Accounting for Decision Making and Control 7th Edition by Jerold Zimmerman

Edition 7ISBN: 978-0078136726Accounting for Decision Making and Control 7th Edition by Jerold Zimmerman

Edition 7ISBN: 978-0078136726 Exercise 2

Wellington Co.

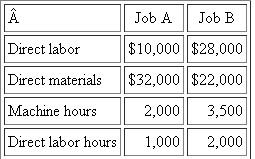

The following figures were taken from the records of Wellington Co. for the year 2008. At the end of the year, two jobs were still in process. Details about the two jobs include: ?Wellington Co. applies overhead at a budgeted rate, calculated at the beginning of the year. The budgeted rate is the ratio of budgeted overhead to budgeted direct labor costs. Budgeted figures for 2008 were

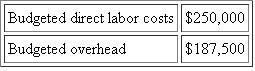

?Wellington Co. applies overhead at a budgeted rate, calculated at the beginning of the year. The budgeted rate is the ratio of budgeted overhead to budgeted direct labor costs. Budgeted figures for 2008 were  Actual figures for 2008 were

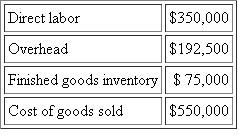

Actual figures for 2008 were  ?There were no opening inventories. It is the practice of the company to prorate any over/ underabsorption of overhead to finished goods inventory, work in process, and cost of goods sold based on the total dollars in these categories.

?There were no opening inventories. It is the practice of the company to prorate any over/ underabsorption of overhead to finished goods inventory, work in process, and cost of goods sold based on the total dollars in these categories.

Required :

a. Compute the cost of work in process before over/underapplied overheads are prorated.

b. Prepare a schedule of finished goods inventory, work in process, and cost of goods sold after over/underapplied overheads are prorated.

c. What is the difference in operating income if the over/underapplied overhead is charged to cost of goods sold instead of being prorated to finished goods inventory, work in process, and cost of goods sold?

The following figures were taken from the records of Wellington Co. for the year 2008. At the end of the year, two jobs were still in process. Details about the two jobs include:

?Wellington Co. applies overhead at a budgeted rate, calculated at the beginning of the year. The budgeted rate is the ratio of budgeted overhead to budgeted direct labor costs. Budgeted figures for 2008 were Actual figures for 2008 were ?There were no opening inventories. It is the practice of the company to prorate any over/ underabsorption of overhead to finished goods inventory, work in process, and cost of goods sold based on the total dollars in these categories.Required :

a. Compute the cost of work in process before over/underapplied overheads are prorated.

b. Prepare a schedule of finished goods inventory, work in process, and cost of goods sold after over/underapplied overheads are prorated.

c. What is the difference in operating income if the over/underapplied overhead is charged to cost of goods sold instead of being prorated to finished goods inventory, work in process, and cost of goods sold?

Explanation Verified

Verified

Absorption costing

Absorption costing i...

Accounting for Decision Making and Control 7th Edition by Jerold Zimmerman

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255