Accounting for Decision Making and Control 8th Edition by Jerold Zimmerman

Edition 8ISBN: 978-0078025747Accounting for Decision Making and Control 8th Edition by Jerold Zimmerman

Edition 8ISBN: 978-0078025747 Exercise 15

Winterton Group

The Winterton Group is an investment advisory firm specializing in high-income investors in upstate New York. Winterton has offices in Rochester, Syracuse, and Buffalo. Operating as a profit center, each office receives central services, including information technology, marketing, accounting, and payroll. Winterton has 20 investment advisors, 7 each in Syracuse and Rochester, and 6 in Buffalo. Each investment advisor is paid a fixed salary, a commission based on the revenue generated from clients, plus 2 percent of regional office profits and 1 percent of firm profits. One of the senior investment advisors in each office is designated as the office manager and is responsible for running the office. The office manager receives 8 percent of the regional office profits instead of 2 percent.

Regional office expenses include commissions paid to investment advisors. The following regional profits are calculated before the 2 percent profit sharing. Firm profits are the sum of the three regional office profits.

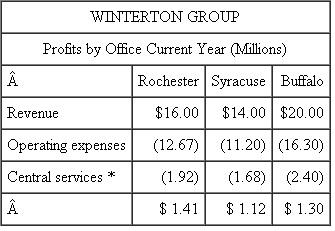

This table summarizes the current profits per office after allocating central service costs based on office revenues.

*Allocated on the basis of revenue.

*Allocated on the basis of revenue.

The manager of the Buffalo office sent the following e-mail to the other office managers, the president, and the chief financial officer:

One of the primary criteria by which all cost allocation schemes are to be judged is fairness. The costs allocated to those bearing them should view the system as fair. Our current system, which allocates central services using office revenues, fails this important test of fairness. Receiving more allocated costs penalizes those offices generating more revenues. A fairer, and hence more defensible, system would be to allocate these central services based on the number of investment advisors in each office.

Required:

a. Recalculate each office's profits before any profit sharing assuming the Buffalo manager's proposal is adopted.

b. Do you believe the Buffalo manager's proposal results in a fairer allocation scheme than the current one? Why or why not?

c. Why is the Buffalo manager concerned about fairness?

The Winterton Group is an investment advisory firm specializing in high-income investors in upstate New York. Winterton has offices in Rochester, Syracuse, and Buffalo. Operating as a profit center, each office receives central services, including information technology, marketing, accounting, and payroll. Winterton has 20 investment advisors, 7 each in Syracuse and Rochester, and 6 in Buffalo. Each investment advisor is paid a fixed salary, a commission based on the revenue generated from clients, plus 2 percent of regional office profits and 1 percent of firm profits. One of the senior investment advisors in each office is designated as the office manager and is responsible for running the office. The office manager receives 8 percent of the regional office profits instead of 2 percent.

Regional office expenses include commissions paid to investment advisors. The following regional profits are calculated before the 2 percent profit sharing. Firm profits are the sum of the three regional office profits.

This table summarizes the current profits per office after allocating central service costs based on office revenues.

*Allocated on the basis of revenue.The manager of the Buffalo office sent the following e-mail to the other office managers, the president, and the chief financial officer:

One of the primary criteria by which all cost allocation schemes are to be judged is fairness. The costs allocated to those bearing them should view the system as fair. Our current system, which allocates central services using office revenues, fails this important test of fairness. Receiving more allocated costs penalizes those offices generating more revenues. A fairer, and hence more defensible, system would be to allocate these central services based on the number of investment advisors in each office.

Required:

a. Recalculate each office's profits before any profit sharing assuming the Buffalo manager's proposal is adopted.

b. Do you believe the Buffalo manager's proposal results in a fairer allocation scheme than the current one? Why or why not?

c. Why is the Buffalo manager concerned about fairness?

Explanation Verified

Verified

Operating Income

It is also known as Re...

Accounting for Decision Making and Control 8th Edition by Jerold Zimmerman

Why don’t you like this exercise?

Other Minimum 8 character and maximum 255 character

Character 255