarily concerned with the control of inputs.

A) i and ii

B) i and iii

C) ii and iii

D) All of the given answers

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

12

A series of pictures that shows the flow of activities that make up a process is called:

A) Pareto analysis.

B) a process flow chart.

C) a fishbone diagram.

D) an Ishikawa diagram.

A) Pareto analysis.

B) a process flow chart.

C) a fishbone diagram.

D) an Ishikawa diagram.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

13

Which statement is incorrect?

A) Total quality management (TQM) relates only to the manufacturing processes.

B) TQM is customer-driven.

C) TQM focuses on the flow of activity across the organisation.

D) Continuous improvement is a key element of TQM.

A) Total quality management (TQM) relates only to the manufacturing processes.

B) TQM is customer-driven.

C) TQM focuses on the flow of activity across the organisation.

D) Continuous improvement is a key element of TQM.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

14

Appraisal costs in quality programs are incurred:

A) to value the fixed assets of the firm.

B) to detect which production units do not conform to specifications.

C) to value ending work in process.

D) by external appraisers to value the costs of external failures.

A) to value the fixed assets of the firm.

B) to detect which production units do not conform to specifications.

C) to value ending work in process.

D) by external appraisers to value the costs of external failures.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

15

The following are the expected quality costs for a firm for a selected period.

A) $10 500

B) $9000

C) $11 000

D) $8500

A) $10 500

B) $9000

C) $11 000

D) $8500

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

16

The following are the expected quality costs for a firm for a selected period.

A) $5000

B) $7500

C) $8500

D) $9500

A) $5000

B) $7500

C) $8500

D) $9500

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is not a type of cost of quality?

A) External failure cost

B) Productive inefficiency cost

C) Prevention cost

D) Appraisal cost

A) External failure cost

B) Productive inefficiency cost

C) Prevention cost

D) Appraisal cost

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following are modern approaches to managing costs?

A) Life cycle costing

B) Target costing

C) Both life cycle costing and target costing

D) Neither life cycle costing nor target costing

A) Life cycle costing

B) Target costing

C) Both life cycle costing and target costing

D) Neither life cycle costing nor target costing

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

19

Appraisal costs refer to costs incurred:

A) in preventing defects.

B) in determining whether defects exist.

C) because defective products or services are delivered to customers.

D) in determining customer demand.

A) in preventing defects.

B) in determining whether defects exist.

C) because defective products or services are delivered to customers.

D) in determining customer demand.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following is not a characteristic of total quality management?

A) A focus primarily on internal customers

B) All members of the organisation are responsible for quality measures.

C) Statistical process control

D) Continuous improvement measures

A) A focus primarily on internal customers

B) All members of the organisation are responsible for quality measures.

C) Statistical process control

D) Continuous improvement measures

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

21

Orwell is about to introduce a new product and has established a target cost of $144 and a target margin on sales of 40 per cent. What is the target price?

A) $200

B) $225

C) $240

D) $280

A) $200

B) $225

C) $240

D) $280

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

22

Given the current design and resources, the cost that a new product could be manufactured for, including upstream and downstream costs, is known as:

A) target cost.

B) allowable cost.

C) current cost.

D) strategic cost.

A) target cost.

B) allowable cost.

C) current cost.

D) strategic cost.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

23

The following steps are required to implement business process re-engineering.

I) Establish goals

Ii) Reorganise work flow

Iii) Prepare a business process map

Iv) Implementation

What is the correct order for these steps?

A) i, ii, iii and iv

B) i, iii, ii and iv

C) iii, i, ii and iv

D) ii, iii, i and iv

I) Establish goals

Ii) Reorganise work flow

Iii) Prepare a business process map

Iv) Implementation

What is the correct order for these steps?

A) i, ii, iii and iv

B) i, iii, ii and iv

C) iii, i, ii and iv

D) ii, iii, i and iv

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

24

The following four tasks take place in the concept known as target costing.

I) Value engineering

Ii) Establish a target price

Iii) Establish a target cost

Iv) Establish a target profit

Which of the following correctly depicts the sequence of these tasks?

A) iii, i, iv and ii

B) ii, iv, iii and i

C) ii, iii, i and iv

D) iii, ii, i and iv

I) Value engineering

Ii) Establish a target price

Iii) Establish a target cost

Iv) Establish a target profit

Which of the following correctly depicts the sequence of these tasks?

A) iii, i, iv and ii

B) ii, iv, iii and i

C) ii, iii, i and iv

D) iii, ii, i and iv

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

25

If the target selling price is $120 and the target profit margin is a 40 per cent mark-up on cost, what is the target cost?

A) $48

B) $72

C) $85.70

D) $34.30

A) $48

B) $72

C) $85.70

D) $34.30

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following do traditional costing systems ignore?

I) Production costs

Ii) Design costs

Iii) Development costs

Iv) Marketing and customer service costs

A) i, ii and iii

B) i, ii and iv

C) ii, iii and iv

D) i, iii and iv

I) Production costs

Ii) Design costs

Iii) Development costs

Iv) Marketing and customer service costs

A) i, ii and iii

B) i, ii and iv

C) ii, iii and iv

D) i, iii and iv

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

27

A systematic approach in analysing the product and process design, with the aim of eliminating any non-value-added elements, to achieve the target cost is known as:

A) component level target costs.

B) value engineering.

C) strategic cost reduction.

D) cost reduction objective.

A) component level target costs.

B) value engineering.

C) strategic cost reduction.

D) cost reduction objective.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following statements is/are false?

I) Determining the cause of non-value-added activities requires cost driver analysis.

Ii) Building activities into processes will quickly identify the causes of non-value-added activities.

Iii) Identifying root cause cost drivers is sufficient to enable non-value-added activities to be eliminated.

A) i and ii

B) ii and iii

C) i and iii

D) All of the given answers

I) Determining the cause of non-value-added activities requires cost driver analysis.

Ii) Building activities into processes will quickly identify the causes of non-value-added activities.

Iii) Identifying root cause cost drivers is sufficient to enable non-value-added activities to be eliminated.

A) i and ii

B) ii and iii

C) i and iii

D) All of the given answers

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following is a possible cause of a firm's reluctance to implement activity-based management (ABM)?

I Employee resistance to change.

Ii) Lack of understanding of the benefits of ABM.

Iii) Significant resources required.

Iv) Focus is on value-added activities.

A) i, ii and iii

B) i, ii and iv

C) ii, iii and iv

D) i, iii and iv

I Employee resistance to change.

Ii) Lack of understanding of the benefits of ABM.

Iii) Significant resources required.

Iv) Focus is on value-added activities.

A) i, ii and iii

B) i, ii and iv

C) ii, iii and iv

D) i, iii and iv

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following are key features of target costing?

I) Cross functionality

Ii) Market price driven

Iii) Focus on customer value

Iv) Based on life cycle management

A) i, ii and iii

B) i, iii and iv

C) i, ii and iv

D) All of the given answers

I) Cross functionality

Ii) Market price driven

Iii) Focus on customer value

Iv) Based on life cycle management

A) i, ii and iii

B) i, iii and iv

C) i, ii and iv

D) All of the given answers

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following statements about re-engineering is/are true?

I) Re-engineering is the complete redesign of a process in an attempt to find new creative ways to accomplish objectivity.

Ii) Re-engineering involves more of a 'giant leap' than the concept of activity-based management.

Iii) Re-engineering may entail high risks.

A) i and ii

B) i and iii

C) ii and iii

D) All of the given answers

I) Re-engineering is the complete redesign of a process in an attempt to find new creative ways to accomplish objectivity.

Ii) Re-engineering involves more of a 'giant leap' than the concept of activity-based management.

Iii) Re-engineering may entail high risks.

A) i and ii

B) i and iii

C) ii and iii

D) All of the given answers

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

32

Cartel Ltd has introduced a new product with a target price of $240 and a profit requirement of 33.3 per cent on sales. What is the target cost?

A) $120

B) $160

C) $180

D) $200

A) $120

B) $160

C) $180

D) $200

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

33

Beaufort Ltd is introducing a new range of products. It has established that the target selling prices of the three products are $120, $150 and $210. Beaufort requires a profit mark-up on cost of 33.3 per cent for all its products. What percentage of the target prices is the target cost in each case?

A) 50%

B) 60%

C) 66.7%

D) 75%

A) 50%

B) 60%

C) 66.7%

D) 75%

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

34

When we consider the life cycle sequence of a product, the majority of costs for a typical product have been committed by the end of:

A) product planning.

B) design and development.

C) customer support.

D) production.

A) product planning.

B) design and development.

C) customer support.

D) production.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following are considerations in determining a target selling price?

I) Customer expectations

Ii) Competitors' actions

Iii) Product cost

Iv) Strategic objectives

A) i, ii and iii

B) ii, iii and iv

C) i, iii and iv

D) i, ii and iv

I) Customer expectations

Ii) Competitors' actions

Iii) Product cost

Iv) Strategic objectives

A) i, ii and iii

B) ii, iii and iv

C) i, iii and iv

D) i, ii and iv

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

36

In the process of target costing, where is the concentration of effort required to have the greatest impact on cost savings?

I) Product design

Ii) Process design

Iii) Production costs

Iv) After sales costs

A) i and ii

B) ii and iii

C) i and iii

D) ii and iv

I) Product design

Ii) Process design

Iii) Production costs

Iv) After sales costs

A) i and ii

B) ii and iii

C) i and iii

D) ii and iv

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

37

Carwell has introduced a new product with a target price of $150 and a target cost of $90. What is the target percentage margin on sales?

A) 20%

B) 33.3%

C) 40%

D) 50%

A) 20%

B) 33.3%

C) 40%

D) 50%

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following activities are value-added activities?

I) Preventive maintenance

Ii) Repairs to machinery

Iii) Move work-in-process inventory between machines

Iv) Process receivables

A) i and ii

B) iii and iv

C) i and iv

D) ii and iv

I) Preventive maintenance

Ii) Repairs to machinery

Iii) Move work-in-process inventory between machines

Iv) Process receivables

A) i and ii

B) iii and iv

C) i and iv

D) ii and iv

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following are possible root-cause cost drivers?

I) Complexity

Ii) Defects produced

Iii) Plant layout

Iv) Inadequate employee training

A) i, ii and iii

B) ii, iii and iv

C) i, iii and iv

D) All of the given answers

I) Complexity

Ii) Defects produced

Iii) Plant layout

Iv) Inadequate employee training

A) i, ii and iii

B) ii, iii and iv

C) i, iii and iv

D) All of the given answers

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following activities are non-value-added activities?

I) Inspect work in process

Ii) Process sales orders

Iii) Repair drilling machine

Iv) Move raw material to the work station

A) i, iii and iv

B) i, ii and iv

C) i, ii and iii

D) ii, iii and iv

I) Inspect work in process

Ii) Process sales orders

Iii) Repair drilling machine

Iv) Move raw material to the work station

A) i, iii and iv

B) i, ii and iv

C) i, ii and iii

D) ii, iii and iv

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

41

The theory of constraints focuses on:

A) idle time.

B) poor quality.

C) cost reduction.

D) bottlenecks.

A) idle time.

B) poor quality.

C) cost reduction.

D) bottlenecks.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

42

The modern management tool that focuses on restrictions that limit a firm's ability to maximise long-run profit is commonly known as:

A) linear progression.

B) constraint manipulation.

C) theory of constraints.

D) game theory.

A) linear progression.

B) constraint manipulation.

C) theory of constraints.

D) game theory.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

43

Assuming one answer only can be chosen, which of the following is a non-value-added activity for a manufacturing firm?

A) Machining a metal plate in the factory.

B) Packing finished product into cartons for delivery.

C) Moving partly finished production to storage.

D) Inserting a warranty-card and instruction booklet into the boxed product.

A) Machining a metal plate in the factory.

B) Packing finished product into cartons for delivery.

C) Moving partly finished production to storage.

D) Inserting a warranty-card and instruction booklet into the boxed product.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

44

There are certain features of traditional management accounting. Which of the following is/are not a focus of life cycle costing?

A) Annual profit calculations

B) Focus on production costs only

C) Calculation of cost variances

D) Annual profit calculations AND focus on production costs only

A) Annual profit calculations

B) Focus on production costs only

C) Calculation of cost variances

D) Annual profit calculations AND focus on production costs only

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following statements is not specifically related to product life cycle costing?

A) It considers that costs in areas such as design, marketing and customer service should be included in the true cost of the product.

B) Costs are accumulated in responsibility centres, with managers of each centre being accountable for costs, revenues or return on investment.

C) Cost is more effectively managed by more attention to the design of the process rather than effort spent on correcting an out-of-control process.

D) The amount of cash generated depends in part on the stage of the product life cycle.

A) It considers that costs in areas such as design, marketing and customer service should be included in the true cost of the product.

B) Costs are accumulated in responsibility centres, with managers of each centre being accountable for costs, revenues or return on investment.

C) Cost is more effectively managed by more attention to the design of the process rather than effort spent on correcting an out-of-control process.

D) The amount of cash generated depends in part on the stage of the product life cycle.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

46

Which of the following time drivers contribute to non-value-added activities?

I) Poor quality

Ii) Efficient inventory management

Iii) Bottlenecks in production

Iv) Poorly structured delivery processes

A) i, ii and iii

B) i, iii and iv

C) i, ii and iv

D) All of the given answers

I) Poor quality

Ii) Efficient inventory management

Iii) Bottlenecks in production

Iv) Poorly structured delivery processes

A) i, ii and iii

B) i, iii and iv

C) i, ii and iv

D) All of the given answers

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

47

Six sigma refers to:

A) business improvement methodology that involves rigours data analysis.

B) the amount of quality deviation that is considered acceptable in total quality management.

C) the formal quality accreditation relating to a series of standards recognised by an international quality setting agency.

D) the six key features of total quality management.

A) business improvement methodology that involves rigours data analysis.

B) the amount of quality deviation that is considered acceptable in total quality management.

C) the formal quality accreditation relating to a series of standards recognised by an international quality setting agency.

D) the six key features of total quality management.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following stages are considered in a product's life cycle?

I) Preliminary design

Ii) Product pricing

Iii) Product decline

A) i and ii

B) i and iii

C) ii and iii

D) i

I) Preliminary design

Ii) Product pricing

Iii) Product decline

A) i and ii

B) i and iii

C) ii and iii

D) i

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

49

When throughput increases with no change in operating expenses or inventory levels, then:

A) profit and return on investment will increase and cash flow will decrease.

B) profit will increase and return on investment and cash flow will decrease.

C) profit, return on investment and cash flow will increase.

D) profit and cash flow will increase and return on investment will decrease.

A) profit and return on investment will increase and cash flow will decrease.

B) profit will increase and return on investment and cash flow will decrease.

C) profit, return on investment and cash flow will increase.

D) profit and cash flow will increase and return on investment will decrease.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following statements best describes performance measurement in line with continuous improvement?

A) Firms select relevant performance measures.

B) The measure will keep changing over time.

C) The measure will keep improving over time.

D) The firm targets an area to improve, moving the target until the desired outcome is achieved. The firm is then likely to target another area for improvement.

A) Firms select relevant performance measures.

B) The measure will keep changing over time.

C) The measure will keep improving over time.

D) The firm targets an area to improve, moving the target until the desired outcome is achieved. The firm is then likely to target another area for improvement.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

51

From the following list of costs, determine the amount of non-value-added cost.

A) $17 000

B) $18 000

C) $16 000

D) $8000

A) $17 000

B) $18 000

C) $16 000

D) $8000

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

52

From a customer perspective, a value-added cost is one:

A) which increases the value of the product to the customer.

B) which the firm has determined is essential in the production of the product.

C) on which the firm must focus.

D) which increases the value of the product to the customer and the customer is prepared to pay for the added value.

A) which increases the value of the product to the customer.

B) which the firm has determined is essential in the production of the product.

C) on which the firm must focus.

D) which increases the value of the product to the customer and the customer is prepared to pay for the added value.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following methods may be used to overcome bottlenecks?

I) Increase staff training

Ii) Increase overtime

Iii) Reduce work in process

Iv) Acquire additional plant and equipment

A) i, ii and iii

B) ii, iii and iv

C) i, iii and iv

D) i, ii and iv

I) Increase staff training

Ii) Increase overtime

Iii) Reduce work in process

Iv) Acquire additional plant and equipment

A) i, ii and iii

B) ii, iii and iv

C) i, iii and iv

D) i, ii and iv

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

54

From the following list of costs for a kitchen manufacturer, determine the amount of value-added cost.

A) $57 000

B) $54 000

C) $58 000

D) $59 000

A) $57 000

B) $54 000

C) $58 000

D) $59 000

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

55

Assume a production process that typically moves the following number of products through its five processes:

Assuming there is room for improvement in all processes, in what order of processes would the firm apply the theory of constraints to remove the bottlenecks?

A) 4 first, and then any order

B) 2, 1, 3, 5, 4

C) Work must be carried out in order of the physical flow of activities, i.e. 1, 2, 3, 4, 5

D) 4, 5, 3, 1, 2

Assuming there is room for improvement in all processes, in what order of processes would the firm apply the theory of constraints to remove the bottlenecks?

A) 4 first, and then any order

B) 2, 1, 3, 5, 4

C) Work must be carried out in order of the physical flow of activities, i.e. 1, 2, 3, 4, 5

D) 4, 5, 3, 1, 2

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following statements is consistent with target costing?

A) It does not consider market share or sales volume.

B) Market prices are used to determine product costs.

C) Product design has little or no regard for the long-run manufacturing costs.

D) It is described as a reactive costing strategy, rather than a proactive costing strategy.

A) It does not consider market share or sales volume.

B) Market prices are used to determine product costs.

C) Product design has little or no regard for the long-run manufacturing costs.

D) It is described as a reactive costing strategy, rather than a proactive costing strategy.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

57

When inventory decreases with no change in throughput or operating expenses, then:

A) profit will increase and return on investment and cash flow will decrease.

B) profit, return on investment and cash flow will increase.

C) profit and cash flow will increase and return on investment will decrease.

D) profit, return on investment and cash flow will decrease.

A) profit will increase and return on investment and cash flow will decrease.

B) profit, return on investment and cash flow will increase.

C) profit and cash flow will increase and return on investment will decrease.

D) profit, return on investment and cash flow will decrease.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

58

What management approaches might be used to overcome the problem of poorly structured production processes?

I) Value analysis to identify and remove non-value-added activities.

Ii) Implement continuous improvement processes.

Iii) Process re-engineering.

A) i

B) i and iii

C) iii

D) All of the given answers

I) Value analysis to identify and remove non-value-added activities.

Ii) Implement continuous improvement processes.

Iii) Process re-engineering.

A) i

B) i and iii

C) iii

D) All of the given answers

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

59

The removal of bottlenecks has which of the following benefits?

I) Increased customer value

Ii) Reduced costs

Iii) Improved quality

Iv) Increased profitability

A) ii, iii and iv

B) i, iii and iv

C) i, ii and iv

D) All of the given answers

I) Increased customer value

Ii) Reduced costs

Iii) Improved quality

Iv) Increased profitability

A) ii, iii and iv

B) i, iii and iv

C) i, ii and iv

D) All of the given answers

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

60

Throughput accounting uses which of the following measures of the effects of bottlenecks?

I) Financial measures of inventory

Ii) Financial measures of throughput

Iii) Non-financial measures of throughput

Iv) Operating expenses

A) i, ii and iii

B) ii, iii and iv

C) i, iii and iv

D) i, ii and iv

I) Financial measures of inventory

Ii) Financial measures of throughput

Iii) Non-financial measures of throughput

Iv) Operating expenses

A) i, ii and iii

B) ii, iii and iv

C) i, iii and iv

D) i, ii and iv

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

61

Business Process Re-engineering (BPR) focuses on the processes that are essential to achieving the company's business objectives and strategies. As each process is identified the four major steps used in BPR are applied. Describe these four major steps.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

62

Identify and describe the major differences between the traditional approach to cost control and modern cost management.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

63

Three processes are involved in the manufacturing of Product X. First, the components go through the Machining Process, then the Assembling Process, and finally the Packaging Process. The hourly production capacity of the three processes is 500 units, 600 units and 800 units respectively. How many units of Product X can be produced in one hour?

A) 500 units

B) 600 units

C) 800 units

D) 633 units

A) 500 units

B) 600 units

C) 800 units

D) 633 units

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

64

Lazy Linda Ltd manufactures small kitchen appliances. One of the non-value added activities identified by the production manager is 'reworking the electrical component in a toaster'. Which of the following is a likely root cause cost driver?

A) The number of products requiring rework.

B) The quality of the completed toaster.

C) The quality of the electrical wiring purchased from suppliers.

D) Idle labour hours.

A) The number of products requiring rework.

B) The quality of the completed toaster.

C) The quality of the electrical wiring purchased from suppliers.

D) Idle labour hours.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

65

The underlying factors that trigger costs to be incurred when an activity is performed are known as:

A) activity trigger costs.

B) root cause.

C) cost driver analysis.

D) root cause cost driver.

A) activity trigger costs.

B) root cause.

C) cost driver analysis.

D) root cause cost driver.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

66

When monitored, activity-based performance measures can provide managers with feedback on their:

A) budgets.

B) targets.

C) performance.

D) initiatives.

A) budgets.

B) targets.

C) performance.

D) initiatives.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

67

Lazy Linda Kitchen Appliances manufactures small kitchen appliances such as toasters and blenders. Last month Lazy Linda recorded the following quality costs:

Lazy Linda's total appraisal cost was:

A) $5000.

B) $9500.

C) $12 000.

D) $18 000.

Lazy Linda's total appraisal cost was:

A) $5000.

B) $9500.

C) $12 000.

D) $18 000.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

68

A value-added activity provides essential value to:

A) customers and management.

B) management and employees.

C) customers and the functioning of the business.

D) management and the functioning of the business.

A) customers and management.

B) management and employees.

C) customers and the functioning of the business.

D) management and the functioning of the business.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

69

Discuss how life cycle budgeting can provide useful information for managing and reducing costs. Provide and explain a graph to support your discussion.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

70

When management uses financial measures to determine the effect of bottlenecks and operational decisions, they are likely to be using:

A) activity-based costing.

B) throughput accounting.

C) total quality management.

D) financial evaluation.

A) activity-based costing.

B) throughput accounting.

C) total quality management.

D) financial evaluation.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

71

Define the term 'bottleneck' and describe how the application of the 'theory of constraints' can assist management in production.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

72

Lazy Linda Kitchen Appliances manufactures small kitchen appliances such as toasters and blenders. Last month Lazy Linda recorded the following quality costs:

Lazy Linda's total external failure cost was:

A) $6000.

B) $9000.

C) $12 000.

D) $15 000.

Lazy Linda's total external failure cost was:

A) $6000.

B) $9000.

C) $12 000.

D) $15 000.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

73

Lazy Linda Kitchen Appliances manufactures small kitchen appliances such as toasters and blenders. Last month Lazy Linda recorded the following quality costs:

Lazy Linda's total prevention cost was:

A) $5000.

B) $11 000.

C) $14 000.

D) $15 500.

Lazy Linda's total prevention cost was:

A) $5000.

B) $11 000.

C) $14 000.

D) $15 500.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

74

Lazy Linda Kitchen Appliances manufactures small kitchen appliances such as toasters and blenders. Last month Lazy Linda recorded the following quality costs:

Lazy Linda's total internal failure cost was:

A) $9500.

B) $7500.

C) $5000.

D) $2000.

Lazy Linda's total internal failure cost was:

A) $9500.

B) $7500.

C) $5000.

D) $2000.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

75

Lazy Linda Kitchen Appliances has just begun the development of a new energy-saving, voice-activated toaster. The accountant, Linda Rest, is preparing a life cycle budget. Which of the following costs should be included?

I) The salaries of the designers dedicated to the design of the new toaster.

Ii) The committed costs associated with the acquisition of a new machine that manufacturers the voice recognition component of the toaster.

Iii) The cost of producing the new toasters.

Iv) The costs associated with establishing a distribution network for the new product.

A) i, ii and iii

B) i, iii and iv

C) ii and iii

D) All of these costs should be included.

I) The salaries of the designers dedicated to the design of the new toaster.

Ii) The committed costs associated with the acquisition of a new machine that manufacturers the voice recognition component of the toaster.

Iii) The cost of producing the new toasters.

Iv) The costs associated with establishing a distribution network for the new product.

A) i, ii and iii

B) i, iii and iv

C) ii and iii

D) All of these costs should be included.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

76

Three processes are involved in the manufacturing of Chemical Z. First, the raw mixture goes through the Mixing Process, then the Heating Process, and finally the Bottling Process. The hourly production capacity of the three processes is 400 units, 600 units and 400 units respectively. Assume that a recent process improvement has resulted in a 20 per cent increase in the capacity of the Bottling Process. This process improvement will:

A) increase the production of Chemical Z by 80 units per hour.

B) increase the production of Chemical Z by 120 units per hour.

C) increase the production of Chemical Z by 200 units.

D) have no effect on the production level per hour.

A) increase the production of Chemical Z by 80 units per hour.

B) increase the production of Chemical Z by 120 units per hour.

C) increase the production of Chemical Z by 200 units.

D) have no effect on the production level per hour.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

77

The cost reduction objective is the difference between:

A) the target cost and the current cost.

B) the target profit and the target cost.

C) the target selling price and the current cost.

D) the current cost and the target profit.

A) the target cost and the current cost.

B) the target profit and the target cost.

C) the target selling price and the current cost.

D) the current cost and the target profit.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

78

Describe how target costing assists management in determining the life cycle cost of a product and the approach management would take if the planned level of sales could not be achieved at the cost-plus price.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

79

When a manufacturer incurs costs to determine whether defects exist in their products, these costs are known as:

A) internal failure costs.

B) external failure costs.

C) appraisal costs.

D) prevention costs.

A) internal failure costs.

B) external failure costs.

C) appraisal costs.

D) prevention costs.

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

80

Which of the following statements about throughput accounting is false?

A) Throughput accounting is criticised for having a short-term focus.

B) Under throughput accounting, operating expenses are not relevant.

C) Throughput accounting measures the financial effects of bottlenecks.

D) Under throughput accounting, inventory is considered undesirable..

A) Throughput accounting is criticised for having a short-term focus.

B) Under throughput accounting, operating expenses are not relevant.

C) Throughput accounting measures the financial effects of bottlenecks.

D) Under throughput accounting, inventory is considered undesirable..

Unlock Deck

Unlock for access to all 92 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 92 flashcards in this deck.