Deck 9: The Rise and Fall of Industries

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

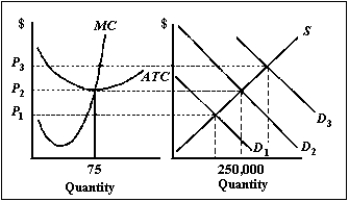

Exhibit 9-1

Refer to Exhibit 9-1. If the market demand curve is D3, what happens over time?

A) Some existing firms increase capital input.

B) Firm exit occurs.

C) Some existing firms decrease labor input.

D) Market price decreases.

E) Most firms do nothing.

Refer to Exhibit 9-1. If the market demand curve is D3, what happens over time?

A) Some existing firms increase capital input.

B) Firm exit occurs.

C) Some existing firms decrease labor input.

D) Market price decreases.

E) Most firms do nothing.

Question

Exhibit 9-1

Refer to Exhibit 9-1. If all firms are identical, the equilibrium number of firms in the industry is

A) 125,000.

B) 3,333.

C) 2,500.

D) 3,000.

E) 250,000.

Refer to Exhibit 9-1. If all firms are identical, the equilibrium number of firms in the industry is

A) 125,000.

B) 3,333.

C) 2,500.

D) 3,000.

E) 250,000.

Question

Exhibit 9-1

Refer to Exhibit 9-1. When does firm entry occur?

A) When demand is at D3

B) When demand is at D1

C) When demand is at D2

D) When price is P1 or greater

E) When price is P2 or less

Refer to Exhibit 9-1. When does firm entry occur?

A) When demand is at D3

B) When demand is at D1

C) When demand is at D2

D) When price is P1 or greater

E) When price is P2 or less

Question

Question

Question

Exhibit 9-1

Refer to Exhibit 9-1. Which of the following describes a long-run competitive equilibrium?

A) When market demand is at D2, each firm produces more than 75 units.

B) When market demand is at D2, each firm produces 75 units.

C) When market demand is at D2, each firm produces fewer than 75 units.

D) When market demand is at D2, each firm produces 250,000 units.

E) When price is P2, each firm produces 250,000 units.

Refer to Exhibit 9-1. Which of the following describes a long-run competitive equilibrium?

A) When market demand is at D2, each firm produces more than 75 units.

B) When market demand is at D2, each firm produces 75 units.

C) When market demand is at D2, each firm produces fewer than 75 units.

D) When market demand is at D2, each firm produces 250,000 units.

E) When price is P2, each firm produces 250,000 units.

Question

Question

Question

Question

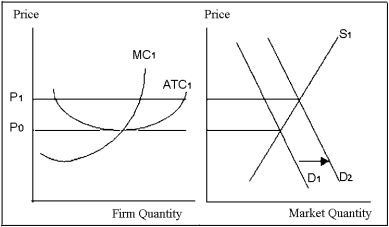

Exhibit 9-2

Refer to Exhibit 9-2. If the demand curve shifts from D1 to D2, then

A) some firms enter the industry.

B) some firms exit the industry.

C) the number of firms does not change.

D) firms earn a normal profit.

E) most firms earn a loss.

Refer to Exhibit 9-2. If the demand curve shifts from D1 to D2, then

A) some firms enter the industry.

B) some firms exit the industry.

C) the number of firms does not change.

D) firms earn a normal profit.

E) most firms earn a loss.

Question

Question

Question

Exhibit 9-1

Refer to Exhibit 9-1. Which demand curve results in normal profits?

A) D1

B) D2

C) D3

D) Both D1 and D2

E) Both D2 and D3

Refer to Exhibit 9-1. Which demand curve results in normal profits?

A) D1

B) D2

C) D3

D) Both D1 and D2

E) Both D2 and D3

Question

Question

Question

Exhibit 9-1

Refer to Exhibit 9-1. Which demand curve results in economic losses?

A) D1

B) D2

C) D3

D) Both D1 and D2

E) Both D2 and D3

Refer to Exhibit 9-1. Which demand curve results in economic losses?

A) D1

B) D2

C) D3

D) Both D1 and D2

E) Both D2 and D3

Question

Exhibit 9-1

Refer to Exhibit 9-1. If the market demand curve is D1, what happens in the long run?

A) Firm entry occurs.

B) Firm exit occurs.

C) Some firms increase capital input.

D) Some firms increase labor input.

E) Most firms do nothing.

Refer to Exhibit 9-1. If the market demand curve is D1, what happens in the long run?

A) Firm entry occurs.

B) Firm exit occurs.

C) Some firms increase capital input.

D) Some firms increase labor input.

E) Most firms do nothing.

Question

Exhibit 9-2

Refer to Exhibit 9-2. If the market demand curve is D1, then the firm earns normal profit.

Refer to Exhibit 9-2. If the market demand curve is D1, then the firm earns normal profit.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/139

Play

Full screen (f)

Deck 9: The Rise and Fall of Industries

1

Three reasons for the rise and fall of industries are

A) government subsidy, cost-reducing technology, and changing tastes.

B) new ideas, cost-reducing technology, and changing tastes.

C) government subsidy, population growth, and cost-reducing technology.

D) population growth, cost-reducing technology, and changing tastes.

E) new ideas, necessity, and changing tastes.

A) government subsidy, cost-reducing technology, and changing tastes.

B) new ideas, cost-reducing technology, and changing tastes.

C) government subsidy, population growth, and cost-reducing technology.

D) population growth, cost-reducing technology, and changing tastes.

E) new ideas, necessity, and changing tastes.

new ideas, cost-reducing technology, and changing tastes.

2

An industry is

A) a group of firms that produce similar products.

B) a collection of production facilities.

C) a group of consumers who wish to purchase similar products.

D) supply and demand for a product.

E) a union of workers from different firms.

A) a group of firms that produce similar products.

B) a collection of production facilities.

C) a group of consumers who wish to purchase similar products.

D) supply and demand for a product.

E) a union of workers from different firms.

a group of firms that produce similar products.

3

Define the term industry.

An industry is a group of firms that produce similar products.

4

The long-run competitive equilibrium model can be used to predict the number of firms in an industry given a certain level of market demand.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

5

In economics, firms can enter an industry in the short run.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

6

The number of firms increases in the long run when the industry realizes profits.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

7

A group of firms, each of which produces similar products, is called a(n)

A) market.

B) trust.

C) conglomerate.

D) industry.

E) production group.

A) market.

B) trust.

C) conglomerate.

D) industry.

E) production group.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

8

The entry and exit of firms occurs in the long run.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

9

The definition of a market is broader than that of an industry.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

10

One reason old industries die off is that entrepreneurs create new industries that replace the old ones.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

11

In a competitive industry, firm demand is

A) downward-sloping.

B) vertical.

C) nonexistent.

D) horizontal.

E) unchanging.

A) downward-sloping.

B) vertical.

C) nonexistent.

D) horizontal.

E) unchanging.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

12

An industry tends to expand as market demand increases.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

13

The long-run competitive equilibrium model describes what happens to an industry after

A) all existing firms disappear.

B) only one firm survives.

C) the government intervenes.

D) the entry and exit of firms over time.

E) the market no longer exists.

A) all existing firms disappear.

B) only one firm survives.

C) the government intervenes.

D) the entry and exit of firms over time.

E) the market no longer exists.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following statements is false?

A) The long-run equilibrium model takes into account the entry and exit of firms.

B) The long-run equilibrium model is an attempt to explain the behavior of industries.

C) Firms enter an industry when economic profits are positive.

D) The long-run equilibrium model can be applied only to U.S. industries.

E) Firms exit an industry in the long run when economic profits are negative.

A) The long-run equilibrium model takes into account the entry and exit of firms.

B) The long-run equilibrium model is an attempt to explain the behavior of industries.

C) Firms enter an industry when economic profits are positive.

D) The long-run equilibrium model can be applied only to U.S. industries.

E) Firms exit an industry in the long run when economic profits are negative.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

15

Firms may enter or exit a competitive industry

A) in the short run.

B) in the long run.

C) in either the short run or the long run.

D) only when they are no longer price-takers.

E) immediately after they begin operation.

A) in the short run.

B) in the long run.

C) in either the short run or the long run.

D) only when they are no longer price-takers.

E) immediately after they begin operation.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is a condition of long-run competitive equilibrium?

A) There are incentives for firms to enter the industry.

B) There are incentives for firms to exit the industry.

C) There is no incentive for firms to enter or exit the industry.

D) There are incentives for firms to produce more output.

E) There are incentives for firms to change plant size.

A) There are incentives for firms to enter the industry.

B) There are incentives for firms to exit the industry.

C) There is no incentive for firms to enter or exit the industry.

D) There are incentives for firms to produce more output.

E) There are incentives for firms to change plant size.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

17

List three reasons for the rise and fall of industries.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

18

In the long run, firms enter an industry when

A) firms in the industry realize positive economic profits.

B) firms in the industry realize economic losses.

C) other firms exit the industry.

D) economic profits in the industry are zero.

E) firms in the industry become price-makers.

A) firms in the industry realize positive economic profits.

B) firms in the industry realize economic losses.

C) other firms exit the industry.

D) economic profits in the industry are zero.

E) firms in the industry become price-makers.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

19

In the long run, if price is greater than average total cost in an industry, then

A) some firms leave the industry.

B) some firms are attracted to the industry.

C) all firms leave the industry.

D) there is no incentive for any firm to enter or leave the industry.

E) the industry disappears.

A) some firms leave the industry.

B) some firms are attracted to the industry.

C) all firms leave the industry.

D) there is no incentive for any firm to enter or leave the industry.

E) the industry disappears.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

20

Consumers are part of an industry.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

21

If the government subsidizes the production of wind energy, then the industry produces

A) more energy in the short run and firm entry occurs in the long run.

B) more energy in the short run and firm exit occurs in the long run.

C) less energy in the short run and firm entry occurs in the long run.

D) less energy in the short run and firm exit occurs in the long run.

E) the same amount of energy in both the short run and long run.

A) more energy in the short run and firm entry occurs in the long run.

B) more energy in the short run and firm exit occurs in the long run.

C) less energy in the short run and firm entry occurs in the long run.

D) less energy in the short run and firm exit occurs in the long run.

E) the same amount of energy in both the short run and long run.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

22

Firm demand in a competitive industry, like market demand, is downward-sloping.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following does not need to be true for long-run equilibrium to be attained?

A) Constant returns to scale are reached.

B) The latest in technology is utilized.

C) Profit is being maximized.

D) There is no incentive to enter or exit the industry.

E) Economic profits equal zero.

A) Constant returns to scale are reached.

B) The latest in technology is utilized.

C) Profit is being maximized.

D) There is no incentive to enter or exit the industry.

E) Economic profits equal zero.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

24

If higher taxes raise the unit cost of a competitive industry, then in the long run, industry supply

A) and market price decrease.

B) decreases and market price increases.

C) increases and market price decreases.

D) and market price increase.

E) and market price remain constant.

A) and market price decrease.

B) decreases and market price increases.

C) increases and market price decreases.

D) and market price increase.

E) and market price remain constant.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

25

If higher taxes raise the unit cost of a competitive industry, then producers

A) decrease production in the short run and the number of producers decreases in the long run.

B) decrease production in the short run and the number of producers increases in the long run.

C) increase production in the short run and the number of producers decreases in the long run.

D) increase production in the short run and the number of producers increases in the long run.

E) keep production constant in the short run and the number of producers remains the same in the long run.

A) decrease production in the short run and the number of producers decreases in the long run.

B) decrease production in the short run and the number of producers increases in the long run.

C) increase production in the short run and the number of producers decreases in the long run.

D) increase production in the short run and the number of producers increases in the long run.

E) keep production constant in the short run and the number of producers remains the same in the long run.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

26

If zero economic profit is being earned in a competitive industry,

A) firms leave the industry.

B) firms permanently shut down.

C) firms enter the industry.

D) no firms enter or leave the industry.

E) firms temporarily shut down.

A) firms leave the industry.

B) firms permanently shut down.

C) firms enter the industry.

D) no firms enter or leave the industry.

E) firms temporarily shut down.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

27

By definition, when market supply (the sum of firms' marginal cost curves) equals market demand, long-run equilibrium is achieved.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

28

Free entry and exit refers to industries with very low start-up costs.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

29

When firms exit an industry,

A) firm profits typically fall.

B) market supply decreases, pushing market price higher.

C) market supply decreases, decreasing the firm's output price.

D) demand decreases and economic profits continue to decline.

E) market supply decreases, increasing price and bringing firms back into the industry.

A) firm profits typically fall.

B) market supply decreases, pushing market price higher.

C) market supply decreases, decreasing the firm's output price.

D) demand decreases and economic profits continue to decline.

E) market supply decreases, increasing price and bringing firms back into the industry.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following is true in a long-run competitive equilibrium?

A) Price is greater than average total cost.

B) Profits are greater than zero.

C) Marginal cost is greater than average total cost.

D) Market supply is greater than market demand.

E) There is no incentive to enter or exit the industry.

A) Price is greater than average total cost.

B) Profits are greater than zero.

C) Marginal cost is greater than average total cost.

D) Market supply is greater than market demand.

E) There is no incentive to enter or exit the industry.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

31

If an innovation lowers the marginal cost of production for firms in a competitive industry, then in the long run, the number of firms

A) increases and firms in the industry make normal profits.

B) does not change and firms in the industry make profits.

C) decreases and firms in the industry incur losses.

D) decreases and firms in the industry make profits.

E) decreases and firms in the industry make normal profits.

A) increases and firms in the industry make normal profits.

B) does not change and firms in the industry make profits.

C) decreases and firms in the industry incur losses.

D) decreases and firms in the industry make profits.

E) decreases and firms in the industry make normal profits.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

32

When economic profits equal zero for firms in an industry, there is no entry or exit.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

33

Free entry and exit means that

A) banks charge no interest on a loan to start a firm.

B) there are no artificial barriers to entering and exiting an industry.

C) no investment is necessary in order to enter an industry.

D) it costs nothing to start a firm.

E) a firm is free to enter and exit a nation without having to pay high tax levies.

A) banks charge no interest on a loan to start a firm.

B) there are no artificial barriers to entering and exiting an industry.

C) no investment is necessary in order to enter an industry.

D) it costs nothing to start a firm.

E) a firm is free to enter and exit a nation without having to pay high tax levies.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

34

If, at the equilibrium level of output, a typical competitive firm's price is greater than its ATC, the firm

A) should raise the price.

B) should lower the price.

C) should decrease output.

D) finds that new firms are attracted to this industry.

E) should increase output.

A) should raise the price.

B) should lower the price.

C) should decrease output.

D) finds that new firms are attracted to this industry.

E) should increase output.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

35

The market demand curve in a competitive market is

A) vertical.

B) downward-sloping.

C) horizontal.

D) unit elastic.

E) perfectly elastic.

A) vertical.

B) downward-sloping.

C) horizontal.

D) unit elastic.

E) perfectly elastic.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

36

When firms enter an industry, market supply

A) and firm demand both decrease.

B) increases and firm demand does not change.

C) and firm supply both decrease.

D) and firm demand both increase.

E) increases and firm demand shifts down.

A) and firm demand both decrease.

B) increases and firm demand does not change.

C) and firm supply both decrease.

D) and firm demand both increase.

E) increases and firm demand shifts down.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

37

If the typical firm in an industry is experiencing economies of scale,

A) short-run equilibrium cannot exist.

B) some firms exit the industry.

C) industry expansion occurs.

D) long-run equilibrium is achieved.

E) firms need to divest and become smaller.

A) short-run equilibrium cannot exist.

B) some firms exit the industry.

C) industry expansion occurs.

D) long-run equilibrium is achieved.

E) firms need to divest and become smaller.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

38

A firm in a long-run equilibrium state

A) produces at the minimum of average variable cost.

B) produces at the minimum of marginal cost.

C) suffers accounting profit losses.

D) enjoys economies of scale.

E) makes no economic profit.

A) produces at the minimum of average variable cost.

B) produces at the minimum of marginal cost.

C) suffers accounting profit losses.

D) enjoys economies of scale.

E) makes no economic profit.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

39

In a competitive market, the presence of short-run economic profits would, in the long run, cause economic profits to

A) disappear because market costs increase.

B) disappear because firms are able to take advantage of economies of scale.

C) continue.

D) decline but be larger than zero.

E) disappear because the market supply curve has shifted to the right.

A) disappear because market costs increase.

B) disappear because firms are able to take advantage of economies of scale.

C) continue.

D) decline but be larger than zero.

E) disappear because the market supply curve has shifted to the right.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

40

In long-run competitive equilibrium, market price equals a firm's average total cost.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

41

An increase in market demand can be shown by shifting a firm's demand curve to the right.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

42

Exhibit 9-1

Refer to Exhibit 9-1. If the market demand curve is D3, what happens over time?

A) Some existing firms increase capital input.

B) Firm exit occurs.

C) Some existing firms decrease labor input.

D) Market price decreases.

E) Most firms do nothing.

Refer to Exhibit 9-1. If the market demand curve is D3, what happens over time?

A) Some existing firms increase capital input.

B) Firm exit occurs.

C) Some existing firms decrease labor input.

D) Market price decreases.

E) Most firms do nothing.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

43

Exhibit 9-1

Refer to Exhibit 9-1. If all firms are identical, the equilibrium number of firms in the industry is

A) 125,000.

B) 3,333.

C) 2,500.

D) 3,000.

E) 250,000.

Refer to Exhibit 9-1. If all firms are identical, the equilibrium number of firms in the industry is

A) 125,000.

B) 3,333.

C) 2,500.

D) 3,000.

E) 250,000.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

44

Exhibit 9-1

Refer to Exhibit 9-1. When does firm entry occur?

A) When demand is at D3

B) When demand is at D1

C) When demand is at D2

D) When price is P1 or greater

E) When price is P2 or less

Refer to Exhibit 9-1. When does firm entry occur?

A) When demand is at D3

B) When demand is at D1

C) When demand is at D2

D) When price is P1 or greater

E) When price is P2 or less

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

45

If market demand increases, a competitive firm sees

A) its cost curves shift up.

B) its profit-maximizing output level increase.

C) its marginal cost fall.

D) its profits decrease.

E) the demand curve facing the firm shift down.

A) its cost curves shift up.

B) its profit-maximizing output level increase.

C) its marginal cost fall.

D) its profits decrease.

E) the demand curve facing the firm shift down.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

46

Suppose that a competitive market is initially in long-run equilibrium. Which of the following are the most likely results of an increase in market demand?

A) Existing firms will produce less and some firms will exit the market so that the market supply curve will shift to the left.

B) Some existing firms will produce more while some other firms will exit the market so that the market supply curve will remain the same.

C) Existing firms will produce more and new firms will enter the market so that the market supply curve will shift to the right.

D) Existing firms will produce less while new firms will enter the market so that the effect on the market supply curve is uncertain.

E) Nothing will change in the market.

A) Existing firms will produce less and some firms will exit the market so that the market supply curve will shift to the left.

B) Some existing firms will produce more while some other firms will exit the market so that the market supply curve will remain the same.

C) Existing firms will produce more and new firms will enter the market so that the market supply curve will shift to the right.

D) Existing firms will produce less while new firms will enter the market so that the effect on the market supply curve is uncertain.

E) Nothing will change in the market.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

47

Exhibit 9-1

Refer to Exhibit 9-1. Which of the following describes a long-run competitive equilibrium?

A) When market demand is at D2, each firm produces more than 75 units.

B) When market demand is at D2, each firm produces 75 units.

C) When market demand is at D2, each firm produces fewer than 75 units.

D) When market demand is at D2, each firm produces 250,000 units.

E) When price is P2, each firm produces 250,000 units.

Refer to Exhibit 9-1. Which of the following describes a long-run competitive equilibrium?

A) When market demand is at D2, each firm produces more than 75 units.

B) When market demand is at D2, each firm produces 75 units.

C) When market demand is at D2, each firm produces fewer than 75 units.

D) When market demand is at D2, each firm produces 250,000 units.

E) When price is P2, each firm produces 250,000 units.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

48

Suppose a mechanic uses $150,000 of his own money to start a business. The rate of interest he could earn in a savings account is 5 percent, and the rate of interest he could earn by investing in bonds is 8 percent. What is the opportunity cost of capital when the mechanic uses his money to start his own business?

A) $8,000/year

B) $7,500/year

C) $150,000

D) $12,000/year

E) $19,500/year

A) $8,000/year

B) $7,500/year

C) $150,000

D) $12,000/year

E) $19,500/year

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

49

When economic profit is equal to zero, we say that

A) implicit costs equal zero.

B) a normal profit is being earned.

C) total cost is greater than total revenue.

D) accounting profit is negative.

E) the business is not profitable.

A) implicit costs equal zero.

B) a normal profit is being earned.

C) total cost is greater than total revenue.

D) accounting profit is negative.

E) the business is not profitable.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

50

In the long run, market supply increases as market demand increases.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

51

Exhibit 9-2

Refer to Exhibit 9-2. If the demand curve shifts from D1 to D2, then

A) some firms enter the industry.

B) some firms exit the industry.

C) the number of firms does not change.

D) firms earn a normal profit.

E) most firms earn a loss.

Refer to Exhibit 9-2. If the demand curve shifts from D1 to D2, then

A) some firms enter the industry.

B) some firms exit the industry.

C) the number of firms does not change.

D) firms earn a normal profit.

E) most firms earn a loss.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

52

A normal profit may be defined as

A) the minimum amount of profit required to keep a business operating in the long run.

B) an accounting profit equal to the sum of all opportunity costs.

C) the maximum amount of profit that a business has ever made.

D) economic profit that is equal to accounting profit.

E) accounting profit equal to zero.

A) the minimum amount of profit required to keep a business operating in the long run.

B) an accounting profit equal to the sum of all opportunity costs.

C) the maximum amount of profit that a business has ever made.

D) economic profit that is equal to accounting profit.

E) accounting profit equal to zero.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

53

Suppose a dentist has total revenue of $320,000, and his total costs are $250,000 for the year. Also suppose the dentist left a job paying $112,000 a year to start his own practice. What is the dentist's economic profit?

A) $182,000

B) -$42,000

C) -$28,000

D) $112,000

E) $70,000

A) $182,000

B) -$42,000

C) -$28,000

D) $112,000

E) $70,000

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

54

Exhibit 9-1

Refer to Exhibit 9-1. Which demand curve results in normal profits?

A) D1

B) D2

C) D3

D) Both D1 and D2

E) Both D2 and D3

Refer to Exhibit 9-1. Which demand curve results in normal profits?

A) D1

B) D2

C) D3

D) Both D1 and D2

E) Both D2 and D3

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

55

The difference between accounting profit and economic profit is

A) total costs.

B) implicit costs.

C) total opportunity costs.

D) normal profits.

E) marginal cost.

A) total costs.

B) implicit costs.

C) total opportunity costs.

D) normal profits.

E) marginal cost.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

56

When market demand increases in a competitive industry,

A) the number of firms increases, causing short-run market supply to increase.

B) firms become less efficient.

C) firms' marginal cost curves shift to the right.

D) economic profits stay at zero because of competition.

E) market price increases, making it possible for ATC curves to shift up.

A) the number of firms increases, causing short-run market supply to increase.

B) firms become less efficient.

C) firms' marginal cost curves shift to the right.

D) economic profits stay at zero because of competition.

E) market price increases, making it possible for ATC curves to shift up.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

57

Exhibit 9-1

Refer to Exhibit 9-1. Which demand curve results in economic losses?

A) D1

B) D2

C) D3

D) Both D1 and D2

E) Both D2 and D3

Refer to Exhibit 9-1. Which demand curve results in economic losses?

A) D1

B) D2

C) D3

D) Both D1 and D2

E) Both D2 and D3

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

58

Exhibit 9-1

Refer to Exhibit 9-1. If the market demand curve is D1, what happens in the long run?

A) Firm entry occurs.

B) Firm exit occurs.

C) Some firms increase capital input.

D) Some firms increase labor input.

E) Most firms do nothing.

Refer to Exhibit 9-1. If the market demand curve is D1, what happens in the long run?

A) Firm entry occurs.

B) Firm exit occurs.

C) Some firms increase capital input.

D) Some firms increase labor input.

E) Most firms do nothing.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

59

Exhibit 9-2

Refer to Exhibit 9-2. If the market demand curve is D1, then the firm earns normal profit.

Refer to Exhibit 9-2. If the market demand curve is D1, then the firm earns normal profit.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

60

Suppose a dentist has total revenue of $320,000, and his total costs are $250,000 for the year. Also suppose the dentist left a job paying $112,000 a year to start his own practice. What is the dentist's accounting profit?

A) -$28,000

B) -$42,000

C) $182,000

D) $70,000

E) $112,000

A) -$28,000

B) -$42,000

C) $182,000

D) $70,000

E) $112,000

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

61

When firms leave an industry,

A) it is due to long-term losses.

B) other firms immediately enter to take their place.

C) it is because they anticipate an increase in demand.

D) other firms enter.

E) it is always due to a decrease in demand.

A) it is due to long-term losses.

B) other firms immediately enter to take their place.

C) it is because they anticipate an increase in demand.

D) other firms enter.

E) it is always due to a decrease in demand.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

62

As firms enter a competitive industry,

A) both market demand and industry output increase.

B) industry economic profits increase.

C) output price falls and individual firms increase output.

D) output price falls and cost curves shift down.

E) output price falls and industry output increases.

A) both market demand and industry output increase.

B) industry economic profits increase.

C) output price falls and individual firms increase output.

D) output price falls and cost curves shift down.

E) output price falls and industry output increases.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

63

Suppose that a competitive market is initially in long-run equilibrium. Which of the following are the most likely results of a decrease in market demand?

A) Some existing firms will produce more while some other firms will exit the market so that the market supply curve will remain the same.

B) Existing firms will produce less and some firms will exit the market so that the market supply curve will shift to the left.

C) Existing firms will produce more and new firms will enter the market so that the market supply curve will shift to the right.

D) Existing firms will produce less while new firms will enter the market so that the effect on the market supply curve is uncertain.

E) Nothing will change in the market.

A) Some existing firms will produce more while some other firms will exit the market so that the market supply curve will remain the same.

B) Existing firms will produce less and some firms will exit the market so that the market supply curve will shift to the left.

C) Existing firms will produce more and new firms will enter the market so that the market supply curve will shift to the right.

D) Existing firms will produce less while new firms will enter the market so that the effect on the market supply curve is uncertain.

E) Nothing will change in the market.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

64

Firms leave a competitive industry in the long run when

A) price is less than the minimum of marginal cost.

B) price is less than the minimum of average variable cost.

C) the return on investment is less than 10 percent.

D) price is less than the minimum of average total cost.

E) price is equal to the minimum of average total cost.

A) price is less than the minimum of marginal cost.

B) price is less than the minimum of average variable cost.

C) the return on investment is less than 10 percent.

D) price is less than the minimum of average total cost.

E) price is equal to the minimum of average total cost.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

65

Which of the following statements is false?

A) Given the nature of cost curves, positive economic profits can only induce entry of new firms.

B) Entry and expansion can occur at the same time in the same industry.

C) When positive economic profits prevail in an industry, firms often expand.

D) When economic profits are negative, firms might leave an industry.

E) An industry ceases to either expand or contract when economic profits are zero.

A) Given the nature of cost curves, positive economic profits can only induce entry of new firms.

B) Entry and expansion can occur at the same time in the same industry.

C) When positive economic profits prevail in an industry, firms often expand.

D) When economic profits are negative, firms might leave an industry.

E) An industry ceases to either expand or contract when economic profits are zero.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

66

In a competitive industry, which of the following cannot be true for a firm in the long run?

A) Price equals marginal cost.

B) Profits are maximized.

C) The firm takes market price as given.

D) Economic profits equal zero.

E) Price equals average variable cost.

A) Price equals marginal cost.

B) Profits are maximized.

C) The firm takes market price as given.

D) Economic profits equal zero.

E) Price equals average variable cost.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

67

In the long run, an industry can expand when existing firms expand by investing in new capital.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

68

In a competitive industry where the typical firm is making economic profit,

A) entry occurs as long as economic profit can be made.

B) entry occurs until supply equals demand.

C) entry occurs until price equals minimum average variable cost.

D) entry occurs until price equals marginal cost.

E) exit occurs as firms are sold to the highest bidders.

A) entry occurs as long as economic profit can be made.

B) entry occurs until supply equals demand.

C) entry occurs until price equals minimum average variable cost.

D) entry occurs until price equals marginal cost.

E) exit occurs as firms are sold to the highest bidders.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

69

Which of the following is a condition for industry expansion through expansion of existing firms instead of entry of new firms?

A) Firms take advantage of diseconomies of scale.

B) A firm size is greater than the minimum efficient sale.

C) A firm's average total cost decreases as a result of technological change.

D) A firm produces beyond the minimum long-run average total cost.

E) Firms make normal profits.

A) Firms take advantage of diseconomies of scale.

B) A firm size is greater than the minimum efficient sale.

C) A firm's average total cost decreases as a result of technological change.

D) A firm produces beyond the minimum long-run average total cost.

E) Firms make normal profits.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

70

Industry expansion cannot occur without firms entering an industry.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

71

Which of the following is false?

A) As firms exit an industry, market supply decreases.

B) As firms exit an industry, market price increases as demand increases.

C) As firms exit an industry, economic losses for the remaining firms decrease.

D) As firms exit an industry, at least some firm output increases.

E) As firms exit an industry, industry output is reduced.

A) As firms exit an industry, market supply decreases.

B) As firms exit an industry, market price increases as demand increases.

C) As firms exit an industry, economic losses for the remaining firms decrease.

D) As firms exit an industry, at least some firm output increases.

E) As firms exit an industry, industry output is reduced.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

72

Suppose a competitive industry is in long-run equilibrium. When demand increases, market price

A) decreases in the short and long run.

B) rises in the short run and falls in the long run.

C) decreases in the short run and rises in the long run.

D) rises in the short and long run.

E) rises in the short run and rises more in the long run.

A) decreases in the short and long run.

B) rises in the short run and falls in the long run.

C) decreases in the short run and rises in the long run.

D) rises in the short and long run.

E) rises in the short run and rises more in the long run.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

73

In the long run, if a firm cannot cover its costs, then the profit-maximizing firm

A) increases output and lowers price.

B) continues to produce as long as total revenue exceeds fixed costs.

C) seeks more rewarding opportunities in some other industry.

D) continues to produce so that it maximizes its opportunity costs.

E) continues to produce as long as total revenue exceeds variable costs.

A) increases output and lowers price.

B) continues to produce as long as total revenue exceeds fixed costs.

C) seeks more rewarding opportunities in some other industry.

D) continues to produce so that it maximizes its opportunity costs.

E) continues to produce as long as total revenue exceeds variable costs.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

74

A competitive firm's long-run equilibrium exists where price

A) equals MC at minimum ATC.

B) equals TR.

C) exceeds AFC.

D) equals both AVC and MC.

E) exceeds ATC.

A) equals MC at minimum ATC.

B) equals TR.

C) exceeds AFC.

D) equals both AVC and MC.

E) exceeds ATC.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

75

If market demand decreases in a market previously in long-run equilibrium,

A) the number of firms increases as each firm downsizes.

B) it is an indication that the industry has not kept up with new technology.

C) market price first rises and then falls in the movement to a new long-run equilibrium.

D) the immediate or short-run effect is a decrease in market price.

E) the industry ceases to exist.

A) the number of firms increases as each firm downsizes.

B) it is an indication that the industry has not kept up with new technology.

C) market price first rises and then falls in the movement to a new long-run equilibrium.

D) the immediate or short-run effect is a decrease in market price.

E) the industry ceases to exist.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

76

When economic losses occur in an industry,

A) the industry ceases to exist.

B) the only way the industry can change is by firms leaving it.

C) the only way the industry can change is by firms divesting themselves of capital.

D) firms in the industry may divest; others may exit the industry.

E) the industry expands with more firms.

A) the industry ceases to exist.

B) the only way the industry can change is by firms leaving it.

C) the only way the industry can change is by firms divesting themselves of capital.

D) firms in the industry may divest; others may exit the industry.

E) the industry expands with more firms.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

77

An increase in market price is likely to result in more firm entry in the long run.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

78

All else being constant, when firms leave a competitive market, then

A) market supply decreases and market price rises.

B) both market demand and market supply decrease.

C) market supply decreases and market price falls.

D) market demand decreases and market price falls.

E) market demand increases and market price rises.

A) market supply decreases and market price rises.

B) both market demand and market supply decrease.

C) market supply decreases and market price falls.

D) market demand decreases and market price falls.

E) market demand increases and market price rises.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

79

A firm earns normal profit if its total revenue is greater than its total cost.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

80

When an industry is in decline,

A) it is indicative of a weak economy.

B) it might be due to an increase in demand for the product.

C) it is common for firms to earn economic losses.

D) firm entry occurs.

E) all firms eventually leave the industry.

A) it is indicative of a weak economy.

B) it might be due to an increase in demand for the product.

C) it is common for firms to earn economic losses.

D) firm entry occurs.

E) all firms eventually leave the industry.

Unlock Deck

Unlock for access to all 139 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 139 flashcards in this deck.