Accounting for Decision Making and Control 8th Edition by Jerold Zimmerman

Edition 8ISBN: 978-0078025747Accounting for Decision Making and Control 8th Edition by Jerold Zimmerman

Edition 8ISBN: 978-0078025747 Exercise 11

Economic Earnings

A large consulting firm is looking to expand the services currently offered its clients. The firm has developed a new performance metric called "Economic Earnings," or EE for short. The performance metric is argued to be a better measure of both divisional performance and firmwide performance, and hence "a more rational platform for compensating employees and managers." The consulting firm is seeking to convince clients they should replace their current metrics, such as accounting net income, ROA, EVA, and so forth, with EE.

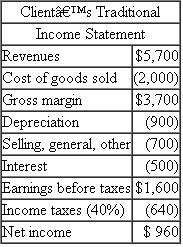

EE starts with traditional accounting net income but then makes a series of adjustments. The primary adjustment is to add back depreciation and then subtract a required return on invested capital. The consultants argue for adding accounting depreciation back because it is a sunk cost. It does not represent a current cash flow. For example, suppose a client has accounting net income calculated as:

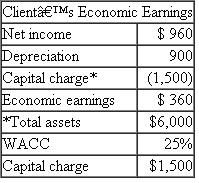

Suppose the client has total assets of $6,000 and a risk-adjusted weighted-average cost of capital (WACC) of 25 percent. Then this client's EE is calculated as follows:

Suppose the client has total assets of $6,000 and a risk-adjusted weighted-average cost of capital (WACC) of 25 percent. Then this client's EE is calculated as follows:

Required:

Required:

Critically evaluate EE as a performance measure. What are its strengths and weaknesses?

A large consulting firm is looking to expand the services currently offered its clients. The firm has developed a new performance metric called "Economic Earnings," or EE for short. The performance metric is argued to be a better measure of both divisional performance and firmwide performance, and hence "a more rational platform for compensating employees and managers." The consulting firm is seeking to convince clients they should replace their current metrics, such as accounting net income, ROA, EVA, and so forth, with EE.

EE starts with traditional accounting net income but then makes a series of adjustments. The primary adjustment is to add back depreciation and then subtract a required return on invested capital. The consultants argue for adding accounting depreciation back because it is a sunk cost. It does not represent a current cash flow. For example, suppose a client has accounting net income calculated as:

Suppose the client has total assets of $6,000 and a risk-adjusted weighted-average cost of capital (WACC) of 25 percent. Then this client's EE is calculated as follows: Required: Critically evaluate EE as a performance measure. What are its strengths and weaknesses?

Explanation Verified

Verified

Net Income:

The resultant amount after ...

Accounting for Decision Making and Control 8th Edition by Jerold Zimmerman

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255