Deck 11: Standard Costs for Control: Flexible Budgets and Manufacturing Overhead

Full screen (f)

Question

Question

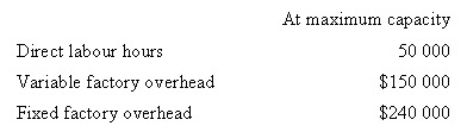

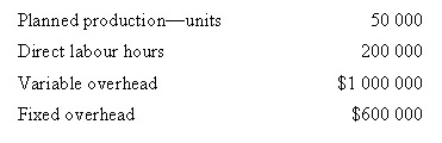

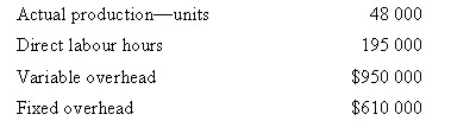

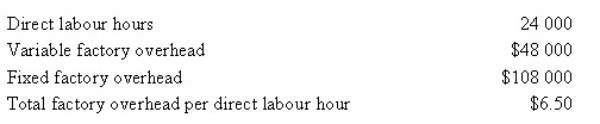

Star Company is preparing a flexible budget for 2008 and the following maximum capacity estimates for department Z are:

Assume that Star's normal capacity is 80 per cent of maximum capacity.What would be the total factory overhead rate per direct labour hour in a flexible budget at normal capacity?

A) $6.00

B) $6.50

C) $7.50

D) None of the given answers

Assume that Star's normal capacity is 80 per cent of maximum capacity.What would be the total factory overhead rate per direct labour hour in a flexible budget at normal capacity?

A) $6.00

B) $6.50

C) $7.50

D) None of the given answers

Question

Question

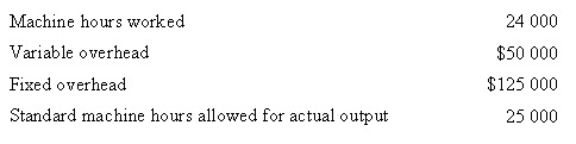

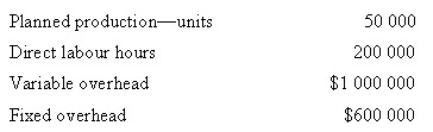

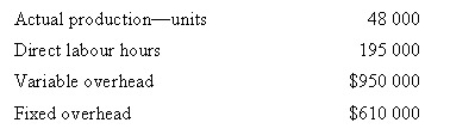

Dean Company used a standard cost system to prepare the following budget at normal capacity for the month of May.Actual data for May were as follows:

Determine the fixed overhead budget and volume variances.

Budget

Volume

A) $5000 F

$5000 U

B) $5000 U

$0

C) $5000 U

$5000 F

D) $0

$5000 U

Determine the fixed overhead budget and volume variances.

Budget

Volume

A) $5000 F

$5000 U

B) $5000 U

$0

C) $5000 U

$5000 F

D) $0

$5000 U

Question

Question

Question

Question

Question

Question

Question

Question

A flexible budget for Heath Company for 5 000 hours is shown below:

What are the total overhead costs for 10 000 hours?

A) $35 000

B) $45 000

C) $50 000

D) $60 000

What are the total overhead costs for 10 000 hours?

A) $35 000

B) $45 000

C) $50 000

D) $60 000

Question

Question

Question

Question

Question

Question

Question

Question

Question

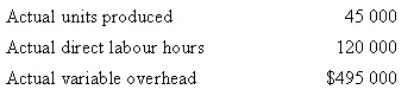

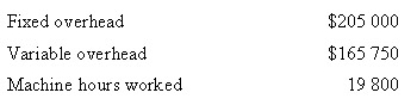

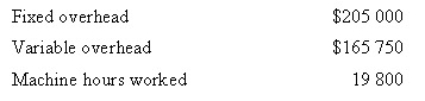

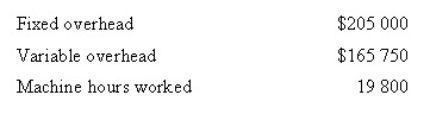

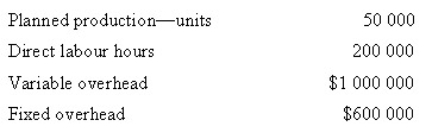

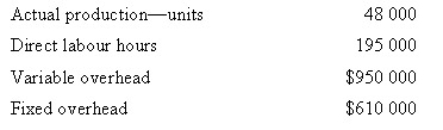

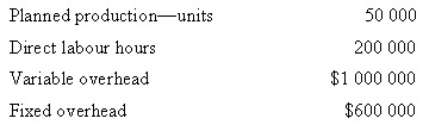

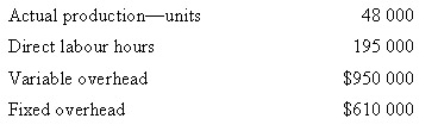

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.What was Carvelle's fixed overhead budget variance?

A) $2000 unfavourable

B) $7000 unfavourable

C) $5000 unfavourable

D) $4000 favourable

A) $2000 unfavourable

B) $7000 unfavourable

C) $5000 unfavourable

D) $4000 favourable

Question

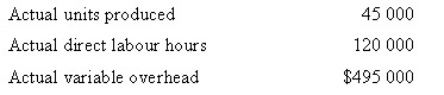

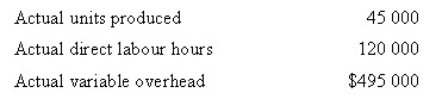

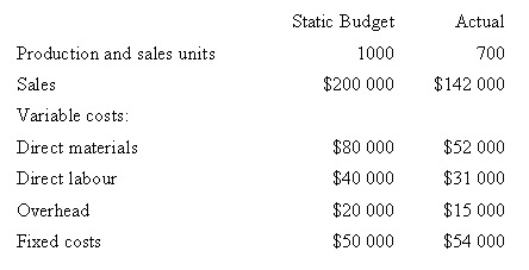

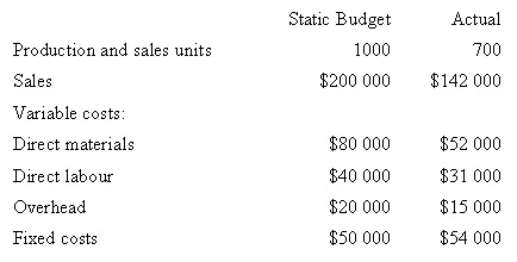

Security Doors has a standard variable overhead rate of $4 per direct labour hour.The standard quantity of direct labour per unit of production is 3 hours.The company's static budget was based on 50 000 units.Actual results for the year are as follows.What is Security Door's flexible budget for variable overhead costs for the actual output?

A) $600 000

B) $540 000

C) $495 000

D) $432 000

A) $600 000

B) $540 000

C) $495 000

D) $432 000

Question

Question

Question

Question

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.How many units had Carvelle budgeted to produce?

A) 5100

B) 5000

C) 20 000

D) Insufficient information to determine

A) 5100

B) 5000

C) 20 000

D) Insufficient information to determine

Question

Question

Security Doors has a standard variable overhead rate of $4 per direct labour hour.The standard quantity of direct labour per unit of production is 3 hours.The company's static budget was based on 50 000 units.Actual results for the year are as follows.What was Security Door's variable overhead efficiency variance?

A) $45 000 favourable

B) $60 000 favourable

C) $45 000 unfavourable

D) $60 000 unfavourable

A) $45 000 favourable

B) $60 000 favourable

C) $45 000 unfavourable

D) $60 000 unfavourable

Question

Question

Question

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.What was the amount of total overhead (fixed and variable)applied to work in process inventory during 2008?

A) $356 400

B) $365 750

C) $367 200

D) $370 750

A) $356 400

B) $365 750

C) $367 200

D) $370 750

Question

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.What was Carvelle's fixed overhead volume variance?

A) $4000 favourable

B) $1000 unfavourable

C) $2000 favourable

D) $4000 unfavourable

A) $4000 favourable

B) $1000 unfavourable

C) $2000 favourable

D) $4000 unfavourable

Question

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.What was Carvelle's variable overhead efficiency variance?

A) $4800 favourable

B) $2550 unfavourable

C) $7350 unfavourable

D) $4800 unfavourable

A) $4800 favourable

B) $2550 unfavourable

C) $7350 unfavourable

D) $4800 unfavourable

Question

Question

Question

Security Doors has a standard variable overhead rate of $4 per direct labour hour.The standard quantity of direct labour per unit of production is 3 hours.The company's static budget was based on 50 000 units.Actual results for the year are as follows.What was Security Door's variable overhead spending variance?

A) $45 000 favourable

B) $60 000 favourable

C) $15 000 unfavourable

D) $45 000 unfavourable

A) $45 000 favourable

B) $60 000 favourable

C) $15 000 unfavourable

D) $45 000 unfavourable

Question

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.What was the total amount of under/overapplied overhead for the firm?

A) $3550 under

B) $3550 over

C) $3550 debit

D) Both A and C

A) $3550 under

B) $3550 over

C) $3550 debit

D) Both A and C

Question

Question

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.What was Carvelle's variable overhead spending variance?

A) $7350 unfavourable

B) $2550 unfavourable

C) $4800 favourable

D) $7350 favourable

A) $7350 unfavourable

B) $2550 unfavourable

C) $4800 favourable

D) $7350 favourable

Question

Question

Question

Question

Question

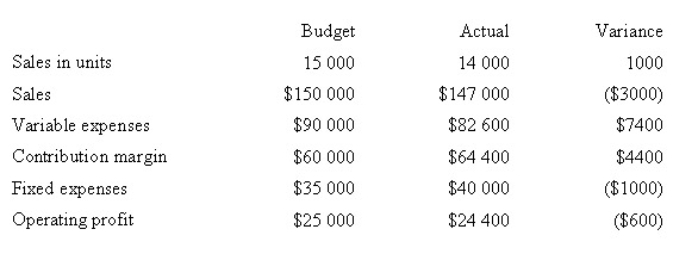

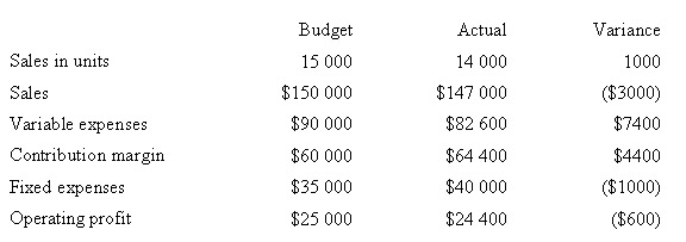

Master Products has the following information at the end of the year:

What is Master Product's sales price variance?

A) $3000 favourable

B) $7500 favourable

C) $7000 favourable

D) $10 000 unfavourable

What is Master Product's sales price variance?

A) $3000 favourable

B) $7500 favourable

C) $7000 favourable

D) $10 000 unfavourable

Question

Question

Question

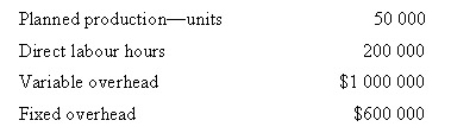

Hamilton Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

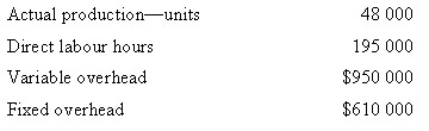

The following were the actual results:

Calculate the total amount of underapplied or overapplied manufacturing overhead.

A) $80 000 underapplied

B) $64 000 underapplied

C) $50 000 overapplied

D) $24 000 underapplied

The following were the actual results:

Calculate the total amount of underapplied or overapplied manufacturing overhead.

A) $80 000 underapplied

B) $64 000 underapplied

C) $50 000 overapplied

D) $24 000 underapplied

Question

Hamilton Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

The following were the actual results:

Calculate the amount of overhead cost applied to work in process inventory.

A) $1 520 000

B) $1 536 000

C) $1 550 000

D) $1 600 000

The following were the actual results:

Calculate the amount of overhead cost applied to work in process inventory.

A) $1 520 000

B) $1 536 000

C) $1 550 000

D) $1 600 000

Question

Hamilton Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

The following were the actual results:

Calculate the fixed overhead volume variance.

A) $24 000 favourable

B) $24 000 unfavourable

C) $34 000 favourable

D) $10 000 unfavourable

The following were the actual results:

Calculate the fixed overhead volume variance.

A) $24 000 favourable

B) $24 000 unfavourable

C) $34 000 favourable

D) $10 000 unfavourable

Question

Bozo Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

Calculate the total standard overhead rate per direct labour hour (variable and fixed).

A) $0.125

B) $4.06

C) $8.00

D) $8.20

Calculate the total standard overhead rate per direct labour hour (variable and fixed).

A) $0.125

B) $4.06

C) $8.00

D) $8.20

Question

Question

Master Products has the following information at the end of the year.What is Master Product's sales volume variance?

A) $10 000 unfavourable

B) $4000 unfavourable

C) $4400 favourable

D) $3000 unfavourable

A) $10 000 unfavourable

B) $4000 unfavourable

C) $4400 favourable

D) $3000 unfavourable

Question

Framlingham uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

The following were the actual results:

Calculate the variable overhead spending variance.

A) $25 000 favourable

B) $50 000 favourable

C) $25 000 unfavourable

D) $10 000 unfavourable

The following were the actual results:

Calculate the variable overhead spending variance.

A) $25 000 favourable

B) $50 000 favourable

C) $25 000 unfavourable

D) $10 000 unfavourable

Question

Question

Question

Hamilton Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

The following were the actual results:

Calculate the amount of fixed overhead budget variance.

A) $10 000 favourable

B) $10 000 unfavourable

C) $24 000 favourable

D) $34 000 unfavourable

The following were the actual results:

Calculate the amount of fixed overhead budget variance.

A) $10 000 favourable

B) $10 000 unfavourable

C) $24 000 favourable

D) $34 000 unfavourable

Question

Question

Question

Hamilton Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

The following were the actual results:

Calculate the amount of variable overhead spending variance.

A) $25 000 favourable

B) $15 000 unfavourable

C) $25 000 unfavourable

D) $15 000 favourable

The following were the actual results:

Calculate the amount of variable overhead spending variance.

A) $25 000 favourable

B) $15 000 unfavourable

C) $25 000 unfavourable

D) $15 000 favourable

Question

Hamilton Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

The following were the actual results:

Calculate the amount of variable overhead efficiency variance.

A) $25 000 favourable

B) $25 000 unfavourable

C) $15 000 favourable

D) $15 000 unfavourable

The following were the actual results:

Calculate the amount of variable overhead efficiency variance.

A) $25 000 favourable

B) $25 000 unfavourable

C) $15 000 favourable

D) $15 000 unfavourable

Question

Question

Question

Question

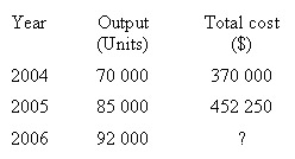

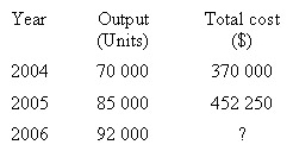

The following table provides information about a company's production.If variable costs increased in 2005 by 10 per cent and fixed overheads increased in 2006 by 20 per cent,what was the variable cost per unit in 2004?

A) $3.35

B) $3.40

C) $3.45

D) $3.50

A) $3.35

B) $3.40

C) $3.45

D) $3.50

Question

Question

Z Company uses a variable costing system.There was no opening or closing stock.The following data is available:

Use this data to determine Z's sales volume variance:

A) $8000 unfavourable

B) $18 000 unfavourable

C) $60 000 unfavourable

D) $18 000 favourable

Use this data to determine Z's sales volume variance:

A) $8000 unfavourable

B) $18 000 unfavourable

C) $60 000 unfavourable

D) $18 000 favourable

Question

Z Company uses a variable costing system.There was no opening or closing stock.The following data is available.Use this data to determine Z's sales price variance.

A) $2000 favourable

B) $10 000 unfavourable

C) $58 000 unfavourable

D) $10 000 favourable

A) $2000 favourable

B) $10 000 unfavourable

C) $58 000 unfavourable

D) $10 000 favourable

Question

Question

Universal Pty Ltd used a standard cost system to prepare the following budget at normal operating capacity for the month of January 2007.Actual data for January 2007 were as follows:

Using the two-way analysis of overhead variances,what is the total of the fixed budget variance and the variable overhead spending variance for January 2007?

A) $3000 favourable

B) $5000 favourable

C) $9000 favourable

D) $3000 unfavourable

Using the two-way analysis of overhead variances,what is the total of the fixed budget variance and the variable overhead spending variance for January 2007?

A) $3000 favourable

B) $5000 favourable

C) $9000 favourable

D) $3000 unfavourable

Question

Question

The following table provides information about a company's production.If variable costs increased in 2005 by 10 per cent and fixed overheads increased in 2006 by 20 per cent,what was the estimated total cost in 2006?

A) $447 600

B) $472 800

C) $504 200

D) More than $514 400

A) $447 600

B) $472 800

C) $504 200

D) More than $514 400

Question

Question

Question

Question

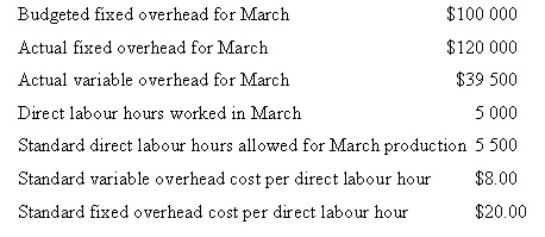

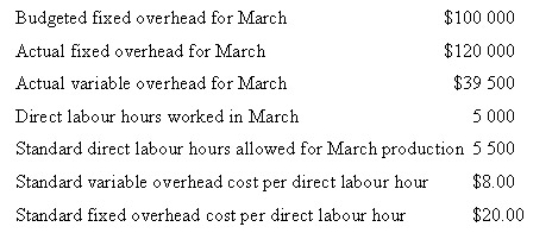

Use the following data to determine the company's variable overhead spending variance for March.

A) $500 favourable

B) $500 unfavourable

C) $4 500 favourable

D) $4 500 unfavourable

A) $500 favourable

B) $500 unfavourable

C) $4 500 favourable

D) $4 500 unfavourable

Question

Question

Use the following data to determine the company's fixed overhead volume variance for March.

A) $10 000 overapplied

B) $10 000 underapplied

C) $20 000 overapplied

D) $20 000 underapplied

A) $10 000 overapplied

B) $10 000 underapplied

C) $20 000 overapplied

D) $20 000 underapplied

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/97

Play

Full screen (f)

Deck 11: Standard Costs for Control: Flexible Budgets and Manufacturing Overhead

1

DBC Company applies fixed overhead at $8 per machine hour.During the year actual fixed overhead amounted to $75 000 and the standard machine hours allowed for units produced was 11 000.Budgeted fixed overhead was $80 000.Which of the following is the best description of the items used to calculate the volume variance?

A.

$80 000

$88 000

ignore

B.

$88 000

$88 000

ignore

C.

$88 000

$75 000

ignore

D.

ignore

$88 000

$75 000

A.

$80 000

$88 000

ignore

B.

$88 000

$88 000

ignore

C.

$88 000

$75 000

ignore

D.

ignore

$88 000

$75 000

Budgeted FOH

Applied FOH

Actual FOH

A.

$80 000

$88 000

ignore

B.

$88 000

$88 000

ignore

C.

$88 000

$75 000

ignore

D.

ignore

$88 000

$75 000

Applied FOH

Actual FOH

A.

$80 000

$88 000

ignore

B.

$88 000

$88 000

ignore

C.

$88 000

$75 000

ignore

D.

ignore

$88 000

$75 000

2

Star Company is preparing a flexible budget for 2008 and the following maximum capacity estimates for department Z are:

Assume that Star's normal capacity is 80 per cent of maximum capacity.What would be the total factory overhead rate per direct labour hour in a flexible budget at normal capacity?

A) $6.00

B) $6.50

C) $7.50

D) None of the given answers

Assume that Star's normal capacity is 80 per cent of maximum capacity.What would be the total factory overhead rate per direct labour hour in a flexible budget at normal capacity?

A) $6.00

B) $6.50

C) $7.50

D) None of the given answers

D

3

In a standard costing system,the total manufacturing overhead variance is measured as:

A) the difference between applied overhead based on actual output and actual overhead cost incurred

B) the difference between actual overhead costs for two subsequent periods

C) the difference between overhead costs in the flexible budget for two subsequent periods

D) the difference between standard overhead applied and the overhead cost in the flexible budget

A) the difference between applied overhead based on actual output and actual overhead cost incurred

B) the difference between actual overhead costs for two subsequent periods

C) the difference between overhead costs in the flexible budget for two subsequent periods

D) the difference between standard overhead applied and the overhead cost in the flexible budget

A

4

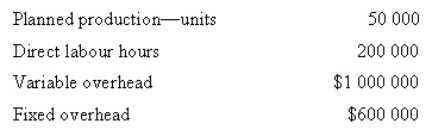

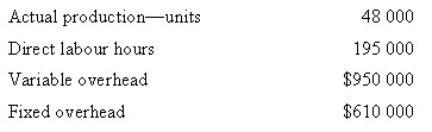

Dean Company used a standard cost system to prepare the following budget at normal capacity for the month of May.Actual data for May were as follows:

Determine the fixed overhead budget and volume variances.

Budget

Volume

A) $5000 F

$5000 U

B) $5000 U

$0

C) $5000 U

$5000 F

D) $0

$5000 U

Determine the fixed overhead budget and volume variances.

Budget

Volume

A) $5000 F

$5000 U

B) $5000 U

$0

C) $5000 U

$5000 F

D) $0

$5000 U

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following cannot cause an unfavourable variable overhead efficiency variance?

A) Using more direct labour hours or direct machine hours than the standard quantity,given actual output.

B) Higher than expected production accomplished in less than the standard machine hours allowed.

C) Using more of the variable overhead item,such as electricity,than the standard amount allowed.

D) All of the given answers

A) Using more direct labour hours or direct machine hours than the standard quantity,given actual output.

B) Higher than expected production accomplished in less than the standard machine hours allowed.

C) Using more of the variable overhead item,such as electricity,than the standard amount allowed.

D) All of the given answers

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

6

The predetermined fixed overhead rate is found by:

A) budgeted total overhead / actual total activity

B) actual fixed overhead / planned activity measure

C) budgeted fixed overhead / planned activity measure

D) budgeted fixed overhead / actual activity measure

A) budgeted total overhead / actual total activity

B) actual fixed overhead / planned activity measure

C) budgeted fixed overhead / planned activity measure

D) budgeted fixed overhead / actual activity measure

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following statements on flexible budgets is false?

A) It enables companies to control overhead costs.

B) It can be used to calculate direct material and direct labour variances.

C) It is the same as a static budget.

D) It provides a useful basis for comparison between actual and expected costs for a given level of activity.

A) It enables companies to control overhead costs.

B) It can be used to calculate direct material and direct labour variances.

C) It is the same as a static budget.

D) It provides a useful basis for comparison between actual and expected costs for a given level of activity.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following formulas is the relationship between activity and total budgeted overhead cost is represented by?

A) Budgeted variable overhead cost per unit × total activity units

B) Budgeted variable overhead cost per unit + budgeted fixed overhead cost

C) (Budgeted variable overhead cost per unit × total activity units)+ budgeted fixed overhead costs

D) (Budgeted fixed overhead cost per unit × total activity units)+ (budgeted variable overhead cost per unit × total activity units)

A) Budgeted variable overhead cost per unit × total activity units

B) Budgeted variable overhead cost per unit + budgeted fixed overhead cost

C) (Budgeted variable overhead cost per unit × total activity units)+ budgeted fixed overhead costs

D) (Budgeted fixed overhead cost per unit × total activity units)+ (budgeted variable overhead cost per unit × total activity units)

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

9

Assume the number of machine hours is the cost driver for variable overhead.The difference between the actual variable overhead and the flexible budget for variable overhead (based on standard machine hours allowed for actual output)is the:

A) volume variance

B) net overhead variance

C) efficiency variance

D) sum of variable spending and efficiency variances

A) volume variance

B) net overhead variance

C) efficiency variance

D) sum of variable spending and efficiency variances

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

10

Overhead application refers to:

A) the addition of overhead cost to work in process inventory as a product cost

B) a system of allocating manufacturing cost to products

C) static budget applications

D) Both the addition of overhead cost to work in process inventory as a product cost AND a system of allocating manufacturing cost to products

A) the addition of overhead cost to work in process inventory as a product cost

B) a system of allocating manufacturing cost to products

C) static budget applications

D) Both the addition of overhead cost to work in process inventory as a product cost AND a system of allocating manufacturing cost to products

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following is used in the calculation of the variable overhead spending variance?

Flexible budget based on standard hours allowed

Standard variable overhead applied to production

Flexible budget based on actual hours

A) Yes

Yes

Yes

B) Yes

No

No

C) No

Yes

No

D) No

No

Yes

Flexible budget based on standard hours allowed

Standard variable overhead applied to production

Flexible budget based on actual hours

A) Yes

Yes

Yes

B) Yes

No

No

C) No

Yes

No

D) No

No

Yes

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

12

A flexible budget for Heath Company for 5 000 hours is shown below:

What are the total overhead costs for 10 000 hours?

A) $35 000

B) $45 000

C) $50 000

D) $60 000

What are the total overhead costs for 10 000 hours?

A) $35 000

B) $45 000

C) $50 000

D) $60 000

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following statements is true?

A) In a standard costing system,standard costs can only be used for cost control.

B) In a standard costing system,standard costs can only be used for product costing.

C) In a standard costing system,standard costs are used for both cost control and product costing.

D) In a normal costing system,standard costs are used for cost control and normal costs are used for product costing.

A) In a standard costing system,standard costs can only be used for cost control.

B) In a standard costing system,standard costs can only be used for product costing.

C) In a standard costing system,standard costs are used for both cost control and product costing.

D) In a normal costing system,standard costs are used for cost control and normal costs are used for product costing.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

14

A static budget is always:

A) based on a specific planned activity level

B) based on a range of activity within which the firm may operate

C) the same as a flexible budget

D) based on maximum capacity

A) based on a specific planned activity level

B) based on a range of activity within which the firm may operate

C) the same as a flexible budget

D) based on maximum capacity

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

15

The activity measure for overhead allocation should be one:

A) that varies in a similar pattern to the way that variable overhead varies

B) that follows a fixed pattern

C) that has a magnitude that never changes

D) that is always based on units produced,not on hours used

A) that varies in a similar pattern to the way that variable overhead varies

B) that follows a fixed pattern

C) that has a magnitude that never changes

D) that is always based on units produced,not on hours used

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is used in the computation of the variable overhead spending variance?

Actual variable

Factory overhead

Flexible budget based

On standard hours

Standard variable

Overhead rate

A) No

Yes

No

B) No

No

No

C) Yes

No

Yes

D) Yes

Yes

Yes

Actual variable

Factory overhead

Flexible budget based

On standard hours

Standard variable

Overhead rate

A) No

Yes

No

B) No

No

No

C) Yes

No

Yes

D) Yes

Yes

Yes

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

17

When a flexible budget is used,a decrease in the actual production level within a range of activity would:

A) decrease variable cost per unit

B) decrease total variable costs

C) increase variable cost per unit

D) decrease fixed cost per unit

A) decrease variable cost per unit

B) decrease total variable costs

C) increase variable cost per unit

D) decrease fixed cost per unit

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following is used in the computation of the variable overhead spending variance?

A.

No

Yes

No

B.

No

No

No

C.

Yes

No

Yes

D.

Yes

Yes

Yes

A.

No

Yes

No

B.

No

No

No

C.

Yes

No

Yes

D.

Yes

Yes

Yes

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

19

A flexible budget is appropriate for a:

Sales commission budget

Direct material budget

Variable overhead budget

A) Yes

No

Yes

B) Yes

Yes

Yes

C) No

Yes

No

D) No

No

No

Sales commission budget

Direct material budget

Variable overhead budget

A) Yes

No

Yes

B) Yes

Yes

Yes

C) No

Yes

No

D) No

No

No

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

20

The difference between the actual manufacturing overhead and the manufacturing overhead applied to production is the:

A) sum of spending,efficiency,budget and volume variances

B) efficiency variance

C) spending variance

D) volume variance

A) sum of spending,efficiency,budget and volume variances

B) efficiency variance

C) spending variance

D) volume variance

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

21

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.What was Carvelle's fixed overhead budget variance?

A) $2000 unfavourable

B) $7000 unfavourable

C) $5000 unfavourable

D) $4000 favourable

A) $2000 unfavourable

B) $7000 unfavourable

C) $5000 unfavourable

D) $4000 favourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

22

Security Doors has a standard variable overhead rate of $4 per direct labour hour.The standard quantity of direct labour per unit of production is 3 hours.The company's static budget was based on 50 000 units.Actual results for the year are as follows.What is Security Door's flexible budget for variable overhead costs for the actual output?

A) $600 000

B) $540 000

C) $495 000

D) $432 000

A) $600 000

B) $540 000

C) $495 000

D) $432 000

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

23

The fixed overhead budget variance compares:

A) actual variable overhead with actual fixed overhead

B) budgeted variable overhead with budgeted fixed overhead

C) actual fixed overhead with budgeted fixed overhead

D) actual total cost of units produced with the budgeted production

A) actual variable overhead with actual fixed overhead

B) budgeted variable overhead with budgeted fixed overhead

C) actual fixed overhead with budgeted fixed overhead

D) actual total cost of units produced with the budgeted production

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

24

Atrex Company determined that its variable overhead spending variance was $10 000 unfavourable for the year.Actual variable overhead was $100 000 for the year.Variable overhead is applied based on machine hours.The standard rate per machine hour was $9.The standard quantity of machine hours allowed for good output was 9000.What was the actual quantity of machine hours used?

A) 12 222

B) 11 000

C) 10 000

D) 9000

A) 12 222

B) 11 000

C) 10 000

D) 9000

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

25

Why is the budget variance the real control variance,for fixed overhead?

A) It compares budgeted expenditures with budgeted fixed overhead costs.

B) It compares actual expenditures with budgeted fixed overhead costs.

C) It compares actual expenditures with budgeted variable overhead costs.

D) It compares the static budget with the flexible budget.

A) It compares budgeted expenditures with budgeted fixed overhead costs.

B) It compares actual expenditures with budgeted fixed overhead costs.

C) It compares actual expenditures with budgeted variable overhead costs.

D) It compares the static budget with the flexible budget.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

26

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.How many units had Carvelle budgeted to produce?

A) 5100

B) 5000

C) 20 000

D) Insufficient information to determine

A) 5100

B) 5000

C) 20 000

D) Insufficient information to determine

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

27

As overall productive activity changes,the following should move in the same direction,in roughly the same proportion:

A) total variable overhead cost;standard variable overhead rate

B) total variable overhead cost;fixed overhead budget variance

C) cost driver;total variable overhead cost

D) cost driver;fixed overhead cost

A) total variable overhead cost;standard variable overhead rate

B) total variable overhead cost;fixed overhead budget variance

C) cost driver;total variable overhead cost

D) cost driver;fixed overhead cost

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

28

Security Doors has a standard variable overhead rate of $4 per direct labour hour.The standard quantity of direct labour per unit of production is 3 hours.The company's static budget was based on 50 000 units.Actual results for the year are as follows.What was Security Door's variable overhead efficiency variance?

A) $45 000 favourable

B) $60 000 favourable

C) $45 000 unfavourable

D) $60 000 unfavourable

A) $45 000 favourable

B) $60 000 favourable

C) $45 000 unfavourable

D) $60 000 unfavourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following best describes the cost of underutilising productive capacity?

A) Lost sales of products that are produced.

B) Lost contribution margin of products that are not produced.

C) An implicit cost that is inevitable.

D) There is no cost.

A) Lost sales of products that are produced.

B) Lost contribution margin of products that are not produced.

C) An implicit cost that is inevitable.

D) There is no cost.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

30

Budgeted fixed overhead is the basis for controlling fixed overhead because:

A) it provides the benchmark against which actual expenditure is compared

B) fixed overhead does not change as production activity varies

C) budgeted fixed overhead is the same at all activity levels in the flexible budget

D) All of the given answers

A) it provides the benchmark against which actual expenditure is compared

B) fixed overhead does not change as production activity varies

C) budgeted fixed overhead is the same at all activity levels in the flexible budget

D) All of the given answers

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

31

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.What was the amount of total overhead (fixed and variable)applied to work in process inventory during 2008?

A) $356 400

B) $365 750

C) $367 200

D) $370 750

A) $356 400

B) $365 750

C) $367 200

D) $370 750

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

32

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.What was Carvelle's fixed overhead volume variance?

A) $4000 favourable

B) $1000 unfavourable

C) $2000 favourable

D) $4000 unfavourable

A) $4000 favourable

B) $1000 unfavourable

C) $2000 favourable

D) $4000 unfavourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

33

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.What was Carvelle's variable overhead efficiency variance?

A) $4800 favourable

B) $2550 unfavourable

C) $7350 unfavourable

D) $4800 unfavourable

A) $4800 favourable

B) $2550 unfavourable

C) $7350 unfavourable

D) $4800 unfavourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

34

What can create the variable overhead efficiency variance?

A) Efficient or inefficient usage of a specific component of variable overhead (e.g.electricity)

B) Production of units for finished goods inventory versus production for sale

C) Efficient or inefficient use of the cost driver (e.g.machine hours)for variable overhead

D) A difference between the planned level of output and the actual level of output

A) Efficient or inefficient usage of a specific component of variable overhead (e.g.electricity)

B) Production of units for finished goods inventory versus production for sale

C) Efficient or inefficient use of the cost driver (e.g.machine hours)for variable overhead

D) A difference between the planned level of output and the actual level of output

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

35

When does budgeted fixed overhead differ from applied fixed overhead? (Assume the number of machine hours is the activity base. )

A) During any period in which the number of standard machine hours allowed differs from the budgeted or planned activity level.

B) It always differs.

C) During any period in which actual overhead costs exceed planned overhead costs.

D) During any period in which budgeted production equals planned production.

A) During any period in which the number of standard machine hours allowed differs from the budgeted or planned activity level.

B) It always differs.

C) During any period in which actual overhead costs exceed planned overhead costs.

D) During any period in which budgeted production equals planned production.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

36

Security Doors has a standard variable overhead rate of $4 per direct labour hour.The standard quantity of direct labour per unit of production is 3 hours.The company's static budget was based on 50 000 units.Actual results for the year are as follows.What was Security Door's variable overhead spending variance?

A) $45 000 favourable

B) $60 000 favourable

C) $15 000 unfavourable

D) $45 000 unfavourable

A) $45 000 favourable

B) $60 000 favourable

C) $15 000 unfavourable

D) $45 000 unfavourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

37

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.What was the total amount of under/overapplied overhead for the firm?

A) $3550 under

B) $3550 over

C) $3550 debit

D) Both A and C

A) $3550 under

B) $3550 over

C) $3550 debit

D) Both A and C

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following statements is false?

A) An unfavourable variable overhead spending variance can result from paying a higher than expected price for variable overhead items.

B) A favourable variable overhead spending variance can result from using less of the variable overhead items than expected at the actual activity level.

C) An unfavourable variable overhead spending variance can result from producing fewer units than expected at the actual activity level.

D) The spending variance is the real control variance for variable overhead.

A) An unfavourable variable overhead spending variance can result from paying a higher than expected price for variable overhead items.

B) A favourable variable overhead spending variance can result from using less of the variable overhead items than expected at the actual activity level.

C) An unfavourable variable overhead spending variance can result from producing fewer units than expected at the actual activity level.

D) The spending variance is the real control variance for variable overhead.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

39

Carvelle Cabinets set the following standard cost per unit for 2008.The standards were set based on a capacity of 20 000 machine hours.During the year,5100 units were produced.What was Carvelle's variable overhead spending variance?

A) $7350 unfavourable

B) $2550 unfavourable

C) $4800 favourable

D) $7350 favourable

A) $7350 unfavourable

B) $2550 unfavourable

C) $4800 favourable

D) $7350 favourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

40

DBC Company applies fixed overhead at $8 per machine hour.During the year actual fixed overhead amounted to $75 000 and the standard machine hours allowed for units produced was 11 000.Budgeted fixed overhead was $80 000.Which of the following is the best description of the items used to calculate the volume variance?

Budgeted FOH

Applied FOH

Actual FOH

A) $80 000

$88 000

Ignore

B) $88 000

$88 000

Ignore

C) $88 000

$75 000

Ignore

D) ignore

$88 000

$75 000

Budgeted FOH

Applied FOH

Actual FOH

A) $80 000

$88 000

Ignore

B) $88 000

$88 000

Ignore

C) $88 000

$75 000

Ignore

D) ignore

$88 000

$75 000

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

41

Which of the following statements relating to standard costs is false?

A) Standard costs result in more stable product costs.

B) Standard costs enable management to concentrate on significant variances.

C) Standard costs provide a valid basis for cost comparisons.

D) Standard costs cannot be used for external reporting.

A) Standard costs result in more stable product costs.

B) Standard costs enable management to concentrate on significant variances.

C) Standard costs provide a valid basis for cost comparisons.

D) Standard costs cannot be used for external reporting.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following is not an advantage of standard costing?

A) Standard costing provides a basis for sensible cost comparisons.

B) Standard costing provides a means of performance evaluation.

C) Standard costing can be a motivational tool for employees.

D) Once standards have been set,they need not be revised,resulting in a more efficient accounting department.

A) Standard costing provides a basis for sensible cost comparisons.

B) Standard costing provides a means of performance evaluation.

C) Standard costing can be a motivational tool for employees.

D) Once standards have been set,they need not be revised,resulting in a more efficient accounting department.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

43

To which ledger account are the standard costs of direct material,direct labour and manufacturing overhead charged?

A) Not used at all

B) Used for variances only

C) Entered into work in process inventory

D) Entered into a standard control account

A) Not used at all

B) Used for variances only

C) Entered into work in process inventory

D) Entered into a standard control account

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

44

Master Products has the following information at the end of the year:

What is Master Product's sales price variance?

A) $3000 favourable

B) $7500 favourable

C) $7000 favourable

D) $10 000 unfavourable

What is Master Product's sales price variance?

A) $3000 favourable

B) $7500 favourable

C) $7000 favourable

D) $10 000 unfavourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following statements is false?

A) Standard costing systems do not indicate the causes of the variances.

B) Standard costing systems enable the production of timely performance reports.

C) Standard costing systems may create undesirable behaviour.

D) Standard costing systems tend to forget the importance of product quality and customer service.

A) Standard costing systems do not indicate the causes of the variances.

B) Standard costing systems enable the production of timely performance reports.

C) Standard costing systems may create undesirable behaviour.

D) Standard costing systems tend to forget the importance of product quality and customer service.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

46

Since variances are temporary accounts,how are they usually handled?

A) Closed directly to cost of goods sold at the end of each month.

B) Closed directly to cost of goods sold at the end of each accounting period.

C) Closed directly to cost of goods manufactured at the end of each accounting period.

D) Closed directly to profit and loss account at the end of the year.

A) Closed directly to cost of goods sold at the end of each month.

B) Closed directly to cost of goods sold at the end of each accounting period.

C) Closed directly to cost of goods manufactured at the end of each accounting period.

D) Closed directly to profit and loss account at the end of the year.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

47

Hamilton Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

The following were the actual results:

Calculate the total amount of underapplied or overapplied manufacturing overhead.

A) $80 000 underapplied

B) $64 000 underapplied

C) $50 000 overapplied

D) $24 000 underapplied

The following were the actual results:

Calculate the total amount of underapplied or overapplied manufacturing overhead.

A) $80 000 underapplied

B) $64 000 underapplied

C) $50 000 overapplied

D) $24 000 underapplied

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

48

Hamilton Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

The following were the actual results:

Calculate the amount of overhead cost applied to work in process inventory.

A) $1 520 000

B) $1 536 000

C) $1 550 000

D) $1 600 000

The following were the actual results:

Calculate the amount of overhead cost applied to work in process inventory.

A) $1 520 000

B) $1 536 000

C) $1 550 000

D) $1 600 000

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

49

Hamilton Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

The following were the actual results:

Calculate the fixed overhead volume variance.

A) $24 000 favourable

B) $24 000 unfavourable

C) $34 000 favourable

D) $10 000 unfavourable

The following were the actual results:

Calculate the fixed overhead volume variance.

A) $24 000 favourable

B) $24 000 unfavourable

C) $34 000 favourable

D) $10 000 unfavourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

50

Bozo Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

Calculate the total standard overhead rate per direct labour hour (variable and fixed).

A) $0.125

B) $4.06

C) $8.00

D) $8.20

Calculate the total standard overhead rate per direct labour hour (variable and fixed).

A) $0.125

B) $4.06

C) $8.00

D) $8.20

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

51

An overhead cost performance report is composed of the:

A) actual and budgeted costs for each overhead item

B) variable overhead spending and efficiency variances

C) fixed overhead budget variance along with actual and budgeted costs for each overhead item

D) variable overhead spending and efficiency variances,fixed overhead budget variance,and actual and budgeted costs for each overhead item

A) actual and budgeted costs for each overhead item

B) variable overhead spending and efficiency variances

C) fixed overhead budget variance along with actual and budgeted costs for each overhead item

D) variable overhead spending and efficiency variances,fixed overhead budget variance,and actual and budgeted costs for each overhead item

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

52

Master Products has the following information at the end of the year.What is Master Product's sales volume variance?

A) $10 000 unfavourable

B) $4000 unfavourable

C) $4400 favourable

D) $3000 unfavourable

A) $10 000 unfavourable

B) $4000 unfavourable

C) $4400 favourable

D) $3000 unfavourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

53

Framlingham uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

The following were the actual results:

Calculate the variable overhead spending variance.

A) $25 000 favourable

B) $50 000 favourable

C) $25 000 unfavourable

D) $10 000 unfavourable

The following were the actual results:

Calculate the variable overhead spending variance.

A) $25 000 favourable

B) $50 000 favourable

C) $25 000 unfavourable

D) $10 000 unfavourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following interpretations of an unfavourable fixed overhead volume variance is correct?

A) It measures the cost of underutilising productive capacity.

B) It is overapplied overhead.

C) It is similar to a favourable variable overhead efficiency variance.

D) It has no use for control purposes.

A) It measures the cost of underutilising productive capacity.

B) It is overapplied overhead.

C) It is similar to a favourable variable overhead efficiency variance.

D) It has no use for control purposes.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following criticisms of standard costing systems is false?

A) Variances concentrate on results rather than causes.

B) Standard costing systems concentrate on activities.

C) Standard costing systems place too much emphasis on direct labour costs and efficiency.

D) Standard costing systems are too narrowly defined.

A) Variances concentrate on results rather than causes.

B) Standard costing systems concentrate on activities.

C) Standard costing systems place too much emphasis on direct labour costs and efficiency.

D) Standard costing systems are too narrowly defined.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

56

Hamilton Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

The following were the actual results:

Calculate the amount of fixed overhead budget variance.

A) $10 000 favourable

B) $10 000 unfavourable

C) $24 000 favourable

D) $34 000 unfavourable

The following were the actual results:

Calculate the amount of fixed overhead budget variance.

A) $10 000 favourable

B) $10 000 unfavourable

C) $24 000 favourable

D) $34 000 unfavourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

57

Which of the following statements is true for a standard cost system?

A) Applied fixed manufacturing overhead is recorded as a debit to the manufacturing overhead account.

B) Overapplied fixed overhead is always debited to cost of goods sold.

C) Underapplied fixed overhead is always credited to finished goods inventory.

D) Applied fixed manufacturing overhead is recorded as a debit to the work in process inventory account.

A) Applied fixed manufacturing overhead is recorded as a debit to the manufacturing overhead account.

B) Overapplied fixed overhead is always debited to cost of goods sold.

C) Underapplied fixed overhead is always credited to finished goods inventory.

D) Applied fixed manufacturing overhead is recorded as a debit to the work in process inventory account.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

58

When is the predetermined fixed overhead rate used?

A) To apply fixed overhead to the cost of goods manufactured.

B) To apply fixed overhead to the work in process inventory account.

C) To apply fixed overhead to the cost of goods sold.

D) To prepare the budget.

A) To apply fixed overhead to the cost of goods manufactured.

B) To apply fixed overhead to the work in process inventory account.

C) To apply fixed overhead to the cost of goods sold.

D) To prepare the budget.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

59

Hamilton Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

The following were the actual results:

Calculate the amount of variable overhead spending variance.

A) $25 000 favourable

B) $15 000 unfavourable

C) $25 000 unfavourable

D) $15 000 favourable

The following were the actual results:

Calculate the amount of variable overhead spending variance.

A) $25 000 favourable

B) $15 000 unfavourable

C) $25 000 unfavourable

D) $15 000 favourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

60

Hamilton Pty Ltd uses a standard costing system for product costing.The company uses direct labour hours as the cost driver to apply overhead costs.The following amounts were budgeted for the year:

The following were the actual results:

Calculate the amount of variable overhead efficiency variance.

A) $25 000 favourable

B) $25 000 unfavourable

C) $15 000 favourable

D) $15 000 unfavourable

The following were the actual results:

Calculate the amount of variable overhead efficiency variance.

A) $25 000 favourable

B) $25 000 unfavourable

C) $15 000 favourable

D) $15 000 unfavourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

61

The sales price variance equals:

A) (actual sales price - budgeted sales price)× budgeted sales volume

B) (actual sales price - budgeted sales price)× actual contribution margin

C) (actual sales price - budgeted sales price)× actual sales volume

D) (actual sales volume - budgeted sales volume)× budgeted contribution margin

A) (actual sales price - budgeted sales price)× budgeted sales volume

B) (actual sales price - budgeted sales price)× actual contribution margin

C) (actual sales price - budgeted sales price)× actual sales volume

D) (actual sales volume - budgeted sales volume)× budgeted contribution margin

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

62

A particular company incurs actual overhead of $10 per unit produced.The company's budgeted (standard)overhead cost per unit produced is $9 per unit.Overhead is applied based on machine hours.If the company's actual machine hours worked was 1000,and standard hours allowed for units produced in the period was 1100 hours,what amount would be debited to work in process for overhead if the company used actual costing,normal costing and standard costing respectively?

A) $11 000;$9 900;$9 000

B) $11 000;$9 000;$9 900

C) $10 000;$9 900;$9 000

D) $10 000;$9 000;$9 900

A) $11 000;$9 900;$9 000

B) $11 000;$9 000;$9 900

C) $10 000;$9 900;$9 000

D) $10 000;$9 000;$9 900

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

63

A favourable overhead efficiency variance is the result of:

A) actual outputs exceeding actual inputs within the framework of a flexible budget

B) standard outputs allowed for actual inputs exceeding the flexible budget inputs

C) the flexible budget for actual input exceeding the actual costs incurred

D) standard inputs allowed for actual outputs achieved exceeding the actual inputs within the framework of a flexible budget

A) actual outputs exceeding actual inputs within the framework of a flexible budget

B) standard outputs allowed for actual inputs exceeding the flexible budget inputs

C) the flexible budget for actual input exceeding the actual costs incurred

D) standard inputs allowed for actual outputs achieved exceeding the actual inputs within the framework of a flexible budget

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

64

The following table provides information about a company's production.If variable costs increased in 2005 by 10 per cent and fixed overheads increased in 2006 by 20 per cent,what was the variable cost per unit in 2004?

A) $3.35

B) $3.40

C) $3.45

D) $3.50

A) $3.35

B) $3.40

C) $3.45

D) $3.50

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

65

The sales volume variance equals:

A) (actual sales volume - budgeted sales volume)× actual sales price

B) (actual sales volume - budgeted sales volume)× actual contribution margin

C) (actual sales volume - budgeted sales volume)× budgeted contribution margin

D) (actual sales price - budgeted sales price)× budgeted sales volume

A) (actual sales volume - budgeted sales volume)× actual sales price

B) (actual sales volume - budgeted sales volume)× actual contribution margin

C) (actual sales volume - budgeted sales volume)× budgeted contribution margin

D) (actual sales price - budgeted sales price)× budgeted sales volume

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

66

Z Company uses a variable costing system.There was no opening or closing stock.The following data is available:

Use this data to determine Z's sales volume variance:

A) $8000 unfavourable

B) $18 000 unfavourable

C) $60 000 unfavourable

D) $18 000 favourable

Use this data to determine Z's sales volume variance:

A) $8000 unfavourable

B) $18 000 unfavourable

C) $60 000 unfavourable

D) $18 000 favourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

67

Z Company uses a variable costing system.There was no opening or closing stock.The following data is available.Use this data to determine Z's sales price variance.

A) $2000 favourable

B) $10 000 unfavourable

C) $58 000 unfavourable

D) $10 000 favourable

A) $2000 favourable

B) $10 000 unfavourable

C) $58 000 unfavourable

D) $10 000 favourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following statements is correct?

A) A flexible budget is calculated for actual activity level only.

B) A static budget can be calculated for a number of activity levels.

C) A static budget is prepared for budgeted activity level only.

D) Both A and C

A) A flexible budget is calculated for actual activity level only.

B) A static budget can be calculated for a number of activity levels.

C) A static budget is prepared for budgeted activity level only.

D) Both A and C

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

69

Universal Pty Ltd used a standard cost system to prepare the following budget at normal operating capacity for the month of January 2007.Actual data for January 2007 were as follows:

Using the two-way analysis of overhead variances,what is the total of the fixed budget variance and the variable overhead spending variance for January 2007?

A) $3000 favourable

B) $5000 favourable

C) $9000 favourable

D) $3000 unfavourable

Using the two-way analysis of overhead variances,what is the total of the fixed budget variance and the variable overhead spending variance for January 2007?

A) $3000 favourable

B) $5000 favourable

C) $9000 favourable

D) $3000 unfavourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

70

Which of the following statements is correct?

A) Budgeted hours and standard hours are always the same.

B) Budgeted hours and standard hours are never the same.

C) Budgeted hours and standard hours will be the same when budgeted production equals actual production.

D) Budgeted hours and standard hours are both related to budgeted production levels.

A) Budgeted hours and standard hours are always the same.

B) Budgeted hours and standard hours are never the same.

C) Budgeted hours and standard hours will be the same when budgeted production equals actual production.

D) Budgeted hours and standard hours are both related to budgeted production levels.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

71

The following table provides information about a company's production.If variable costs increased in 2005 by 10 per cent and fixed overheads increased in 2006 by 20 per cent,what was the estimated total cost in 2006?

A) $447 600

B) $472 800

C) $504 200

D) More than $514 400

A) $447 600

B) $472 800

C) $504 200

D) More than $514 400

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following is not a limitation of standard costing system?

A) Standard costing system takes a process perspective rather than a departmental perspective.

B) Standard costing system becomes outdated easily.

C) Standard costing systems do not encourage continuous improvement

D) Standard costing system focuses on the consequences rather than the causes of variances.

A) Standard costing system takes a process perspective rather than a departmental perspective.

B) Standard costing system becomes outdated easily.

C) Standard costing systems do not encourage continuous improvement

D) Standard costing system focuses on the consequences rather than the causes of variances.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

73

When using activity-based costing,we recognise four types of activity costs: unit level,batch level,product level and facility level.Under activity-based budgeting,which of the following types of cost would be 'flexed'?

A) Product level

B) Batch level

C) Unit level

D) All of the given answers

A) Product level

B) Batch level

C) Unit level

D) All of the given answers

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

74

Which of the following statements about activity-based budgeting (ABB)is incorrect?

A) ABB is based on the estimated cost of activities,while conventional budgeting is based on estimated costs of line items.

B) ABB starts with estimating the costs of resources,while conventional costing starts with estimating sales.

C) ABB is generally a more accurate planning tool than conventional budgeting.

D) ABB focuses on resource consumption rather than resource acquisition.

A) ABB is based on the estimated cost of activities,while conventional budgeting is based on estimated costs of line items.

B) ABB starts with estimating the costs of resources,while conventional costing starts with estimating sales.

C) ABB is generally a more accurate planning tool than conventional budgeting.

D) ABB focuses on resource consumption rather than resource acquisition.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

75

Use the following data to determine the company's variable overhead spending variance for March.

A) $500 favourable

B) $500 unfavourable

C) $4 500 favourable

D) $4 500 unfavourable

A) $500 favourable

B) $500 unfavourable

C) $4 500 favourable

D) $4 500 unfavourable

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

76

Adams Corporation has developed the following flexible budget formula for annual indirect labour cost: Total cost = $4800 + 50c per machine hour.Operating budgets for the current month are based on 20 000 hours of planned machine time.Calculate the amount of indirect labour costs included in this planning budget.

A) $7200

B) $10 000

C) $14 400

D) None of the given answers

A) $7200

B) $10 000

C) $14 400

D) None of the given answers

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

77

Use the following data to determine the company's fixed overhead volume variance for March.

A) $10 000 overapplied

B) $10 000 underapplied

C) $20 000 overapplied

D) $20 000 underapplied

A) $10 000 overapplied

B) $10 000 underapplied

C) $20 000 overapplied

D) $20 000 underapplied

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

78

Which of the following statements is incorrect?

A) The company's fixed overhead costs can be expressed as a flexible budget formula.

B) The company's variable costs can be expressed as a flexible budget formula.

C) The company's total production costs can be expressed as a flexible budget formula.

D) A cost must have a fixed and a variable component before it can be expressed as a flexible budget formula.

A) The company's fixed overhead costs can be expressed as a flexible budget formula.

B) The company's variable costs can be expressed as a flexible budget formula.

C) The company's total production costs can be expressed as a flexible budget formula.

D) A cost must have a fixed and a variable component before it can be expressed as a flexible budget formula.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

79

The budgeted costs per unit for a company are fixed costs $2 per unit;variable costs $3 per unit.What is the expected cost of producing 1005 units?

A) $2013

B) $5025

C) $3017

D) Insufficient information to determine

A) $2013

B) $5025

C) $3017

D) Insufficient information to determine

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

80

Felter Company uses a standard costing system based on direct labour hours.Last month,Felter Company used more electricity and indirect materials than planned.This is likely to result in:

A) Unfavourable variable overhead efficiency variance.

B) Unfavourable variable overhead efficiency variance and unfavourable variable overhead spending variance.

C) Unfavourable variable overhead efficiency variance and unfavourable fixed overhead variance.

D) Unfavourable variable overhead spending variance.

A) Unfavourable variable overhead efficiency variance.

B) Unfavourable variable overhead efficiency variance and unfavourable variable overhead spending variance.

C) Unfavourable variable overhead efficiency variance and unfavourable fixed overhead variance.

D) Unfavourable variable overhead spending variance.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 97 flashcards in this deck.