Accounting for Decision Making and Control 7th Edition by Jerold Zimmerman

Edition 7ISBN: 978-0078136726Accounting for Decision Making and Control 7th Edition by Jerold Zimmerman

Edition 7ISBN: 978-0078136726 Exercise 9

PortCo Products

PortCo Products is a divisionalized furniture manufacturer. The divisions are autonomous segments, each responsible for its own sales, costs of operations, working capital management, and equipment acquisition. Each division serves a different market in the furniture industry. Because the markets and products of the divisions are so different, there have never been any transfers between divisions.

?The commercial division manufactures equipment and furniture that is purchased by the restaurant industry. The division plans to introduce a new line of counter and chair units that feature a cushioned seat for the counter chairs. John Kline, the division manager, has discussed the manufacturing of the cushioned seat with Russ Fiegel of the office division. They both believe a cushioned seat currently made by the office division for use on its deluxe office stool could be modified for use on the new counter chair. Consequently, Kline has asked Russ Fiegel for a price for 100-unit lots of the cushioned seat. The following conversation took place about the price to be charged for the cushioned seats.

FIEGEL: John, we can make the necessary modifications to the cushioned seat easily. The raw materials used in your seat are slightly different and should cost about 10 percent more than those used in our deluxe office stool. However, the labor time should be the same because the seat fabrication operation basically is the same. I would price the seat at our regular rate-full cost plus 30 percent markup.

KLINE: That's higher than I expected, Russ. I was thinking that a good price would be your variable manufacturing costs. After all, your capacity costs will be incurred regardless of this job.

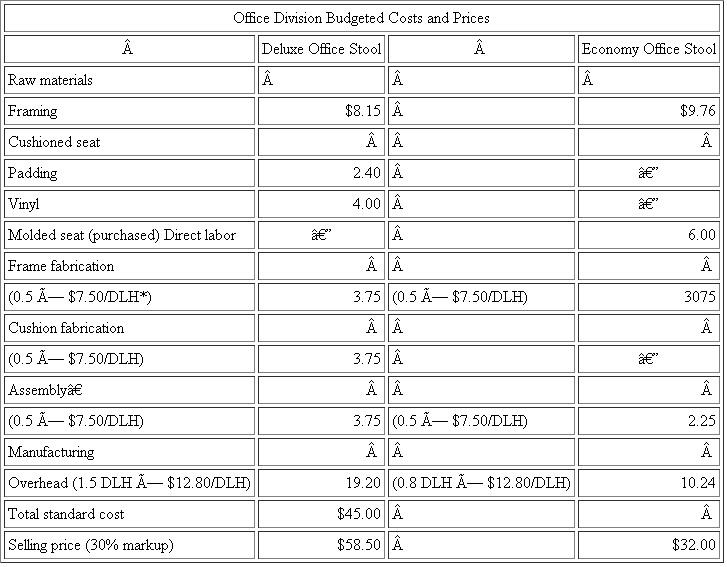

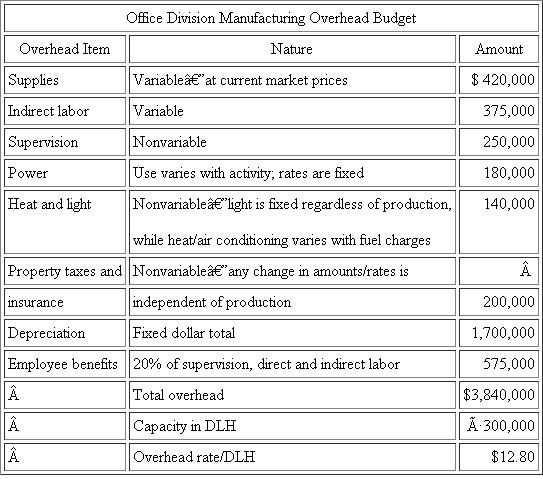

FIEGEL: John, I'm at capacity. By making the cushioned seats for you, I'll have to cut my production of deluxe office stools. Of course, I can increase my production of economy office stools. The labor time freed by not having to fabricate the frame or assemble the deluxe stool can be shifted to the frame fabrication and assembly of the economy office stool. And you will save the cost of the framing raw materials. However, I am constrained in terms of the number of hours I have for cushion fabrication. Fortunately, I can switch my labor force between these two models of stools without any loss of efficiency. As you know, overtime is not a feasible alternative in our community. I'd like to sell it to you at variable cost, but I have excess demand for both products. I don't mind changing my product mix to the economy model if I get a good return on the seats I make for you. Here are my budgeted costs for the two stools and a schedule of my manufacturing overhead (see the tables that follow).

KLINE: I guess I see your point, Russ, but I don't want to price myself out of the market. Maybe we should talk to corporate to see if they can give us any guidance. *Direct labor hours.

*Direct labor hours.

†Attaching seats to frames and attaching rubber feet. Required:

Required:

a. John Kline and Russ Fiegel ask PortCo corporate management for guidance on an appropriate transfer price. Corporate management suggests they consider using a transfer price based upon opportunity cost. Calculate a transfer price for the cushioned seat based upon variable manufacturing cost plus forgone profits.

b. Which alternative transfer price system-full cost, variable manufacturing cost, or opportunity cost-would be better as the underlying concept for an intracompany transfer price policy? Explain your answer.

PortCo Products is a divisionalized furniture manufacturer. The divisions are autonomous segments, each responsible for its own sales, costs of operations, working capital management, and equipment acquisition. Each division serves a different market in the furniture industry. Because the markets and products of the divisions are so different, there have never been any transfers between divisions.

?The commercial division manufactures equipment and furniture that is purchased by the restaurant industry. The division plans to introduce a new line of counter and chair units that feature a cushioned seat for the counter chairs. John Kline, the division manager, has discussed the manufacturing of the cushioned seat with Russ Fiegel of the office division. They both believe a cushioned seat currently made by the office division for use on its deluxe office stool could be modified for use on the new counter chair. Consequently, Kline has asked Russ Fiegel for a price for 100-unit lots of the cushioned seat. The following conversation took place about the price to be charged for the cushioned seats.

FIEGEL: John, we can make the necessary modifications to the cushioned seat easily. The raw materials used in your seat are slightly different and should cost about 10 percent more than those used in our deluxe office stool. However, the labor time should be the same because the seat fabrication operation basically is the same. I would price the seat at our regular rate-full cost plus 30 percent markup.

KLINE: That's higher than I expected, Russ. I was thinking that a good price would be your variable manufacturing costs. After all, your capacity costs will be incurred regardless of this job.

FIEGEL: John, I'm at capacity. By making the cushioned seats for you, I'll have to cut my production of deluxe office stools. Of course, I can increase my production of economy office stools. The labor time freed by not having to fabricate the frame or assemble the deluxe stool can be shifted to the frame fabrication and assembly of the economy office stool. And you will save the cost of the framing raw materials. However, I am constrained in terms of the number of hours I have for cushion fabrication. Fortunately, I can switch my labor force between these two models of stools without any loss of efficiency. As you know, overtime is not a feasible alternative in our community. I'd like to sell it to you at variable cost, but I have excess demand for both products. I don't mind changing my product mix to the economy model if I get a good return on the seats I make for you. Here are my budgeted costs for the two stools and a schedule of my manufacturing overhead (see the tables that follow).

KLINE: I guess I see your point, Russ, but I don't want to price myself out of the market. Maybe we should talk to corporate to see if they can give us any guidance.

*Direct labor hours.†Attaching seats to frames and attaching rubber feet.

Required: a. John Kline and Russ Fiegel ask PortCo corporate management for guidance on an appropriate transfer price. Corporate management suggests they consider using a transfer price based upon opportunity cost. Calculate a transfer price for the cushioned seat based upon variable manufacturing cost plus forgone profits.

b. Which alternative transfer price system-full cost, variable manufacturing cost, or opportunity cost-would be better as the underlying concept for an intracompany transfer price policy? Explain your answer.

Explanation Verified

Verified

This is a good review problem to assign ...

Accounting for Decision Making and Control 7th Edition by Jerold Zimmerman

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255